Owner income$95k+

Owner income$95k+How Much Cabinet Refacing Owners Make: $95K Salary Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$95k+  Net margin51%–65%

Net margin51%–65% Revenue for target pay$187k

Revenue for target pay$187k Business difficultyMedium

Business difficultyMedium

<

div class="step-circle step4">4

A cabinet refacing business owner can model income as a salary plus possible profit distributions, not as revenue In the provided plan, the General Manager role is paid $95,000 per year, while the business shows $1183M Year 1 EBITDA before taxes, debt service, capex, reserves, and reinvestment Year 1 revenue is $2326M, rising to $9257M by Year 5 under the researched assumptions Owner take-home depends most on completed jobs, average ticket, 705% Year 1 contribution margin before payroll and fixed overhead, lead cost, crew capacity, and cash reserves

Owner income$95k+Net margin51%–65%Revenue for target pay$187kBusiness difficultyMediumWant to test your cabinet refacing owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It uses the model’s Year 1 project mix, costs, and owner-manager pay as a starting point.

Want to check owner income in the Cabinet Refacing Service model?

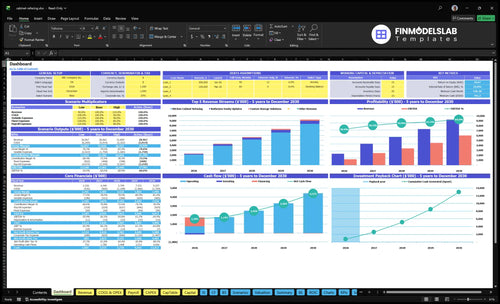

The dashboard shows revenue, EBITDA, breakeven, payback, IRR, ROE, and minimum cash; open the Cabinet Refacing Service Financial Model Template.

Owner-income model highlights

- Owner income: cash and reserves

- Revenue: $2,326M to $9,257M

- EBITDA: $1,183M to $6,011M

- Assumptions: prices, hours, CAC

- Scenarios: hiring and cash flow

Should the owner install, hire crews, or subcontract cabinet refacing work?

If you're deciding how to scale Cabinet Refacing Service, the short answer is this: owner-installed work protects early cash, employee crews improve control, and subcontractors add capacity but can فشار margins and quality. The model points to growth from $2.326M in Year 1 revenue to $9.257M in Year 5, so the install setup has to match lead flow, callbacks, and owner take-home goals.

Owner start

- Protects early cash.

- Caps job volume.

- Makes sales coverage harder.

- Fits low lead flow.

Scale with crews

- Year 1 installer payroll: $120,000.

- Adds scheduling control.

- Sets quality standards.

- Use subs to add capacity.

Is cabinet refacing profitable for an owner?

Yes — Cabinet Refacing Service can be profitable for an owner because the work is repeatable and less complex than full cabinet replacement. Year 1 revenue is $2,326M and EBITDA is $1,183M before taxes, debt service, capex, reserves, and owner distributions, but profit still comes down to price discipline, door and hardware costs, installer productivity, rework, CAC, and close rate.

Profit drivers

- Repeatable scopes lower job chaos.

- Lower complexity than full replacement.

- Materials are 23% of revenue.

- EBITDA is $1,183M before owner draws.

Cost risks

- Variable lead plus fuel costs are 65%.

- Door and hardware costs can squeeze margin.

- Installer productivity changes profit fast.

- Rework, CAC, and close rate drive owner economics.

How many cabinet refacing jobs per month are needed for owner income?

For a Cabinet Refacing Service, plan on about 15 jobs per month to cover fixed overhead, Year 1 payroll, and a separate $95,000 owner pay target; see What Are Operating Costs For Cabinet Refacing Service? for the cost base behind the math. Here’s the quick math: $38,633 monthly cash need ÷ $2,733 contribution per job = 14.1 jobs, rounded to 15.

Job Target

- Weighted project price: $3,876

- Contribution margin: 70.5%

- Contribution per job: $2,733

- Owner-income break-even: 15 jobs/month

Cost Load

- Fixed overhead: $7,800/month

- Year 1 payroll: $22,917/month

- Owner pay load: $7,917/month

- Modeled revenue implies about 50 jobs/month

Owner-installed work changes both payroll and capacity, so the 15-job target can move if the owner replaces paid labor or becomes the production bottleneck.

Want to see the cabinet refacing income drivers?

1

600 jobsCompleted Jobs

About 600 Year 1 jobs spread the fixed base over more revenue, so owner take-home climbs faster than sales.

2

70.5%Gross Margin

Year 1 contribution is about 70.5% after materials, lead fees, and fuel, so small cost slips hit cash fast.

3

$3.9KAverage Project

Year 1 projects average about $3,876, so bigger kitchens and add-on work lift income without the same sales effort.

4

$450 CACLead Close

Customer acquisition cost is about $450, so better targeting and close rate cut waste and protect take-home.

5

32 hrsInstall Capacity

Each active customer uses about 32 billable hours a month in Year 1, so labor capacity sets the ceiling on deliverable revenue.

