How Much a Commercial Crab Pot Supply Owner Can Make at $282M Sales

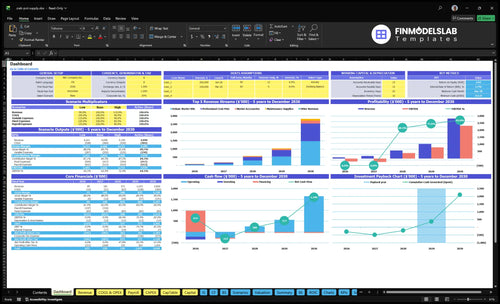

This five-year model estimates owner income from crab pots, starter kits, accessories, and maintenance supplies, not a fixed wage The business reaches Month 26 breakeven, with EBITDA, or profit before interest, taxes, depreciation, and amortization, moving from -$211k in Year 1 to $2313M in Year 5

Owner income$75kNet margin68%Revenue for target pay$571kBusiness difficultyHard

Want to test your crab pot supply owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Actual owner income changes with sales, margins, payroll, debt, taxes, and reserves.

How do you check owner income in the Commercial Crab Pot Supply model?

Commercial Crab Pot Supply makes money on a blended margin, not a simple retail markup model. In Year 1, inventory sourcing runs at 120% and order fulfillment plus shipping at 70%, leaving about 810% before fixed costs and payroll; for setup cost context, see How Much Does It Cost To Start Commercial Crab Pot Supply Business?. By Year 5, those direct costs ease to 100% and 50%, leaving about 850%, but owner income still gets squeezed if freight, damaged stock, supplier pricing, or fleet discounts compress margin.

Margin mix

Professional pots move from 400% to 300%.

Starter kits rise from 250% to 350%.

Direct costs are sourcing, fulfillment, shipping.

Blended margin matters more than markup.

What cuts profit

Freight costs can erode spread fast.

Damaged stock hits margin immediately.

Supplier pricing changes move the floor.

Fleet discounts can lower owner income.

How much revenue does a crab pot supply business need to pay the owner?

Revenue by itself won’t pay the owner at Commercial Crab Pot Supply; the model says cash has to clear 150% to 190% direct costs, $834k a year of fixed overhead, payroll, and seasonal inventory timing first. Breakeven lands in Month 26, after $181k in Year 2 revenue and before $571k in Year 3 revenue. For a $100k owner target, the model also needs a peak cash reserve of $311k, and that excludes taxes and personal debt.

What cash must cover

150% to 190% direct costs first

$834k fixed overhead per year

Seasonal inventory ties up cash

Payroll starts near $181k in Year 1

Owner pay math

Breakeven hits in Month 26

Year 2 revenue is $181k

Year 3 revenue rises to $571k

Peak reserve reaches $311k

Is a crab pot supply business profitable year-round?

Commercial Crab Pot Supply can make money over a full mature year, but it’s not a quick cash business: the model shows losses in Years 1 and 2, breakeven in Month 26, and payback in Month 45. Cash gets tight because you buy inventory before peak sales, and regional rules, fleet ties, warehouse space, and delivery limits all affect how fast that stock turns into cash. Unpaid owner labor can hide the real picture, so true profit is lower than the headline number if you don’t pay yourself.

Cash pressure

Years 1 and 2 show losses

Month 26 is breakeven

Month 45 is payback

Pre-season buying strains cash

Profit levers

Improve pre-orders

Grow repeat accounts

Lift accessory attach rates

Speed inventory turns

Commercial Crab Pot Supply Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers behind crab pot supplier profit?

1

Seasonal Volume

$85K-$2.82M

Weekend traffic is the main engine, and visitor growth turns into the jump from $85K in Year 1 revenue to $2.82M in Year 5.

2

Product Mix

2-4 units

More deluxe kits and a bigger basket lift average ticket and spread fulfillment cost across more items.

3

Landed Cost

19%-15%

Inventory sourcing and shipping drop from 19% of sales to 15%, so each order keeps more cash.

4

Cash Cycle

$311K

Slower stock turns tie up cash, and the model still needs a $311K floor before Month 26 breakeven.

5

Channel Mix

15%-28%

More repeat buyers lift the share from 15% to 28% of new customers, which cuts ad drag and steadies reorders.

6

Labor Load

$22K/mo

Rent, payroll, and ops work run about $22K a month, so lean staffing is what protects owner take-home.

Commercial Crab Pot Supply Core Six Income Drivers

Seasonal order volume and pre-season demand

Seasonal Order Volume

Seasonal order volume is the number of visitors and orders before and during peak crab season. In the model, Mondays rise from 45 to 160 visitors, Fridays from 75 to 270, and Saturdays from 120 to 450; conversion improves from 45% to 70%. That lift spreads fixed overhead and payroll across more sales, so owner pay improves only if cash comes in before stock gets bought.

