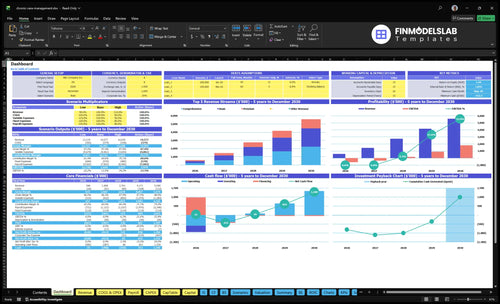

Chronic Care Management Owner Income: $596K Revenue To Year 3 Profit

You’re modeling owner pay in a service where revenue depends on active enrolled patients, monthly collections, staffing, billing performance, and compliance costs In the researched model, revenue grows from $596K in Year 1 to $5590M in Year 5, while EBITDA moves from -$577K to $1833M and breakeven lands in Month 30 This is owner-income planning, not clinical advice, tax advice, coding guidance, or a guarantee of reimbursement or distributions

Owner income$175KNet margin-97% to 33%Revenue for target pay$535KBusiness difficultyHard

Want to test your chronic care management owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Chronic Care Management Service model?

How many chronic care management patients do I need to pay myself?

For a Chronic Care Management Service, don’t plan around one fixed patient count: at $149 weighted monthly revenue per patient in Year 1, you need about 98 patients just to cover a $175K CEO salary, before overhead and other costs. To cover that salary plus $95K monthly fixed overhead, the math jumps to about 736 patients before payroll, marketing, denials, and reserves; see What Are The Operating Costs For Chronic Care Management Service? for the cost side.

Salary math

Year 1: $14,583 / $149 = 98 patients

Year 3: $14,583 / $164 = 89 patients

Year 5: $14,583 / $181 = 81 patients

EBITDA stays negative in Years 1 and 2

Real breakeven

Month 30 is modeled breakeven

$95K monthly fixed overhead matters most

Collections and plan mix change the census target

Slow onboarding or denials raise patient need

How much revenue does a chronic care management service make per patient?

For Chronic Care Management Service, revenue per enrolled patient depends on the tier mix: Basic runs $99 to $111 per month, Comprehensive is $199 to $224, and Premium is $299 to $337. In the model, the weighted monthly price rises from $149 in Year 1 to about $181 in Year 5 as higher tiers take a bigger share, but actual revenue still comes down to CPT mix, documented care time, provider agreements, payer policy, collections, and patient enrollment.

Tier prices

Basic:$99-$111 monthly

Comprehensive:$199-$224 monthly

Premium:$299-$337 monthly

Higher tier mix lifts revenue

Revenue drivers

Year 1: weighted price $149

Year 5: weighted price $181

CPT mix affects actual revenue

Collections and enrollment matter

Can a chronic care management service owner make more by scaling patients?

Yes—scaling a Chronic Care Management Service can lift owner income, but only if the business can fund staffing, documentation, and billing as it grows from 20 FTE care coordinators to 120 FTE. Revenue rises from $596K in Year 1 to $5.590M in Year 5, and EBITDA turns positive in Year 3 at $172K before reaching $1.833M in Year 5. The hard part is cash: minimum cash drops to -$552K in Month 29, so growth needs strong collections and working-capital support.

Scale helps

$596K Year 1 revenue

$5.590M Year 5 revenue

EBITDA turns positive in Year 3

$1.833M EBITDA in Year 5

Risk rises too

20 FTE grows to 120 FTE

Minimum cash hits -$552K

Cash trough lands in Month 29

Billing and retention need tighter control

Chronic Care Management Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see the six main chronic care management income drivers?

1

Patient Census

$596K-$5.6M

More active patients push revenue from $596K to $5.6M, and slow intake keeps cash negative through Month 29.

2

Price Mix

$149-$181

The weighted monthly price rises from $149 to $181, so mix shifts change take-home before headcount does.

3

Coordinator Output

2-12 FTE

Care coordinator FTE grows from 2 to 12, so output per coordinator decides whether EBITDA turns from -$577K to $1.8M.

4

Referral Conversion

$300-$450

Better referral conversion lowers CAC from $450 to $300, which buys more enrollments for the same marketing dollars.

5

Collections

2.5%-1.5%

Lower denial and fee drag protects margin, and processing costs ease from 2.5% to 1.5% by Year 5.

6

Overhead Buffer

-$552K

Fixed overhead and reserves decide survival, since cash bottoms at -$552K before breakeven in Month 30.

Chronic Care Management Service Core Six Income Drivers

Active Enrolled Patient Census

Active Enrolled Patient Census

This driver is the count of qualified, consenting, retained patients on monthly service. Do not count raw leads. When active census rises, recurring revenue grows, and the base that pays for staff, software, compliance, and owner draw gets safer.

