How Much Construction Management Owners Make: $180K Pay Target

Construction Management Bundle

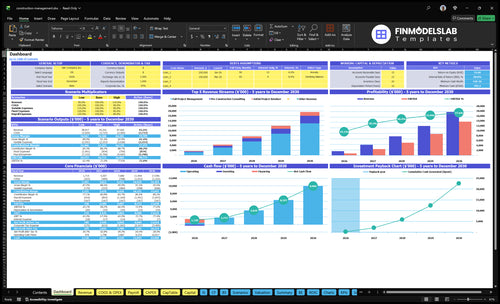

You’re planning owner pay before the firm has steady backlog, so revenue is not the same as take-home This five-year construction management business revenue and profit model uses $180,000 as the annual CEO/founder salary target, with fee revenue growing from $285,600 in Year 1 to $2,454,667 in Year 5 It covers fees, payroll, overhead, marketing, margins, reserves, and owner pay before personal taxes

Owner income$180kNet margin19%Revenue for target pay$2.45MBusiness difficultyHard

Want to test your construction management owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, reserves, debt, and operating discipline.

How do you check owner income in the Construction Management model?

Open the Construction Management Financial Model Template to see revenue build-up, staffing, direct costs, margin, cash reserve line, and owner take-home scenarios. Assumptions tabs cover service mix, billable hours, hourly rates, CAC, payroll, fixed expenses, and marketing charts. $285,600 Year 1 revenue rises to $2,454,667 in Year 5, while operating profit moves from -$348,320 to $462,400. Open the model.

Owner income model highlights

Owner take-home scenarios

Revenue and margin view

Assumptions tabs drive planning

Can a small construction management business be profitable?

Construction Management is not profitable in the staffed Year 1 model shown here: revenue is $285,600 versus $360,000 payroll, $166,800 fixed overhead, and $50,000 marketing, for a -$348,320 operating loss before reserves. A one-person version may work differently if overhead and staffing are much lower, but that is outside these source assumptions.

Why Year 1 misses

$285,600 revenue is the ceiling

$360,000 payroll is the biggest drag

$166,800 overhead adds heavy fixed cost

$50,000 marketing still burns cash

What to separate

Split owner work from staffed work

Lower overhead before adding headcount

Track billable hours per project

Test a lean solo model first

How much revenue does a construction management business need to pay the owner?

Construction Management needs about $1,940,889 in annual revenue to cover the $180,000 owner salary target as payroll, before reserves; for the key metric behind this, see What Is The Most Critical Measure Of Success For Your Construction Management Business?. Here’s the quick math: $1,746,800 in fixed payroll, overhead, and marketing divided by a 90% contribution margin.

Pay Owner

Treat $180,000 as payroll

Break-even revenue: $1,940,889

Contribution margin: 90%

Fixed cost base: $1,746,800

Year 5

Modeled revenue: $2,454,667

Operating profit: $462,400

Profit shown before reserves

Slow collections can limit distributions

How does scaling a construction management business affect owner income?

Scaling Construction Management can lift owner income, but the payoff comes late: revenue grows from $285,600 in Year 1 to $2,454,667 in Year 5, while payroll rises from $360,000 to $1,440,000. Here’s the quick math: operating profit stays negative through Year 4 and only reaches $462,400 in Year 5, before reserves. So the owner’s job shifts from delivery to sales, hiring, quality control, backlog management, and cash discipline.

Income path

200 customers in Year 1

933 customers in Year 5

$285,600 revenue in Year 1

$2,454,667 revenue in Year 5

Owner role shift

$360,000 payroll in Year 1

$1,440,000 payroll in Year 5

Profit stays negative through Year 4

Year 5 profit hits $462,400 before reserves

Construction Management Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six construction management income drivers?

1

Project Volume

$286K-$2.45M

Hitting 200 to 933 customers lifts revenue from $285.6K in Year 1 to $2.45M in Year 5, so owner pay depends on pipeline depth.

2

Contract Mix

70%-90%

A bigger share of full project management work raises fee capture and keeps more income in higher-value contracts.

3

Staffing Leverage

$360K-$1.44M

Payroll grows from $360K to $1.44M, so keeping senior time on billable work protects take-home profit.

4

Direct Margin

80%-90%

Keeping direct costs low leaves 80% to 90% of revenue to cover payroll, overhead, and profit.

5

Overhead Discipline

$166.8K

Fixed overhead runs at $166.8K a year, so small cuts here flow straight into operating profit.

6

Backlog Timing

10 mo

Cash stays tight until backlog turns into billing, and the model reaches payback in 10 months.

Construction Management Core Six Income Drivers

Managed Project Volume And Fee Capture

Managed Project Fee Capture

Owner income starts with construction management fee revenue, not the total construction cost under oversight. Fee capture means the share of customers, service allocation, billable hours, and hourly rate that turns into collected revenue. In the Year 5 math, 933 customers at 90% full project management, 120 hours each, and $200 per hour points to about $20.2 million in fee revenue.