6

$7.8KOverhead Reserve

Fixed overhead runs about $7,800 a month, plus a $95,000 owner-manager salary, so reserve discipline keeps cash from getting tight.

Cabinet Refacing Service Core Six Income Drivers

Completed Job Volume

Completed Job Volume

Income here comes from completed and collected jobs, not estimates or raw leads. At 50 weighted jobs per month with $3,876 average project value, Year 1 revenue is about $193,800 per month, or $2.326M a year. Here’s the quick math: $3,876 × 70.5% ≈ $2,733 contribution per job before payroll and fixed overhead.

That matters because the same $7,800 monthly fixed base gets spread across more finished jobs as volume rises. The risk is timing: install delays, punch lists, material lead times, and poor scheduling slow cash collection and push profit into later months. One late job can hurt owner pay even when the pipeline looks full.

Track Completed, Not Just Sold

Measure the full funnel: leads, wins, starts, completions, and collections. The real driver is the gap between what is sold and what is finished and paid. If completions lag, the business may look busy but still miss cash, margin, and owner draw.

- Count completed jobs monthly.

- Track days to collect cash.

- Log punch-list rework hours.

- Watch material lead times.

- Protect install schedules daily.

More clean completions raise take-home income because they spread overhead and payroll across more billable work. Fewer delays mean faster collection, steadier cash flow, and less strain on owner pay.

1

Average Project Size

Average Project Size

Average project size is the dollars per completed job, and it moves owner income fast. In Year 1, the modeled mix gives $5,000 kitchen refacing, $1,320 vanity updates, and $1,120 custom storage, for a weighted average of $3,876. Bigger kitchens, premium doors, drawer fronts, soft-close hardware, trim, and custom storage lift revenue per job without adding a new sale.

That matters because each extra dollar flows through after variable costs. If the team pushes unwanted scope, close rate can slip and cash comes in slower. The right test is simple: raise ticket size with useful upgrades that protect margin and still feel like a better result for the homeowner.

Track Mix and Upsell Quality

Measure project size by job type, add-on rate, and average billed dollars per closed job. Split the mix between kitchen refacing, vanity work, and storage so you can see which jobs pull the average above $3,876. Here’s the quick math: if larger kitchens and hardware add $500 to $1,000 per job, that lifts revenue and profit only if labor and rework stay controlled.

- Track sold price by project type.

- Track add-ons sold per job.

- Track labor hours versus ticket size.

- Protect margin on custom scope.

Use upsells to add value, not pressure. The best way to grow owner pay is to price the scope cleanly, document what is included, and forecast cash from the actual mix, not the highest quote on the board.

2

Gross Margin Control

Gross Margin Control

Cabinet refacing margin comes from what you charge versus doors, drawer fronts, veneer, hardware, finishing supplies, labor, delivery, rework, and warranty callbacks. In the model, materials are 23% of revenue in Year 1 and improve to 19% by Year 5, so every point of waste or discount hits owner pay fast. Small leaks repeat on every project.

Here’s the quick math: if custom work is underpriced or callbacks rise, gross profit shrinks before fixed overhead and owner draw. The model also shows a stated Year 1 contribution margin after direct lead fees and fuel of 705%, so margin control is the guardrail on take-home income. One sloppy install can erase profit from a clean sale.

Protect Job Margin

Price each job from a line-item takeoff, not a flat guess. Track quote price, labor hours, delivery, and callback cost by project. If a quote can’t hold margin after 23% materials, raise price or cut scope. That keeps cash available for payroll, overhead, and owner draw.

Watch rework and warranty calls weekly. Underpriced custom work is the biggest leak, and it compounds across every project. Use the same install steps, sign-off checklist, and change-order rules on every job so the margin holds from first quote to final payment.

- Track margin by job line item.

- Separate custom work from standard work.

- Log callbacks and rework dollars.

- Reprice scope creep before install.

3

Lead Cost And Close Rate

Lead Cost And Close Rate

This driver is cost per sold job, not lead count. With a $45,000 Year 1 marketing budget and $450 CAC (customer acquisition cost), the model assumes about 100 customers acquired. If close rate slips, the same spend buys fewer sold jobs, so revenue, gross profit, and owner draw all fall even if lead volume looks strong.

Direct project marketing and lead fees also run at 4% of Year 1 revenue, so weak conversion hits twice: higher spend per sale and more overhead tied to demand generation. By Year 5, CAC improves to $350, which frees cash only if close rates hold and sold jobs stay profitable after labor, materials, and callbacks.

Track cost per sold job

Track each source by close rate and gross profit per sold job: referrals, local search, showroom visits, and in-home estimates. That tells you which channel earns the best jobs, not just the most leads. One clean rule: if a channel adds leads but lowers gross profit, cut it or tighten the sales process.

Use simple formulas: CAC = marketing spend ÷ closed customers, and cost per sold job = spend ÷ sold jobs. Watch these weekly, plus estimate-to-close time and no-show rate. If showroom traffic is high but closing is weak, fix follow-up, price clarity, and proposal speed before raising spend.

