How Much Does It Cost To Start A Bail Bond Business: $275K Plan

Bail Bond Service

In this researched planning model, opening a bail bond company is not a $23,000 office project plan around $275,000 of Year 1 launch financing capacity before state-specific licensing, surety collateral, and forfeiture reserves are finalized Visible startup costs include at least $15,000 for office furnishings and $8,000 for security and surveillance, plus $9,350 per month in fixed overhead and about $16,667 per month for the initial three-person payroll The model also carries a $50,000 surety line, $20,000 credit line, $15,000 equipment loan, and $40,000 facility loan as funding assumptions, not universal requirements Treat these as researched assumptions, not vendor quotes, legal advice, or guaranteed state rules

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates startup capitalized assets before launch, not operating cash needs.

!

What this excludes This calculator covers startup CAPEX only. It excludes licensing, insurance, payroll runway, marketing, surety collateral, working capital, debt service, deposits, inventory runway, and forfeiture reserves.

How much collateral does a bail bond company need?

There’s no single national collateral rule for a Bail Bond Service; treat collateral as a funding variable tied to state rules, surety underwriting, credit, experience, and bond-writing limits. A common planning model starts with $50,000 cash collateral in Year 1 plus a $50,000 surety line, then scales to $100,000 in Year 2 and $500,000 by Year 5. Keep a forfeiture reserve too, because one missed court appearance can create cash pressure fast. Verify state and surety requirements before you write any bonds.

What drives collateral

State rules set the floor.

Surety appointment controls access.

Credit and experience shape limits.

Indemnity agreements back the risk.

How to plan cash

Start with $50,000 cash collateral.

Add a $50,000 surety line.

Build to $100,000 in Year 2.

Target $500,000 by Year 5.

How to fund a bail bond business?

If you’re funding a Bail Bond Service, don’t stop at startup cost; lenders and sureties want a cash flow plan that shows bond volume, 10% premium income, interest assumptions, forfeiture risk, collections, payroll, marketing, and reserve needs. With $275,000 in Year 1 debt capacity, $405,000 in first-year bond and loan balances, $100,000 in interest-earning assets, and $51,550 in estimated Year 1 interest income, the model has to prove repayment capacity and show when a surety line or credit line will be used. The key question is simple: can monthly premiums and collections cover operating cash gaps before the reserve is hit?

Funding plan

Model monthly bond volume first.

Apply the 10% premium rate.

Include forfeiture risk in cash needs.

Match debt repayment to premium timing.

Cash flow checks

Track payroll and marketing monthly.

Set reserve cash before approval.

Use the surety line only when needed.

Map credit line timing and gaps.

What hidden costs of starting a bail bond business should founders model?

Model the hidden costs as reserves and timing cushions, not one-time office buys: forfeiture exposure, bail recovery, 24/7 phone coverage, skip tracing, compliance renewals, payment delays, software onboarding, professional fees, and early payroll. If you need the planning frame, see How Do I Write A Bail Bond Service Business Plan?

Here’s the quick math: the source model assumes 50% bail recovery costs in Year 1, 200% surety premium share in Year 1, $350 per month for case management software, $200 per month for licensing maintenance, and $65,000 a year for night shift agent payroll. One clean rule: if cash timing is tight, these costs hit before the fee does.

Core reserve items

Forfeiture exposure can drain cash fast

Bail recovery is a real operating cost

Skip tracing adds variable spend

24/7 coverage needs paid staff

Timing and fixed monthly costs

$350 monthly case software

$200 monthly licensing maintenance

$65,000 annual night shift payroll

Payment delays slow cash in

Calculate Fuding Needs

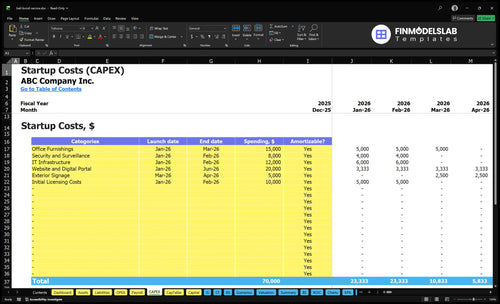

Startup cost summary

This table summarizes launch CAPEX and excluded cash needs for a licensed bail bond service.

Highlighted CAPEX$65,000Base planning example

Excluded cash needs$49,493Outside CAPEX total

Funding need$114,493CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Office Furnishings

$15,000

Reception, desks, seating, and storage

Yes

Security and Surveillance

$8,000

Cameras, alarms, and monitored access

Yes

IT Infrastructure

$12,000

Computers, networking, and case systems

Yes

Website and Digital Portal

$20,000

Client intake, forms, and online access

Yes

Initial Licensing Costs

$10,000

State licensing, approvals, and compliance setup

Yes

Operating Reserve

$49,493

Minimum cash, opening payroll, and launch cushion

No

Bail Bond Service Core Five Startup Costs

Licensing, Training, and Compliance Startup Expense

License Costs

Start with the known $200 per month licensing maintenance fee, then add state application, pre-licensing education, exam, background check, agency registration, renewals, and regulator filing costs. Requirements vary by state, so verify each fee with the relevant insurance department, court authority, or licensing regulator before you budget.

