How Much Conference Interpretation Rental Owners Can Make At $297M Revenue

You’re pricing rentals, labor, and equipment before the cash curve is clear This US model covers $507K to $297M in annual revenue, EBITDA from -$24K to $1465M, owner take-home, overhead, reserves, and onsite technical support economics

Owner income$110K-$1.58MNet margin-5% to 49%Revenue for target pay$223KBusiness difficultyHard

Want to test your owner-income case?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, gross margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. The model shows minimum cash near $669K in Month 13, and Year 1 EBITDA is negative, so early owner pay can be tight.

What profit margin can a conference interpretation equipment rental business make?

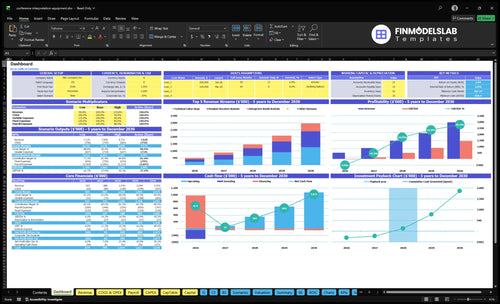

For a Conference Interpretation Equipment Rental business, the margin is tight at the start—see How Increase Profits Conference Interpretation Equipment Rental?—because direct event costs can run 165% of revenue in Year 1 and rise to 195% by Year 5. EBITDA, or cash left after direct event costs and before overhead, payroll, reserves, taxes, and debt, can move from negative in Year 1 to about 49% in Year 5 on $297M revenue. Accounting profit is not the same as spendable cash.

Year 1 pressure

165% direct cost load in Year 1

Freelance technicians drive labor cost

Freight and maintenance hit hard

Sales commissions add more drag

Year 5 take-home

EBITDA margin reaches about 49%

Based on $297M revenue

Sensitive to missing receivers and booth wear

Insurance and replacement reserves still matter

Can a conference interpretation equipment rental business scale?

Yes—Conference Interpretation Equipment Rental can scale, but only if it keeps buying inventory, adding technicians, and reinvesting cash. The model grows from 300 to 1,500 technical labor days and from 120 to 600 booth rentals, while payroll climbs from $250K in Year 1 to $590K in Year 5, a 136% increase. Scale improves when repeat conferences fill the calendar and equipment utilization stays high, but owner-operated installs protect early margin and also limit how many events you can run at once.

What drives growth

Repeat conferences fill more dates.

High utilization keeps gear productive.

Owner installs protect early margin.

More labor days support more events.

What constrains scale

Freelancers add capacity fast.

Quality risk rises with freelancers.

Overtime risk rises with peak dates.

Reinvestment is required, not optional.

How much revenue does a conference interpretation equipment rental business need to pay the owner?

Conference Interpretation Equipment Rental needs roughly $888K in Year 2 revenue before a $110K owner GM salary looks realistic; at $507K Year 1 revenue, EBITDA is -$24K, so distributions don’t pencil out. For setup context, see How To Launch Conference Interpretation Equipment Rental Business?; the key is that owner pay sits behind direct costs, payroll, overhead, capex, and cash reserves.

Pay Reality

Year 1 revenue: $507K

Year 1 EBITDA: -$24K

Owner GM target: $110K

No safe distributions in Year 1

Revenue Target

Year 2 revenue: $888K

Year 2 EBITDA: $127K

Fixed overhead: $159K before payroll

Payroll: $250K Year 1 to $590K Year 5

Conference Interpretation Equipment Rental Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers that matter most?

1

Booked Days

$507K-$2.97M

More conference days sold push revenue from $507K in Year 1 to $2.97M in Year 5.

2

Rental Rates

-$24K-$1.47M

Higher rates on receivers, booths, and labor lift operating profit fast as volume scales.

3

Utilization

300-1,500

Better use of inventory and crew days lets you handle more work before adding more gear.

4

Labor Control

16.5%-19.5%

Freight, subcontracting, and sales commissions sit near that cost band, so small cuts help margin.

5

Repeat Clients

34 mo

A stronger repeat base fills the calendar faster and supports the 34-month payback.

Conference Interpretation Equipment Rental Core Six Income Drivers

Booked Event Days

Booked Event Days

Booked event days are the number of paid days a conference uses receivers, booths, and on-site technical labor. More days mean the same sale can cover more billable time, so revenue per booking rises and fixed overhead gets absorbed faster. Here’s the quick math: technical labor days scale from 300 to 1,500, and booth rentals from 120 to 600.

The strongest lift comes from qualified multi-day conferences, not more small jobs. That improves utilization, but seasonality, cancellations, venue changes, and weak pipeline quality can cut booked days fast. One clean rule: if the calendar slips, take-home income slips with it because labor and equipment sit idle.

