How Much Bonded Warehouse Owners Make: 5-Year Profit View

Key Takeaways

Occupied bonded space drives revenue, not empty capacity.

Storage fees depend on dwell time and renewals.

Accessorials matter, but labor pricing must cover overtime.

Strong contracts reduce vacancy and steady owner cash.

Owner income≈$1.33MNet margin24.7%Revenue for target pay≈$5.4MBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Bonded Warehouse Service model?

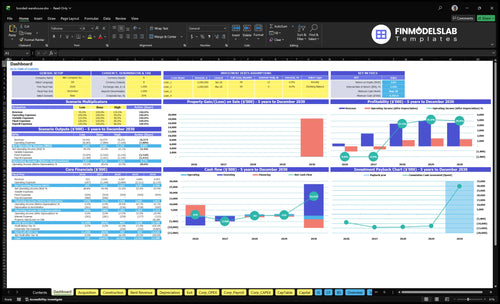

This screenshot shows the dashboard, assumptions, income outputs, cash curve, and scenario tabs in the Bonded Warehouse Service Financial Model Template, with Month 29 minimum cash of -$4,394M. Open it.

Owner-income model highlights

Owner income shown

Month 25 breakeven

146% IRR, 282 ROE

What costs reduce bonded warehouse owner income most?

The biggest hit to owner income is fixed cost pressure that starts before occupancy fills up: labor scheduling, rent, security, insurance, compliance, systems, maintenance, and underused space. In the data, monthly fixed expenses total $42k, including $12k security monitoring, $9k insurance, $7k utilities, and $3k customs compliance software, so even strong storage revenue can still leave weak owner income. If you want the startup cost side, see How Much To Start Bonded Warehouse Service?

Main income drains

$12k security monitoring

$9k insurance

$7k utilities

$3k compliance software

Later-stage pressure

Year 5 payroll reaches $795k

Rented facilities cost $63k per month

Underused space still costs cash

Labor scheduling must match occupancy

Does a small bonded warehouse owner make more by operating hands-on?

If you’re running Bonded Warehouse Service, being hands-on can protect cash early only if you’re doing a real operating job, not just “watching the floor.” Here’s the quick math: the model already includes a $120k Facility General Manager from Month 1, and negative EBITDA in Years 1-2 means cash control matters more than headline revenue.

Early cash control

Owner role can cut early payroll pressure

Real ops work beats passive oversight

$120k GM already starts Month 1

Cash matters more than revenue now

What drives scale

Capacity limits growth, not square footage

Contract quality shapes margin and risk

Staff depth supports $795k payroll by Year 5

Compliance discipline protects the business

How much can a bonded warehouse owner pay themselves?

A Bonded Warehouse Service owner should plan on $0 operating-funded salary in Year 1 and Year 2; pay needs outside funding or must wait until after Month 25 breakeven. For more setup context, see How To Launch Bonded Warehouse Service Business?, but keep duties separate because they are pass-through cash, not owner income.

Owner Pay Rules

Delay salary during negative EBITDA years

Start pay after Month 25 breakeven

Separate salary from profit distributions

Exclude customs duties from income

Cash Limits

Year 5 EBITDA reaches $1332M

Not all EBITDA is take-home

Minimum cash hits -$4394M in Month 29

Reserve cash for reinvestment first

Bonded Warehouse Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Utilization

$450K

More occupied bonded space lifts the $450K monthly fee base, and duties stay outside revenue.

2

Storage Rates

Month 25

Better storage pricing and longer dwell time are what get the model to breakeven by Month 25.

3

Accessorial Fees

$42K

Accessorial charges help cover the $42K fixed overhead without adding much floor space.

4

Rent Load

$63K

Site rent at $63K a month makes location choice a direct hit to margin.

5

Labor Control

$795K

Year 5 payroll reaches $795K, so staffing, security, insurance, and compliance discipline protect EBITDA.

6

Collections

-$4.394M

Tighter contracts and faster payment protect cash, since late pay can drive the cash trough to -$4.394M.

Bonded Warehouse Service Core Six Income Drivers

Bonded Warehouse Utilization

Bonded Space Utilization

Utilization is the core income lever. Empty bonded space earns nothing, but rent, security, insurance, utilities, and compliance still run, so owner income depends on occupied bonded space, storage fill rate, paid pallet positions, and monthly fee capture. Use $450k in modeled monthly rental fees as the revenue ceiling proxy; if paid occupancy lags, cash flow stays tight and owner draws stay thin.

Track Paid Capacity, Not Building Size

Measure paid occupied capacity each month: occupied square footage, pallet positions sold, fill rate, and fee collected per occupied slot. Higher fill rate lifts gross margin because fixed costs spread over more billable space. One clean test is whether revenue per occupied position climbs fast enough to ease Month 29 cash pressure; if not, the facility looks big but earns small.

