How Much Can A Data Entry Service Owner Make With $150k CEO Pay?

You’re planning owner pay before the data entry service is fully stable, so the clean answer is salary first, distributions later In this five-year model, planned owner compensation is $150,000 per year, but EBITDA is negative in Year 1 and Year 2, with break-even in Month 20 These are planning assumptions, not guaranteed earnings, wages, tax advice, or required owner distributions

Owner income$12.5kNet margin85.0%–88.8%Revenue for target pay$79.7kBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want the six income drivers?

1

Contract Volume

$-349K->$3.1M

More active contracts and more billable hours are what move this business from a Year 1 loss to a Year 5 profit.

2

Price Mix

$450-$3.4K

Shifting work from basic entry to advanced and custom jobs raises revenue per customer and lifts owner take-home.

3

Labor Cost

15%-11.2%

Direct COGS ease from about 15% to 11.2%, so every point saved drops straight into profit.

4

Utilization

25-45h

Pushing billable hours per active customer from 25 to 45 spreads staff and software cost across more revenue.

5

QA Quality

1.5%-1%

Fewer errors and less rework protect margin by keeping compliance and QA cost from creeping up.

6

Retention

$550->$420

Lower CAC and better retention cut the cash needed to replace lost clients while the business works toward Month 20 break-even.

Want to see how owner income shows up in the model view?

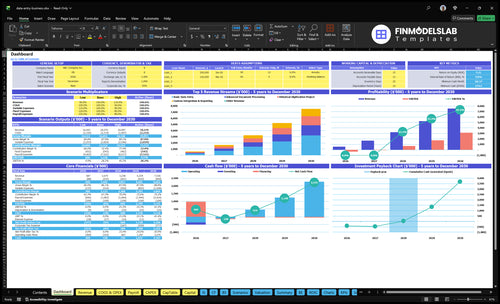

This view shows revenue, EBITDA, costs, reserves, owner pay assumptions in the Data Entry Service Financial Model Template; open it. The dashboard tracks Year 1 EBITDA of -$349,000, month 20 break-even, $274,000 minimum cash need, and Year 5 EBITDA of $3.131 million.

Owner-income model highlights

Revenue, EBITDA, cash

Owner pay scenarios

Next planning step

How many clients does a data entry business need?

No universal client count exists for a Data Entry Service, because revenue changes with contract size, workload, and margin. Under Year 1 assumptions, you need about $79,700 in monthly revenue to cover $150,000 owner pay, non-owner payroll, fixed overhead, marketing, and 275% variable cost needs. That works out to about 177 Basic Data Entry clients at $450/month or 29 Custom Integration and Reporting clients at $2,800/month, before capacity checks.

Revenue math

$79,700 monthly revenue target

177 Basic clients at $450

29 Custom clients at $2,800

275% variable cost load

Client count reality

109 acquired customers in Year 1

Retention is separate from acquisition

Active workload is a separate check

Capacity can cap client growth fast

Is it better to hire data entry operators or do the work yourself?

If you want near-term cash, doing the work yourself helps because you avoid operator payroll, but it caps billable capacity and keeps you in production. In a Data Entry Service, the model starts with 3 data entry operators at $40,000 each in Year 1 and grows to 20 operators by Year 5, while QA staffing rises from 1 specialist to 5. That means hiring is a scale choice, not an automatic upgrade.

Do it yourself

Protects short-term cash

Avoids operator payroll

Keeps you in production

Limits billable capacity

Hire and scale

Starts with 3 operators in Year 1

Reaches 20 operators by Year 5

QA grows from 1 to 5

Shifts owner to sales and supervision

Can a data entry business owner make a full-time income?

Yes, a Data Entry Service owner can make a full-time income, but this model pays it through planned CEO compensation of $150,000 per year, or $12,500 per month, not early excess profit. The key issue is cash timing: What Is The Most Critical Metric To Measure The Success Of Your Data Entry Service Business? matters because EBITDA is -$349,000 in Year 1, -$64,000 in Year 2, and break-even comes in Month 20.

Owner Pay

Set CEO pay at $12,500/month

Plan annual pay of $150,000

Use payroll, not early profit draws

Fund losses before Month 20

Staffed Model

Year 1 EBITDA: -$349,000

Year 2 EBITDA: -$64,000

Team includes CEO, operations, QA, sales

Also includes 3 operators and 1 QA specialist

Key Takeaways

Recurring contracts stabilize revenue and cut sales pressure.

Advanced work helps only if costs stay controlled.

Labor and QA costs can compress margins fast.

Renewals matter more than chasing new leads.

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts fast here because early ramp losses, staffing, and overhead hit before scale. By Year 3 and Year 5, EBITDA improves, but take-home still depends on taxes, reserves, debt service, and reinvestment.

Low, base, and high cases show how ramp, staffing, and margin shape owner pay.

Scenario

Low CaseSolo caution

Base CaseStaffed growth

High CaseMature platform

Launch model

Owner income is still constrained by early ramp losses and funding needs before break-even.

Owner income becomes modeled on a post-breakeven platform with Year 3 EBITDA at $695,000 before taxes and reserves.

Owner income comes from a mature Year 5 platform with $3.131 million EBITDA and a larger staffed bench.

Typical setup

The business is in early stage mode, with $150,000 owner salary, Year 1 EBITDA of -$349,000, 150% direct COGS, 125% variable costs, and $9,050 monthly fixed overhead.

The model is past break-even by Year 3, with $150,000 owner salary, $695,000 EBITDA before taxes, and room for reserves, debt service, reinvestment, and optional distributions.

By Year 5, the platform runs with 20 data entry operators and 5 QA specialists, $150,000 owner salary, and $3.131 million EBITDA before owner payouts.

