How Much Does a Car Modification Shop Owner Make on $142M Sales

Key Takeaways

Finished profitable jobs drive revenue, not booked work.

Labor profit depends on scheduling and bay utilization.

Parts markup must cover handling, warranty, and cash.

Fixed overhead is $91k monthly, so throughput matters.

Owner income$708kNet margin49.9%Revenue for target pay$1.42MBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on demand, margin, payroll, reserves, financing, and timing.

How do I check owner income in the Car Modification Shop model?

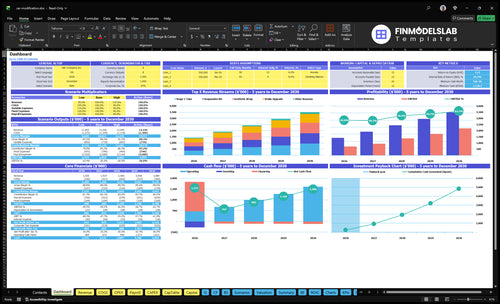

See this Car Modification Shop Financial Model Template screenshot: revenue, margin, costs, reserves, and owner take-home assumptions. Dashboard shows $142M revenue, $8,998k owner cash, 888% gross margin, and 634% after costs.

Owner-income model highlights

Owner cash at year one

Revenue and gross margin

Scenarios change inputs fast

How does owner operated car modification shop income change?

For a Car Modification Shop, owner income usually rises fastest when the owner sells and manages work flow, but it is not passive. An owner-as-technician can cut payroll, yet it can cap sales, scheduling, and quality control; an owner-as-salesperson can lift average ticket and close more packages, while technicians keep bays moving. First-year payroll already includes $85k for a lead technician and $60k for one technician, so if the owner pulls cash too early, equipment, warranty, and parts reserves get squeezed.

Owner in the bay

Lower payroll, but less sales time

More control over rework and fit

Can cap daily ticket growth

Best when skill depth is high

Owner off the bay

More time to sell packages

Higher average ticket is possible

Technicians keep bays moving

Absentee ownership raises quality risk

How much revenue does a car modification shop need to pay the owner?

To pay the owner $100,000 before tax in year one, the Car Modification Shop needs about $435,700 in revenue. Here’s the quick math: after cost of goods sold (COGS) and variable fees, the shop keeps about 81.3% of sales as contribution, and with a first-year average ticket of $2,367, that works out to about 184 jobs a year, or 15 a month.

Revenue math

$435,700 revenue target

$354,200 contribution dollars

81.3% post-COGS margin

184 jobs per year

What pushes it higher

$254,200 fixed overhead plus payroll

15 jobs per month is the floor

Reserves reduce owner cash fast

Taxes, debt, slow collections add pressure

What are the most profitable car modification services?

If you’re choosing what to sell in a Car Modification Shop, there isn’t one always-best service; profitability depends on skill, pricing, supplier terms, local demand, and rework risk. On the numbers provided, brake upgrades lead with about $3,973 gross profit per job, and you can see the setup cost context here: How Much Does It Cost To Open A Car Modification Shop?

The catch is capacity: high-ticket jobs can lock bays, use more parts cash, and create comeback risk, so the top gross profit job is not always the best cash job.

Top earners

Brake upgrades: $3,973 per job

Wraps: $3,488 per job

Suspension kits: $2,923 per job

Tunes: $2,373 per job

Risk check

Dyno sessions: only $276 per job

Reported tune margin: 949%

Reported dyno margin: 920%

High-ticket work can tie up bays

What drives owner take-home most?

1

Ticket Mix

$2.37K

At 600 jobs in year 1, the mix lands near a $2,367 average ticket, so small shifts in service mix move revenue fast.

2

Labor Utilization

600 jobs

The model pays on finished jobs, so keeping tech time billable—not just busy—turns labor into owner cash.

3

Parts Terms

4.6%-16%

Material cost runs from 4.6% on a tune to 16% on a suspension kit, so markup and supplier terms shape take-home.

4

Shop Throughput

50/mo

Year 1 averages 50 jobs a month, so every extra slot you fill lifts sales without much extra fixed cost.

5

Rework Control

Margin

Rework and warranty issues eat margin fast, so clean installs keep the cash from each ticket in the shop.

6

Fixed Overhead

$34.7K/mo

Recurring fixed spend is about $34.7K a month in year 1, so reserves matter when volume dips or payroll steps up.