Here’s the quick math: model revenue rises from $596K to $5,590M as weighted monthly price moves from $149 to $181. CAC also improves from $450 to $300, but only if onboarding works and ineligible patients are screened out fast. One bad month of churn hits profit twice: less revenue and more wasted acquisition spend.

Track Enrolled Census Quality

Track new enrollments, active census, 30-day retention, and eligibility pass rate. A full funnel matters because leads are not patients, and signed patients who never finish onboarding do not create stable monthly revenue.

Watch census by cohort and by source. If marketing spend rises from $300K to $12M, the owner should test which channels deliver retained patients, not just cheaper clicks. If onboarding takes too long or eligibility is weak, revenue coverage for payroll and fixed costs slips fast.

1

Revenue Per Patient

Revenue Per Patient

This driver is the average monthly revenue per active patient, shaped by plan mix, documented activity, payer rules, provider contracts, and collections. In the model, pricing moves from $99, $199, and $299 in Year 1 to $111, $224, and $337 by Year 5, lifting weighted revenue per patient from $149 to about $181.

That spread matters fast. At an active census, every $10 per patient per month adds $120 per year per patient before costs. What this estimate hides: reimbursement is not automatic, so the owner’s income only rises if the billed mix, documentation, and cash collection all hold up.

Track the paid mix

Measure revenue per patient by tier, payer, and month, then compare it to the weighted target of $149 to $181. Track these inputs each month:

Active paid patients

Tier mix by plan

Collected revenue per patient

Denied or unpaid claims

Contracted payer rates

If the higher-tier mix grows but collections lag, reported revenue can look healthy while cash stays tight. The owner pays themselves from collected margin, not hoped-for revenue.

2

Care Coordinator Productivity

Care Coordinator Productivity

Labor efficiency is a direct profit lever here because revenue is already booked before the care work is done. At $82K per FTE, coordinator payroll runs about $6.8K per month per person, so moving from 20 FTE to 120 FTE takes annual labor from roughly $1.64M to $9.84M. Owner income rises when each coordinator carries a compliant caseload without letting documentation, follow-up, or patient engagement slip.

The key inputs are active members per coordinator, documentation time, engagement touchpoints, and denial or churn risk. Push caseloads too high and you may save payroll on paper, but denials, drop-off, and quality problems can erase the gain fast. One extra hour of wasted work per case is margin leakage.

Protect Caseload Quality

Track members per FTE, documentation completion, outreach response time, and denied or reopened cases by coordinator. Then test caseload caps by team, not by guesswork, so you can see where productivity stays compliant and where quality breaks. The goal is simple: keep each coordinator busy enough to cover payroll, but not so overloaded that churn or denials cut owner draw.

Measure cases per FTE weekly.

Review denials and rework monthly.

Cap caseloads before quality slips.

Link staffing to active census.

3

Collections And Denial Control

Collections and denial control

Collection rate should hit the revenue formula before profit. In this model, payment processing runs 25% of revenue in Year 1 and falls to 15% by Year 5, so weak billing can hit owner pay before profit shows up. If claims are denied or paid late, revenue leaks while payroll and fixed overhead keep running.

The key inputs are submitted claims, denial rate, collection rate, documentation quality, and days to payment. Strong patient volume still misses plan if paperwork is incomplete or follow-up is slow. Billing performance changes cash timing, not just revenue, and minimum cash reaches -$552K before breakeven.

Track cash, not just claims

Measure the billing chain end to end: claims sent, denied claims, collected cash, and aging receivables. Here’s the quick rule: if cash collected trails booked revenue, owner income is overstated.

Track denial rate by reason.

Review unpaid claims weekly.

Use collected revenue in forecasts.

Hold documentation before billing.

Keep staffing, software, and owner draws tied to cash collected, not just patient volume. If payment lag grows, cut distributions or slow spend early so payroll and fixed overhead stay covered.

4

Referral Partnerships And Enrollment Conversion

Referral-to-Enrollment Conversion

This driver is about turning referral partners into qualified, consenting, recurring patients. Income rises when marketing spend of $300K to $12M lowers customer acquisition cost (CAC) from $450 to $300, because a larger enrolled census supports monthly subscription revenue, coordinator hours, and owner draw. Broad traffic that does not enroll still burns cash.

The key inputs are referral quality, script conversion, eligibility, and retention. If referrals are weak, census stalls, staffing stays underused, and Month 30 breakeven slips. Here’s the quick math: spend only works when each partner sends patients who stay, not just names. One bad channel can raise cash burn before revenue shows up.

Measure Qualified Referrals, Not Traffic

Track each partner by eligible referrals, enrollment rate, first-payment rate, and 90-day retention. Use one clean funnel: referral → qualified patient → enrolled member → active monthly participant. If a partner’s CAC stays near $450 after documentation and close rates, cut spend there until quality improves.