Budget Range

Use low, base, and high fields so you can separate known monthly maintenance from unknown state charges. The model gives only the $200/month maintenance input, so the other fields should come from quotes and official rules for renewals, document retention, and continuing compliance.

Low: minimum required filings

Base:$200/month maintenance

High: education and renewal load

Reduce Waste

Buy only the state-required training, file on time, and keep one compliance calendar for renewals and document retention. Don’t skip exams or background checks to save a little cash; delays and rework usually cost more than the fee itself. One clean filing beats three rushed ones.

Verify the checklist before paying

Track every renewal date

Store filings in one system

Compliance Load

Set one owner for filings, continuing education, and recordkeeping, because the risk is lost authority to write bonds if a deadline slips. Recheck the rule set before launch and at each renewal cycle, since state requirements can change and some regulators want extra proof on file.

Surety Appointment, Collateral, and Reserve Startup Expense

Surety Access

Treat this as working capital, not CAPEX. The cost includes surety company approval, indemnity agreements, collateral, a build-up fund, reserve account, bond limits, and a forfeiture reserve for early losses. The source model uses a $50,000 surety line, $50,000 collateral cash, 900% Year 1, and 200% surety premium share in Year 1.

Collateral Cash

Budget the cash you must park, not just the fee you pay. The model ties up $50,000 in collateral cash and a surety line of $50,000. That cash earns 40% in the model, but it is still restricted and may not be free for payroll or marketing.

Verify state filing rules

Match bond limits first

Separate reserve cash

Reduce The Drag

Terms change by state rules, the surety partner, credit, experience, and bond volume. To reduce the hit, ask for the smallest line that matches first-month volume, keep claims clean, and separate operating cash from reserve cash. If onboarding drags, the collateral can strain working capital fast.

Start with lower bond limits

Track losses weekly

Keep reserve accounts separate

Loss Reserve

Watch early loss exposure closely. A forfeiture reserve should sit beside the collateral so one bad bond does not hit rent or payroll. If the agency is new, treat the surety appointment as a gating item: no appointment, no bond capacity, no revenue.

Office Setup and Equipment Startup Expense

Office Lease

The courthouse-area office starts with $4,500 monthly rent, plus rent deposits and any pre-opening occupancy costs tied to the lease. Budget for the first months of rent before revenue starts, and keep utilities and security at $600 monthly separate from the lease. One clean rule: lease cash is not equipment cash.

Furniture and Fixtures

The model shows $15,000 for office furnishings, which should cover desks, chairs, printers, secure file storage, signage, and the waiting area setup. Add basic buildout only if the space needs tenant work before opening. IT infrastructure is an input field here, since no amount is provided.

Security Setup

$8,000 is listed for security and surveillance, so treat cameras, access control, and other protection gear as a separate fixed asset from rent deposits and occupancy costs. That split matters because it affects depreciation and startup cash. If the office handles sensitive files and after-hours traffic, don’t trim this line just to save a few dollars.

Keep Costs Tightly Split

Here’s the quick math: office setup cash is a mix of recurring rent, one-time furnishings, and security assets. Keep monthly rent, pre-opening deposits, and depreciable items on different lines, so you can see what burns cash now and what lasts. That makes lender talks, tax tracking, and opening-week spending much cleaner.

Technology and Communications Startup Expense

Core Tech Stack

Technology spend should cover case management software, online intake, electronic signature (e-signature), payment processing setup, customer relationship management (CRM), mobile phones, call forwarding, website hosting, and skip-tracing subscriptions. Split it into one-time setup and monthly software as a service. The model already shows $350 a month for case management software.

Budget Split

Price the stack as setup plus monthly run rate. One-time items usually include implementation and account setup; monthly items include phone service, hosting, processing, and software. The model also carries $2,500 monthly for marketing and local SEO, so the launch budget needs both software and lead flow.

Separate setup fees from subscriptions.

Quote phone lines and hosting monthly.

Track processor fees before launch.

Keep It Lean

Keep quality high by buying only the tools that support fast intake and round-the-clock response. Skip duplicate systems, use one phone platform, and confirm whether e-signature and CRM are bundled. The mistake to avoid is pricing software without the staffing and call coverage to use it, because missed calls can mean missed cases.