The trap is treating a bigger project budget as bigger firm revenue. It is not. If hours, pricing, or allocation slip, payroll, overhead, and owner pay get squeezed fast. This driver has a high effect because more fee revenue funds staff, fixed costs, and the cash left for the owner to take home.

Track Billable Hours and Pricing

Measure customers, service mix, billable hours, and hourly rate every month. Here’s the quick math: 933 × 90% × 120 × $200 gives the Year 5 revenue path, so even small cuts in hours or rate hit the top line hard. One clean rule: if hours are not billable, they do not help owner pay.

Track actual hours by service type, then compare them with plan. Separate full project management from lighter support work, and watch whether projects are priced on real effort or on the size of the build. If fee capture drops, cash for payroll and overhead drops too, and the owner’s draw usually follows.

Track customers by service type

Log billable hours weekly

Compare rate to plan

Review collected fees monthly

1

Contract And Service Mix

Service Mix Drives Revenue Quality

This income driver is the mix of contract types and pricing. A bigger share of full project management at 70% to 90% allocation, priced around $180 to $200 per hour, lifts revenue quality more than lower-touch work. Initial retainers often run 20 hours at $150 to $170, while pre-construction consulting uses 40 to 60 hours at $200 to $220.

Here’s the quick math: the owner earns more when the firm sells higher-rate, higher-scope work, but cash and margin can swing by contract type. Fixed-fee and percentage-fee jobs can improve upside or compress it, and owner representative or CM at-risk work changes how much labor sits in each dollar of revenue. The key input is billable hours by contract type, not total project value.

Track Mix, Not Just Revenue

Measure hours, realized rate, and scope by service line each month. If pre-construction work is selling at $200 to $220 and full project management is landing near $180 to $200, the mix should tell you where gross margin and owner draw are strongest. What this estimate hides is collection timing, so watch cash conversion too.

Track hours by contract type.

Watch realized rate per hour.

Separate retainers from delivery work.

Forecast cash by project phase.

Test which mix funds payroll.

Use service mix to steer toward better-paying, easier-to-plan work. A heavier share of consulting or full management can raise near-term margin if staffing stays tight, but low-rate retainers can fill the pipeline without supporting much owner pay. The goal is a mix that keeps revenue steady and labor covered.

2

Staffing Leverage And Project Manager Capacity

Project Manager Load

This driver is the gap between revenue and delivery capacity. If senior project managers rise from 10 to 50 FTE at $120,000 each and junior project managers rise from 0 to 40 FTE at $80,000 each, stated Year 5 payroll reaches $1,440,000. That only helps owner income if each manager carries the right mix of work.

Here’s the quick math: more projects per manager can raise revenue, but only until supervision breaks down. When utilization gets too high for project complexity and site demands, the firm risks delays, rework, claims, and client churn. Those problems hit fee collection, margin, and cash flow, so the owner’s draw shrinks even when top-line growth looks strong.

Control Utilization

Track workload by project type, not just by headcount. The key inputs are active projects per manager, billable hours, supervision time, and how much senior review each job needs. If a manager is spending time on admin or fire drills, the firm is paying high salaries without getting clean delivery.

Use a simple weekly check: planned hours versus actual hours, plus open issues on each job. Keep senior managers on the hardest projects and push routine coordination to junior staff where possible. That helps protect gross margin and keeps payroll from outrunning fee revenue.

Track utilization by role.

Review project load weekly.

Flag rework and claim risk early.

Match senior staff to complex sites.

3

Direct Gross Margin After Delivery Costs

Direct Gross Margin After Delivery Costs

Owner income rises when project fees stay high and direct delivery costs stay lean. In this model, gross margin = fee revenue minus direct delivery costs, and those costs are expected to drop from 20% of revenue in Year 1 to 10% in Year 5. Pass-through construction costs are not firm revenue, so they should not inflate margin or owner pay.

Here’s the quick math: at $2,454,667 in revenue, each 1 margin point is about $24,547. That means small changes in site visits, specialist help, travel, tech, and client launch spend can move take-home profit fast. If delivery costs creep up, gross margin falls, and there is less cash left for payroll, overhead, and owner draw.

Control Delivery Cost Ratio

Track direct delivery cost by project and by month: project-related technology, specialist services, travel, site visits, and launch costs. Compare each job to the 20% to 10% target band and flag any project that runs hot early, because margin loss shows up before year-end. Use fee revenue, hours billed, and direct spend together so you can see true project profit.

Set a simple rule: if a project needs more travel, more expert support, or more client handholding, price it to protect margin. The goal is to keep delivery spend low enough that each fee dollar turns into cash for overhead and owner pay. When direct costs stay controlled, the business keeps more of every billed dollar.

4

Overhead Discipline

Overhead Discipline

Fixed overhead is $13,900 a month, or $166,800 a year, and it hits owner take-home before any profit draw. In Year 1, revenue is only $285,600, so overhead alone eats about 58% of sales. This includes rent, accounting and legal, utilities, software, insurance, and other admin costs, not project labor or direct delivery costs.

