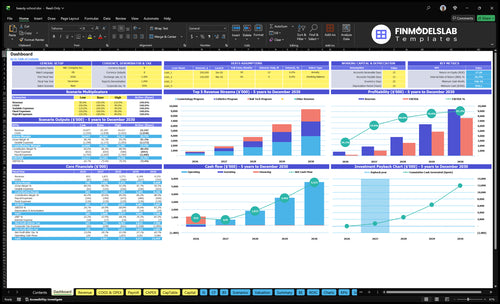

How Much Does A Beauty School Owner Make? $201K Year 1 EBITDA

You’re trying to separate tuition revenue from real beauty school owner take-home pay This five-year planning view uses $201K Year 1 EBITDA, $7607M Year 5 EBITDA, 55% to 88% occupancy, instructor payroll, rent, supplies, marketing, cash reserves, and pre-tax owner pay logic

Owner incomeY1 $201K to Y5 $7.6MNet marginY1 25%Revenue for target pay~$792KBusiness difficultyHard

Want to test your beauty school income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How does the Beauty School model show owner income?

A Beauty School’s gross margin depends on keeping direct costs low, but net margin gets squeezed fast by fixed overhead and payroll. For startup-cost context, see What Is The Estimated Cost To Open And Launch Your Beauty School Business? because $8,500 rent, $1,200 utilities, and $310K to $390K annual payroll can eat the spread quickly.

Gross margin drivers

Beauty supplies run 70% to 50%.

Student kits run 35% to 25%.

Marketing and recruitment fall from 60% to 40%.

Salon consumables fall from 15% to 5%.

Net margin pressure

Rent is $8,500 per month.

Utilities are $1,200 per month.

Insurance, software, cleaning, and accounting total $1,850.

Cash available to owner is what remains after payroll and overhead.

How many students does a beauty school need to be profitable?

There’s no universal student count for a Beauty School to be profitable; the real drivers are occupancy, program mix, tuition, retention, instructor ratios, and fixed costs. In the source model, the school starts with 50 seats split across 25 cosmetology, 15 esthetics, and 10 nail tech seats at 55% occupancy, then reaches 110 seats at 88% occupancy by Year 5. Monthly fixed overhead is $11,550 before payroll, breakeven lands in Month 2, but cash still needs an $839K cushion.

Profit drivers

Occupancy beats raw headcount.

Program mix changes tuition revenue.

Retention keeps seats filled longer.

Instructor ratios limit growth speed.

Model numbers

Starts with 50 seats total.

Ramps to 110 seats by Year 5.

Fixed overhead is $11,550 monthly.

Needs an $839K cash cushion.

Is owning a beauty school profitable?

Beauty School can be profitable, but it is not a passive buy. If you run it yourself and are qualified, you can cut management payroll; if you hire a director, budget about $85K for that role. Income is still capped by seats, schedules, licensed instructors, and facility limits, and launch capex totals $193K.

Filling more seats spreads fixed costs across more tuition, so more EBITDA can reach owner take-home after reserves.

2

Tuition Mix

$700-$1,300

A bigger share of cosmetology seats lifts average tuition, and that extra revenue flows through to cash after supplies and payroll.

3

Instructor Payroll

$310K-$390K

Keeping payroll in this range while classes fill protects margin, which is what turns revenue into owner take-home.

4

Facility Overhead

$11.6K

Holding fixed overhead near $11,550 a month lowers break-even, so more of each tuition dollar can end up as owner cash.

5

Admissions Efficiency

6%-4%

Cutting marketing and recruitment from 6% to 4% keeps more cash after student acquisition costs and supports higher owner draws.

6

Funding Readiness

Month 2

Reaching breakeven in Month 2 and staying compliant helps cash build sooner, which supports owner take-home after reserves.

Beauty School Core Six Income Drivers

Enrollment Utilization

Enrollment Utilization

Enrollment utilization is the share of seats that are filled and kept through completion. For a beauty school, that means converting inquiries into enrolled students, then keeping them active long enough to bill monthly tuition. Here’s the quick math: 50 × 55% = 28 filled seats, while 110 × 88% = 97. More filled seats spread fixed campus costs over more tuition.

The income impact is direct: higher utilization lifts EBITDA because rent, staff, software, and insurance do not rise one-for-one with each student. With fixed overhead at $11,550 per month, underfilled cohorts squeeze cash flow fast. Inquiries are not revenue. Completion rates matter too, since a dropped student stops tuition while most costs stay in place.

Raise Seat Fill and Retention

Track inquiries, applications, enrolled students, and completed students separately. The key rates are inquiry-to-enrollment, enrollment-to-completion, and seats filled per cohort. If occupancy moves from 55% toward 88%, the school uses more of its tuition capacity, which improves gross margin and makes owner pay less dependent on new leads.

