How Much Does an Auto Body Shop Owner Make? $312k Year 1 EBITDA

Auto Body Shop Bundle

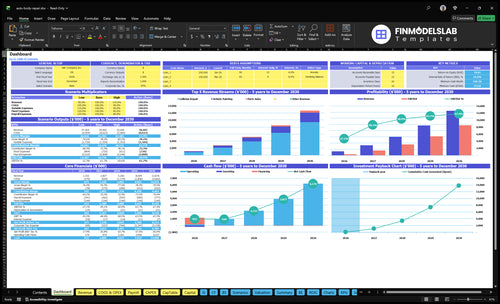

You’re trying to turn repair work into owner take-home, not just busy bays This five-year US auto body shop model shows $312k EBITDA in Year 1, breakeven in Month 5, and a $714k minimum cash need in Month 2, before personal taxes, debt principal, and owner distributions

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target owner pay.

!

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment.

Want to see the full Auto Body Shop forecast?

This dashboard shows revenue, EBITDA, cash, breakeven, payback, and owner-pay planning; charts split sales, margin, payroll, capex, and cash flow. Open the Auto Body Shop Financial Model Template.

Owner-income model highlights

EBITDA $312k to $8.541M

Cash minimum $714k in Month 2

Breakeven Month 5; payback 12

Test volume, ticket, labor

Test parts, overhead, draws

How much can an auto body shop owner make?

An Auto Body Shop owner can make the cash left after payroll, rent, parts, and operating costs, not just a fixed salary; in this model, EBITDA is $312k in Year 1, $1.388M in Year 2, $3.089M in Year 3, $5.421M in Year 4, and $8.541M in Year 5. For context, track profit quality beside repair flow using What Is The Most Critical Indicator For Measuring The Success Of Your Auto Body Shop?, because two shops with similar sales can leave very different owner cash.

Owner Take-Home

Use EBITDA as take-home potential

Year 1 model: $312k

Year 3 model: $3.089M

Year 5 model: $8.541M

What Changes Cash

Improve labor productivity

Capture repair supplements fully

Control parts delays and rent

Keep the staffed $75k manager

What affects auto body shop profit margin?

Auto Body Shop profit margin comes down to billable labor hours, technician productivity, estimate accuracy, and rework, plus parts, consumables, subcontracted labor, and customer acquisition cost. If you’re sizing the model, see How Much Does It Cost To Open An Auto Body Shop? — Year 1 assumptions already put parts at 18%, consumables at 6%, marketing at 4%, and subcontracted labor at 15%. Margin gets better when throughput rises without rework or excess overtime.

Gross margin drivers

Bill more labor hours.

Raise tech productivity.

Cut estimate errors.

Reduce rework and parts waste.

Fixed overhead pressure

$85k rent hits hard.

$12k utilities add steady drag.

$750 insurance stays fixed.

$300 software runs every month.

How much revenue does an auto body shop need to pay the owner?

Auto Body Shop owners should not pick one revenue number; the right target depends on owner pay plus overhead, payroll, reserves, debt service, and capex. With $144k of Year 1 fixed overhead and $295k of payroll, the provided model puts break-even before owner pay at about $52k in monthly sales. The formula is (owner pay + fixed costs + payroll + reserves) ÷ contribution margin, and the model uses 295% variable costs and 705% contribution margin.

Cost base

$144k Year 1 fixed overhead

$295k Year 1 payroll

$52k monthly break-even sales

705% contribution margin in the model

Cash add-ons

Add owner pay first

Add debt service next

Add capex replacement next

Keep reserves before distributions

Auto Body Shop Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see what drives owner income most?

1

Repair Volume

High

More paid repair orders spread rent, payroll, and shop time over more work, so owner take-home rises fastest here.

2

Order Size

$2.3K

Bigger repair orders lift revenue per vehicle and help cover fixed shop costs sooner.

3

Labor Productivity

23h

Year 1 has 15 collision hours at $95 and 8 paint hours at $105, so billed hours and tech speed drive how much payroll turns into revenue.

4

Overhead Load

$144K

Annual fixed overhead is $144K, and with $295K Year 1 payroll, low bay use cuts owner income fast.

5

Materials Margin

76%

Parts cost at 18% and consumables at 6% leave 76% before labor, so waste and shrinkage hit take-home hard.

6

Insurance Mix

80%

Collision repair is 80% of Year 1 mix, so insurer approvals and supplement capture shape cash flow and margin.

Auto Body Shop Core Six Income Drivers

Repair Order Volume

Repair Order Volume

Monthly repair orders set the revenue base: revenue is repair orders × average repair order. More cars only lift owner income if technicians, estimators, parts flow, and paint capacity can keep up. If those stalls hit, cycle time stretches, cash comes in later, and the owner feels it in slower pay and lower profit.