Installation Capacity

Installation Capacity

When install slots run out, demand stops turning into cash. In year 1, the base crew is one lead installation carpenter at $75,000 plus one apprentice at $45,000, so the first $120,000 of wages buys output control, but it also caps how many jobs can be finished and billed each month.

Here’s the quick math: the model’s average job is $3,876, and the implied contribution is about $2,733 per completed job before payroll and fixed overhead. Owner labor can protect early margin, but it also steals time from selling, estimating, and managing; if installs slip, cash slips too.

Track install backlog weekly

Measure booked jobs, open install days, and average days from sale to finish. One clean rule: if the crew cannot close the backlog fast enough, revenue is capped no matter how strong lead flow is. Also watch callback hours and punch-list days, because rework eats margin and delays collection.

As revenue scales from $2.326M to $9.257M, add installers before the schedule breaks. Employees improve control, while subcontractors can speed work but raise margin and callback risk, so compare each option by completed jobs per labor dollar, not just wage cost.

5

Overhead And Cash Reserves

Cash Before Owner Pay

Profitable jobs do not mean cash is ready for owner take-home. This model has $7,800 a month in fixed operating expenses and $275,000 in Year 1 payroll before any separate owner distribution if the owner is not the general manager, so cash can stay tight even when projects look strong.

The reserve target is $791,000 in Month 2. That buffer protects deposits, warranty work, hiring, and reinvestment, and it keeps vendors and payroll current when job timing slips or collections land later than expected.

Hold a Reserve Floor

Track cash by month, not just profit by job. Keep a floor that covers fixed overhead, payroll, and planned capital spending before any owner draw. If cash drops under $791,000, pause distributions and slow hiring until collections rebuild the balance.

Tie every project forecast to collection timing. A job can be profitable and still squeeze cash if deposits, change orders, and final payment lag while warranty calls and supplier bills hit first.

- Watch monthly cash on hand.

- Separate payroll from owner pay.

- Log capex timing before spending.

- Set a warranty reserve.

- Track deposit-to-final-payment lag.

6

Compare lean, base, and high-output cabinet refacing owner pay scenarios

Owner income scenarios

Owner income shifts with jobs per month, average ticket, margin, and payroll. These cases map Year 1, Year 3, and Year 5 operating assumptions for a cabinet refacing service.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | Year 1 is the lower earnings path, built from $2.326 million revenue and $1.183 million EBITDA. | Year 3 is the modeled middle path, with $5.709 million revenue and $3.412 million EBITDA. | Year 5 is the stronger earnings path, with $9.257 million revenue and $6.011 million EBITDA. |

| Typical setup | About 50 jobs a month at a roughly $3.9k average ticket, 70.5% contribution margin, 23% materials, $7.8k monthly overhead, $275k payroll, and a reserve for the Month 2 cash dip. | About 127 jobs a month at a roughly $3.7k average ticket, 73.7% contribution margin, 21% materials, $7.8k monthly overhead, and $520k payroll. | About 214 jobs a month at a roughly $3.6k average ticket, 76.9% contribution margin, 19% materials, $7.8k monthly overhead, and $715k payroll. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $1.18M EBITDAYear 1 case | $3.41M EBITDAYear 3 case | $6.01M EBITDAYear 5 case |

| Best fit | Best for owners stress-testing slow lead flow, harder installs, and a tighter reserve. | Best for operators planning a steady scale-up with a larger crew. | Best for teams testing a high-output shop that can keep crews busy and CAC falling. |

Planning note: Ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions. EBITDA is before taxes, debt service, capex, and owner distributions.

Related Products

- Cabinet Refacing Service Porter's Five Forces Analysis

- Cabinet Refacing Service BCG Matrix

- Cabinet Refacing Service Business Model Canvas

- What Are The 5 KPIs For Cabinet Refacing Service Business?

- Cabinet Refacing Business Plan Template in Pre-Written Word

- How Increase Cabinet Refacing Service Profitability?

- What Are Operating Costs For Cabinet Refacing Service?

- Cabinet Refacing Startup Costs: $1515K CAPEX And $791K Cash

- Cabinet Refacing Financial Model Template in Excel

- How To Start A Cabinet Refacing Business In 6 To 12 Weeks

- How To Write A Business Plan For Cabinet Refacing Service?

- Cabinet Refacing Service Marketing Mix

- Cabinet Refacing Service Marketing Plan

- Cabinet Refacing Service Business Proposal

- Cabinet Refacing Service PESTEL Analysis

- Cabinet Refacing Pitch Deck Example Editable PPTX

- Cabinet Refacing Service Business SWOT Analysis

- Cabinet Refacing Service Value Proposition Canvas

Frequently Asked Questions

In this plan, the owner can model $95,000 as General Manager salary plus possible distributions from profit The business shows $2326M Year 1 revenue and $1183M Year 1 EBITDA That EBITDA is not automatic take-home because taxes, debt service, capex, reserves, and reinvestment still come first