How Much Does A Claims Processing Service Owner Earn?

Claims Processing Service

Factors Influencing Claims Processing Service Owners' Income

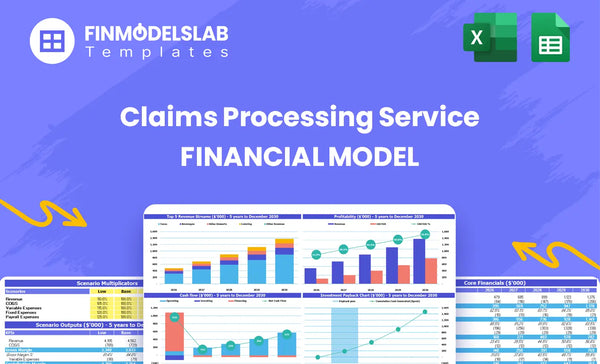

Subheader variant #2: Claims Processing Service businesses show strong scaling potential, moving from negative earnings in the first year to over $17 million in EBITDA by Year 5, based on a projected revenue of $57 million Initial investment is substantial, requiring a minimum cash buffer of $222,000 to cover early losses and a 41-month payback period The primary drivers of owner income are high-value contracts (Construction/Property claims at $1,200/month in 2026) and reducing variable costs, which drop from 130% to 90% by 2030

7 Factors That Influence Claims Processing Service Owner's Income

#

Factor Name

Factor Type

Impact on Owner Income

1

Revenue Scale

Revenue

Higher revenue from Construction/Property clients paying $1,200/month increases owner income more than Medical/Dental clients at $850/month.

2

Gross Margin

Cost

Lowering claims verification costs (COGS) from 80% to 60% directly improves the contribution margin per client.

3

Fixed Overhead

Cost

High fixed costs of $15,600 monthly necessitate rapid client acquisition to cover overhead and hit the 8-month break-even goal.

4

Client Acquisition Cost

Cost

Reducing CAC from $1,200 to $900 by 2030 is essential because the annual marketing spend reaches $420,000.

5

Labor Efficiency

Cost

Managing the mix of high-salary Senior Specialists ($85,000) versus standard Specialists ($65,000) controls the scaling payroll expense.

6

Initial CAPEX

Capital

The $455,000 initial investment in software development slows the Internal Rate of Return (IRR) and extends the payback period to 41 months.

7

Variable Costs

Cost

Decreasing Carrier Communication costs from 50% to 30% of revenue directly boosts the final net profit margin as volume grows.

Claims Processing Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What is the realistic owner compensation trajectory for a Claims Processing Service?

The owner of the Claims Processing Service will draw a set salary of $150,000, but the business shows negative earnings of $195,000 in Year 1 before owner compensation truly pays off, which you can see reflected in the operational cost analysis found here: What Does It Cost To Run Claims Processing Service? Real financial upside, where owner earnings become substantial, appears around Year 3, projecting to $177 million in EBITDA by Year 5. That's a long ramp, so runway planning is defintely critical.

Year 1 Cash Reality

CEO salary is fixed at $150,000 annually.

Year 1 EBITDA shows a negative $195,000 swing.

This means the owner is funding operations initially.

You need enough cash reserves to cover this gap.

The Long-Term Payout

Revenue growth must hit $57 million by Year 5.

Substantial owner earnings begin after Year 3.

Year 5 EBITDA is projected at $177 million.

Focus on scaling client volume fast.

Which operational levers most quickly drive profitability and scale in this business?

The fastest way to profitability for the Claims Processing Service is fixing the current 130% variable cost ratio and driving down the $1,200 starting Customer Acquisition Cost (CAC) by targeting premium clients. If you are planning this out, you'll defintely want to review the steps in How To Write A Business Plan For Claims Processing Service?.

Driving Acquisition Efficiency

Customer Acquisition Cost (CAC) starts at $1,200.

Focus sales on Construction/Property Management immediately.

These clients pay the top $1,200 monthly price point.

You must lower CAC through efficient channel sourcing.

Fixing the Cost Structure

Variable costs are currently 130% of revenue.

