How Much CGM Supplies Owners Make: $180K Pay Plus EBITDA

Continuous Glucose Monitoring Supplies

A CGM supplies business owner can make the modeled $180,000 CEO salary if the owner works in the business, plus possible distributions from EBITDA after reserves and other claims on cash In the first year, researched assumptions show $9863M in revenue, $6203M in EBITDA, and break-even in Month 2 The economics depend on collections, payer mix, product costs, denied claims, staffing, shipping, and how much cash the company keeps for inventory and compliance The mature-year scenario reaches $199389M in revenue and $164442M in EBITDA, but those figures are planning outputs, not guaranteed owner income

Owner income$6.38MNet margin62.9%Revenue for target pay$286kBusiness difficultyMedium

Want to test your CGM owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see how owner income shows up in the CGM model?

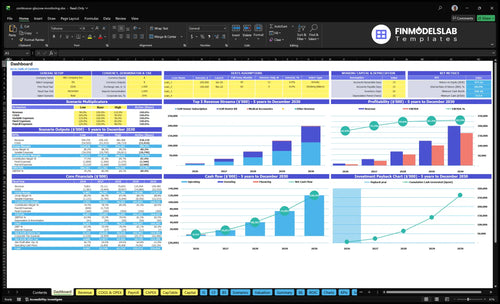

The dashboard connects patient volume, sales mix, costs, cash flow, and owner pay in the Continuous Glucose Monitoring Supplies Financial Model Template; Year 1 revenue is $9863M, EBITDA is $6203M, and minimum cash need hits $717K in Month 2. The charts also show mature-year revenue at $199389M and EBITDA at $164442M. Open the model.

Owner-income model highlights

Owner pay scenarios included

Month 2 break-even

Payback in 3 months

Mature year hits $199389M

How many CGM patients are needed to pay the owner?

For Continuous Glucose Monitoring Supplies, the owner needs about 31 active monthly repeat patients to cover a $180,000 salary alone, using collections, not billed charges. Here’s the quick math: Year 1 weighted order value is about $629, and after product, shipping, and payment costs, contribution is about $498 per monthly repeat customer. If you also cover Year 1 marketing, fixed overhead, non-owner payroll, and owner pay, the model needs about 249 active monthly repeat patients, and denials, missed reorders, delayed collections, and inventory buffers can push that higher.

Owner salary math

$629 Year 1 weighted order value

$498 contribution per repeat patient

31 patients cover $180,000

Use collections, not billed charges

Full monthly load

249 active repeat patients needed

Includes marketing and overhead

Adds non-owner payroll too

Reserve for denials and delays

Is a CGM supplies business profitable for an owner operator?

Yes, under the provided assumptions, a Continuous Glucose Monitoring Supplies owner-operator can turn profitable fast, with break-even in Month 2, payback in 3 months, and Year 1 EBITDA of $6,203M as stated in the model. But that profit is not cash you can safely pull out, because collections, reorders, and inventory timing drive the real result. The founder’s upside is best when they cover the modeled $180K CEO role and keep referrals, documentation, billing follow-up, and reorder cadence tight.

Owner-run upside

Break-even lands in Month 2.

Payback comes in 3 months.

Founder fills the $180K CEO cost.

Cash improves with faster collections.

Costs that stay real

Compliance audits cost $3K per month.

Insurance costs $45K per month.

Warehouse rent costs $12K per month.

Working capital still matters most.

How much does a CGM supplies business owner make in the United States?

A Continuous Glucose Monitoring Supplies owner can plan around a modeled $180,000 CEO salary if they run the company day to day, plus possible distributions from EBITDA after reserves, taxes, debt, reinvestment, and working capital; for KPI context, see What Are The 5 KPIs For Continuous Glucose Monitoring Supplies Business?. Year 1 shows $9.863M revenue and $6.203M EBITDA, a 62.9% EBITDA margin.

Owner Pay

Base operator salary: $180,000

Year 1 EBITDA: $6.203M

EBITDA margin: 62.9%

Distributions depend on cash needs

What Changes Pay

Keep collections on track

Control claim denials

Hold product costs near model

Grow the reorder base

Continuous Glucose Monitoring Supplies Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers behind CGM owner income?