Use start dates, follow-up, and class schedules to keep cohorts full. Add staff and space only when fill is stable, not when leads look strong. If retention slips, billed months fall but most fixed costs do not, so cash flow tightens quickly. One empty seat can hurt twice: lost tuition and wasted capacity.

Track fill by program and cohort.

Watch completion before expansion.

Delay hires until occupancy holds.

Match schedules to student demand.

1

Tuition And Program Mix

Tuition Mix

Tuition revenue comes from monthly price, program length, seat mix, demand, and when students pay. Year 1 monthly tuition is $1,200 for cosmetology, $950 for esthetics, and $700 for nail tech; by Year 5, that rises to $1,300, $1,030, and $760. More cosmetology seats usually lifts revenue, but only if pricing stays competitive and compliant.

Here’s the quick math: a stronger mix of higher-priced programs raises gross revenue per filled seat, which helps cover fixed payroll and campus costs. The catch is cash timing. Tuition that is billed but not collected still leaves the owner short on rent, instructors, and marketing. Full seats only help if they pay on time.

Price and Collection Control

Track enrolled seats, monthly tuition collected, and mix by program every month. The seat plan shifts from 25 cosmetology, 15 esthetics, and 10 nail tech seats in Year 1 to 45, 35, and 30 in Year 5, so the owner should watch which program fills first and which one delays payment.

Test each program separately for pricing, discounts, and payment plans. Keep a simple report on price per seat, cash collected, and delinquent balances. If one program needs deeper discounts to fill, it may add volume but hurt owner pay. Profit comes from the right mix, not just more students.

2

Instructor Productivity And Payroll

Instructor Payroll

Instructor pay is a direct margin lever. The model uses $60K for the lead cosmetology instructor, $55K for esthetics, $50K for nail tech, and $50K for the assistant cosmetology instructor starting in Month 25. Total payroll rises from $310K in Year 1 to $390K from Year 3 onward, so monthly labor cost moves from about $25.8K to $32.5K before owner pay.

The real driver is full classes per instructor, not cheaper instruction. If seats stay filled and licensed coverage holds, higher payroll supports tuition revenue and protects EBITDA. If classes run light, payroll still gets paid, but gross margin drops fast and there is less cash left for the owner draw.

Fill Classes, Protect Coverage

Track filled seats per instructor, not just enrollment. Here’s the quick math: if payroll is $390K, every weak cohort makes labor cost heavier per student, while full classes spread that cost across more tuition. Keep student-to-teacher standards intact so service quality and compliance do not slip.

Track payroll by role monthly.

Model Month 25 staffing early.

Watch seats per licensed instructor.

Link hiring to filled cohorts.

Test class size before adding staff.

3

Facility And Campus Overhead

Campus Overhead Floor

$11,550 a month is the fixed campus floor before owner pay: $8,500 rent, $1,200 utilities, $450 insurance, $300 software, $600 cleaning, and $500 accounting. That is $138,600 a year before any variable cost. If enrollment misses plan, this overhead comes out of cash first and pushes owner draw back.

The launch buildout and setup capex is $193K, and minimum cash in Month 2 is $839K. So the real risk is not just monthly profit; it is whether tuition and collection timing can carry rent, payroll, supplies, and marketing long enough to reach breakeven enrollment.

Track the Overhead Run-Rate

Measure the campus floor every month and tie it to filled seats. If the overhead ratio stays high, tuition has to do more work before the owner can pay themselves. One clean rule: keep the fixed-cost base visible before adding space, software, or services.

$11,550 monthly fixed overhead

$193K launch capex

$839K Month 2 cash minimum

Rent, utilities, insurance, software

Cleaning and accounting support

Stress test enrollment against those costs before opening extra cohorts or hiring ahead of demand. If cash dips below the reserve, the owner’s income gets delayed even when classrooms are busy.

4

Marketing And Admissions Efficiency

Admissions Conversion

When inquiries do not turn into enrollments, marketing spend turns into dead cash. In this model, marketing and recruitment run at 60% of revenue in Year 1 and fall to 40% by Year 5, so admissions quality is a direct margin lever. Track inquiries, applications, enrolled students, and completed students separately, because only filled seats pay tuition.

Strong follow-up can lift occupancy from 55% to 88% without wasting ad spend. Weak conversion raises cost per enrolled student, delays payback, and squeezes cash available for payroll, rent, and owner draw. The quick test is simple: if spend rises but enrollments do not, the funnel is leaking.

Track the Funnel, Not Just Leads

Measure conversion weekly from inquiry to application, application to enrollment, and enrollment to completion. If inquiries are strong but enrollments lag, the issue is follow-up, timing, or document collection, not more ads. If completions slip, tuition quality drops because empty seats and dropouts do not cover fixed costs.

