Owner income$95k

Owner income$95kHow Much Cement Grouting Service Owners Make With $25M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$95k  Net margin54%-66%

Net margin54%-66% Revenue for target pay$208k/mo

Revenue for target pay$208k/mo Business difficultyHard

Business difficultyHard

You’re pricing heavy field work before cash is steady, so owner pay has to sit behind revenue, crew payroll, materials, equipment, insurance, and reserves This page estimates cement grouting business revenue, expenses, margins, and owner take-home across a five-year model period, using Year 1 revenue of $2495M and Year 2 revenue of $4986M It does not promise wages, distributions, financing terms, or personal tax outcomes

Owner income$95kNet margin54%-66%Revenue for target pay$208k/moBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice, and it excludes personal taxes, financing guarantees, and one-time startup costs unless separately modeled.

Want to see owner take-home in the full forecast?

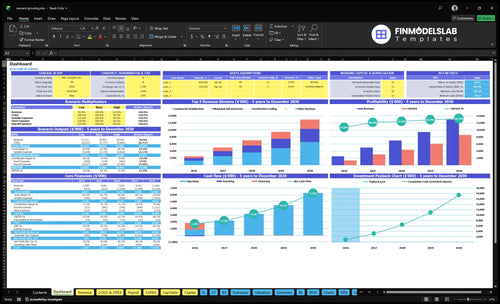

This screenshot shows revenue, gross margin, payroll, capex, cash flow, reserves, and owner pay in the Cement Grouting Service Financial Model Template; open it.

Owner-income model highlights

- Owner pay stays visible

- Year 1: $2.495M revenue

- Year 2: $4.986M revenue

- Month 2: $737k cash

- Startup capex: $145k

How much revenue does a cement grouting business need to pay the owner?

A Cement Grouting Service needs about $603k in annual revenue, or roughly $50k a month, to cover Year 1 overhead before owner distributions. The math starts with a 73% contribution margin after 27% variable costs. Every extra $10k of pre-tax owner pay needs about $137k more annual revenue, and debt service, reserves, and taxes push the true target higher.

Break-even math

- 73% contribution margin stays after costs.

- $50k per month covers core overhead.

- $603k per year is the break-even line.

- Owner pay comes after that base level.

Owner pay impact

- $10k more pay needs $137k more revenue.

- 27% of sales go to variable costs.

- Debt service raises cash needs further.

- Taxes and reserves also lift the target.

How much can a cement grouting business owner make per year?

A Cement Grouting Service owner doesn’t earn a fixed salary; if you run daily operations, you can take the modeled $95,000 General Manager pay, then take distributions only if cash flow allows. For startup context, see How Much To Start Cement Grouting Service Business?; the model shows $2.495M Year 1 revenue with about $1.38M pre-tax operating profit, and $4.986M Year 2 revenue with about $3.10M pre-tax operating profit before debt, taxes, reserves, and owner distributions.

Owner Pay

- Owner-operator salary: $95,000

- Managed-crew owner may skip salary

- Distributions depend on free cash

- Year 1 modeled margin: 55.3%

Take-Home Limits

- Reserve cash for callbacks

- Plan taxes before distributions

- Debt service reduces owner cash

- Year 2 modeled margin: 62.2%

Can a cement grouting business scale beyond the owner-operator model?

Yes, Cement Grouting Service can scale past the owner-operator model, but the tradeoff is more management load. In the model, staff grows from 1 lead injection technician and 1 assistant in Year 1 to 2 of each in Year 2, revenue rises from $2.495M to $4.986M, and payroll rises from $279.5k to $409k. Here’s the catch: scale helps dollars, but it can pull down margin if rework, debt, or supervision grows faster than jobs.

Year 1 to Year 2

- Revenue doubles to $4.986M

- Payroll climbs to $409k

- Utilization improves from 176% to 117%

- More crews need tighter scheduling

What breaks first

- Quality control gets harder fast

- Equipment capacity becomes a bottleneck

- Sales pipeline must stay deep

- Callback discipline protects margin

Want the six levers that drive owner income?

1

$208K-$416K/moJob Volume

More booked jobs and higher utilization lift revenue fast, and the model shows monthly revenue roughly doubles from Year 1 to Year 2.

2

$220-$420/hrProject Size

Shifting mix toward commercial and municipal work raises billed hours and improves take-home because those jobs price higher than residential leveling.

3

$280KCrew Productivity

Keeping payroll tight while crews complete more field hours turns labor into profit instead of letting wage cost outrun revenue.

4

19%Material Control

Cement, grout, fuel, and consumables run at about 19% combined in Year 1, so small savings drop straight to EBITDA.

5

$395KOverhead Utilization

The model carries about $395K a year in fixed pay and overhead, so better dispatch and admin coverage spread that cost over more billable hours.