1

Active Reorders

1.95K

A Year 1 repeat base of 1,950 with a 24-month life turns one sale into recurring orders, which is the cleanest path to owner take-home.

2

Collections

$9.9M

Year 1 revenue is about $9.9M, but only cash collected after denials and adjustments can pay the owner, so payer mix matters more than billed sales.

3

Gross Margin

79.1%

Year 1 cost load is about 20.9%, so gross margin near 79.1% drives how much EBITDA can flow into distributions.

4

Referral CAC

$150

A $150 CAC against a $450K Year 1 marketing budget keeps new-patient growth efficient, and higher CAC cuts take-home fast.

5

Cash Timing

$717K

Minimum cash bottoms at $717K in Month 2, so slow payments and bad debt reserves can block distributions even when revenue looks strong.

6

Operating Costs

$1.03M

Year 1 payroll is $735K and fixed overhead is $300K, so staffing and the $180K CEO salary have to stay tight for EBITDA to reach the owner.

Continuous Glucose Monitoring Supplies Core Six Income Drivers

Active Reorder Patients

Active Reorders

Here’s the quick math: $450K of marketing at $150 CAC creates 3,000 new customers. If 65% repeat, that’s 1,950 repeat customers. For a CGM supply business, the revenue ceiling comes from sensor and accessory reorders, not the first starter kit. If patients stop refilling, owner income drops fast because recurring cash is what funds profit and pay.

With a 24-month repeat lifetime in Year 1, active reorder volume is the core cash engine. The mature case assumes 48 months of lifetime and 120 monthly orders, which supports higher revenue and more stable distributions. Missed reorders cut revenue, slow inventory turns, and leave the owner with less cash to draw.

Protect Reorder Flow

Track active reorder rate, days since last order, and cohort retention by month. The key question is simple: how many patients are still buying sensors and accessories this month? Build refill reminders before stock runs out, and watch the gap between the 3,000 new customers and the 1,950 repeat customers. That gap tells you where owner income is leaking.

Use reorder data to plan inventory and cash. If monthly orders slip below the expected 100 in Year 1, cut spend before distributions, not after. Better reorder timing raises gross margin on recurring sales and keeps cash moving. If onboarding or refill follow-up takes too long, churn risk rises and the owner feels it in lower profit.

1

Payer Mix And Collections

Payer Mix and Collections

When CGM orders ship, revenue is not cash until the payer pays. Medicare, Medicaid, commercial insurance, and cash-pay each collect at different speeds, and denials or patient balances can cut the money that reaches the bank. The model shows revenue of $9,863M in Year 1 and $199,389M by mature year, but owner pay depends on collected revenue, not billed charges.

No cash, no draw. A stronger collection rate helps fund the $180K CEO salary and distributions; weak documentation can block cash even when orders ship. Watch denial rate, approval timing, accounts receivable age, and bad debt reserves, because slower cash pushes profit into the future and shrinks take-home income.

Measure Cash by Payer

Track paid claims by payer, not just shipped orders. Break out Medicare, Medicaid, commercial, and cash-pay, then compare approval time, denial rate, and A/R age each week. Here’s the quick math: if claims sit in receivables longer, the business needs more working cash, which can delay owner distributions even when sales look strong.

Fix missing chart notes fast.

Follow up on denials daily.

Reserve for bad debt.

Separate cash-pay from billed.

Use a cash forecast that starts with collected revenue, then subtracts write-offs and delayed payer cash. If onboarding takes too long or documentation is thin, orders can ship without payment landing on time, and that pressure hits payroll, the $180K CEO draw, and any distributions.

2

Gross Margin After Product Costs

Gross Margin After Product Costs

For continuous glucose monitoring (CGM) supplies, gross margin starts with what it costs to land each order: sensors, transmitters, receivers, adhesives, accessories, packaging, and shipping. In Year 1, wholesale inventory is 120% of revenue and packaging is 20%, so the model shows 860% product gross margin before shipping and merchant fees.