Track Pre-Season Demand Early

Here’s the quick math: more pre-season orders help cash conversion, but early inventory buys can trap cash. Fleet buyers ordering pots and replacement supplies before season are the best signal. Watch daily visitors, conversion rate, and pre-season deposits together, not just annual revenue. Annual sales can look strong while monthly cash stays tight, especially if inventory is bought before orders are collected.

Track weekday and weekend traffic separately.

Compare pre-season orders to inventory buys.

Hold back cash for peak replenishment.

1

Product mix and blended gross margin

Product Mix and Blended Gross Margin

Blended gross margin is the average margin across the whole cart. When bulky pots are paired with accessories, repair items, and repeat supplies, owner take-home improves because those add margin without adding much freight. In the model, pots move from $145 to $165 and kits from $325 to $365, so the same customer can generate more profit.

The mix still matters. Professional pots fall from 400% to 300% of mix, starter kits rise from 250% to 350%, accessories hold at 200%, and maintenance supplies hold at 150%. Blended margin depends on sourcing, pricing, freight, and customer type; heavy fleet discounts can lift volume but cut distributable cash.

Track Margin by Cart Type

Track margin by order type, not just total revenue. Measure average order value, freight per order, and the attach rate for accessories and maintenance supplies. If a pot sale adds volume but the shipping bill eats the extra margin, the mix is too heavy on low-return items.

Set a price floor before discounting fleet accounts. Use $165 for pots and $365 for kits as current markers, then test whether bundles still cover sourcing and freight and leave enough gross profit for owner pay. If discounts rise faster than repeat supply sales, cash gets tight fast.

2

Landed cost, freight, and supplier pricing

Landed Cost and Freight Pressure

Landed cost is the product cost plus freight and handling to get inventory ready to sell. For bulky crab pots and traps, that cost can eat owner income fast. In this model, inventory sourcing costs improve from 120% of revenue in Year 1 to 100% in Year 5, while fulfillment and shipping improve from 70% to 50%. Less drag here means more gross profit and more cash available for owner draw.

Here’s the quick math: a 1-point cost increase on $282M of revenue means about $282k less gross profit. What this hides is the extra hit from damaged inventory, minimum order quantities, and rushed replenishment before peak demand. If supplier terms worsen or freight spikes, the owner can grow sales and still see take-home pay fall.

Track Freight Before It Hits Margin

Measure landed cost per sellable unit by line item: unit price, inbound freight, handling, and damage. Also track freight as a share of revenue, order minimums, and rush replenishment spend. If a heavier pot line or slow supplier pushes landed cost above plan, raise price, trim mix, or switch to smaller, faster buys before owner draw gets squeezed.

Use a simple rule: compare quoted supplier cost to the final sell-ready cost, not just the invoice price. The business wins when it can keep fulfillment and shipping near the planned 50% level and avoid emergency reorders right before season. That protects gross margin, cash flow, and the owner’s paycheck.

Track landed cost by SKU.

Log damage and freight claims.

Test smaller, earlier replenishment.

3

Inventory turns and working capital

Inventory Turns

Inventory turns is how often stock is sold and replaced. For a crab gear seller, that matters because profitable pots and traps can still block owner draw if cash is trapped on shelves. With $45k of starting inventory and $1.285M of capital spending, plus a $311k minimum cash need in Month 25, slow turns can force outside funding.

The income effect is simple: faster turns free cash, reduce warehouse drag, and keep buying power for the next season. Slow-moving sizes or shifting regional gear tastes create dead cash, so sales can look fine while take-home pay stays thin. One clean rule: cash on hand matters as much as gross margin.

Track Turns Before You Reorder

Track turns by SKU, not just total sales. Inventory turns means cost of goods sold divided by average inventory, so the inputs are units sold, average stock value, reorder timing, and cash tied in open purchase orders. Faster turns lower outside borrowing and make owner pay more reliable.

Use deposits before bulk buys.

Watch aged stock by size.

Cut slow regional items early.

Pre-season commercial deposits help fund bulk pots before cash leaves the account. If turns slip, stock sits longer, borrowing rises, and owner draw gets pushed back even when the P&L shows profit.

4

Customer channel mix and repeat buyer relationships

Repeat commercial accounts

Repeat commercial crabber accounts make demand more stable, so the owner can forecast inventory and labor with less guesswork. In this model, repeat customers rise from 150% of new customers in Year 1 to 280% in Year 5, repeat customer lifetime grows from 12 to 24 months, and repeat orders move from 2 to 4 per month.

That helps revenue visibility, but it can also pull down near-term income if larger buyers ask for discounts or credit terms. More volume from repeat accounts can still leave owner draw tight when receivables lag, wholesale pricing is pressured, or one buyer becomes too large a share of sales.

Track repeat order quality

Measure repeat share, orders per account per month, average discount, and days to pay. If repeat demand rises but cash stays tight, the issue is usually credit terms, not sales. Keep a simple view by account so you can see which buyers add profit and which ones only add volume.

Watch concentration by top accounts.

Limit deep discounts on bulk orders.

Shorten terms for slow payers.

