How Much Does an After-School Program Owner Make? $365K Year 1

Key Takeaways

Filling paid slots drives revenue faster than costs rise.

Tuition mix lifts revenue per child and margin.

Payroll control can make or break profit.

Fixed space costs set the enrollment break-even floor.

Owner income$365K–$3.95MNet margin46%–80%Revenue for target pay$790K–$4.94MBusiness difficultyHard

Want to test your after-school program owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and your pay goal.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to see owner income in the After-School Program model?

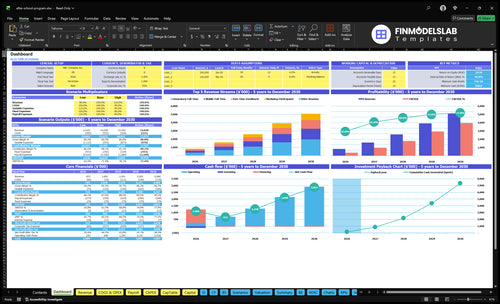

This dashboard in the After-School Program Financial Model Template ties enrollment, tuition, payroll, fixed costs, capex, EBITDA, and owner income into one view, with low/base/high scenarios and core tabs for assumptions, revenue build, staffing, operating expenses, startup costs, cash flow, and charts. Clarity, not guaranteed earnings.

Owner-income model highlights

Year 1 EBITDA: $365K

Year 5 EBITDA: $3951M

Payroll: $236K to $437K

Fixed overhead: $6,850/month

How many kids does an after-school program need to make money?

An After-School Program does not have one universal break-even child count, because tuition can range from $100 to $550 a month. In the modeled case, it reaches break-even in Month 1 at 50% occupancy on 75 slots, or about 38 paid participants, with $6,850 in monthly fixed overhead before payroll. Payroll is the real hurdle: $236K in Year 1, so the tuition mix and staff-child ratios drive the math.

Break-even drivers

38 paid kids can hit break-even.

50% occupancy means 75 slots.

$6,850 monthly overhead comes first.

Tuition mix changes the child count.

Profit pressure points

$236K Year 1 payroll is the hurdle.

Elementary, middle, part-time, and workshops differ.

$100 to $550 pricing changes enrollment needs.

Reserve needs can raise the target.

How do staffing costs affect after-school program profit?

If staffing runs ahead of attendance, an After-School Program loses margin fast. Payroll rises from $236K in Year 1 to $437K in Year 5, and the How Much Does It Cost To Open, Start, Launch Your After-School Program Business? setup page shows why labor needs tight control from day one. The Program Director stays at $65K, while Certified Educator FTEs grow from 20 to 40 and Program Assistant FTEs from 10 to 30.

Payroll drives profit

$236K Year 1 payroll

$437K Year 5 payroll

20 to 40 educator FTEs

10 to 30 assistant FTEs

Protect owner take-home

Match shifts to attendance

Plan substitutes before gaps hit

Keep admin lean early

Protect safety and compliance

Can a single after-school program support a full-time owner?

Yes, the modeled After-School Program can support a full-time owner if the owner serves as Program Director at a modeled $65K salary and the site holds its economics. For deeper tracking, start with What Is The Most Important Measure Of Success For Your After-School Program?, because the answer depends on paid enrollment, tuition, staffing, and facility costs working together.

Modeled Case

75 slots modeled in Year 1

50% occupancy in the base case

$100-$450 monthly tuition range

$365K EBITDA before owner distributions

Owner Test

$236K payroll must stay controlled

$822K fixed overhead needs coverage

Reserve for taxes, debt, and capex

Add sites after repeatable collections

After-School Program Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main after-school program income drivers?

1

Enrollment Utilization

50%-90%

Higher occupancy raises take-home fastest because each filled seat spreads fixed costs across more tuition, so low fill is the main risk; keep referrals and retention front and center.

2

Tuition Mix

$350-$420

Higher monthly tuition lifts revenue per child right away, so pricing discipline matters once seats fill; avoid discounting unless it clearly improves retention.

3

Staffing Efficiency

$236K-$437K

Payroll swings a lot as FTEs rise, so hiring too early can crush margin; tie staff hours to enrollment blocks and daily attendance.

4

Facility Costs

$6.85K/mo

Lease, utilities, insurance, and cleaning are fixed, so they hit hardest when occupancy is light; keep the space and service plan lean.

5

Holiday Add-Ons

$15K-$35K

Holiday camp fees add extra cash with limited fixed cost, so pre-sell break weeks and fill them before spending more on ads.

6

Owner Overhead

$65K

The $65K Program Director role protects quality, but owner cash falls if admin work and overhead stack up; keep leadership duties tight and separate.