Track paid slots daily.

Separate free from billable space.

Compare fees to $450k ceiling.

Flag slow ramp by month 29.

1

Storage Pricing and Dwell Time

Storage Price and Dwell Time

Income here comes from monthly storage fees and how long imported goods stay under bond. The modeled monthly rent across North Hub $85k, Port Zone A $65k, East Terminal $75k, South Depot $60k, West Annex $95k, and Central Bay $70k totals $450k. Customs duties and importer taxes are not owner revenue.

Owner pay rises when average dwell time and customer renewal rate hold up, because each occupied position bills longer. What this hides: if rate cuts fill space but shorten cash collected per bay, revenue per occupied position can fall even when the warehouse looks busy.

Monthly storage fee

Average dwell time

Customer renewal rate

Revenue per occupied position

Price for Paid Days

Track revenue per occupied position by site and compare it with security, insurance, utilities, and labor. Here’s the quick math: higher dwell time at the same fee lifts cash flow; lower dwell time means the same space must turn faster or pricing must rise to protect margin.

Set lease terms and storage tiers around real flow patterns, not just fill rate. If onboarding takes 14+ days, cash lags and renewal risk rises, so late-paying or short-dwell accounts should not get the same price as steady repeat importers.

2

Handling and Accessorial Fee Mix

Handling and Accessorial Fee Mix

Accessorial fees can lift owner income when storage tenants also pay for receiving, unloading, palletizing, labeling, inventory manipulation, examinations, release processing, and document handling. The key is to keep this revenue separate from recurring storage rent, so you can see whether labor-heavy work is adding margin or just adding activity.

The risk is simple: if these services are priced too low, the extra revenue gets eaten by overtime and supervisor time. That hurts gross margin and cash flow fast, even when storage occupancy looks healthy. Here’s the quick math to watch: accessorial revenue minus direct labor and overtime should stay positive on every job, or it drags owner pay down.

Price and Track Every Touch

Build the model with an editable monthly accessorial revenue input, since no benchmark number is provided. Track the mix by service line and tie it to labor hours, overtime, and customer count. One clean rule: if a task takes labor, it needs its own price, not a guess folded into storage rent.

Measure revenue per handled shipment, labor cost per task, and overtime as a share of accessorial revenue. If overtime rises faster than fee revenue, raise rates or tighten scope before margin leaks out. That keeps the extra work from turning into extra payroll instead of extra owner income.

Track each fee by service line.

Separate rent from accessorials.

Test labor minutes per task.

Raise prices when overtime appears.

3

Facility Cost and Location Economics

Location Premium

Location helps this business only when demand is strong enough to cover the fixed base. The modeled rented sites are $20k, $18k, and $25k a month, or $63k total rent, while owned sites need $93M for purchase and $203M more for construction across all facilities. Better port or airport access can support pricing, but empty space still burns cash and cuts owner pay.

Here’s the quick math: the owner wins only if higher rent and storage fees outpace those fixed site costs. Track utilization, rent per location, and revenue per occupied position before you sign. If the site cannot reach steady paid occupancy fast, the premium address turns into lower profit and thinner distributions.

Break-Even by Site

Model each site on paid occupancy, not square feet. Build a break-even sheet with monthly rent, expected storage income, and any location-based price lift. The test is simple: can the site cover the $63k monthly rented base, or the much heavier owned-site cost stack, with real utilization?

Track occupied space every month.

Test port versus inland pricing.

Raise rates only with fill-rate gains.

4

Labor, Security, Insurance, and Compliance

Compliance Control Spend

This driver covers security monitoring, insurance, maintenance, compliance software, and the labor that keeps bonded cargo moving. Year 5 payroll is $795k; the named roles total $400k, with two Customs Compliance Officers at $95k each and three Warehouse Operations Leads at $70k each. Add $89k a month in fixed spend, and profit plus owner draw stay under pressure even when space sits empty.

Cheap cuts can backfire. If controls drop, shrinkage, audit delays, or release holds can hit cash flow and erase the savings. Keep compliance spend tied to cargo release speed and loss rate, because a bonded site only earns if goods can move on time.

Track the cost to stay open

Track payroll, security, insurance, maintenance, and compliance software as one fixed-cost block. Here’s the quick math: $12k + $9k + $65k + $3k = $89k a month, or $1.068M a year before payroll. Estimate it from headcount, pay rates, and monthly control spend. That tells you the minimum revenue and utilization needed to protect owner pay.

Headcount and pay rates

Monthly control spend

Release delays and shrinkage

Audit issues and exam holds

Test staffing against incident logs and cargo release time. If a labor cut saves cash but raises shrinkage or audit risk, it is not a real saving. Use that data to decide where to add, trim, or keep controls tight.