Here’s the quick read: more repeat orders can raise gross profit, but owner pay improves only when margin and cash collection stay in line. If a big account buys often but pays slowly, the business looks stronger than the bank balance.

5

Overhead, labor, delivery, and owner involvement

Overhead, labor, and owner time

This driver is the cost of keeping the crab gear business running: rent, marketing, utilities, platform fees, insurance, payroll, and delivery work. Fixed overhead is $834k per year, including $54k rent, $144k marketing, $78k utilities and security, $42k platform and hosting, and $3k insurance. Payroll is about $181k in Year 1 and $266k in Year 5, so owner take-home depends on sales covering those costs.

The key trap is the $75k general manager line. If the owner does that work, it can be owner pay; if staff does it, it is a real expense. Replacing paid labor with unpaid owner hours can make profit look stronger than cash really is, especially when sales, purchasing, fulfillment, and delivery all hit at once.

Separate paid labor from owner hours

Track paid labor, owner hours, and delivery cost on separate lines. Here’s the quick math: every dollar saved in overhead or payroll raises cash for owner draw, but only if the work still gets done. If the owner handles sales, purchasing, packing, and delivery, count those hours as compensation when you judge true profit.

Set a monthly labor cap against sales and review it with order volume. If you add staff before demand is steady, owner income gets squeezed fast. Document who does sales, picking, packing, and delivery, and mark each role as paid or owner-run so the business does not overstate earnings.

6

Commercial Crab Pot Supply Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high crab pot supply owner-income cases

Owner income scenarios

Owner income swings with traffic, stock turns, and freight. Year 1 has no safe draw; Year 3 can support pay after reserves; Year 5 has strong distribution capacity.

Low, base, and high owner-pay paths for this crab pot supply business.

Scenario

Low CaseLoss case

Base CaseBreak-even+

High CaseUpside case

Launch model

This is the lower earnings path, where the store is still absorbing rent, payroll, and inventory costs.

This is the modeled middle path, where volume and mix support positive EBITDA and owner pay after reserves.

This is the stronger earnings path, where scale, repeat accounts, and mix create high distribution capacity.

Typical setup

Year 1 models about $85k revenue, 4.5% visitor-to-buyer conversion, 2 units per order, 19% direct costs, about $181k payroll, and no safe owner draw.

Year 3 models about $571k revenue, 5.5% conversion, 3 units per order, 17% direct costs, and $390k EBITDA before owner pay.

Year 5 models about $2.82M revenue, 7.0% conversion, 4 units per order, 15% direct costs, about $266k payroll, and $2.313M EBITDA before taxes and reinvestment.

Cost drivers

Year 1 traffic

19% direct costs

$181k payroll

$83.4k fixed overhead

Year 3 traffic

17% direct costs

stronger conversion

repeat customer lift

controlled overhead

Year 5 traffic

15% direct costs

$266k payroll

repeat fleet accounts

scale mix

Owner income rangeBefore owner reserves

No safe drawNo safe draw

Pay after reservesPay after reserves

Strong draw capacityStrong draw capacity

Best fit

Use this to stress-test a launch year with thin traffic and no distribution room.

Best for owners planning a stable operating year and checking when pay starts after reserves.

Fits owners who can manage pre-orders, stock, freight, and repeat fleet accounts.

!

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or promised distributions.

In this model, early owner distributions are limited because EBITDA is -$211k in Year 1 and -$251k in Year 2 If the owner works as general manager, the payroll plan includes $75k per year Larger distributions become more realistic after Month 26 breakeven, subject to reserves, taxes, debt, and inventory needs

The researched model reaches breakeven in Month 26 and payback in Month 45 That timing reflects revenue rising from $85k in Year 1 to $571k in Year 3, while the business absorbs payroll, rent, marketing, inventory, and delivery costs Cash gets tight first, with a $311k minimum cash need in Month 25

You likely need working capital or financing in this model Startup capex totals $1285k, including $45k for initial inventory, and the minimum cash need reaches $311k before breakeven Even profitable orders can strain cash if pots, rope, buoys, and supplies must be bought before seasonal sales arrive

The biggest factors are seasonal order volume, product mix, freight, inventory turns, repeat accounts, and payroll Direct costs move from 190% of revenue in Year 1 to 150% in Year 5 Repeat customers also matter, rising from 150% to 280% of new customers across the model

Improve cash timing before chasing more revenue Pre-orders, deposits, faster inventory turns, higher accessory attach rates, and repeat commercial accounts help turn gross profit into owner draw In this model, revenue reaches $282M by Year 5, but distributions still depend on taxes, debt service, reserves, and reinvestment

About the author

Ryan Spencer

First-Time Founder Guide Writer

Ryan Spencer writes for Financial Models Lab, where he focuses on launch budget planning and simple launch planning for first-time founders. He helps readers estimate startup needs before opening a physical location, breaking down business costs in clear, practical language. His work is built for people who want a realistic view of what it really takes to open a business, so they can plan with more confidence and fewer surprises.

Choosing a selection results in a full page refresh.