24/7 Coverage

For a bail bond agency, 24/7 response is part of the communications budget. Call forwarding, mobile phones, and live answer coverage matter because a single missed call can mean a lost bond. Build the plan around night, weekend, and courthouse-hours coverage, then size phone and staffing costs to match that response window.

Insurance, Marketing, Payroll, and Launch Cushion Startup Expense

Coverage costs

Insurance, legal help, and launch cash sit in this bucket. The model includes $1,200 per month for professional liability insurance, plus attorney and accountant support, website, local SEO, permitted jail-area marketing, and the first payroll. If you need general business insurance or contractor coverage, price those separately by quote and month of coverage.

Payroll base

Payroll is the biggest opening hit. The source model lists $85,000 for a principal agent, $65,000 for a night shift agent, and $50,000 for an office manager. That equals about $16,667 in opening-month payroll before taxes and benefits. Build this from annual salary ÷ 12, then add payroll taxes and benefits.

Split salary from taxes.

Model each role separately.

Keep coverage for first month.

Marketing rules

Marketing is not free if it breaks the rules. The model uses $2,500 per month for marketing and local SEO, but referral and jail-area outreach must follow state law and court rules. Use exact quotes for ad spend, website work, and local search. If a tactic can’t be documented, don’t budget it.

Use written ad approvals.

Track every referral source.

Avoid banned solicitation.

Launch cushion

The cushion keeps you open before collections settle. Fund at least one month of payroll, insurance, and marketing, then add room for attorney and accountant work, contractor coverage, and payment timing gaps. Here’s the quick math: $16,667 payroll + $1,200 insurance + $2,500 marketing, before any taxes, benefits, or other bills.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Bail bond launch costs move with staffing, office footprint, software, and reserve depth. Lean suits a single-agent start, while Full fits a multi-agent agency with wider coverage.

Lean, Base, and Full launch comparison

Scenario

Lean LaunchLower cash need

Base LaunchModeled setup

Full LaunchHigher reserve need

Launch model

Start with a single-agent or owner-led office and keep coverage tight.

Use the source model's core setup with steady coverage and standard reserves.

Build for deeper reserves, wider 24/7 staffing, and stronger reach.

Typical setup

Use a smaller office, limited software, and lighter marketing.

Plan for $23,000 known CAPEX, $9,350 monthly fixed overhead, $16,667 opening-month payroll, a $50,000 surety line, and $275,000 Year 1 debt capacity.

Add more staff, stronger software, heavier local SEO, and larger surety capacity.

Cost drivers

Smaller office

owner-led coverage

limited software

thinner marketing

lower reserves

Core CAPEX

monthly overhead

opening payroll

surety line

debt capacity

Deeper reserves

24/7 staffing

stronger software

heavier SEO

larger surety capacity

Planning rangeCAPEX only

$75,000 - $125,000Tight setup

$150,000 - $275,000Core plan

$300,000 - $500,000Aggressive build

Best fit

Best for a single-agent or courthouse office in a state with lighter surety needs.

Best for a single-agent or small courthouse office that wants the model's standard launch shape.

Best for a multi-agent agency in a state with tighter licensing, higher surety limits, or heavier call volume.

!

Planning note: These ranges are researched planning assumptions, not exact quotes. State rules, surety access, and staffing needs can shift the final number.

In this model, plan around $275,000 of Year 1 launch financing capacity, not just the office setup Known CAPEX includes $15,000 for furnishings and $8,000 for security and surveillance The opening-month run-rate is about $26,017 before variable costs, based on $9,350 fixed overhead and about $16,667 payroll

The data does not provide a break-even month, so do not force one The first year carries $200,000 of annual payroll, $112,200 of fixed overhead, 200% surety premium share, and 50% recovery costs You need a full cash flow forecast tied to bond volume, collections, reserves, and forfeiture timing

Yes, insurance should be modeled before opening, but exact requirements vary by state and policy type This plan includes professional liability insurance at $1,200 per month, or $14,400 for the first year You may also need other business coverage, but those costs are not specified in the provided model

Maybe, but state licensing, court access, records rules, and surety requirements drive that decision The base model assumes a courthouse office at $4,500 per month, plus $600 for utilities and security A home-office version may lower rent, but it still needs 24/7 phone coverage, secure files, software, and compliant marketing

Model surety costs as both operating expense and funding capacity This plan includes a $50,000 surety line at 900% interest in Year 1, plus a 200% surety premium share Also model collateral cash, forfeiture reserves, bond limits, and recovery costs, because those items affect cash long before they look like profit

About the author

Edward Fisher

Practical Business Analyst

Edward Fisher is a practical business analyst at Financial Models Lab, focused on small business budgeting and estimating what service businesses can realistically earn. He writes break-even explanations and other planning content for founders who want optimistic growth ideas grounded in realistic assumptions and cost-aware decision-making.

Choosing a selection results in a full page refresh.