How Much CNC Machining Owners Can Make: $624K Before Reserves

Key Takeaways

Billable machine hours must outrun downtime and overhead.

Quotes must cover scrap, setup, finishing, and shipping.

Mix repeat jobs with complex parts to protect margin.

Payroll and financing can erase operating profit fast.

Owner income$52K/moNet margin36.4%Revenue for target pay$1.71MBusiness difficultyHard

Want to test your CNC owner pay?

Owner income calculator

Estimate owner take-home and the gap to target pay from revenue, gross margin, costs, reserves, and the pay you want to pull out.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, legal advice, or owner distribution advice.

Want to see owner income in the CNC shop model?

Yes—the CNC Machining Service Financial Model Template shows revenue, gross margin, operating profit, cash flow, and owner income; open it and test utilization, machine buys, hiring, and cash needs.

Owner-income model highlights

Year 1 revenue: $124M

Year 3 revenue: $264M

Mature revenue: $357M

Profit before owner pay

Scenarios for draw timing

What affects CNC machining profit margin?

Margin in a CNC Machining Service is mostly driven by part mix and direct costs: $1,650 for a Precision Shaft, $900 for a Custom Bracket, $2,800 for a Valve Body, $3,800 for a Gear Housing, and $2,050 for a Fixture Plate. Revenue-based COGS can run from 28% to 49% by part type, and you can lose more on 25% sales commissions, 10% expedited shipping, plus scrap, setup time, rework, tooling wear, and downtime before overhead is even covered; see How Much Does It Cost To Open And Launch Your CNC Machining Service Business?

Direct margin drivers

Part mix changes unit economics fast

COGS range: 28% to 49%

Commissions start at 25%

Expedited shipping starts at 10%

Hidden margin leaks

Scrap cuts sellable output

Setup time lowers hourly output

Rework adds unpaid labor

Tooling wear and downtime hit take-home

How much revenue does a CNC shop need to pay the owner?

There isn’t one universal revenue target for a CNC Machining Service. With $130K of fixed overhead and $280K of total payroll, break-even before owner pay is about $491K/year, or $41K/month; to add $100K of pre-tax owner cash, revenue needs to rise to about $610K/year, or $51K/month.

Break-even math

$130K fixed overhead

$280K payroll load

$491K/year break-even before owner pay

$41K/month quick monthly target

Owner pay target

Add $100K pre-tax owner cash

Revenue rises to $610K/year

That is about $51K/month

Still before debt, taxes, reserves

Can a CNC machining business make money without the owner running machines?

Yes, a CNC Machining Service can make money without the owner running machines, but only if pricing and machine utilization cover the added payroll. Here’s the quick math: payroll lines rise from $280K in Year 1 to $475K by Year 3, while revenue rises from $124M to $264M over the same period. The owner shifts from operator to estimator, salesperson, manager, and quality-control leader, so the win is more capacity but the risk is hiring, scheduling, QC, and cash tied up before customers pay.

Can it work?

Yes, if jobs stay booked.

Pricing must cover payroll growth.

Utilization has to stay high.

Quality must hold without owner labor.

What changes?

Owner role moves to manager.

Hiring risk rises fast.

Cash flow gets tighter.

Scheduling pressure goes up.

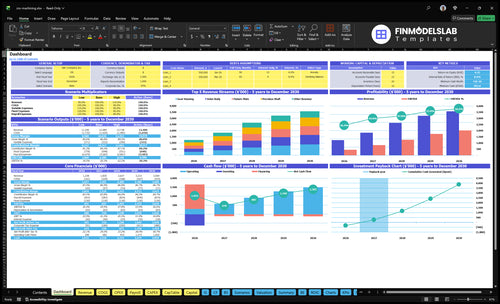

CNC Machining Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six CNC income drivers?

1

Billable Utilization

$1.24M

Year 1 output and pricing point to about $1.24M in sales, so more billable machine time drops straight into take-home.

2

Pricing Accuracy

91%

The quoted part margins sit near 91%, and even a small quoting miss on a custom job can wipe out a lot of profit.

3

Part Mix

4.7x

Moving more volume to Gear Housing and Valve Body work lifts revenue per part, since those jobs pay up to 4.7x a Custom Bracket.

4

Labor Productivity

6.0 FTE

Year 1 staffing totals 6.0 FTE, so every setup saved and every rework avoided protects the dollars left after payroll.

5

Direct Costs

8%-10%

Direct job cost runs about 8%-10% of price, so scrap, waste, and finish rework cut margin faster than most owners expect.

6

Fixed Overhead

$10.8K/mo

Fixed shop costs hit every month, and the equipment buy-in keeps cash tight until volume clears the base load.

CNC Machining Service Core Six Income Drivers

Billable Machine Utilization

Billable Machine Utilization

If more of the day becomes billable CNC machine hours, you spread $108K/month of fixed overhead and payroll across more revenue. Use utilization rate = billable hours ÷ available spindle hours, and keep setup, idle time, maintenance, inspection, and rework out of productive machine hours. If utilization supports the stated first-year volume of 6,100 total parts, revenue reaches $124M.