After-School Program Core Six Income Drivers

Capacity Utilization And Paid Enrollment

Paid Enrollment Utilization

Capacity utilization is the share of slots that are paid and attended. In Year 1, the model uses 75 slots at 50% occupancy, so only about 38 slots are billed. By Year 5, 120 slots at 90% occupancy means 108 paid slots. That lift raises revenue faster than fixed costs, so the owner’s draw improves as enrollment fills.

Here’s the quick math: 10 more full-time elementary children at $450/month adds $4,500 in monthly revenue before added labor. What this hides is staffing pressure. Ratios, licensing, and pickup coverage can force payroll up before every seat is full, so profit depends on paid attendance, not just signups.

Track Paid Seats, Not Just Leads

Measure enrolled seats, paid seats, attendance consistency, collections, and waitlist depth each month. If collections slip or families miss days often, cash flow drops even when the roster looks full. A full-fee seat that is actually paid and used is what funds payroll, rent, and owner pay.

Track paid occupancy weekly.

Watch no-show and late-pay rates.

Keep a waitlist ready.

Use fill-rate targets to time hiring. If staffing steps up too early, margin gets squeezed; if staffing lags, licensing and safety can block growth. The goal is simple: fill seats with consistent, paying families before adding more labor.

1

Revenue Per Child

Revenue per child

Revenue per child is the tuition mix across full-time elementary, full-time middle, part-time, and workshops. Year 1 pricing is $450, $400, $250, and $100; Year 5 rises to $550, $500, $320, and $130. That lifts weighted tuition from about $350 to $420 a month before Holiday Camp Fees, a $70 gain per child.

That matters because higher tuition per child can cover fixed payroll and rent faster and improve cash for owner pay. But the realized number can drop if sibling discounts, subsidies, registration fees, or late-pickup fees change what families actually pay. One clean line: price only helps if families still enroll and keep paying.

Track realized tuition, not sticker price

Measure monthly revenue per enrolled child by tier, then compare it to the weighted target of $350 in Year 1 and $420 in Year 5. Split out tuition, registration fees, subsidies, discount leakage, and late-pickup fees so you can see what is really driving cash and margin.

Track mix by age group

Log every discount and subsidy

Test price changes by cohort

If a higher price weakens demand, occupancy and cash flow can fall faster than revenue per child rises. Watch retention after each price change and document which fees parents accept without pushing churn.

2

Staffing Efficiency And Payroll Control

Staffing Efficiency And Payroll Control

Payroll is the main margin swing factor. Part-time shifts, director coverage, driver schedules, training time, and substitute use all hit take-home income fast. In the model, payroll totals $236K in Year 1, $2,849K in Year 2, $346K in Year 3, $3,931K in Year 4, and $437K in Year 5, so small schedule changes can move profit more than price changes.

If educator FTEs are added before occupancy catches up, labor costs rise before tuition does and margin compresses. Do not cut below licensing, safety, or quality needs; the goal is lean coverage, not understaffing. The owner’s income depends on keeping the staff mix tight while still covering ratios, openings, and training.

Track Payroll Before You Add Headcount

Track payroll per enrolled child, payroll as a percent of tuition, substitute hours, and training hours by week. Here’s the quick math: if enrollment is flat and paid hours rise, cash for owner pay falls first. Keep a simple rule for new hires tied to occupancy, attendance, and waitlist depth.

Watch payroll per child

Cap substitute drift

Stagger part-time shifts

Protect required ratios

Test coverage changes before locking in another FTE. One clean rule works: no permanent staff add unless occupancy and attendance can support it for several weeks. That keeps payroll aligned with real demand instead of hopeful demand.

3

Facility Cost Structure

Facility Cost Load

If the space bill is too high, the program needs more enrolled children just to stay even. Here the fixed monthly load is $3,500 lease, $800 utilities, $600 cleaning, and $300 business insurance, for $6,850/month before payroll and owner pay.

Here’s the quick math: at 38 paid participants, rent alone is about $92 per participant per month ($3,500 ÷ 38). A lower-overhead school, church, or community center can reduce break-even pressure, but cheap space still fails if capacity is tight or transportation makes pickup hard.

Cut the Space Burden

Track fixed cost per paid child each month, not just total rent. The right input set is paid enrollment, room capacity, commute ease, and total space cost. When occupancy is soft, every extra dollar of fixed overhead hits profit hard and delays owner draw.

Test sites by asking one question: can the current enrollment cover $6,850 without pushing tuition too high? If not, use a cheaper site or a shared facility, but only if it still supports safe pickup, enough room, and steady attendance.

Calculate cost per paid seat monthly.

Compare lease, church, and school space.

Watch attendance, not just signups.

Check pickup flow and parking.

4

Calendar And Add-On Revenue

Add-On Calendar Revenue

Extra care days add revenue beyond regular tuition when families pay for early release days, school breaks, workshops, and summer bridge programs. Billable days move from 20/month in Year 1 to 22/month in Year 5, a 10% lift in billable days, while Holiday Camp Fees rise from $15K to $35K.