This means you lose money on every dollar earned.

Identify the specific operational cost inflating the 130%.

The immediate goal is pushing variable costs below 50%.

What is the financial risk profile and minimum cash requirement to survive the launch phase?

The Claims Processing Service needs $222,000 in minimum cash to cover operations until the projected August 2026 break-even point, but the primary financial risk is slow client adoption against $15,600 in monthly fixed overhead. Before diving deeper into metrics like those found in What Are The 5 KPIs For Claims Processing Service Business?, you must secure funding for the initial build. That initial capital outlay is substantial, so understanding runway is defintely key.

Initial Capital Needs

Total initial CAPEX (Capital Expenditure) is $455,000 for software and infrastructure.

Minimum cash required to fund operations until break-even is $222,000.

Monthly fixed overhead costs are set at $15,600.

Break-even is currently projected for August 2026.

Launch Risk Profile

The main financial risk is slow client adoption against fixed costs.

If adoption stalls, you burn $15,600 every month.

This burn rate eats into the $222,000 survival buffer quickly.

If onboarding takes 14+ days, churn risk rises, stretching the runway further.

How does the high upfront investment impact long-term returns like IRR and payback period?

The Claims Processing Service's hefty $455,000 CAPEX directly pressures long-term returns, yielding an initial Internal Rate of Return (IRR) of 335% and a 41-month payback period; scaling revenue quickly is defintely needed to justify this infrastructure spend and improve these metrics, which you can explore further at How Increase Claims Processing Service Profitability?

Initial Return Metrics

Upfront infrastructure spend is $455,000.

Initial IRR sits at 335%.

Payback takes 41 months.

This timeline is slow for a new venture.

Improving the Return Profile

Focus on rapid client acquisition.

Increase recurring monthly fees collected.

Reduce time to positive cash flow.

If onboarding takes 14+ days, churn risk rises.

Claims Processing Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Key Takeaways

Owner earnings (EBITDA) transition rapidly from a $195,000 first-year loss to a potential $177 million by Year 5, demonstrating massive scaling potential.

Despite achieving operational break-even within 8 months, the substantial $455,000 initial CAPEX results in a lengthy 41-month payback period for the total investment.

Profitability hinges on aggressively managing high initial fixed costs ($15,600 monthly) and optimizing client acquisition costs, which start at $1,200 per customer.

Maximizing owner income requires prioritizing high-value client segments, such as Construction/Property claims priced at $1,200 monthly, to drive revenue scale efficiently.

Factor 1

: Revenue Scale

Client Mix Drives Income

Owner income growth hinges on shifting the client mix toward higher-paying sectors. In 2026, securing a Construction/Property client generates $1,200 monthly revenue, significantly better than the $850 from a Medical/Dental client. Focus sales efforts where the dollar yield is highest.

Client Acquisition Inputs

Acquiring the higher-value Construction/Property client requires careful spending management. The starting Customer Acquisition Cost (CAC) is $1,200 per client in 2026. You need to track the payback period for this initial spend against the $1,200 monthly fee to ensure quick unit economics payoff.

Margin Optimization

To maximize owner income from this revenue, you must aggressively lower Cost of Goods Sold (COGS). Gross margin starts low, at 20% (80% COGS) in 2026, but improving verification efficiency to reach 40% margin by 2030 is key. This optimization directly increases the profit captured from every $1,200 invoice.

Scaling Priority

To hit owner income targets quickly, prioritize sales pipelines that convert Construction/Property accounts first. That $350 monthly difference per client-$1,200 versus $850-compounds rapidly when overcoming the $15,600 fixed overhead. It's defintely a revenue mix problem.

Factor 2

: Gross Margin

Margin Improvement Driver

Your gross margin hinges on cutting verification costs, which are your COGS. Expect these costs to fall from 80% of revenue in 2026 down to 60% by 2030. This efficiency gain directly boosts the contribution you make on every client service, so focus on process automation now.

Estimating Verification Costs

Claims verification costs are your main Cost of Goods Sold (COGS). Estimate this by tracking specialist time spent per claim type against the revenue generated. In 2026, these costs consume 80% of revenue, which is typical for early-stage service models. This high initial burden strains early profitability.

