Can a BIPV installation business scale owner income?

Yes—Building-Integrated Photovoltaics Installation can scale owner income, but only if you keep payroll, working capital, and delivery risk tight. In the owner-operator stage, income comes from selling, design review, and project control, with about $145K in salary; once you add project managers, certified lead installers, engineers, and business development, the business gets bigger, but overhead rises fast. The model works when commercial façade projects, architect relationships, and repeat contractor work lift throughput without hurting gross margin; idle crews and delayed commissioning can cut owner income quickly.

Owner-operator stage

Sell the deal and control scope.

Review design before crews mobilize.

Keep staffing lean at $145K salary.

Protect margin with tight commissioning.

Managed team stage

Add project managers and lead installers.

Bring in engineers and business development.

Scale with repeat contractor work.

Avoid idle crews and slow starts.

How much can the owner of a BIPV installation business take home?

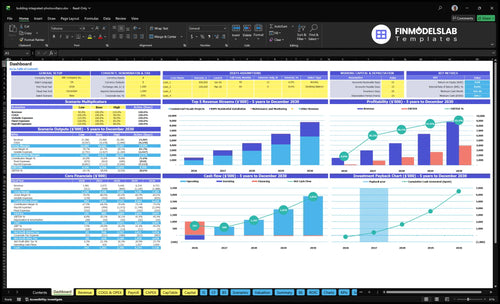

The owner of a Building-Integrated Photovoltaics Installation business can take home a modeled payroll salary of $145K per year; for operating cost context, see What Are Operating Costs For Building-Integrated Photovoltaics Installation?. Year 1 EBITDA is $131K after payroll, but the owner shouldn’t drain profit because Month 6 minimum cash need reaches $504K.

Owner Take-Home

Model salary: $145K/year

Year 1 EBITDA: $131K

Cash need: $504K in Month 6

Profit is not free cash

Scale Upside

Year 2 revenue: $2.972M

Year 2 EBITDA: $895K

Year 5 revenue: $8.753M

Year 5 EBITDA: $3.973M

How much revenue does a BIPV installation business need to pay the owner?

For a Building-Integrated Photovoltaics Installation business, the owner-pay floor is about $1.16M in revenue. Here’s the quick math: $145K owner pay + $460K non-owner payroll + $162K fixed overhead + $45K marketing = $812K to cover, and at 70% gross margin that means roughly $1.16M revenue before reserves and timing gaps. The researched $1.481M Year 1 revenue case produces about $131K EBITDA, so high contract value only helps when margin, billing, and collections stay tight.

Cost floor

$145K owner salary

$460K non-owner payroll

$162K fixed overhead

$45K marketing spend

Revenue check

$812K must be covered

70% gross margin assumed

$1.16M revenue needed

$131K EBITDA at $1.481M

Building-Integrated Photovoltaics Installation Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main BIPV income drivers?

1

Contract Value

$222K-$7.9M

The mix from residential jobs to commercial facade work can swing Year 1 project math from about $222K to $7.9M, so deal size sets the top line.

2

Gross Margin

70%-75%

Moving gross margin from 70% to 75% leaves more of each job after materials, subcontractors, and freight.

3

Crew Utilization

42.5-55.5h

Raising billable hours per active customer from 42.5 to 55.5 spreads labor across more revenue and lifts take-home.

4

Sales Pipeline

$3.2K-$4.5K

Lower CAC from $4.5K to $3.2K keeps the $45K-$135K marketing budget from shrinking project profit.

5

Overhead Control

$15.5K/mo

Keeping fixed overhead near $15.5K a month protects cash when work is lumpy and bids take time to convert.

6

Cash Reserve

$504K

The model needs about $504K of minimum cash in month 6, so reserve discipline decides whether growth survives the ramp.

Building-Integrated Photovoltaics Installation Core Six Income Drivers

Project Contract Value

Project Contract Value

Higher building-integrated photovoltaics (BIPV) contract value can raise owner income fast, but only if gross margin and cash timing hold. A Year 1 residential job at 120 hours × $185 = $22,200 is very different from a commercial façade job at 350 hours × $225 = $78,750. Bigger roof, façade, canopy, skylight, and curtain-wall scopes improve revenue density per project.

The risk is simple: larger deals often mean longer sales cycles, deposits, retainage, and supplier bills due before final customer cash arrives. If billing lags the work, reported revenue won’t translate into take-home pay right away. Here’s the quick math: more contract value helps only when collection terms and material timing stay under control.

Price Bigger, Bill Faster

Track average contract value, deposit %, retainage %, and days from signed deal to first invoice. A larger contract should not just look good on paper; it needs enough upfront cash to cover labor and supplier payments. If a project needs heavy custom materials, price that timing risk into the quote.