Volume matters more when quality holds. If rework or supplements rise, gross margin gets cut even when the shop looks busy. The model ties marketing spend from $15k in Year 1 to $70k in Year 5, while CAC falls from $120 to $100; that should create more completed jobs, not just more leads.

Track Volume Against Capacity

Watch completed repair orders, cycle time, supplement rate, and rework by month. If orders rise but bays, tech hours, or paint slots do not, owner draw usually lags because cash gets stuck in unfinished jobs.

Track completed orders, not leads.

Match orders to staffed hours.

Flag jobs with supplements.

Measure cash days from release.

Use marketing spend only if the shop can finish the work. Lower CAC helps, but the real win is more completed repair orders at steady quality and faster collections.

1

Average Repair Order

Average Repair Order

Average repair order is the dollars earned per vehicle, and it drives revenue faster than raw volume when the shop can handle the work. Using the model’s labor assumptions, Year 1 ticket value is about $2,265 from 15 billable hours × $95/hour plus 8 paint hours × $105/hour.

By Year 5, that rises to $3,203 from 19 hours × $107/hour and 10 hours × $117/hour, or about 41% more per job. Bigger jobs can lift owner income, but they also use more labor hours, parts coordination, paint booth time, supplements, and working capital. More revenue only helps if cycle time and collections stay tight.

Raise ticket size without slowing cash

Track billable hours, realized labor rate, supplement approval, and collection timing on every repair order. Split collision and paint labor so you can see whether higher-severity jobs are actually paying off or just tying up bays and cash. That’s the quick test: bigger tickets should raise gross profit, not just increase work in process.

Review estimates before tear-down

Approve supplements fast

Watch cycle time weekly

Set pricing and staffing around the job mix you can finish on time. If severe repairs add dollars but also stretch delivery or delay payment, the owner’s take-home income drops even when sales look stronger. The goal is a higher ticket that still converts into cash fast enough to fund payroll and profit draws.

2

Labor Hours and Technician Productivity

Technician Hours Sold

Labor productivity is the share of paid shop time that turns into billed labor. With Year 1 production pay of $65k for the lead technician, $55k for the technician, and $60k for the painter, plus $295k total payroll including manager and customer service, weak utilization cuts owner cash fast because wages keep running whether bays are full or not.

The key metric is billed hours per paid hour, plus rework and downtime. If estimates miss damage or jobs come back for fixes, EBITDA means earnings before interest, taxes, depreciation, and amortization, and it falls before rent changes. More accurate labor plans raise profit without adding space or headcount.

Track Hours vs Payroll

Track paid hours, billed hours, comeback repairs, and schedule gaps by technician. Compare estimated labor to actual labor on every repair order, then flag jobs where downtime or supplements push hours over plan. The goal is simple: keep each paid hour tied to a billed hour.

Review the weekly ratio of billed labor dollars to payroll dollars. If the shop is busy but the ratio slips, fix dispatch, estimating, or repair quality before adding staff. Better scheduling and fewer comebacks move more of the $295k payroll into revenue, which helps owner take-home faster.

3

Parts Paint and Materials Margin

Parts, Paint, and Materials Margin

Parts, paint, and consumables are not pure profit. In Year 1, parts cost is 18% of revenue and shop consumables are 6%, so these costs take 24% before labor and overhead. By Year 5, they improve to 16% and 5%, or 21% total. That 3-point swing lifts cash that can go to owner pay.

Here’s the catch: margin depends on sourcing, freight, returns, discounts, reimbursement limits, and supplement approval delays. If a repair order is done but the supplement is still pending, cash receipts can stall. Track parts gross profit by repair order, not just total spend, or you can look profitable on paper and still feel tight on cash.

Track leakage by repair order

Measure materials billed versus used and returns aging by repair order. That shows where cash gets trapped and where margin leaks out. If you bill $100,000 of revenue, Year 1 parts and consumables cost about $24,000; by Year 5, that drops to $21,000. The owner keeps more only when buying, returns, and approvals stay tight.

Track parts gross profit by job.

Match billed and used materials.

Age returns by repair order.

Watch supplement approval delays.

Audit freight and discount leakage.

4

Insurance Mix and Supplement Capture

Insurance Mix and Supplement Capture

If more of your repair mix comes from insurers, you can fill bays faster, but you give up some pricing control. In the model, collision repair rises from 80% of work in Year 1 to 90% in Year 5, so profit depends on how well you document supplements, hold labor rates, and avoid unpaid parts or procedures. Missed damage can turn a strong ticket into a weak one.

Key inputs are insurer share, supplement dollars per repair order, approval time, labor rate, parts changes, and cycle time. Strong files help collections, but insurer-heavy volume can still compress margin if the shop accepts low rates or absorbs rework. One delayed supplement can stretch cash flow and push owner pay back.

Track and protect supplement dollars

Measure supplements by repair order, not just total sales. Track supplement hit rate, average supplement value, days to approval, and unpaid parts or labor at close. If the shop is sending a lot of insurer work, review estimate photos and teardown notes on every job so added damage is billed fast, not written off later.