5

Customer Contracts and Payment Reliability

Contract Quality

For a bonded warehouse, contract quality decides how much storage revenue turns into steady owner cash. Repeat importers, freight forwarders, and customs brokers with predictable dwell patterns reduce vacancy swings, support better pricing, and make distributions more reliable once the site clears breakeven.

Weak contracts are expensive. The owner still carries $42k a month of fixed overhead plus $63k a month of rent, or $105k/month before enough paid storage is booked. If minimum commitments are thin or payment terms slip, cash gets trapped in empty space instead of reaching owner pay.

Track Contracted Fill and Payment Discipline

Measure contract length, minimum storage commitments, payment terms, and accessorial acceptance on every account. Also track the share of occupied pallets or square feet tied to signed agreements, because contracted space is what protects revenue when spot demand slows.

Push for longer terms, prepaid or tight net terms, and clear fees for receiving, palletizing, and release work. One clean rule helps: if a customer won’t commit to paid storage and fee acceptance, the facility is still carrying the fixed base but not yet earning enough to support owner distributions.

Track contracted fill, not just occupancy.

Separate storage rent from accessorial fees.

Test renewal rates by customer type.

Review late pays before extending terms.

6

Bonded Warehouse Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: compare low, base, and high owner-income planning cases from the provided 60-month model

Owner income scenarios

Income shifts with ramp-up, customs throughput, and fixed overhead. Early years stay negative, then breakeven lands in Month 25 as the model scales.

Low, base, and high cases show how ramp speed changes owner income.

Scenario

Low CaseRamp-up

Base CaseStabilized

High CasePeak year

Launch model

Owner income stays negative while the business is still ramping and funding the early cash gap.

Owner income turns positive once the warehouse reaches a steadier operating rhythm.

Owner income reaches its strongest path when the model hits peak EBITDA in the mature year.

Typical setup

Year 1 EBITDA is -$996k and Year 2 EBITDA is -$589k, with cash bottoming in Month 29 before the model reaches breakeven in Month 25.

Year 3 EBITDA reaches $1.183M and Year 5 EBITDA is $1.332M before debt, tax, and reserves, after breakeven in Month 25.

Year 4 EBITDA peaks at $1.507M as the full warehouse stack is running and fixed costs are spread across more volume.

Cost drivers

Year 1 EBITDA -$996k

Year 2 EBITDA -$589k

fixed overhead

staffing and compliance

outside funding need

Year 3 EBITDA $1.183M

Year 5 EBITDA $1.332M

Month 25 breakeven

owned sites

fixed overhead spread

Year 4 EBITDA $1.507M

mature operations

full asset ramp

fixed costs spread

stronger throughput

Owner income rangeBefore owner reserves

-$996k to -$589kRamp-up loss

$1.183M to $1.332MStabilized income

$1.507MPeak upside

Best fit

Use this to test downside cash needs and funding gaps before distributions are possible.

Use this as the main planning case for owner income after the initial ramp.

Use this to test upside if ramp, utilization, and cost control all hold.

!

Planning note: Scenario ranges are researched planning assumptions from the model, not guaranteed earnings, salary promises, tax advice, or distributions.

In this 60-month model, owner distributions are unlikely in the first two years because EBITDA is -$996k in Year 1 and -$589k in Year 2 The business turns positive after Month 25, with EBITDA of $1183M in Year 3 and $1332M in Year 5 before debt, taxes, reserves, and owner distributions

The modeled breakeven point is Month 25, with payback at Month 60 That matters because the cash low reaches -$4394M in Month 29, after operations improve but before the full investment is recovered Owner pay should be planned around cash timing, not just annual profit

No, customs duties are pass-through obligations tied to the importer, not owner income The owner’s revenue comes from storage fees, handling fees, accessorial services, and related warehouse charges In this model, full-scale rental fee capacity is $450k per month, while duties and taxes remain outside profit calculations

Utilization, storage pricing, labor, rent, security, insurance, and compliance drive profitability Year 5 payroll is $795k, fixed overhead is $42k per month, and rented-site costs are $63k per month If paid occupancy lags, those costs still run, which can delay owner pay even with strong long-term demand

The best time is after the business clears breakeven, funds reserves, and covers debt service In this model, that means looking past Month 25 and watching the Month 29 cash low of -$4394M A founder can budget salary earlier, but distributions should wait until cash is stable

About the author

Ava Mitchell

Business Plan Writer

Ava Mitchell is a business plan writer at Financial Models Lab who helps early-stage founders choose realistic business ideas with founder-friendly numbers. She explains startup planning in plain English, with a focus on operating expense planning and on breaking down revenue, expenses, and profit so founders can make practical real-world decisions.

Choosing a selection results in a full page refresh.