Add 40% logistics and 29% payment fees, and Year 1 contribution drops to 791%. Mature year improves to 100% wholesale, 12% packaging, 32% shipping, and 25% merchant fees, or 831% contribution. That still is not owner pay; payroll, marketing, rent, insurance, compliance, software, and reserves come out next.

Track Landed Cost Hard

Contribution margin means revenue left after product, shipping, and card fees. Track landed cost by SKU, then split freight, packaging, and merchant fees so margin leaks show up fast. If shipping or card fees rise, distributions tighten even when revenue looks strong.

Track landed cost by SKU.

Separate freight from packaging.

Watch contribution per order.

Here’s the quick math: every point saved on logistics or payment fees stays in cash for payroll and owner draw. What this estimate hides is timing risk; if inventory, shipping, or fees are paid before cash collects, the business can look profitable and still feel tight.

3

Referral And Prescription Pipeline

Referral And Prescription Pipeline

Owner income here depends on how many eligible patients get documented, approved, and onboarded fast enough to become repeat sensor buyers. With $450K of Year 1 marketing spend at $150 CAC, the model adds about 3,000 new customers; in the mature year, $950K at $120 CAC adds about 7,917. One clean one-liner: no pipeline, no recurring orders.

Here’s the quick math: more clean referrals lift active accounts, and active accounts create monthly reorder cash that supports profit and owner draws. The risk is operational, not just sales. If documentation is missing, follow-up is slow, or reorder setup is weak, the business ships fewer recurring orders and the owner’s take-home income drops even when leads are coming in.

Improve Referral Flow And Onboarding

Track referrals received, documentation completion, days to onboard, and reorder activation rate. Those four inputs tell you whether marketing is turning into cash. The mix also matters: recurring sensor subscriptions rise from 700% in Year 1 to 800% in the mature year, so the pipeline should be built for retention, not just first orders.

Keep a tight handoff between referral, chart review, and first shipment. If onboarding slips, patients churn before the monthly order cycle starts, which raises CAC payback time and cuts cash available for payroll, inventory, and owner profit. The best fix is simple: fast document chase, same-day follow-up, and a clear reorder setup before the first box ships.

Measure approval lag daily.

Audit missing documents weekly.

Set reorders before first delivery.

4

Billing Denials And Cash Timing

Billing Denials And Cash Timing

Billing denials hit owner pay fast because rejected claims, missing notes, delayed payer checks, bad debt, and refunds reduce cash even when devices ship. In continuous glucose monitoring (CGM), that means accounts receivable risk, or money owed but not yet collected. The model breaks even in Month 2, and minimum cash need peaks at $717K in Month 2, so slow collections can block distributions.

What this estimate hides is timing. If payroll, rent, inventory replacement, and refunds are already committed, even a small denial-rate rise can wipe out several months of owner draws. The key inputs are clean-claim rate, days sales outstanding (days to collect cash), denial rate, and reserve levels. One clean claim today is worth more than a bigger bill paid late.

Cut Denials Before They Cut Draws

Track the full cash path, not just billed revenue. Measure clean-claim rate, denial reasons, payer age buckets, and days sales outstanding. If claims sit too long or docs are missing, cash stays trapped and owner pay shrinks even when sales look fine. Use reserves first for denied claims, payer delays, inventory replacement, and refunds before any distribution.

Watch these four numbers every week:

Clean-claim rate

Denial rate

Days sales outstanding

Cash reserve balance

Here’s the quick rule: faster documentation, faster follow-up, and tighter reserves protect owner income. If collections slip while payroll and rent stay fixed, profit on paper can turn into a cash squeeze fast.

5

Operating Costs And Owner Role

Owner Role and Overhead

This cost bucket covers billing staff, customer service, fulfillment, software, insurance, compliance, rent, and owner replacement labor for continuous glucose monitoring (CGM) supplies. Year 1 fixed overhead is $25K per month, or $300K per year, and payroll is $735K. Before product cost, the business is already carrying $1.035M a year in operating spend.

The $180K CEO line is the key owner decision: if the founder runs the company, that can be owner salary; if not, it is a hired cost. True owner profit only matters after paying for the labor needed to run the business, not after hiding the founder’s time outside the model.