6

ReserveWarranty Risk

Callbacks and rework can eat billable capacity, so thin reserves cut owner income even when top-line sales look fine.

Cement Grouting Service Core Six Income Drivers

Job Volume And Crew Utilization

Billable Job Volume

This driver is the share of crew, pump, and schedule time that turns into billable work. With Year 1 revenue at $2.495M, or about $208k per month, more jobs only help if weather, permits, site access, and downtime do not block production. At a weighted rate of $260.50 and 85 billable hours per active customer, utilization drives cash and owner pay after fixed costs.

Keep Crews Billable

Track billable hours by crew, pump, and site. Here’s the quick math: one active customer at 85 billable hours times $260.50 equals about $22,142.50 of billable capacity before costs. Cut weather gaps, permit delays, equipment downtime, and weak follow-up so the schedule stays full; that is what turns higher volume into profit after fixed costs are covered.

1

Average Project Size And Mix

Average Project Size And Mix

Project size drives revenue per mobilization. Residential leveling is 6 hours at $220, or $1,320; commercial stabilization is 24 hours at $350, or $8,400; municipal infrastructure is 40 hours at $300, or $12,000. Bigger jobs can lift gross revenue fast, but they also add access, engineering, and scope risk, so one bad estimate can erase the gain.

When mix shifts from 65% residential in Year 1 to 60% in Year 2, while commercial rises from 25% to 30%, the owner can earn more per crew day if pricing holds. The key is whether the same truck, pump, and crew can handle the larger jobs without more downtime, change orders, or unpaid rework.

Track Ticket Mix by Job Type

Measure average ticket, billable hours, and gross margin by residential, commercial, and municipal work. The inputs are simple: job type, hours sold, hourly rate, and extra scope for access or prep. If a site needs more engineering or setup, price it in upfront so higher revenue turns into real owner pay.

Review mix monthly: booked jobs, completed jobs, and revenue per mobilization. $1,320, $8,400, and $12,000 are very different days on the schedule, so the model should show which jobs actually improve cash flow. If commercial share grows, watch close rates and change orders closely.

- Residential: $1,320 per job

- Commercial: $8,400 per job

- Municipal: $12,000 per job

- Commercial mix: 25% to 30%

2

Direct Labor And Crew Productivity

Crew Time Split

Direct labor is the crew time spent on setup, drilling, mixing, pumping, cleanup, and travel. In Year 1, the model shows a $65k lead injection technician and a $42k assistant technician, with management, estimating, and admin added to total wages. The key question is how much of that payroll turns into billable field hours, because non-billable time cuts labor margin and leaves less cash for owner pay.

At a $26,050 weighted Year 1 hourly rate, every 10 lost billable hours removes about $2,605 of revenue capacity. If the crew spends too long on travel or cleanup, you still pay the wages but collect less job revenue. That gap flows straight through to gross margin, operating cash, and the owner’s distribution.

Track Billable Hours

Track billable field hours and non-billable hours by job. Split time sheets into setup, drilling, mixing, pumping, cleanup, travel, and rework, then compare each job to the hours priced. That shows where labor leaks out. One clean rule helps: if it is not billable, it still counts against margin.

Pay close attention to crew balance. A lead technician at $65k plus an assistant at $42k only helps if the pair finishes more jobs with fewer unpaid hours. Build forecasts around utilization, not headcount, and keep owner management and admin time separate from field labor so pricing and profit draws stay realistic.

3

Material, Pump, And Equipment Cost Control

Grout Mix, Fuel, and Pump Uptime

Cement grout materials run at 14% of Year 1 revenue, and fuel plus equipment consumables add another 5%. That means 19% of revenue is already tied to variable job costs before overhead. If mix usage runs heavy, or the pump sits idle, gross margin, the profit left after direct job costs, drops fast and the owner has less cash for pay and reinvestment.

The driver includes grout yield, fuel miles, pump uptime, and small parts use. The $800 per month maintenance contract matters because a down pump turns billable hours into dead time. The model also carries $145k of startup equipment, including the $28k pump, $65k truck, $12k mixer, and $75k testing kit, so reliability is part of margin control.

Track Waste, Downtime, and Repair Spend

Track grout used per job, fuel per mobilization, and pump downtime by day. Compare each project’s actual material use to the estimate, then flag overages fast. Here’s the quick rule: if the mix is off, the lost material lands straight in direct job cost and cuts the owner’s draw.

- Log mix ratio on every pour

- Review pump service monthly

- Price fuel into mobilization

Also watch spare parts and cleaning waste. Tight mix control keeps jobs on spec, and better uptime keeps crews billing instead of waiting. The real win is fewer remobilizations, fewer wasted bags, and fewer days where a repair turns into a cash drain.

