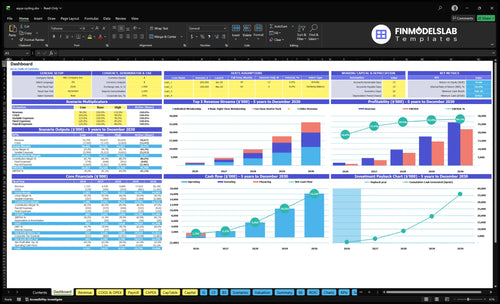

How Much Aqua Cycling Fitness Class Owners Make: $964K Year 1 EBITDA

An aqua cycling studio owner can make strong pre-tax cash flow only if paid occupancy, memberships, and pool costs work together In the researched base case, the studio produces $1722M revenue and $964K EBITDA in Year 1, with occupancy at 45% Owner take-home is not the same as EBITDA, because debt service, taxes, reserves, and reinvestment still come out after operating profit By Year 5, the model reaches $26106M revenue and $21966M EBITDA, but that assumes major growth to 80% occupancy and a much larger member base

Owner income$964KNet margin56%Revenue for target pay$143.5K run-rateBusiness difficultyMedium

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and your pay goal.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see how owner income is built in the model?

How many aqua cycling riders are needed to pay the owner?

For Aqua Cycling Fitness Class, you can’t pin owner pay to one rider count because bike count and classes per week aren’t given, so the right lens is occupancy and monthly revenue. The Year 1 model breaks even in Month 1 at 45% occupancy and the stated monthly revenue run-rate; if the owner wants more pay, the studio needs more paid rides, a better package mix, or more classes.

What drives riders

Bikes per class set capacity

Weekly classes set volume

Occupancy sets paid spots

Price mix sets revenue

What to calculate

Target owner pay first

Then back into filled spots

Then estimate paid rides

Use the class schedule next

Can an aqua cycling studio owner increase income by adding more classes?

Yes—adding more classes can lift income for an Aqua Cycling Fitness Class if demand and pool access are there, because it spreads lease, utilities, insurance, software, and towel costs over more paid riders. The model gets better when billable days move from 26 to 30 and occupancy rises from 45% to 80%, but pool time, instructor coverage, customer demand, and maintenance downtime can cap the gain. Memberships improve cash stability, yet payroll can climb from $25–35K in Year 1 to $474K in Year 5.

More classes help when demand is real

Spread fixed costs across more riders.

Move billable days from 26 to 30.

Push occupancy from 45% toward 80%.

Keep pool slots fully booked.

Limits that can block the upside

Pool access can cap class volume.

Instructor payroll rises with scale.

Maintenance downtime cuts billable hours.

Thin demand can dilute occupancy.

What costs reduce aqua cycling studio owner income?

For Aqua Cycling Fitness Class, the recurring costs cut income faster than the one-time buildout after launch; see How Much To Open Aqua Cycling Fitness Class Business? for launch cost context. In year 1, the biggest drag is 45% pool chemicals and filtration supplies, 30% retail inventory cost, 40% booking fees, and 80% marketing and referral commissions, while fixed monthly costs stay heavy at $108K overhead plus $22K pool heating and utilities.

Variable drag

45% chemicals and filtration supplies

30% retail inventory cost

40% booking fees

80% marketing and referral commissions

Fixed burn

$108K monthly overhead

$22K pool heating and utilities

$65K lease

Paid occupancy beats fixed cost risk

Aqua Cycling Fitness Class Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What drives owner income most?

1

Class Utilization

45%-80%

This is the biggest income swing: fuller classes spread the fixed pool and labor load across more sales, so owner take-home rises fast as occupancy climbs.

2

Pricing Mix

$149-$260

A better mix across unlimited, eight-class, and starter pack plans lifts revenue per slot, while discount-heavy sales cap cash before overhead.

3

Facility Costs

$10.8K/mo

Lease, utilities, and pool care set the cash floor, so any waste in the facility shows up quickly in profit.

4

Staffing Load

$21K-$40K/mo

As instructor and front-desk FTEs rise, wages can outrun sales unless the owner teaches and keeps labor per class tight.

5

Class Capacity

26-30/mo

More billable days give you more slots to sell without adding another pool, which is a direct path to higher take-home.

6

Acquisition Cost

4.5%-8%

Lower marketing and referral spend keeps more cash from each sale, but weak retention will push that cost back up.

Aqua Cycling Fitness Class Core Six Income Drivers

Paid Rider Utilization

Paid Rider Utilization

Paid rider utilization is the share of bike spots you actually fill after pool time, instructor coverage, and the class slot are already paid for. In the model, occupancy rises from 45% in Year 1 to 80% in Year 5, which lifts income because each filled bike adds revenue with little added fixed cost.