Price the CEO Seat

Track overhead and payroll by role every month, then test whether each seat is tied to active orders. Here’s the quick math: $25K × 12 + $735K = $1.035M. If revenue or collections slip, fixed pay and rent do not, so owner draws should come after the CEO role is fully funded.

Separate owner salary from profit.

Review payroll by function.

Watch rent, software, compliance.

If the owner is acting as CEO, set the $180K line in the forecast from day one. That keeps cash flow, staffing, and take-home pay honest, and it stops the model from overstating margin with unpaid labor.

6

Continuous Glucose Monitoring Supplies Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and scaled CGM owner income scenarios

Owner income scenarios

Owner income moves with CAC, repeat buying, and staffing. The low, base, and high cases show how scale changes earnings as the model matures.

Low, base, and high cases show how marketing and reorder density change owner income.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is the lower earnings path built on Year 1 economics.

This is the modeled middle path built on Year 3 scale and stronger reorders.

This is the stronger earnings path built on mature-year scale and tighter unit economics.

Typical setup

Revenue is $9.863M, EBITDA is $6.203M, marketing is $450K, payroll is $735K, and fixed overhead is about $300K as 3,000 new customers and 1,950 repeat customers build.

Revenue reaches $70.693M, EBITDA is $56.282M, marketing is $750K, CAC is $130, repeat customers are at 75.0%, lifetime is 36 months, and orders run 110 per month with 1.70 units per order.

Revenue reaches $199.389M, EBITDA is $164.442M, marketing is $950K, CAC is $120, repeat customers are at 80.0%, lifetime is 48 months, orders run 120 per month with 2.00 units per order, and contribution after product and fulfillment costs is 83.1%.

Cost drivers

Marketing spend

payroll load

fixed overhead

repeat orders

product mix

CAC decline

repeat rate

36-month lifetime

order density

unit mix

Lower CAC

48-month lifetime

higher order density

stronger contribution

mature scale

Owner income rangeBefore owner reserves

$6.2M EBITDALow Case

$56.3M EBITDABase Case

$164.4M EBITDAHigh Case

Best fit

Use this to test a slower ramp-up with heavier early overhead and less repeat density.

Use this as the normal planning case for a scaled operation with steadier reorders.

Use this to stress-test upside if repeat buying, order density, and margin all improve together.

!

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The model shows $9863M in first-year revenue and $199389M by the mature year under the provided assumptions That revenue is driven by repeat orders, not just starter kits Year 1 uses 3,000 acquired customers, a 650% repeat rate, and 100 monthly order per repeat customer

The modeled break-even point is Month 2, with payback in 3 months That fast payback depends on collections happening close to plan, CAC staying near $150 in Year 1, and gross contribution staying near 791% If denials or inventory cash needs rise, payback can stretch

Yes, cash reserves matter even with strong EBITDA The model shows minimum cash of $717K in Month 2, plus $495K of startup capex across warehouse systems, refrigeration, platform development, equipment, automation, hardware, security, and vans Inventory, billing delays, and compliance needs can tie up cash before owner distributions

The biggest drivers are active reorder patients, collected revenue, gross margin, denial control, staffing, and reserves In Year 1, the model carries $735K of payroll, $300K of fixed overhead, and $450K of marketing Owner take-home improves when repeat orders rise without matching increases in denials or labor

Start with the modeled $180K CEO salary, then treat EBITDA distributions as variable Year 1 EBITDA is $6203M, but distributions should come after taxes, debt, working capital, inventory reserves, and reinvestment If a hired CEO replaces the owner, that $180K stays as a business cost

About the author

Liam Foster

Business Idea Researcher

Liam Foster is a business idea researcher at Financial Models Lab, focused on the revenue and profit basics that early-stage founders need when preparing a simple business plan. He helps simplify business plans for non-finance readers by turning business model overviews into clear, practical insights. With a simple, confident approach, Liam breaks down revenue, expenses, and profit in a way that makes financial thinking easier to understand and use.

Choosing a selection results in a full page refresh.