How Much Does a Call Center Owner Make? $130k Salary Plus Profit

Call Center Bundle

You’re estimating owner take-home, not employee call center wages This view uses a first-year to mature-year US call center model with $130,000 CEO pay, agent payroll, contract revenue, telecom, software, rent, marketing, and reserves kept separate

Owner income$130kNet margin393%Revenue for target pay$1.07MBusiness difficultyHard

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full Call Center model?

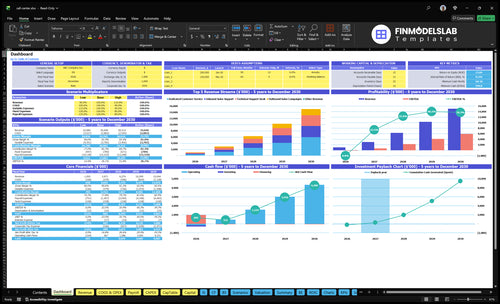

This dashboard shows revenue, payroll, gross margin, operating profit, cash flow, and owner take-home assumptions; open the Call Center Financial Model Template. Tabs also cover staffing, contract revenue, active customers, agent and supervisor payroll, telecom, client software, QA tools, fixed overhead, marketing, CAC, capex, and cash reserves; Year 1 break-even is about $107M versus full-year active-customer revenue of about $211M, with payroll scaling from $650k in Year 1 to $4.925M in Year 5.

Owner-income model highlights

Owner take-home scenarios

Revenue and margin tabs

Costs, reserves, capex

How much revenue does a call center need to pay the owner?

A Call Center needs revenue that covers the $130k CEO salary, Year 1 payroll, fixed overhead, and marketing; on the stated inputs, the listed cost stack is $2.278M, and at an 80% contribution margin that implies about $2.85M of revenue before reserves. The prompt also says break-even is about $107M before reserves, so the model should be checked before using it for owner pay. Each extra $100k of owner draw needs at least $125k more revenue if variable cost stays at 20%.

Cost stack

$650k payroll

$1,578k fixed overhead

$50k marketing

$2.278M total before margin

Owner pay math

80% contribution margin

$125k revenue per $100k draw

Cash timing can cut distributions

Payment terms and onboarding matter

What call center profit margin is left after payroll?

After payroll, a Call Center’s margin is usually thin at first, because labor is the biggest cost driver. In Year 1, payroll is $650k — including $225k for five agents, $65k for one supervisor, and $130k CEO pay — and non-labor variable costs still take 20% of revenue; the real question is how much paid utilization you can keep on the floor. For the startup cost side, see What Is The Estimated Cost To Open And Launch Your Call Center Business?

Year 1 payroll

$650k total payroll

5 agents cost $225k

1 supervisor costs $65k

$130k CEO pay sits inside payroll

Margin pressure

Non-labor costs start at 20%

Non-labor costs fall to 15%

Wages and overtime cut gross margin

Training, turnover, and QA rework add drag

Which call center business model is most profitable?

No single Call Center model is most profitable; the best one depends on pricing, staffing difficulty, utilization, client retention, and payment terms. Dedicated Customer Service is priced at $3,000 per month in Year 1 and $3,500 in Year 5, while Inbound Sales Support runs $2,500 to $3,000, Outbound Sales Campaigns run $2,800 to $3,300, and Technical Support Desk runs $3,200 to $3,800. Technical support can command a higher price but needs more training and quality control, and outbound sales can add performance upside but carries compliance and churn risk.

Highest price band

Technical Support Desk: $3,200 to $3,800

Higher price, higher training load

Needs tight quality control

Best when expertise is scarce

Profit risk factors

Outbound Sales: $2,800 to $3,300

Can lift upside with performance pay

Compliance risk can hit margins

Retention and payment timing matter

Call Center Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers that decide owner take-home?

1

Contract Pricing

$6.3K-$10.2K

Higher monthly rates push revenue per active customer from $6.3K in Year 1 to $10.2K in Year 5, and that flows into owner take-home after reserves.

2

Billable Utilization

80-120h

Raising billable hours per active customer from 80 to 120 spreads payroll and overhead across more revenue, so margin improves fast.

3

Labor Cost

$650K-$4.9M

Payroll climbs from about $650K in Year 1 to $4.925M in Year 5, so hiring pace and turnover control can swing owner cash hard.

4

Client Retention

Renewals

No churn field is set, so renewal loss can cut revenue density and cash reserves, which hits reserve-adjusted take-home.

5

Service Mix

$3.8K

Selling more technical support at $3,800 a month raises the average contract value and helps owner income.

6

Overhead Efficiency

$13.2K/mo

Keeping fixed overhead near $13.15K a month protects contribution before payroll and marketing take the rest.

Call Center Core Six Income Drivers

Contract Pricing Model

Contract Pricing Model

This driver is the rate card: what you charge per active customer, seat, hour, call, retainer, or campaign. In Year 1, pricing sits around $2,500 to $3,200 per month, and by Year 5 it rises to $3,000 to $3,800; weighted monthly revenue per active customer grows from $6,330 to $10,175 as the service mix shifts.