4

Overhead, Insurance, Marketing, And Admin

Fixed Overhead Pressure

Fixed costs cut owner take-home after job costs. The model shows $1,158k of Year 1 fixed expenses, plus $45k of marketing and $4,403k in total payroll, fixed costs, and marketing. If the schedule is full with profitable work, these costs spread over more revenue and hurt less.

Here’s the quick math: $45k of marketing at $450 CAC implies about 100 new customers if spend converts evenly. If jobs are weak, the same overhead stays fixed while owner pay shrinks fast. This is a volume-and-margin issue, not just a cost issue.

Track Overhead Per Job

Measure rent, liability and workers' compensation insurance, accounting, admin payroll, marketing, and CAC against booked jobs and revenue. The key test is whether overhead falls as a share of revenue when profitable jobs fill the schedule.

- Track overhead per booked job.

- Compare CAC to gross profit.

- Watch admin payroll by month.

- Cut spend when utilization drops.

If revenue rises but marketing or back-office costs rise faster, the owner keeps less cash even when sales look strong.

5

Callbacks, Warranty Risk, And Reserves

Callback Reserve Risk

Callbacks hit income twice: they add unpaid labor and block new billable work. With a $26,050 Year 1 weighted hourly rate, every 10 lost billable hours cuts about $2,605 of revenue capacity, before fuel, wages, and equipment wear. Poor site assessment, missed void depth, grout mix errors, or weak repairs can also hurt reputation and repeat sales.

Track the inputs that create warranty work: site review quality, void estimate accuracy, mix batch checks, repair pass/fail rate, and callback hours. If callbacks rise, owner pay falls because more time goes to free return visits instead of paid jobs. A reserve is needed here, since no reserve percentage is given in the model.

Set a Separate Warranty Reserve

Build a user-set reserve before profit draws. That keeps warranty risk from being treated as free cash. In practice, hold back a set share of revenue or gross profit until you know the actual callback rate, then true it up each month. This protects cash flow when repairs take a second visit.

- Count callback hours by job.

- Log root cause codes.

- Compare bid hours to actual hours.

- Review failed repairs weekly.

Here’s the quick math: if a bad month creates 20 unpaid hours, that is about $5,210 of lost revenue capacity at the Year 1 hourly rate. The fix is tighter pre-job checks, mix control, and sign-off before closeout so quality protects owner draw and keeps crews on paid work.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income swings with billable hours, customer mix, and how fast fixed payroll and overhead are covered.

| Scenario | Low CaseBreak-even | Base CaseOwner-operator | High CaseManaged crew |

|---|---|---|---|

| Launch model | The lean case only clears break-even, so owner income stays at zero beyond payroll. | The base case assumes a steady owner-operator model with profit flowing after core costs. | The high case assumes a larger managed crew and stronger profit from higher-volume work. |

| Typical setup | About $50k monthly revenue covers fixed costs and variable job costs, but leaves no room for owner distributions. | Year 1 revenue is $2.495M, about $208k a month, with 73% contribution and a $95k GM salary line. | Year 2 revenue reaches $4.986M, about $416k a month, with 73% contribution and more technician capacity. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0No draw | $1.34MBase case | $3.02MUpside case |

| Best fit | Use this to stress-test cash safety when demand is thin and the crew is still small. | Use this for a realistic first-year plan if sales, pricing, and staffing track the model. | Use this to test upside if the business wins more commercial and municipal work without losing margin. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Cement Grouting Service Porter's Five Forces Analysis

- Cement Grouting Service BCG Matrix

- Cement Grouting Service Business Model Canvas

- What 5 KPIs Drive Cement Grouting Service?

- Cement Grouting Service Business Plan Template in Pre-Written Word

- How Increase Cement Grouting Service Profits?

- What Are The Operating Costs Of Cement Grouting Service?

- Cement Grouting Service Startup Costs: $145K CAPEX, $737K Cash

- Cement Grouting Service Financial Model Template in Excel

- How To Open A Cement Grouting Service In 8–16 Weeks

- How To Write A Cement Grouting Service Business Plan?

- Cement Grouting Service Marketing Mix

- Cement Grouting Service Marketing Plan

- Cement Grouting Service Business Proposal

- Cement Grouting Service PESTEL Analysis

- Cement Grouting Service Pitch Deck Example Editable PPTX

- Cement Grouting Service Business SWOT Analysis

- Cement Grouting Service Value Proposition Canvas

Frequently Asked Questions

The model supports a $95k General Manager salary line if the owner fills that role It also shows about $138M of Year 1 pre-tax operating profit before debt, taxes, reserves, and distributions Actual take-home is lower if cash is held for pump repairs, callbacks, working capital, or financing payments