Track specialist time verifying claims.

Use internal salary rates for input.

Benchmark against the 80% target.

Optimizing Claims COGS

To cut verification costs, standardize documentation intake immediately. Automation in initial data scrubbing reduces manual review time, which is currently too high. You must improve labor efficiency (Factor 5) to hit the 60% COGS goal by 2030. Don't sacrifice accuracy for speed, though.

Standardize client documentation intake.

Automate initial data validation checks.

Hire Senior Specialists wisely.

Contribution Impact

Moving COGS from 80% to 60% is a 20-point margin jump. This effectively doubles your contribution margin from 20% to 40%. That extra cash flow is vital for funding the growth needed to cover your $15,600 monthly overhead and hit that 8-month break-even. That's real leverage, honestly.

Factor 3

: Fixed Overhead

Overhead Pressure

Your $15,600 monthly fixed overhead creates intense pressure on sales velocity. To hit the 8-month break-even goal, you must aggressively scale client volume now to cover these necessary operating costs before cash runs thin. This overhead is your primary near-term hurdle, requiring immediate focus.

Cost Inputs

Fixed overhead starts at $15,600 monthly, which is non-negotiable until you move locations or downsize servers. This includes $6,000 for rent and $3,500 for essential cloud infrastructure supporting your processing platform. These figures must be covered defintely regardless of client count.

Rent commitment: $6,000 monthly.

Cloud infrastructure: $3,500 for hosting.

Total fixed base: $15,600.

Capacity Leverage

You manage this cost by maximizing utilization, not cutting the base figures yet. Since rent and cloud are set, every new client immediately improves the contribution margin against this fixed base. Avoid paying for unneeded software seats today; focus on hitting the required order density fast.

Acquire clients quickly.

Ensure high utilization rates.

Delay non-essential software upgrades.

BE Target

Achieving break-even in 8 months means the revenue needed to cover $15,600 in fixed costs is paramount. If client onboarding lags, you burn cash against these sunk costs, pushing the payback period out significantly past the target timeline.

Factor 4

: Client Acquisition Cost

Control CAC Spend

You must drive down Customer Acquisition Cost (CAC) from $1,200 in 2026 to $900 by 2030. This isn't just about efficiency; it directly supports a $420,000 annual marketing budget planned for 2030. If you miss this target, profitability suffers fast.

Defining CAC Spend

Customer Acquisition Cost (CAC) covers all marketing and sales expenses required to secure one new paying client. For this claims service, inputs include digital ad spend, sales commissions, and any promotional outreach costs leading up to the initial subscription payment. We need to track this monthly against new recurring revenue.

Track cost per lead source.

Map spend to closed deals.

Calculate payback period.

Cutting Acquisition Costs

Reducing CAC requires focusing on high-value channels that deliver better client lifetime value (LTV). Since you target higher-paying Construction/Property clients, prioritize direct outreach over broad digital campaigns. If onboarding takes 14+ days, churn risk rises, wasting that initial CAC investment. We defintely need better lead quality here.

Focus on referrals early on.

Target Construction clients first.

Improve sales script conversion.

Marketing Budget Leverage

Spending $420,000 annually on marketing by 2030 is a massive commitment. If CAC remains at $1,200 instead of hitting $900, you acquire 100 fewer clients that year for the same budget. That lost volume directly impacts reaching your revenue scale goals.

Factor 5

: Labor Efficiency

Control Labor Mix

Scaling headcount from 8 FTE in 2026 to 29 FTE by 2030 demands strict control over labor mix. The ratio between your $85,000 Senior Claims Specialists and the $65,000 standard specialists directly dictates total payroll expense and margin structure. Get this balance wrong, and overhead balloons fast.

What Labor Costs Cover

This labor cost covers the core processing engine handling client claims submissions and follow-up. Estimate total annual payroll by multiplying the number of FTEs by their respective salaries-for example, 8 FTEs in 2026 require precise salary planning. Inputs needed are the $85k senior rate and the $65k standard rate.