Grow Multi-Day Bookings

Track booked days by event type, not just total events. Split pipeline into one-day jobs and multi-day conferences, then watch conversion, cancellation rate, and average booked days per closed deal. If multi-day work is rising, utilization should follow, and that usually means better gross profit and more cash available for owner pay.

Measure booked days by month.

Separate conferences from small jobs.

Flag cancellations and venue changes early.

Price add-on days before quoting.

1

Average Rental Package Value

Average Rental Package Value

Package value rises when one quote bundles receiver units, headsets, transmitters, booths, onsite support, delivery, and add-on days. In this model, receivers move from $12 to $15, booths from $850 to $950, and technical labor days from $750 to $850. That lifts revenue per event and can improve owner pay if the quote covers the full on-site scope.

The risk is simple: if setup complexity is priced like a basic gear drop-off, margin gets squeezed. Here’s the quick math: higher package value raises top-line revenue, but take-home only improves when labor days, freight, and support hours are billed in line with actual work.

Price the full event scope

Track realized package value per event, plus the mix of receiver units, booth rentals, and technical labor days. The key input is total billed revenue divided by event count. If that number rises while labor stays controlled, gross margin improves and the owner has more cash for draws.

Review quotes where receivers stay below $15, booths below $950, or labor below $850. Also watch delivery and onsite support, because those hours can turn a strong sale into weak profit if they are not billed as part of the package.

2

Inventory Utilization And Capacity

Inventory Utilization

Receivers, transmitters, booths, and consoles only earn their keep when they turn into paid rental days. The model starts with $2,655K of capex across transmitters, headset inventory, booths, racking, IT setup, and testing gear, so idle stock hurts cash flow fast. If inventory sits unused, storage, maintenance, and replacement still hit EBITDA; if stock is too tight, the business loses events or pays for subrentals.

Track paid days per unit

Measure utilization as paid rental days divided by available rental days, then compare it with simultaneous bookings by asset type. The key inputs are unit counts, booked event days, and expected overlap across conferences. One line says it best: more paid days per unit means better owner take-home. Use capacity plans before peak dates so the fleet fills without forcing rush subrentals.

Count inventory by asset class.

Track paid versus available days.

Map event overlap by week.

Flag subrental use and shortages.

3

Technician And Delivery Cost Control

Technician and Delivery Cost Control

When direct event costs run high, owner pay gets squeezed fast. In this model, freelance technician subcontracting can take 60% to 75%, logistics and freight 50% to 65%, maintenance 25%, and sales commissions 30%. That means gross margin before payroll and overhead can fall to 40% to 25%, so one long load-in or extra pickup can wipe out profit on a small event.

What this estimate hides is scope creep: overtime, travel, venue load-in rules, testing time, and post-event pickup. If a $10,000 event carries 70% direct cost, only $3,000 is left for fixed overhead and owner draw. The key inputs are technician hours, freight quotes, miles traveled, event days, and rework time. Tighter control here means cleaner cash flow and more predictable distributions.

Track the job cost before dispatch

Build each quote from the actual event plan: technician day rate, freight, setup hours, test time, and pickup time. Then compare the planned direct cost to the target ceiling of 60% to 75% of event revenue. If delivery rules force extra labor or a second trip, reprice it up front. Here’s the quick math: every 10% cut in direct cost flows straight into gross margin and owner take-home.

Track hours by event stage.

Price overtime before the job.

Log freight by lane.

Charge for venue delays.

Review margin after every event.

Use post-event job costing to spot where margin leaks most: subcontract labor, freight, or re-delivery. If testing and pickup keep running over, tighten scope language and require signed load-in rules. That protects cash flow and keeps owner distributions tied to real profit, not padded revenue.

4

Equipment Replacement Reserves

Equipment Replacement Reserves

This reserve covers lost receivers, broken headsets, dead batteries, cases, repairs, firmware updates, and fleet refresh. In this model, the business needs $669K minimum cash in Month 13, so reserve cash is part of survival, not leftover profit. If owner draws ignore that floor, a single gear failure can trigger a cash call and strain delivery on the next event.

The owner’s take-home has to sit behind replacement spend. With $2,655K of capex before growth needs, every dollar paid out too early raises the risk of missed bookings, emergency buys, and rushed repairs. The tradeoff is clear: lower short-term distributions, but better fleet uptime and fewer surprise hits to gross margin and cash flow.

Keep Fleet Cash Ring-Fenced

Track reserve need by paid event days, active headset count, breakage rate, repair tickets, battery life, and refresh timing. Set owner draws only after the $669K cash floor is covered. That protects the business from one-off losses and keeps the fleet ready for the next multilingual event.

Count lost and damaged units.

Log repair and firmware spend.

Age the fleet by unit class.

Hold cash before owner draws.