Push for scope clarity on design, engineering, and install hours before you sign. One clean rule: no margin, no growth. If change orders, rework, or slow collections eat the extra revenue, the owner’s draw falls even when top-line sales rise.

1

Gross Margin Control

Gross Margin Control

Gross margin is the share left after direct project costs. In this model, Year 1 revenue reaches $1,481M and Year 5 reaches $8,753M, so even a 1-point swing matters: about $14.8M in Year 1 and $87.5M in Year 5 before fixed overhead. Gross margin is not owner profit; payroll, rent, and cash timing still decide what you can pay yourself.

The direct cost stack starts at 30% in Year 1 and improves to 25% by Year 5. That stack includes materials, subcontracted engineering, logistics, commissions, plus project overruns. Here’s the quick math: moving from 30% to 25% on Year 5 revenue adds about $437.7M of gross profit before overhead. The risk is simple: bad estimates and rework can erase that gain fast.

Control the Cost Stack

Track each job’s estimated vs. actual materials, labor hours, subcontractor quotes, change orders, rework, and warranty reserve. Use the same takeoff template on every bid so pricing drift shows up fast. If subcontracted engineering or logistics runs hot on a few projects, margin will look fine on paper but owner cash will lag.

Measure margin by project type.

Review change orders weekly.

Lock subcontractor pricing early.

Price rework and warranty risk.

Compare estimate vs. actual monthly.

Use margin as a control metric, not a scorecard. If a project wins revenue but misses its direct-cost target, it can still squeeze distributions because overhead and payroll stay fixed. The owner’s take-home income improves when project teams protect the 30% to 25% cost path and bill cleanly for scope changes.

2

Crew Utilization

Crew Utilization

If crews look busy but owner draws stay flat, the problem is usually crew utilization: turning labor into completed billable projects. In this model, residential installs drop from 120 to 100 hours per job by Year 5, and commercial façade work drops from 350 to 310 hours, so throughput rises only if those hours stay billable.

Idle days don’t just waste labor; they delay invoices and cash. That matters because payroll rises from $605K in Year 1 to $1765M in Year 5, so weak scheduling can squeeze EBITDA and push the owner’s pay back even when the crew is fully booked on paper.

Track Billable Flow

Measure billable hours per job, jobs completed per month, and days from install to commissioning (final testing and sign-off). The key inputs are crew hours, idle days, subcontractor handoffs, and how fast each project turns into an invoice. If hours fall but completions do not rise, the gain is leaking into waiting time or rework.

Split residential and façade hours.

Track idle days by cause.

Lock dates with other trades early.

Bill at commissioning milestones.

Better coordination with roofers, glaziers, electricians, architects, and general contractors lifts project flow and protects cash. One clean rule: if the job is done but not billed, cash is late, and late cash lowers the owner’s take-home income even when the schedule looks full.

3

Sales Pipeline Quality

Qualified Pipeline

Qualified pipeline is the difference between booked BIPV work and expensive proposal churn. With marketing budget rising from $45K in Year 1 to $135K in Year 5, the goal is not more leads; it’s more leads that fit architect specs, general-contractor plans, and owner budgets. That is what stabilizes revenue and owner pay.

Here’s the risk: weak leads soak up estimating time, inflate CAC, and leave crews waiting. As commercial façade work rises from 20% to 40% and maintenance and monitoring from 10% to 85%, the funnel has to match the mix or cash gets lumpy. CAC improving from $4,500 to $3,200 only helps if the win rate holds.

Track the Right Leads

Measure source, stage conversion, average contract value, and proposal-to-award rate. Separate architect specifications, general-contractor referrals, building-owner demand, and incentive-aware deals so you can see which channel really funds payroll. If a channel does not produce qualified opportunities with a clear path to spec approval, it should not get more budget.

Use accurate proposals and fast disqualification to cut waste. What this estimate hides is proposal labor that never turns into billings. A tighter funnel means fewer wasted bids, steadier backlog, and less risk of uneven payroll coverage when project timing slips.

4

Overhead Discipline

Overhead Discipline

$13,500 a month, or $162K a year, comes off gross profit before owner distributions. That stack is rent, software, insurance, fleet, utilities, and collateral subscriptions, so the business has to clear that line before there’s real room for owner pay.

What this hides is simple: if backlog slips, these costs still hit cash. For BIPV work, overhead should follow booked project load, not hope. Add licensing support, engineering review, project management, estimating, safety training, and professional services only when signed work can carry them.

Track Backlog, Not Wishful Spend

Measure monthly overhead against booked gross profit and watch whether the current pipeline covers $13,500 before payroll, marketing, and owner pay. If it doesn’t, the business is using cash that should protect distributions.