Set a simple rule: no close-out until parts changes, added labor, and procedures are documented and approved. Use cycle time, gross margin by payor, and average collection days to see whether insurer growth is helping owner income or just adding busy work.

Track supplements per repair order.

Watch approval days by insurer.

Compare margin by payor mix.

5

Fixed Overhead and Capacity Utilization

Fixed Overhead Break-Even Floor

Fixed overhead is the cost floor. It includes lease, utilities, insurance, software, website and SEO, supplies, and professional services. With $12k monthly fixed overhead plus $246k monthly payroll in Year 1, the shop has to generate sales before the owner can take home profit. The provided quick math says about $52k monthly sales covers payroll and fixed overhead before owner pay.

Empty bays still cost money because rent and insurance keep running. If repair orders fall or cycle time slips, the same fixed cost base is spread over fewer billed hours, so owner income drops fast. Capacity utilization is just how full the bays and tech hours are. Full bays matter more than busy phones.

Fill Bays, Not Just Leads

Track weekly bay utilization, billed labor hours, repair order count, and average repair order. Those inputs show whether fixed overhead is being covered by real production, not just estimates. If staffing, paint time, or parts flow lag, rework and idle time can wipe out the margin.

Watch billed hours per bay.

Match staffing to booked work.

Cut idle time between jobs.

Use the monthly overhead base in your forecast and compare it to actual billed sales, not just booked work. If utilization improves, each extra repair absorbs more fixed cost and more profit can reach owner pay. If supplement approval or collections slow down, cash gets tight even when the schedule looks full.

6

Auto Body Shop Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: Compare lean, base, and high-performing auto body shop owner income cases

Owner income scenarios

Owner income shifts with repair mix, paint work, parts attach, payroll, and capacity. The low case reflects the Year 1 ramp, while the base and high cases assume more volume and better margins.

Low, base, and high income cases for planning.

Scenario

Low CaseDownside case

Base CaseCore case

High CaseUpside case

Launch model

The Year 1 ramp models about $1.065M of revenue, 29.5% variable costs, and $312k EBITDA.

The Year 3 model reaches about $5.049M of revenue, 27.2% variable costs, and $3.089M EBITDA.

The Year 5 model reaches about $12.344M of revenue, 24.8% variable costs, and $8.541M EBITDA.

Typical setup

The shop runs with the manager included, about $295k payroll, $144k fixed overhead, and breakeven in Month 5.

The shop is scaled, with about $443k payroll and a steadier mix of collision repair, painting, and parts sales.

The shop runs at fuller capacity, with about $598k payroll and stronger repair, paint, and parts throughput.

Cost drivers

Repair mix

paint share

parts attach

payroll load

fixed overhead

Higher volume

better labor mix

lower variable rate

more tech FTEs

parts sales

More repair orders

higher paint share

stronger parts sales

lower COGS rate

added tech FTEs

Owner income rangeBefore owner reserves

$312kIncome floor

$3.089MModeled middle

$8.541MUpside path

Best fit

Use this to stress test launch-year income with slower volume and a manager-led shop.

Use this as the main planning case for a steadier, fully built operating year.

Use this to test upside when volume climbs and the editable repair order count stays favorable.

!

Planning note: These scenario ranges are researched planning assumptions only, not guaranteed earnings, salary promises, tax advice, or distributions.

This model shows EBITDA of $312k in Year 1 and $8541M by Year 5 That is operating profit before interest, taxes, depreciation, and amortization, not guaranteed owner salary Owner take-home should come after debt service, cash reserves, equipment replacement, and personal tax planning

The modeled shop reaches breakeven in Month 5 and pays back in 12 months That assumes the staffing plan, pricing, and cost percentages hold The early cash risk is real: minimum cash need peaks at $714k in Month 2, before the business has much operating cushion

This model includes a shop manager at $75k per year from the start If the owner fills that role, cash may improve, but the owner is buying a job and carrying estimating, staffing, vendor, and production-control work If you hire the role, owner income must clear that payroll cost first

The biggest drivers are repair order volume, average repair order, technician productivity, parts and materials margin, insurance mix, and fixed overhead In Year 1, parts cost is 18%, consumables are 6%, and total payroll is $295k Small margin leaks matter because rent and payroll keep running

Start with target owner pay, then add payroll, fixed overhead, debt service, reserves, and capex replacement Year 1 fixed overhead is $144k, payroll is $295k, and startup capex totals $205k Plan distributions from cash after reserves, not from revenue or paper profit alone

About the author

Jonathan Bell

First-Time Founder Guide Writer

Jonathan Bell is a Financial Models Lab writer focused on launch budget planning, helping aspiring small business owners estimate startup needs before opening. As a first-time founder guide writer, he explains business costs in simple language and offers simple launch planning insights that help readers compare business opportunities realistically and make grounded real-world decisions.

Choosing a selection results in a full page refresh.