What this estimate hides is timing: a good month can still fail if replacement cash lands after bookings are already committed. So match reserves to how fast gear wears out and how fast it must be replaced, not just to monthly profit.

5

Sales Pipeline And Repeat Clients

Sales Pipeline And Repeat Clients

Repeat associations, corporate meetings, international conferences, and event planners keep booked event days steadier, which matters because the model has to grow from $507K to $297M in revenue. That is about a 586x lift, so the business cannot rely on one-off jobs. Strong repeat demand feeds more receiver rentals, booth rentals, and labor days, while weak demand leaves gear idle and payroll exposed.

For the owner, this driver changes cash flow and pay. More repeat clients usually means smoother utilization, better forecasting, and less selling cost per booked day. The key inputs are repeat-client count, booked event days, average package value, and cancellation rate. One line: fewer gaps in the calendar means less strain on overhead and more reliable owner distributions.

Track Repeat Bookings

Measure how many event days come from repeat clients versus new leads, then track receiver rentals, booth rentals, and technical labor days per event. If repeat demand is thin, the business may still quote well but miss the volume needed to cover fixed labor, storage, and admin costs. Here’s the quick math: every extra booked day helps spread overhead across more paid rentals.

To improve this driver, keep a simple client file with past event dates, contact names, room counts, and quote history. Requote fast after each event, and forecast bookings by association season and conference calendar. The goal is a pipeline that stays full enough to keep equipment working, not sitting.

6

Conference Interpretation Equipment Rental Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with rental volume, staffing, freight, and fixed overhead. Revenue can rise fast, but distributions still depend on cash reserves and capex timing.

Low, base, and high cases for owner take-home under different operating loads.

Scenario

Low CaseCash tight

Base CaseBalanced

High CaseUpside

Launch model

This is the lower-earning path, where Year 1 volume keeps owner distributions limited.

This is the modeled path, where steady volume supports owner pay and some reserve-aware distributions.

This is the stronger-earnings path, where scale can support larger owner income if cash stays funded.

Typical setup

Year 1 profile with about $507K revenue, -$24K EBITDA, 15,000 receiver rentals, 120 booth rentals, and 300 labor days, so cash stays under pressure.

Year 3 profile with about $1.47M revenue, $500K EBITDA, 40,000 receiver rentals, 300 booth rentals, and 800 labor days, with room for salary plus cautious draws.

Year 5 profile with about $2.97M revenue, $1.465M EBITDA, 75,000 receiver rentals, 600 booth rentals, and 1,500 labor days, with stronger margin spread.

Cost drivers

Low job density

freight and logistics

subcontracted technicians

fixed payroll

reserve build

Higher volume

payroll coverage

freight and logistics

tech labor mix

reserve needs

High utilization

labor scaling

freight control

maintenance reserve

overhead dilution

Owner income rangeBefore owner reserves

No distributionsDeferred pay

Salary plus modest distributionsCore case

Salary plus larger distributionsUpside case

Best fit

Use this to test a slow start, tight cash, and a case where the owner may need to defer draws.

Use this as the main planning case for a working business that is growing but still needs cash discipline.

Use this to stress-test a mature operation with strong conference demand and tighter reserve control.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Under the researched model, owner income can include a $110K general manager salary if the owner fills that role and cash allows it Business EBITDA is -$24K in Year 1, then reaches $127K in Year 2 and $1465M in Year 5 Distributions are not guaranteed and should come after reserves

The model reaches breakeven in Month 14 and payback in 34 months That timing depends on hitting $507K in Year 1 revenue and growing to $888K in Year 2 The pressure point is cash: the model shows a $669K minimum cash need in Month 13

You don’t need to run every cable yourself, but the business needs strong AV technical control The plan starts with one lead AV technician at $75K and adds staff as volume grows If the owner lacks AV skill, they need reliable technicians, clear checklists, and enough margin to cover labor

Booked event days, package value, technician cost, and equipment utilization drive owner income most Year 5 assumes 75,000 receiver rentals, 600 booth rentals, and 1,500 technical labor days If those assets sit idle or freight and subcontractor costs rise, EBITDA and owner distributions fall fast

Protect cash by reserving for equipment replacement, controlling labor scope, and booking repeat multi-day conferences Initial capex is $2655K, fixed overhead is $159K per year, and minimum cash reaches $669K Profit can look strong while cash is tied up in inventory, payroll, and growth

About the author

Caleb Ross

Small Business Advisor

Caleb Ross is a small business advisor at Financial Models Lab who helps first-time entrepreneurs plan startup costs before launch. He studies common expenses, revenue drivers, and launch requirements, then turns broad business ideas into clear planning assumptions. His work focuses on pricing and profitability basics, with a practical, research-based approach to building realistic forecasts.

Choosing a selection results in a full page refresh.