Downtime hurts twice: revenue falls, and rent, software, insurance, and payroll still run. That cuts cash flow fast and leaves less room for owner pay, especially when machines look busy but the hours are not billable.

Track Hours That Can Bill

Measure available spindle hours, billable hours, and uptime by machine and part family. The main inputs are planned downtime, actual production time, setup time, inspection, and rework. Here’s the quick test: if uptime is high but billable hours stay low, the leak is usually changeover loss, poor scheduling, or jobs that do not convert cleanly into revenue.

Log non-billable time by cause.

Review billable hours daily.

Separate setup from production.

Cut rework before buying capacity.

Use the gap between available hours and billable hours in the weekly forecast; that gap is where owner income gets squeezed first.

1

Pricing And Quoting Accuracy

Quote to True Cost

Pricing accuracy decides whether a CNC job pays the owner or just stays busy. A quote has to cover setup time, cycle time, material waste, tolerances, finishing, tooling, inspection, and shipping. If a Gear Housing is sold at $450 but direct unit cost is $38 plus 49% revenue-based COGS, one missed assumption can wipe out take-home even when volume looks strong.

Here’s the quick math: revenue is only useful if quoted margin matches actual margin by part family and customer. Busy shops can still under-earn when scrap, programming time, or rework is left out of the price. The key input is quoted margin versus actual margin; if actual margin falls below quote, owner pay drops fast.

Track Margin by Part Family

Use job costing on every part family and compare estimate to closeout. Track setup hours, machine time, scrap, finishing, and inspection hours, then reconcile them to the quote. If a part family keeps missing by even a few points, raise the price or tighten the process before scaling volume.

One clean rule: quote the job, then prove it after shipment. Build a simple report for quoted margin, actual margin, and customer mix, and review it monthly. That keeps high-volume work from hiding low-profit work, and it protects cash flow needed for owner draws and payroll.

2

Customer And Part Mix

Customer and Part Mix

Customer and part mix is the profit mix behind the sales line. Repeatable parts, tight tolerances, material type, order size, and customer reliability all change setup time, scrap, inspection hours, and cash timing. A shop can grow revenue and still pay the owner less if the mix pushes too much rework or slow-paying work.

First-year part revenue ranges from $190K for Custom Brackets to $270K each for Precision Shafts and Gear Housings. Repeat runs can smooth scheduling, but complex jobs may carry higher prices and more inspection risk. The key inputs are repeat order rate, tolerance level, material, quantity, and customer payment behavior.

Track Margin by Part Family

Measure gross margin by part family, not just total sales. Here’s the quick math: compare quoted price, direct labor, material, finishing, inspection, and scrap for each job class. If one customer buys often but forces extra inspection, its cash value can be lower than a smaller, cleaner order.

Track margin by customer and part.

Flag jobs with heavy inspection.

Watch scrap on tight-tolerance parts.

Price low-volume setups separately.

Prefer reliable repeat orders for flow.

What this hides: high-complexity work can lift price, but it also raises scrap and rework risk. If a part family adds more setup and QC time than the price covers, owner pay falls even when revenue looks strong. The goal is a mix that protects margin quality, not just volume.

3

Direct Job Cost Control

Direct Job Cost Control

With $204K in first-year direct and variable costs against $124M revenue, direct cost control is a profit gate, not a back-office task. Scrap, rework, bad material yield, or weak fixture design cut gross margin before overhead is even paid, so owner income falls even when sales look strong.

Track Cost Per Job

Control the full job cost stack: raw material, direct machining labor, third-party finishing, consumable inserts, packaging, tooling, machine depreciation, QC labor, utilities allocation, and shop supplies. To protect the stated 835% contribution margin in the model, track quote-versus-actual by part family, plus actual hours, scrap rate, rework hours, and tool life.

Compare quoted versus actual margin.

Separate scrap from rework.

Log tool life by part family.

Review material yield on every job.

4

Labor Productivity And Owner Replacement Cost

Labor Productivity and Owner Replacement Cost

Labor productivity is the revenue and billable output each machinist or programmer creates after setup and rework. This matters because payroll rises from $280K in Year 1 to $378K in Year 2 and $475K from Year 3 onward, so hiring only helps owner income if utilization and pricing cover the full wage load.

If the owner runs the machine, treat that work as a replacement cost first: pay the market machinist wage before calling the rest profit. Here’s the quick math: track revenue per production employee, setup hours per job, and rework hours. More labor can raise capacity, but it can also cut take-home if the extra payroll does not turn into enough billable work.

Measure labor before you hire

Watch output by person and by part family. Compare total paid hours to billable hours, then test whether one more machinist or programmer reduces setup or rework enough to pay for the added salary line. If it does not, the hire lowers cash available for owner pay even when sales rise.