That only helps owner pay if demand is real and the schedule is tight. What this hides: every added day also brings staffing, supplies, snacks, and vehicle costs, so unused slots can raise revenue on paper but still cut cash profit.

Track Bookings Before Adding Days

Measure booked seats, attendance, and incremental cost per event before you open a camp or workshop. If extra revenue does not cover added labor and direct costs, the owner’s draw gets squeezed even when sales rise.

Track fill rate by date.

Price each add-on separately.

Staff only after sign-ups land.

Watch cash outlays before billing clears.

5

Owner Role, Overhead, And Reserves

Owner Pay, Overhead, and Reserves

When the owner steps in as Program Director, payroll shifts from owner draw to salary, with a $65,000 annual salary tied to that role. Add administrative staff rising from 05 FTE to 10 FTE and $1,550/month for software, accounting, legal, professional development, and cleaning, and fixed overhead climbs fast. That lowers what can be paid out to the owner, even if enrollment stays solid.

EBITDA is not cash for owner draw. A reserve policy can keep cash back for taxes, payroll timing, and slow collections, so take-home can drop even when EBITDA is positive. An owner-operator can cut early admin load, but that can cap growth once the program needs more coverage and control.

Track Draw Capacity

Measure the gap between owner labor and hired labor, then test whether the owner should stay in the director seat or move into a lighter role. Track the items that change cash first:

Director salary versus draw

Admin FTE by month

$1,550/month overhead

Reserve target

EBITDA versus free cash

Set the reserve rule before raising owner pay. If admin needs keep rising, hire sooner or slow expansion, because weak staffing can protect cash in the short run but hurt service quality and future income.

6

After-School Program Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high after-school program income scenarios

Owner income scenarios

Owner income shifts fast as occupancy, pricing, staffing, and reserves change. The gap between ramp-up, stable site, and mature site is wide in this model.

Low, base, and high cases show how earnings change as the program fills up.

Scenario

Low CaseRamp-up

Base CaseStable site

High CaseMature site

Launch model

This is the lower earnings path while the site ramps up.

This is the modeled middle path once the site is stable.

This is the stronger earnings path at a mature site.

Typical setup

Assumes 50% occupancy, Year 1 pricing, $236k payroll, and $6,850 monthly fixed costs, with EBITDA at about $365k before reserves.

Assumes 75% occupancy, Year 3 pricing, $346k payroll, and a more settled cost base, with EBITDA around $1.782m.

Assumes 90% occupancy, Year 5 pricing, $437k payroll, and fuller utilization, with EBITDA near $3.951m.

Cost drivers

50% occupancy

Year 1 pricing

$236k payroll

$6,850 monthly fixed costs

reserves drag

75% occupancy

Year 3 pricing

$346k payroll

stable staffing

add-on income

90% occupancy

Year 5 pricing

$437k payroll

fuller utilization

add-on fees

Owner income rangeBefore owner reserves

$365kRamp-up income

$1.782mStable site income

$3.951mMature site income

Best fit

Use this to stress-test the first operating year and a slower fill rate.

Use this for the core operating plan and lender or investor discussions.

Use this to test upside from a nearly full program and higher pricing power.

!

Planning note: Scenario values are researched planning assumptions from the model. They are not guaranteed earnings, salary promises, tax advice, or distribution targets.

In the researched model, EBITDA is $365K in Year 1 and $3951M in Year 5 That is business operating profit before taxes, debt service, reserves, capex, and distributions If the owner works as Program Director, the model includes a separate $65K annual salary line

This model shows breakeven in Month 1, with one month to breakeven That result depends on 50% Year 1 occupancy, 75 modeled slots, $100-$450 monthly pricing, and $236K annual payroll A slower enrollment ramp or higher staffing need can push breakeven later

Yes, reserves should come before owner draws EBITDA is not the same as spendable cash This model also includes $130K of startup capex, $6,850 in monthly fixed costs, and payroll that grows from $236K to $437K, so cash discipline matters even when profit looks strong

Paid enrollment, revenue per child, payroll, and facility costs drive owner pay most The model moves from 50% to 90% occupancy, pricing from $100-$450 to $130-$550 per month, and payroll from $236K to $437K Small misses in staffing or collections can cut distributable profit fast

The best setup is the one that balances rent, capacity, licensing, transportation, and demand This leased-space model uses $3,500 monthly rent and $6,850 total fixed monthly overhead A school, church, or community center may lower rent, but only if the agreement supports enough paid enrollment

About the author

Owen Clarke

Small Business Consultant

Owen Clarke is a small business consultant at Financial Models Lab who writes about everyday business finance and business plan basics for founders building a simple plan before investing money. He focuses on realistic assumptions and startup costs, bringing a practical founder perspective to help readers make grounded, real-world decisions.

Choosing a selection results in a full page refresh.