Here’s the quick math: Year 1 percentage costs total 195%, leaving 805% before fixed costs and payroll risk. The model’s EBITDA margin moves from 560% to 841%, so the owner’s take-home improves when more bikes are sold in each class. The risk is adding class slots before demand exists.

Fill Bikes Before You Add Slots

Track occupancy by class time, not just total members. A morning rehab class and a weekend class can behave very differently, so use the fill rate to decide where to open more slots. If a class stays below target occupancy, it drains cash flow because the pool and instructor are already committed.

Measure these inputs each month:

Filled bikes per class

Occupancy by time slot

Revenue per rider

Instructor coverage cost

Pool time already committed

1

Pricing And Package Mix

Pricing and Package Mix

Pricing and package mix changes average revenue per rider without adding bikes. In the model, unlimited moves from $199 to $225, eight-class from $149 to $175, and ten-class starter packs from $220 to $260. That lifts package revenue from about $42.8k to $139.4k as counts rise from 230 to 645.

Here’s the quick math: average revenue per package rises from about $186 to $216, or roughly 16%. The risk is discount-heavy selling. Cheap intro offers can fill classes, but if riders do not renew, take-home cash drops fast. Price only works if local demand and retention can support it.

Track revenue per rider by tier

Measure active members, renewal rate, and cash collected per tier each month. Test price increases one tier at a time, then watch if unlimited, eight-class, and starter-pack conversions hold. If lower-priced packs sell but fail to renew, they are adding volume, not profit.

Track monthly revenue per active member.

Watch renewal by package type.

Cap discount depth before launch.

Compare gross cash, not just signups, because promos, refunds, and churn decide owner pay. A cleaner mix with fewer deep discounts usually means better recurring cash flow and less pressure on payroll and rent coverage.

2

Pool And Facility Economics

Pool Access Cost

Aqua cycling income starts with pool access. If there’s no pool, there’s no class inventory, so this driver is the gatekeeper for revenue. The monthly facility load in the model is about $99,900 from $65,000 lease, $22,000 heating and utilities, $450 liability insurance, $150 music licensing, $12,000 janitorial and towel service, and $300 software.

Here’s the quick math: lower fixed pool cost lowers the class break-even point, while underused pool time leaves the same bills to cover fewer riders. The $260,000 buildout also stretches cash payback if demand builds slowly. One idle hour is pure drag; a fuller schedule turns the same water, heat, and lease into owner profit.

Reduce Idle Pool Time

Track pool hours sold, occupancy, and revenue per scheduled class. The useful inputs are billed sessions, average riders per session, and the fixed monthly base of $99,900. If occupancy stays soft, don’t add slots just to look busy; that spreads demand thinner and raises cost per filled bike. The goal is to keep each reserved hour earning its share of rent, heat, and towels.

Test pricing and class timing before adding more pool time. Early mornings, evenings, and rehab-friendly slots should earn their keep or they should go away. If the pool is rented but not filled, cash gets tight fast, and owner pay gets squeezed after the fixed bill stack clears. One rule works: no new class block until the current block is consistently full enough to cover its fixed share.

3

Staffing And Owner Teaching

Owner Teaching and Staffing Mix

Staffing drives how much of each class dollar stays in the studio after labor. In this model, payroll moves from $2535K in Year 1 to $474K in Year 5, with a $65K general manager, a $52K lead aquatic instructor, staff instructors rising from 20 to 60 FTE, and front desk coverage rising from 15 to 30 FTE. If the owner teaches classes, cash flow can improve, but that time is still compensation for work, not pure business return.

The key inputs are instructor pay, class count, coverage hours, and owner teaching load. Here’s the quick math: every paid class the owner covers may reduce wage expense, but it also adds labor that should be counted against owner pay. If quality slips or burnout cuts coverage, revenue can fall faster than payroll savings help. One clean rule: do not trade paid labor for owner hours without tracking fill rate, refunds, and missed classes.

Measure Labor Savings Against Owner Burnout

Track labor cost per class, owner-taught classes per week, and class fill rate. If owner teaching lowers payroll but occupancy drops or the front desk starts missing coverage, the “savings” can backfire. A better test is simple: compare payroll saved to the owner’s hour value and the risk of schedule gaps. If the owner is teaching too much, the business may look lean but still pay out the same in lost demand.

Use staffing to protect quality first. Keep a lead instructor for consistency, then flex staff instructors and front desk coverage as demand grows. Document who covers opening, peak, and weekend classes, because those are the slots that protect cash flow. If onboarding takes too long or instructors rotate too often, service quality drops and the owner ends up teaching more just to keep the schedule full.

4

Weekly Class Schedule Capacity

Weekly Class Capacity

Schedule capacity is how many aqua cycling classes you can sell each week before pool time, instructor coverage, and cleaning become the hard limit. The model lifts billable days from 26 per month in Year 1 to 30 per month from Year 3 onward, so better scheduling can raise revenue through the same lease and utility base. The catch is simple: if you add sessions faster than fill rate, owner take-home income drops.