Total FTE count scales to 29 by 2030.

Salaries are fixed at $85,000 and $65,000.

This is the largest variable cost component.

Optimizing Specialist Ratios

Manage the ratio to maximize output per dollar spent. Initially, you might need more seniors for process setup, but as volume stabilizes, lean into the lower-cost processors. If onboarding takes 14+ days, churn risk rises defintely due to slow service delivery.

Benchmark senior time spent on training.

Use process automation to buffer growth.

Ensure seniors aren't doing $65k work.

Payroll Impact on Margins

As you move toward 29 FTEs by 2030, every percentage point shift in the specialist ratio impacts the overall Gross Margin improvement goal. High-cost labor must drive disproportionately higher value than standard roles to justify the spend, especially while variable costs drop from 50% to 30%.

Factor 6

: Initial CAPEX

CAPEX Impact on Returns

The $455,000 initial capital expenditure (CAPEX) for software and infrastructure slows down returns significantly. This large upfront spend results in a relatively low initial Internal Rate of Return (IRR) of 335% and pushes the payback period out to 41 months. That's a heavy lift before you see cash back.

CAPEX Drivers

This $455,000 covers building the core technology-the proprietary software platform and the necessary secure data infrastructure. Estimating this requires firm quotes from development teams and architecture planning for compliance. This cost must be covered before the first dollar of subscription revenue hits the bank, defintely requiring significant upfront capital.

Software development quotes

Infrastructure setup costs

Compliance requirements definition

Phasing Initial Spend

You can't really cut corners on secure infrastructure, but you can phase the software build. Avoid building features that aren't needed for the Minimum Viable Product (MVP). Deferring non-essential modules lowers the initial burn rate, though it might delay feature parity later on.

De-scope MVP features

Use off-the-shelf tools first

Negotiate milestone payments

Runway Requirement

Waiting 41 months to recoup $455,000 means your operating cash flow must sustain the business for over three years. You need enough runway or committed funding to cover $15,600 in monthly fixed overhead during this long recoup period. That duration defines your initial funding need.

Factor 7

: Variable Costs

Variable Cost Leverage

Reducing Carrier Communication and Integration costs from 50% down to 30% of revenue is your biggest lever for margin expansion. This 20 percentage point shift directly flows to the bottom line as you acquire more claims volume. Every dollar of revenue gained after this optimization hits profit harder. So, focus here.

Cost Breakdown

These variable costs cover the direct expenses tied to talking to carriers and linking systems for claim submission. To estimate this line item accurately, you need the total monthly communication spend divided by total monthly revenue. This percentage must drop significantly from the starting 50% to hit profitability goals. What this estimate hides is the initial integration setup cost.

Total Carrier API fees

Outsourced follow-up labor

Monthly revenue volume

Hitting the 30% Target

You manage this by automating integration points as volume grows, shifting work from expensive manual communication to cheaper software links. If you don't automate, these costs eat margin alive when you scale past the initial 8-month break-even point. You defintely need engineering focus here to drive down the cost per claim processed.

Automate status checks

Negotiate carrier volume tiers

Standardize integration protocols

Margin Driver

Achieving the 30% target means that for every $100,000 in revenue, you keep $20,000 more than you did at the start. This improvement is how owner income scales faster than revenue alone, especially when servicing those high-value $1,200 Construction clients. Control this cost to control your cash flow.

EBITDA grows from a $195,000 loss in Year 1 to $548,000 by Year 3, and up to $177 million by Year 5 This high growth depends on scaling revenue from $11 million to $57 million over that period

The business is projected to reach break-even quickly, within 8 months (August 2026) However, the full payback period for the substantial initial investment is 41 months

About the author

William Hayes

Small Business Consultant

William Hayes is a small business consultant at Financial Models Lab who writes for early-stage founders building a basic plan before investing money. He focuses on business plan basics and practical everyday business finance, helping readers use realistic assumptions to understand revenue, expenses, and profit in simple terms. His direct, useful approach is designed to give new founders a clearer path from idea to informed decision.

Choosing a selection results in a full page refresh.