Car Modification Shop Core Six Income Drivers

Job Mix and Average Ticket

Job Mix and Ticket Size

Booked work doesn’t pay; finished, collected jobs do. With 600 jobs at a $2,367 average ticket, revenue works out to about $1.42M (600 × $2,367 = $1,420,200). Higher-ticket jobs like $4,500 brake upgrades and $4,000 wraps grow revenue faster than $300 dyno sessions.

Owner take-home rises when the shop closes more profitable jobs without rework, delays, or unpaid change orders. Small installs keep cash moving, but full builds can tie up bays and parts cash, so mix matters as much as volume. Fast, clean completion is what turns a big ticket into real profit.

Measure Ticket Quality

Track completed jobs, average ticket, gross margin per job, and days to collect. Here’s the quick math: revenue = completed jobs × average ticket, so a better mix can lift income even if job count stays flat.

Split jobs by package type

Log change orders before start

Price rework before approval

Compare bay days by job type

Push more high-ticket work only if scheduling, parts readiness, and final checks stay tight. If a $4,500 job runs long, it can hurt owner pay more than several fast $300 jobs that bill cleanly.

1

Labor Rate and Billable Hours

Billable Labor Rate and Hours

Billable labor is the time you charge the customer, not the time techs sit on payroll. With $145k in first-year payroll for one lead technician and one technician, owner income improves only when paid hours turn into finished tickets. If jobs stall on parts or scheduling, the posted labor rate won’t save margin.

The quick math is simple: more billed hours per paid hour means better gross profit per payroll dollar. That matters here because underused bays still carry $91k in monthly fixed overhead, so idle time cuts cash flow fast. One clean line: billed hours pay the bills, clock hours do not.

Track Labor Utilization, Not Just Rate

Use utilization, which means the share of paid technician time that gets billed. Track billed hours, clock hours, labor collected per ticket, and the hours jobs sit waiting on parts or approval. If a bay is open but the job is unfinished, you still pay wages and overhead without getting the labor revenue.

Schedule parts-ready jobs first.

Measure billed hours per tech.

Cut rework and comeback time.

Pre-kit common install parts.

Train for faster, cleaner installs.

Use the labor rate to price the work, but use scheduling and readiness to protect the margin. If demand is strong but jobs sit half-done, the shop can look busy and still miss owner pay. Better flow turns the same payroll into more completed tickets and stronger cash.

2

Parts Markup and Supplier Terms

Parts Markup

Parts sales raise top-line revenue, but they only help owner pay when markup covers freight, warranty exposure, and cash tied up in inventory. In the first-year model, modeled parts COGS per job includes about $12,750 for tunes, $512 for wraps, $57,750 for suspension kits, $527 for brake upgrades, and $24 for dyno sessions. If markup is thin, gross profit gets eaten fast.

Customer-supplied parts can keep the bay busy, but they lower parts margin, so the shop must still earn enough on labor to protect take-home. Here’s the quick math: higher parts margin lifts cash only if collection is fast and returns are rare. If special orders or backordered parts delay the job, cash gets trapped before the ticket closes.

Control Supplier Terms

Track landed cost per job, not sticker price. Landed cost means parts cost plus freight, returns, and any rush charges. Use simple job costing by service type, then compare actual cost to selling price on tunes, wraps, suspension, brake work, and dyno sessions. If a job’s parts margin can’t cover handling and risk, raise price or change the package.

Watch supplier lead times weekly.

Quote freight before final approval.

Charge for special orders upfront.

Set rules for customer-supplied parts.

Reserve cash for returns and delays.

When terms are tight, owner income improves because less cash sits in unpaid inventory and fewer jobs slip on delivery. The goal is not cheap parts; it’s clean margin and fast collection. If the shop buys parts early, it should collect early too, or the owner ends up financing the build.

3

Capacity and Shop Throughput

Capacity Drives Cash

Capacity is the ceiling on finished, collected work. For a custom shop, that means bays, lifts, tools, technician count, parts on hand, and how long each job stays open. With 50 completed jobs per month, throughput is only 1.7 finished jobs per day, so every delay pushes cash out. Backlog only helps income when the job ships and the invoice gets paid.

Long jobs like wraps and suspension kits can block bay space longer than dyno sessions, so the real risk is not booked demand, it’s slow conversion to cash. Watch the choke points: alignment, tuning, and final inspection. If those steps stack up, owner pay falls even when the schedule looks full.