Hourly and per-seat contracts are easier to forecast, while per-call and performance pricing can lift upside but add volume risk. The owner only takes home more after labor, tools, commissions, and overhead are covered, so a higher price helps only if service intensity stays in line.

Price for Margin

Track pricing by contract type, not just total revenue. Build each quote from active customers, seats, hours, calls, retainers, and campaign volume, then compare the mix against staffing and support cost.

Review price by service line monthly.

Test retainers on stable work first.

Use hourly or per-seat for predictability.

Cap per-call exposure on busy accounts.

Watch payroll before raising volume offers.

If pricing rises faster than labor and overtime, owner pay improves. If the mix shifts toward low-control, high-volume work, cash flow can look strong while profit stays thin.

1

Billable Utilization And Capacity

Billable Utilization And Capacity

Headcount does not equal profit; paid utilization does. In this call center model, average billable hours per active customer rise from 80 in Year 1 to 120 in Year 5, so the same staff can produce more revenue only if seats stay filled and idle time stays low. Here’s the quick math: low utilization spreads $13,150 of monthly fixed overhead over too few paid hours, which cuts owner take-home.

Use agent count, filled seats, scheduled hours, idle time, utilization, and campaign volume to test capacity before selling more work. If acquisition outruns staffing, service slips, overtime rises, and burnout can hurt quality. If utilization is high without buffer, margins may look better, but the hidden cost is missed calls, rework, and churn risk.

Capacity Check Before You Sell More Hours

Track billable hours per agent, idle hours, and seat fill rate each week. The useful test is simple: can current staffing cover the next month’s campaign volume without pushing overtime or quality below target? If not, delay new contracts, raise staffing, or narrow service hours. That keeps fixed overhead from sitting on empty time and protects cash flow.

Measure billable hours per seat monthly.

Flag idle time before it grows.

Match new clients to staffed capacity.

Watch overtime and QA failures.

2

Labor Cost, Turnover, And Training

Labor Cost And Training

Here’s the quick math: with 5 agents at $45,000 each, agent payroll is $225,000. Add 1 supervisor at $65,000, and labor is $290,000 before overtime or hiring waste.

At 80 agents and 10 supervisors, payroll reaches $4.25M using the disclosed salaries. Turnover, slow onboarding, overtime, and QA failures all cut gross margin, so owner take-home only rises if pricing or utilization grows with labor.

Track Labor By Seat

Measure filled seats, attrition, training days, overtime hours, and QA pass rate. That shows whether labor is producing billable work or just absorbing cash.

Count agents and supervisors weekly.

Watch overtime before margin slips.

Track onboarding time to full productivity.

Link wage hikes to higher rates.

If wages rise, the fix is simple: raise contract pricing, improve utilization, or both. Otherwise, the extra payroll comes straight out of operating profit and the owner’s draw.

3

Client Retention And Contract Risk

Client Retention And Contract Risk

Recurring revenue can make owner pay steadier, but contract loss hits fast. Here’s the quick math: marketing budget rises from $50k in Year 1 to $320k in Year 5, while CAC falls from $1,800 to $1,300. If churn is ignored, you can overstate profit because acquisition spend is wasted when clients leave early.

The model needs churn, renewal rate, contract length, and customer concentration. One large client can cover payroll, but a loss can trigger a cash gap, leave trained agents underused, and cut the owner draw. Reserves should cover staffing and the transition period.

Track Retention Before You Scale

Track retention by cohort, not just by month. If a contract renews for 12 months instead of 3, cash is easier to plan, and you can spread onboarding cost over more billed time. Use simple fields for client start date, renewal date, contract term, and share of revenue by client.

Monthly churn rate

Renewal rate by cohort

Revenue share of top client

Reserve months of payroll

Stress-test the top account. If one client drives payroll, set a cash reserve that can cover wages, handoff work, and the time it takes to replace volume. That protects gross margin and keeps owner pay from swinging with one cancellation.

4

Service Mix And Specialization

Service Mix And Specialization

Your income changes when the mix shifts toward higher-value services. Technical Support Desk has the highest listed monthly price at $3,200 in Year 1 and $3,800 in Year 5, while Dedicated Customer Service attachment rises from 85% to 95%. A richer mix can lift revenue per client, but only if labor, training, and QA stay in line.

Here’s the quick math: more Inbound Sales Support (60% to 80%) and Outbound Sales Campaigns (30% to 60%) can raise monthly revenue, but outbound often needs incentives and tighter compliance. Specialized work usually supports higher rates, yet it also raises hiring time, training load, and quality checks, so owner take-home depends on margin after those costs.

Track Mix, Not Just Seats

Measure revenue and gross margin by service line, not just total customers. Track active clients, service attach rate, monthly price, training hours, QA rework, and compliance flags. If a higher-priced mix adds too much onboarding or error handling, the extra revenue can disappear fast.