Build each forecast with revenue per production employee, the owner’s market wage, and the next payroll step-up. Keep the owner’s machinist pay separate from profit, and only add labor when higher utilization and pricing still leave room for a healthy owner draw.

5

Fixed Overhead And Equipment Financing

Fixed Overhead Floor

For a CNC shop, this is the monthly bill load you must cover before owner pay. Here, fixed overhead is $108K/month and includes $6K rent, $18K utilities, $750 insurance, $12K software, $250 website, $500 accounting and legal, and $300 office supplies. That is $1.296M a year before debt service or owner draw.

The trap is cash flow. Machine financing, leases, maintenance, and reserve funding can cut distributions even when accounting profit looks solid. So the real test is simple: do monthly collections cover fixed overhead plus equipment cash needs, or does owner pay get pushed back?

Watch the cash coverage

Track fixed overhead as a share of monthly revenue, then add debt service and reserve needs. If collections fall below $108K, owner pay is already squeezed; if machine payments or repairs rise, the squeeze gets worse fast. One clean test: can the shop fund overhead, equipment cash needs, and vendor bills without delay?

Build a monthly model with rent, utilities, software, insurance, admin, and every machine note. Stress it with slower collections and higher repair spend. If the shop can’t keep a cash buffer after those hits, raise prices, cut fixed spend, or delay new equipment before taking more owner draw.

Track overhead weekly, not monthly.

Separate profit from cash.

Model debt service and reserves.

6

CNC Machining Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high CNC owner income scenarios

Owner income scenarios

Owner income here is driven by part mix, machine use, and staffing. Year 1, Year 3, and mature-year output change take-home fast, so low, base, and high cases matter.

Year 1, Year 3, and mature-year cases show how volume and margin change owner take-home.

Scenario

Low CaseDownside

Base CaseCore

High CaseUpside

Launch model

This is the slower opening path, where Year 1 volume and pricing keep owner income on the low side.

This is the modeled plan, where Year 3 scale and a fuller mix support solid owner income.

This is the stronger path, where mature-year throughput and mix push owner income higher.

Typical setup

Year 1 runs at 6,100 parts, about $1.24M revenue, 83.5% contribution margin, and about $624k operating profit before owner pay.

Year 3 reaches 13,000 parts, about $2.64M revenue, about 84.0% contribution margin, and about $1.61M operating profit before owner pay.

Year 5 reaches 17,500 parts, about $3.57M revenue, 84.7% contribution margin, and about $2.42M operating profit before owner pay.

Cost drivers

Lower order volume

tighter pricing

startup waste

fixed overhead

debt service

Higher part volume

steadier pricing

fuller machine use

larger payroll

lower unit overhead

Maxed capacity use

stronger part mix

tighter scrap control

higher throughput

disciplined labor

Owner income rangeBefore owner reserves

$624kLean income

$1.61MCore income

$2.42MUpside income

Best fit

Use this to test a slow launch, thin demand, or a shop that stays under capacity.

Use this as the working plan for budgets, hiring, and lender conversations.

Use this to test upside, expansion timing, and how much profit the shop can carry at full pace.

!

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; taxes, reserves, debt service, and the source's Quality Engineer FTE line can change take-home.

Under these assumptions, the shop generates $624K in first-year operating profit before owner pay, taxes, debt service, and reserves Revenue is $124M, direct and variable costs are $204K, fixed overhead is $130K, and complete payroll lines are $280K Actual owner draw depends on cash timing and reinvestment needs

It can pay the owner once contribution margin covers payroll, rent, utilities, insurance, software, and job costs In the first-year case, break-even before owner pay is about $491K in annual revenue, or $41K per month Any debt service, reserves, or added staff raises that threshold

Not always, but this model assumes staffed operations from the start Complete payroll lines include a $85K Lead Machinist/Shop Manager, a $75K CNC Programmer, and two Skilled Machinists at $60K each in the first year A solo owner may keep more labor cash but has lower capacity and more bottlenecks

Utilization, quoting accuracy, part mix, direct job costs, labor productivity, and fixed overhead drive owner income most In this model, first-year contribution margin is 835%, fixed overhead is $108K per month, and payroll is $280K Small misses in scrap, setup time, or downtime can quickly reduce draw

Improve billable machine time and quote accuracy before buying more equipment The model already carries $108K in monthly fixed overhead and at least $280K in first-year complete payroll Better scheduling, repeat jobs, fewer rejects, and tighter tooling control protect cash without adding debt or management load

About the author

Kevin West

Startup Cost Researcher

Kevin West is a startup cost researcher at Financial Models Lab who writes practical guides for people planning their first business. He focuses on break-even planning and on comparing business ideas by cost and effort, with an emphasis on realistic small business planning for founders with limited capital. His work connects business ideas to realistic startup budgets.

Choosing a selection results in a full page refresh.