Track Cycle Time, Not Just Bookings

Measure days in bay, jobs waiting on parts, and jobs stuck at alignment, tuning, or final inspection. A simple WIP board (work in progress tracker) should show each job’s stage, owner, and due date so the team can clear the oldest work first. The goal is to shorten turnaround without cutting quality.

Split throughput by job type, because a fast dyno session does not tell you much if a wrap or suspension build is tying up space. If the shop finishes more jobs with the same bays and headcount, monthly cash rises faster and the owner can draw from collected profit, not from unfinished work.

4

Rework and Warranty Control

Rework Cost

Rework hits income fast because the shop pays twice for labor, supplies, and bay time on the same job. Common leak points are fitment, electrical troubleshooting, tuning complaints, brake noise, wrap defects, and suspension alignment. One free comeback can wipe out the margin on a small install and delay cash for the next ticket.

Here’s the quick math: if the shop finishes 50 jobs per month and even 5% need rework, that is about 2 to 3 jobs done twice. That cuts owner take-home because unpaid hours replace billable work, and it gets worse when fixed overhead is already $91k per month.

Cut Warranty Leaks

Track rework rate, warranty hours, and parts replaced at no charge by job type. Keep photos, test drives, checklists, and customer signoffs in the file before delivery. One clean rule: if it is not documented, it is hard to defend.

Log the failure reason every time.

Check fitment before final install.

Road test tuning and suspension jobs.

Get signoff on known trade-offs.

Use that data to price risky jobs higher or slow the schedule when repeat fixes rise. The goal is not zero defects; it is fewer unpaid hours so gross profit turns into stable owner draw.

5

Fixed Overhead and Reserves

Fixed Overhead and Reserves

Your shop carries $91k per month in fixed overhead, led by a $65k garage lease. Add $800 electricity, $300 water and gas, $450 liability insurance, $150 hosting, $200 client software, and $700 accounting and legal, and annual fixed overhead reaches $1,092k before payroll. That means owner pay only works if gross profit reliably clears this base.

Reserves matter because this business also needs cash for equipment, tools, warranty claims, slow parts, and cash gaps. Here’s the quick math: even a strong sales month can still squeeze owner draw if cash is tied up in parts or rework. Separate true owner pay from reinvestment cash, or the shop can look profitable and still run tight.

Track Cash Before You Pay Yourself

Measure fixed overhead as a percent of collected revenue, not booked work. The key inputs are completed jobs, average ticket, gross margin, parts timing, and payroll. If revenue slips or collections lag, the lease alone is $65k a month, so owner draw should stay below the cash left after overhead and reserves.

Build a reserve rule and keep it separate from pay. Track these buckets:

Lease and utilities due each month

Warranty and rework cash set aside

Slow parts and freight holds

Equipment and tool replacements

Owner draw after reserves

6

Compare low, base, and high owner-income cases

Owner income scenarios

Owner income moves with job mix, ticket size, and staffing. More work lifts cash fast, but labor-heavy installs and fixed shop costs can cap the owner's take.

Compare low, base, and high owner cash cases.

Scenario

Low CaseEasy

Base CaseBase

High CaseStretched

Launch model

It models a lower path where about 184 jobs and roughly $435k of revenue support about $100k of before-tax owner cash.

It uses first-year assumptions: 600 jobs, about $1.42M of revenue, and about 88.8% gross margin before fixed labor and overhead.

It uses third-year volume: 960 jobs, about $2.44M of revenue, and about 89.3% gross margin with higher technician staffing.

Typical setup

The shop stays small, uses the first-year average ticket, and keeps payroll and overhead tight.

It assumes the full first-year mix, steady throughput, and the modeled shop staffing load.

It assumes a fuller bay schedule, more technicians, and the same fixed shop costs spread over more work.

Cost drivers

Job count

average ticket

fixed overhead

payroll

service mix

Job count

average ticket

gross margin

payroll

fixed overhead

Job count

third-year volume

technician staffing

gross margin

fixed overhead

Owner income rangeBefore owner reserves

$100k before taxLow case

$800k-$900k before taxBase case

$1.6M-$1.7M before taxHigh case

Best fit

Use this to test the minimum work level that still pays the owner.

Use this as the planning baseline for pricing, staffing, and cash needs.

Use this to test upside if the shop fills bays and keeps throughput high.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.