Measure Fill Before Adding Slots

Track weekly class slots, occupied bikes, and no-shows by time of day. Morning, evening, weekend, rehab-friendly, and senior-friendly classes can improve utilization, but only if occupancy holds. More classes help when they spread fixed pool access across more paid rides; they hurt when they dilute demand across too many sessions.

Watch fill rate by class time.

Test new slots in small batches.

Cut low-demand sessions fast.

5

Retention And Acquisition Efficiency

Retention And Acquisition Efficiency

Repeat attendance is the profit lever here. When members keep coming back, marketing and referral commissions fall from 80% of revenue in Year 1 to 45% in Year 5, so more of each sale stays in the studio. The key inputs are member count, repeat visits, intro-offer churn, and the mix of memberships, class packs, referrals, and partner leads.

Here’s the quick math: at 80% acquisition cost, every $1 of revenue leaves $0.20 before other costs; at 45%, it leaves $0.55. Memberships help because recurring payments and habit formation stabilize cash flow, but churn after intro offers can wipe out the gain. The target is higher net income, not just more gross signups.

Track retention before buying more demand

Measure 30-day return rate, 3-month retention, and the share of new sales from referrals and wellness partners. If intro offers convert but do not repeat, the studio is paying for one-time traffic. Lower acquisition cost only helps when repeat attendance stays strong enough to support recurring revenue.

Track churn after intro packs.

Track monthly membership renewals.

Track referral and partner share.

Price for repeat use.

Cut paid spend when retention slips.

If class packs and partners bring in cheaper repeat buyers than paid ads, owner cash flow improves and take-home income becomes less volatile.

6

Aqua Cycling Fitness Class Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income moves fast here because fill rate, class days, and membership mix all hit the same fixed-cost base.

Low, base, and high owner-income cases for an underwater cycling studio.

Scenario

Low CaseDownside

Base CaseModeled

High CaseUpside

Launch model

This is the conservative income path, with lighter class fill and heavier marketing drag.

This is the modeled middle case, using the Year 1 operating plan as the main earnings base.

This is the stronger earnings path, with mature occupancy and a fuller schedule.

Typical setup

Use 45% occupancy, 26 billable days, 80% marketing spend, and cautious owner distributions while the studio stays in startup mode.

It pairs $1.722M Year 1 revenue with $964k EBITDA, Month 1 break-even, and the planned core team.

It reflects 80% occupancy, 30 billable days, Year 5 revenue of $26.106M, and $21.966M EBITDA with a larger instructor bench.

Cost drivers

45% occupancy

26 billable days

80% marketing

fixed lease and staff costs

cautious distributions

Year 1 revenue

$964k EBITDA

Month 1 break-even

core staffing

membership mix

80% occupancy

30 billable days

$26.106M Year 5 revenue

$21.966M EBITDA

larger instructor roster

Owner income rangeBefore owner reserves

Near break-evenDownside band

$964kModeled case

$21.97MUpside band

Best fit

Best for founders stress-testing a slow start or a harder launch.

Best for base planning, lender talks, and cash use checks.

Best for upside checks if demand stays strong and class fill keeps rising.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual owner distributions.

The researched model shows $1722M in Year 1 revenue and $26106M by Year 5 That growth assumes occupancy rises from 45% to 80%, billable days increase from 26 to 30 per month, and memberships scale across three package types Revenue is not owner pay payroll, pool costs, reserves, taxes, and debt still matter

In this model, break-even occurs in Month 1, with payback also shown at 1 month That result depends on strong launch demand, 45% Year 1 occupancy, and $1435K average monthly revenue If member ramp-up is slower or pool costs are higher, break-even can move out quickly

You need reliable pool access, but the structure can vary This model assumes a commercial studio lease of $65K monthly, pool heating and utilities of $22K monthly, and pool installation capex of $120K A partnership model may lower upfront capex, but it can limit class times and revenue capacity

Occupancy, pricing, pool cost, payroll, and marketing efficiency drive profit most Year 1 has 195% combined COGS and variable costs, plus $2535K payroll and $108K fixed monthly overhead By Year 5, marketing falls to 45%, occupancy reaches 80%, and EBITDA margin reaches 841% in the model

Fill existing class slots before adding cost The cleanest path is higher occupancy, stronger membership retention, and better use of fixed pool time For example, fixed overhead is $108K monthly whether classes are full or not Adding members at $199 to $225 monthly helps only if attendance fits capacity and churn stays controlled

About the author

Owen Clarke

Small Business Consultant

Owen Clarke is a small business consultant at Financial Models Lab who writes about everyday business finance and business plan basics for founders building a simple plan before investing money. He focuses on realistic assumptions and startup costs, bringing a practical founder perspective to help readers make grounded, real-world decisions.

Choosing a selection results in a full page refresh.