Price each service separately.

Track labor hours per contract.

Watch outbound incentive cost.

Log QA failures by team.

Use the mix to protect cash flow. A shift toward technical or sales support can improve revenue quality, but if training takes longer or compliance reviews rise, payroll and supervisor time climb too. The owner only feels the upside when the added price covers the added operating load.

5

Overhead Efficiency And Management Structure

Fixed Overhead and Span of Control

Fixed overhead is the monthly cost that stays in place before agent labor: $13,150 a month, including $6,500 rent, $2,000 software, $1,500 accounting and legal, $1,200 utilities and internet, $750 insurance, $800 training, and $400 supplies. That cost hits owner pay even when call volume is light, so low revenue spreads the same overhead across too few billable hours.

Management layers matter too. Headcount grows from one operations manager to two and one sales manager to two by Year 5, so profit only improves when revenue grows faster than supervisors, admin, tools, and rent. If overhead climbs before revenue does, cash gets tight fast.

Track Overhead per Revenue Dollar

Measure overhead as a share of monthly revenue and separate it from agent payroll. Here’s the quick math: start with $13,150, then add software, telecom, QA tools, and sales spend that scale with revenue. Watch whether each new manager is tied to higher billable volume or better close rates; if not, the structure is too heavy.

Track overhead by cost bucket.

Watch revenue per manager.

Test tools against billable hours.

Delay hires until volume needs them.

Build the forecast around rent, admin, and supervisor count, not wishful growth. The owner’s take-home rises when monthly revenue covers fixed overhead plus variable operating costs and still leaves room for profit draw. If onboarding takes too long or sales lag, the same overhead can erase the month’s margin.

6

Call Center Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and mature call center owner-income scenarios

Owner income scenario table

Owner income changes fast as marketing spend, CAC, staffing, and fixed overhead move at different speeds. The low, base, and high cases show where capacity and cash reserves get tight.

Low, base, and high cases show how staffing and acquisition costs change owner income.

Scenario

Low CaseReserve need

Base CasePayroll risk

High CaseCapacity risk

Launch model

This is the lower earnings path, built on Year 1 inputs and a slow ramp.

This is the modeled middle path, using Year 3 inputs and steadier volume.

This is the stronger earnings path, built on Year 5 volume and tighter acquisition economics.

Typical setup

Year 1 uses $50k marketing, $1,800 CAC, about 28 acquired customers, and about $650k payroll, with fixed overhead and non-labor costs still heavy.

Year 3 uses $180k marketing, $1,500 CAC, about 120 acquired customers, and about $2.1M payroll as billable hours and service mix improve.

Year 5 uses $320k marketing, $1,300 CAC, about 246 acquired customers, and about $4.9M payroll, with higher billable hours and lower CAC.

Cost drivers

Year 1 CAC

$50k marketing

$650k payroll

fixed overhead

non-labor costs

Year 3 CAC

$180k marketing

$2.1M payroll

billable hours

customer mix

Year 5 CAC

$320k marketing

$4.9M payroll

billable hours

capacity limits

Owner income rangeBefore owner reserves

-$115kLoss year

$2.3MCore case

$5.9MUpside case

Best fit

Use this if you want a stress test for launch speed and reserve needs.

Use this for the main planning case and the most likely operating mix.

Use this to test scale limits, hiring pace, and reserve needs.

!

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The model includes $130,000 annual CEO pay for an owner-operator role Additional take-home depends on operating profit after reserves, debt service, and cash needs In Year 1, break-even revenue is about $107M before reserves, and full-year active-customer math shows about $211M revenue if acquisition and capacity hold

Profitability depends on filling paid capacity fast enough to cover payroll Year 1 payroll is $650k, fixed overhead is $1578k, and marketing is $50k With 20% non-labor variable costs, the business needs about $107M in annual revenue before reserves just to cover those modeled costs

This model includes an office setup with $6,500 monthly rent, $1,200 utilities and internet, and $2,000 general software subscriptions A remote setup may lower rent, but it can raise security, monitoring, training, and IT needs Compare total overhead, not just rent, before changing the operating model

Payroll, utilization, and contract pricing drive owner pay fastest Agent payroll starts at $225k in Year 1 and reaches $36M in Year 5 Weighted monthly revenue per active customer rises from $6,330 to $10,175 If paid utilization drops, those gains can disappear quickly

The best model is the one you can staff, price, and retain well Technical support has the highest listed price, from $3,200 to $3,800 monthly, but it can need more training and QA Outbound sales may add upside, while customer service can support steadier recurring revenue

About the author

William Hayes

Small Business Consultant

William Hayes is a small business consultant at Financial Models Lab who writes for early-stage founders building a basic plan before investing money. He focuses on business plan basics and practical everyday business finance, helping readers use realistic assumptions to understand revenue, expenses, and profit in simple terms. His direct, useful approach is designed to give new founders a clearer path from idea to informed decision.

Choosing a selection results in a full page refresh.