Build the overhead plan from real inputs: current rent, software, insurance, fleet, utilities, subscriptions, and any added support roles. Keep each add tied to project volume, so margin doesn’t leak into idle capacity.

5

Cash Reserve Management

Cash Reserve Discipline

Profit alone does not pay the owner here. With $504K of minimum cash needed in Month 6, breakeven in Month 7, and 19-month payback, this business can look healthy on paper while cash is still trapped in jobs, retainage, and supplier bills. One clean rule: don’t size owner draws from booked profit alone.

The cash need includes the $320K launch capex plus working cash for deposits, progress billing, customer holdback, supplier terms, interconnection delays, warranty reserves, debt service, and reinvestment. If collections lag the install schedule, owner distributions get squeezed even when gross profit is positive.

Protect Draw Cash

Track cash by project, not by revenue. Use a simple forecast that shows opening cash, deposits, progress billings, retainage, supplier payments, payroll, debt service, and reserve needs. For this model, the key question is whether cash stays above the $504K floor in Month 6.

Track retainage by job.

Match billing to milestones.

Set a warranty reserve.

Negotiate supplier terms early.

Delay draws until reserves hold.

Push for larger deposits and faster progress billing on custom work, since long design and interconnection cycles can trap cash for months. If collections slip, owner pay should slow before payroll or vendor stress does. That protects the business and keeps distributions tied to real cash, not just profit on paper.

6

Building-Integrated Photovoltaics Installation Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high-growth BIPV owner income cases

Owner income scenarios

Owner income moves with project mix, recurring maintenance, and payroll scale. Early cash is tight, Year 3 looks steadier, and Year 5 supports the strongest draw.

Low, base, and high cases show how scale changes owner take-home.

Scenario

Low CaseCash tight

Base CaseScaling

High CaseManaged contractor

Launch model

This is the early-ramp case where owner income stays limited because revenue is still building and cash is tight.

This is the modeled growth case where owner income improves as repeat work and delivery scale up.

This is the stronger earnings path where owner income rises with larger projects and a more mature operating base.

Typical setup

Year 1 revenue is $1.481M, gross margin is about 70%, EBITDA is $131K, marketing is $45K, and the owner is still carrying a lot of delivery work.

Year 3 revenue is $4.445M, gross margin is about 73%, EBITDA is $1.603M, marketing is $85K, and repeat maintenance work starts to matter more.

Year 5 revenue reaches $8.753M, gross margin is 75%, EBITDA is $3.973M, marketing is $135K, and the model runs with more contractor support and reserves.

Cost drivers

Early sales ramp

70% gross margin

$45K marketing

owner-led delivery

tight cash base

Year 3 scale

~73% gross margin

$85K marketing

larger payroll

stronger repeat work

Year 5 scale

75% gross margin

$135K marketing

higher reserves

managed contractor

Owner income rangeBefore owner reserves

$145K salary, thin drawLean draw

$145K salary, mid drawCore draw

$145K salary, strong drawUpside draw

Best fit

Use this to test survival if sales ramp slowly and cash stays tight.

Use this as the main planning case for a growing mix of installs and recurring service.

Use this to test upside if project flow stays strong and reserves keep up.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions.

In this model, the owner has a $145,000 annual payroll salary The business adds EBITDA of $131,000 in Year 1 and $3973 million by Year 5, but that is not the same as cash the owner can take Reserves, payroll, debt service, capex, and reinvestment come first

The model reaches breakeven in Month 7 and payback in 19 months Cash is still tight before that, with minimum cash need of $504,000 in Month 6 That means the owner should plan payroll carefully and avoid early distributions until billing, collections, and project delivery stabilize

Commercial façade work helps because the modeled Year 1 project math is $78,750, compared with $22,200 for residential installation But larger jobs also bring longer sales cycles, engineering review, subcontractor coordination, and working-capital strain Owner income improves only when those projects close, finish, and collect on schedule

Gross margin, crew utilization, and cash timing matter most Year 1 direct costs equal 30% of revenue, leaving about 70% gross margin before payroll and overhead A few bad estimates, delayed materials, or rework events can quickly reduce EBITDA and limit owner distributions, even when top-line revenue looks strong

The best-paid owner usually sells, scopes, and manages project risk instead of staying only in field work In this model, payroll expands from $605,000 in Year 1 to $1765 million in Year 5, so the owner’s job shifts toward pipeline quality, margin control, crew scheduling, and cash management

About the author

Stephen Knight

Business Idea Researcher

Stephen Knight is a business idea researcher at Financial Models Lab who focuses on revenue and profit basics for founders building a simple business plan. He breaks down business model overviews in plain English, helping non-finance readers understand what it really takes to open a physical location and turn an idea into a workable plan.

Choosing a selection results in a full page refresh.