Eligible referrals per partner

Enrollment conversion rate

Monthly retention rate

CAC versus active census

Test scripts with caregivers and doctor offices, since adult children often help choose the service. Keep a simple scorecard for referrals, conversions, cancellations, and monthly recurring revenue per partner. The goal is not more traffic; it is more qualified census that pays payroll and fixed costs.

5

Overhead, Technology, Compliance, And Reserves

Overhead, Tech, and Reserves

Owner take-home starts after $95K per month of fixed overhead, plus hosting, compliance, insurance, admin, and reserves. In Year 1, hosting is 40% of revenue, so every $100 collected leaves $60 before fixed overhead and reserves. By Year 5, hosting drops to 20%, which widens cash available for owner pay.

Here’s the quick math: cash must also cover $200K of platform development and other startup investments, but that spend is capex, not monthly overhead. The real risk is paying the owner too soon. If reserves are thin, payroll and billing delays can force a cash squeeze even when revenue looks solid.

Keep Cash in the Business First

Track monthly revenue, hosting %, fixed overhead, and a reserve target before any owner draw. A simple rule works: cash left after 40% hosting and $95K overhead is not spendable until payroll, vendor bills, and billing lag are covered. That keeps owner pay tied to real cash, not booked revenue.

Test whether reserves can absorb one missed collections cycle without cutting service. If not, defer distributions and rebuild cash first. The operating goal is to let hosting fall toward 20% over time while fixed costs stay flat, so more gross profit can flow to owner income instead of getting trapped in working capital.

6

Chronic Care Management Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high chronic care management owner income scenarios

Owner income scenarios

Owner income here moves with patient count, pricing mix, staffing, and CAC. Early years burn cash, then pay improves as breakeven and scale show up.

Low, base, and high owner income paths for planning.

Scenario

Low CaseDownside case

Base CaseCore case

High CaseUpside case

Launch model

This is the low owner-income path, where the business is still in startup burn and pay depends on outside funding.

This is the modeled owner-income path, where the business reaches breakeven and can support steadier pay.

This is the stronger owner-income path, where scale turns the service into a much larger profit engine.

Typical setup

Year 1 revenue is $596K and EBITDA is -$577K, with a low-price mix, heavy marketing, fixed overhead, and the CEO still hands-on.

By Year 3, revenue reaches $2.761M and EBITDA turns positive at $172K, with breakeven around Month 30 and a more balanced pricing mix.

By Year 5, revenue reaches $5.590M and EBITDA reaches $1.833M, supported by 12 coordinator FTEs, $1.2M marketing, and lower CAC.

Cost drivers

patient census ramp

CAC at $450

fixed overhead

startup capex

CEO pay

price mix shift

CAC at $350

coordinator staffing

breakeven timing

overhead

larger patient census

CAC at $300

12 coordinator FTEs

$1.2M marketing

reserve needs

Owner income rangeBefore owner reserves

$0 - $175kCash tight

$175kBreak-even path

$175k+Scale upside

Best fit

Use this to stress-test the plan if growth is slow and reserves must cover the early burn.

Use this as the main planning case if you expect steady census growth and controlled staffing.

Use this to test what owner pay can look like if scale is strong and the business keeps enough cash in reserve.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In the researched model, owner pay is represented by a $175K CEO salary, but that is not the same as guaranteed profit EBITDA is -$577K in Year 1 and -$361K in Year 2, then turns positive at $172K in Year 3 Extra distributions depend on cash, reserves, taxes, debt, and reinvestment

This model reaches breakeven in Month 30, with payback in Month 56 The hard part is funding the gap before that point, since minimum cash reaches -$552K in Month 29 Faster enrollment, cleaner billing, lower CAC, or slower hiring can improve timing

Yes, in this model the service is staffed from launch Year 1 includes 20 care coordinator FTEs, 10 operations lead, 10 CEO, support, IT, and partial marketing leadership, creating $624K of payroll Owner pay is easier to defend when staffing supports compliant service delivery and collections

The biggest drivers are enrolled patient census, monthly revenue per patient, coordinator productivity, collections, referral conversion, and overhead control Weighted monthly price rises from $149 to $181 across the model, but payroll, marketing, and compliance costs decide how much reaches EBITDA Denials or poor retention can erase margin quickly

Use a forecast before hiring, signing provider agreements, or increasing marketing spend This model commits $300K to Year 1 marketing, $200K to platform development, and $95K per month to fixed overhead A forecast shows whether your cash can survive the ramp before Month 30 breakeven

About the author

Ryan Spencer

First-Time Founder Guide Writer

Ryan Spencer writes for Financial Models Lab, where he focuses on launch budget planning and simple launch planning for first-time founders. He helps readers estimate startup needs before opening a physical location, breaking down business costs in clear, practical language. His work is built for people who want a realistic view of what it really takes to open a business, so they can plan with more confidence and fewer surprises.

Choosing a selection results in a full page refresh.