Set a target occupancy path from 55% to 88% and tie spend to that goal. Cut channels that bring low-intent leads, and keep staff on fast calls, reminders, and enrollment steps. That keeps customer acquisition cost down and moves the business faster toward owner profit.

5

Compliance And Funding Readiness

Compliance and Funding Readiness

If the school’s licensing, accreditation, and reporting are not ready on time, enrollment can stall even when demand is strong. That hits cash twice: tuition starts later, and fixed overhead still runs at about $11,550 per month. Funding readiness matters too, because delayed approvals can push payment timing out and reduce how many seats can actually open.

What this hides is the operating drag. Accreditation work can add staff time, professional fees, documentation, and reporting pressure, so compliance is not just a legal task. It is a profit and cash flow line item. If a cohort slips, owner take-home drops even before demand shows up in the classroom.

Track approval timing, not just demand

Measure the number of days from application to approval, the share of seats blocked by missing paperwork, and the cash gap created by delayed starts. Here’s the quick math: if a cohort delay pushes tuition receipts back by one month, the school still carries rent, utilities, insurance, software, cleaning, and accounting. That can squeeze the draw fast.

Use a simple compliance calendar and tie it to enrollment forecasts. Track license renewals, accreditation milestones, reporting due dates, and any funding terms that affect when tuition can be collected. One missed filing can cost more than one empty seat because it can delay multiple students at once.

Track approval dates and renewal dates.

Track reporting due dates weekly.

Track tuition receipt timing by cohort.

Track staff hours on compliance tasks.

6

Beauty School Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high beauty school owner income scenarios

Income scenario table

Owner income moves with fill rate, tuition mix, payroll, and how much cash stays in reserve. Early cash is tight, then earnings improve as cohorts fill.

Low, base, and high cases show how occupancy and staffing shape owner take-home.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Owner take-home stays light because occupancy builds slowly and more cash gets held back.

Owner take-home follows the modeled operating plan and grows as occupancy and cohort size rise.

Owner take-home rises faster when fill rates stay strong and more revenue drops to the bottom line.

Typical setup

Cohorts fill late, marketing stays high, and the school runs with tighter reserves and slower enrollment growth.

Occupancy moves from 55% to 88%, tuition runs from $700 to $1,300, payroll runs about $310k to $385k, and fixed overhead stays at $11,550 per month.

Cohorts fill faster, instructors are used more efficiently, marketing takes a smaller share, and more cash can flow to the owner after reserves and reinvestment.

Cost drivers

lower occupancy

higher marketing

delayed cohort fill

tighter cash reserves

occupancy climb

tuition mix

payroll load

$11,550 overhead

retail sales

stronger fill rates

better instructor use

lower marketing

higher cohort volume

more retail sales

Owner income rangeBefore owner reserves

$0 - $75,000Slow fill

$100,000 - $400,000Modeled case

$500,000 - $1,500,000Strong fill

Best fit

Use this to stress test a slow launch or weaker enrollment conversion.

Use this as the main planning case for budgeting and owner draws.

Use this to test upside if admissions, staffing, and retention all work well.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

This model shows a minimum cash need of $839K in Month 2 That sits on top of $193K in launch capex, including $75K leasehold improvements, $40K salon stations, and $25K classroom equipment The cash cushion matters because payroll, rent, and admissions costs start before every seat is full

The model shows a 14-month payback period and Month 2 breakeven That assumes occupancy ramps from 55% in Year 1 to 68% in Year 2 and that tuition collection stays on plan Payback can stretch if student starts slip, financing costs rise, or reserves are held back

Not necessarily, but the model already includes hired leadership and instructors Payroll includes an $85K school director, $60K lead cosmetology instructor, $55K esthetics instructor, and other staff If the owner teaches or manages, the economics change, but licensing, quality, and time demands still matter

Enrollment timing, tuition collection, payroll, rent, and reserves drive cash flow The model uses $8,500 monthly rent, $310K Year 1 payroll, and marketing at 60% of revenue Even with positive EBITDA, owner distributions can be limited if cash is needed for growth, compliance, or debt service

Fill seats before adding fixed cost The cleanest levers are raising occupancy from 55% toward 88%, keeping instructor schedules full, and reducing marketing from 60% to 40% of revenue Tuition increases help too, but they must match demand, outcomes, and compliance rules

About the author

Simon Reed

Small Business Educator

Simon Reed is a small business educator at Financial Models Lab who helps service business founders understand the numbers behind everyday business ideas. He focuses on pricing and margin basics, common business costs, and the first months after launch, giving readers a clearer view of what it takes to build a healthy business. Simon brings a simple, confident approach that balances optimism with cost-aware planning.

Choosing a selection results in a full page refresh.