Here’s the quick math: $8,000 rent, $1,500 accounting and legal, $1,200 utilities, $1,000 software, and $700 insurance already total $12,400 a month. That leaves little room for waste. If overhead creeps up while billings stay flat, the owner gets paid later, or not at all.

Cut Fixed Overhead First

Track overhead as a monthly ratio against revenue, and split every cost into fixed overhead versus direct project cost. The goal is simple: keep recurring admin spend from rising faster than billings. If a line does not support more fee work, better cash collection, or lower risk, it needs a hard review.

Test the big levers first: office size at $8,000, software seats at $1,000, and outside services at $1,500. Use a rolling 12-month forecast so you can see when overhead will crowd out owner pay. If a cost saves less than it adds in revenue protection, cut it.

5

Cash Flow, Backlog, And Reserves

Cash Flow, Backlog, And Reserves

Construction management can look profitable on paper and still leave the owner short on cash. In Year 5, operating profit is $462,400 before reserves, taxes, debt, and reinvestment, but collections delays, retainage, paused projects, and claims can trap cash inside the business. That matters because payroll reaches $1,440,000, so the firm needs steady inflows, not just booked profit.

This driver depends on billing timing, backlog quality, client payment speed, and how much cash the firm keeps in reserve. The key warning is simple: accounting profit is not distributable cash. If payroll or project spend lands before client cash does, owner pay gets squeezed even when the income statement looks strong.

Track Cash Before Owner Draw

Measure cash conversion on every project: billed, collected, retainage held, and days cash sits unpaid. Build a weekly forecast that maps expected collections against payroll, overhead, and project spend. Here’s the quick math: with $462,400 operating profit and $1,440,000 of payroll, the business needs disciplined cash timing before any owner draw.

Keep a reserve policy tied to backlog risk, not gut feel. If projects pause or clients stretch payment, delay distributions and protect working capital first. Track backlog quality by payment terms, collection history, and timing gaps, then test whether the firm can cover the next payroll cycle without leaning on new invoices. That tells you if owner income is real or just on paper.

6

Construction Management Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high construction management owner income scenarios

Owner income scenarios

Owner income changes with project mix, staffing, and fixed overhead. Early cases can lose money even with revenue, while later years improve as billable hours and margins rise.

Low, base, and high cases show how project volume changes owner income.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Lower earnings path with early revenue and heavy overhead.

Modeled middle case with Year 3 scale and still-negative profit.

Stronger earnings path once revenue and margin improve by Year 5.

Typical setup

Year 1 uses $285,600 revenue, 80% contribution margin, $360,000 payroll, $166,800 fixed overhead, and $50,000 marketing before owner pay.

Year 3 uses $1,028,421 revenue, 85% contribution margin, $950,000 payroll, and -$342,642 operating profit.

Year 5 uses $2,454,667 revenue, 90% contribution margin, $1,440,000 payroll, and $462,400 profit before reserves.

Cost drivers

early revenue

payroll load

fixed overhead

marketing spend

margin pressure

project mix

senior staff payroll

fixed overhead

marketing spend

utilization

higher revenue

better margin

larger project mix

staffing scale

lower relative overhead

Owner income rangeBefore owner reserves

-$348,320Downside case

-$342,642Core case

$462,400Upside case

Best fit

Fits founders stress-testing a slow start or heavy payroll build.

Fits planners modeling a mid-cycle operating year before profit turns.

Fits upside planning once the team is full and project volume is strong.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The model supports a $180,000 CEO/founder salary target, but profit distributions are not available in the early years under these assumptions Operating profit is negative from Year 1 through Year 4, then reaches $462,400 in Year 5 before reserves, taxes, debt service, and reinvestment Cash timing still matters

In the provided five-year model, operating profitability appears in the mature year Revenue grows from $285,600 in Year 1 to $2,454,667 in Year 5, while payroll grows from $360,000 to $1,440,000 The key issue is that staffing and overhead arrive before enough fee revenue is built

Yes, reserves should come before extra owner distributions The model shows $462,400 in Year 5 operating profit before reserves, but no reserve percentage is provided A practical calculator should let you set a payroll reserve, project risk reserve, and reinvestment reserve before showing cash available to the owner

The biggest drivers are fee revenue, payroll, and margin discipline Year 5 fee revenue is $2,454,667, direct and variable costs are 10%, and payroll is $1,440,000 If project manager utilization slips or collections slow, the owner may still limit take-home even with strong booked revenue

The clean setup is a planned salary plus variable profit only when cash supports it This model uses a $180,000 owner salary target from the start, but the business posts a -$348,320 operating loss in Year 1 If cash is tight, fixed owner pay should be tested against revenue, backlog, and reserves

About the author

James Carter

Startup Guide Author

James Carter is a startup guide author at Financial Models Lab who focuses on startup budget assumptions for founders working with limited capital. He studies common expenses, revenue drivers, and launch requirements to help readers plan for rent, staff, equipment, and supplies. His small business startup guides connect business ideas with realistic startup budgets in a clear, practical way.

Choosing a selection results in a full page refresh.