Cost drivers

Year 1 EBITDA -$349k

150% direct COGS

125% variable costs

$9,050 fixed overhead

funding gap before break-even

Year 3 EBITDA $695k

post-breakeven scale

taxes and reserves

debt service

reinvestment

20 data entry operators

5 QA specialists

$3.131m EBITDA

112% direct COGS

90% variable costs

Owner income rangeBefore owner reserves

Salary at riskNegative EBITDA

Salary plus upsidePost-breakeven

Salary plus distributionsScaled upside

Best fit

Best for solo operators stress-testing a funding gap before scale.

Best for a staffed growth plan that wants a clear profit path.

Best for a mature operating platform checking upside after staffing and QA scale.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; EBITDA does not equal owner take-home.

Data Entry Service Core Six Income Drivers

Recurring contract volume

Recurring contract volume

Owner income rises when monthly work repeats instead of resetting every month. In this model, each active customer carries about 25 billable hours in Year 1, rising to 45 billable hours by Year 5, so the same sales base can support more revenue, steadier cash flow, and less owner selling time. The risk is thin client concentration or too much one-off digitization work.

Here’s the quick math: more active customers and higher renewal rates raise monthly workload without a matching jump in sales effort. That usually improves staffing because you can plan recurring forms, invoices, CRM updates, database cleanup, and document queues. If renewals slip, the owner is back to hunting for new work just to hold revenue flat.

Track volume, not just bookings

Measure active customers, monthly billable hours, renewal rate, and the share of recurring work versus one-off projects. The goal is simple: keep the pipeline full of repeat jobs so revenue stays predictable and the owner can pay themselves from ongoing margin, not emergency sales.

Count active recurring clients monthly.

Track hours per client.

Watch renewals before expiry.

Limit one-client concentration.

If one customer drives too much of the queue, a lost renewal hits profit and payroll fast. The cleanest improvement is to push every new contract toward repeat work with defined forms, invoices, database updates, and fixed monthly queues.

Accuracy, QA, and rework

Accuracy and Rework

When this work slips, revenue can still look fine but owner pay drops fast. The cost sits in free rework, client corrections, missed fields, and QA time. This model assumes data security compliance and audits at 15% of revenue in Year 1, easing to 10% in Year 5, plus QA payroll rising from $55,000 to $275,000.

The key inputs are accuracy rate, error rate, duplicate checks, missed fields, client corrections, and QA hours. If the service promises 99.9% accuracy but the team is not pricing and staffing for it, margin gets eaten by cleanup. That lowers gross profit, slows cash, and cuts the owner’s take-home draw.

Price QA Into the Deal

Track QA like a cost center, not a nice-to-have. Build each tier around the actual review load, then measure how many records need a second pass, how often clients send work back, and how many QA hours each contract uses. If QA is underpriced, the owner is funding the gap out of margin.

Track accuracy by client and task type.

Bill for heavy review and audits.

Cap free corrections in contracts.

Review QA hours every month.

Productivity and utilization

Billable Utilization

Billable utilization is the share of paid operator time that becomes client work. For this model, average billable hours per active customer rise from 25 per month in Year 1 to 45 in Year 5, so the same payroll can support more revenue and better gross profit if records per hour and QA pass rate stay strong.

Here’s the quick math: higher records per paid hour and less idle time mean more deliverable volume before headcount needs to rise. The risk is staffing ahead of demand, which pushes payroll up before billable work fills the schedule and cuts the owner’s draw.

Track Paid Hours, Not Just Output

Measure paid operator hours, billable hours, records per hour, idle time, and QA pass rate each week. Use training, workflow templates, batching, software, and clear intake rules to lift throughput and reduce rework. One clean rule: if a task cannot be billed or checked fast, it needs a tighter process.

Billable hours per customer: 25 to 45

Track idle time: paid but not billed

Watch QA: rework cuts margin

Hire after demand: not before it

Pricing and service mix

Pricing and service mix

This driver is the mix of basic entry, advanced processing, custom integration, and historical digitization, each with different labor, QA, and software load. In Year 1, monthly prices run from $450 for Basic Data Entry to $2,800 for Custom Integration and Reporting; by Year 5, that range rises to $550 to $3,400. More advanced work can lift owner income if delivery cost stays tight.

The margin risk is scope creep. Scope clarity, turnaround time, data complexity, and QA requirements decide whether a higher invoice turns into real profit. If a higher-priced job also needs more review or fix work, cash flow tightens and owner pay shrinks. One clean rule: price the effort, not just the file count.

Price by effort, not by task

Track revenue by service line, hours per job, QA hours, and rework rate before you renew or discount anything. The key test is gross margin by package, not blended revenue. If advanced projects pay more but need twice the review time, they may look good on sales and still hurt take-home.

Separate basic, advanced, and custom work.

Quote rush and complex jobs higher.

Measure fix time on every project.

Review margin by client each month.

For forecasting, split sales into basic versus advanced mix and update it monthly. A higher share of custom integration and historical digitization can raise revenue per client, but only if paid labor and QA do not rise faster than price. That spread is what protects owner income.

Client retention and sales pipeline

Client retention and sales pipeline

For a subscription data entry service, owner income is steadier when recurring clients renew and new sales replace churn with active monthly work. Track CAC, renewals, lost clients, sales cycle, and proposal hours. CAC is modeled at $550 in Year 1 and $420 in Year 5, while annual marketing spend rises from $60,000 to $350,000.

The main risk is paying for leads that never turn into monthly jobs. Sales commissions run 45% of revenue in Year 1 and 35% in Year 5, so weak retention can squeeze cash fast. If renewals slip, owner pay gets hit before the top line looks weak.

Track renewals before chasing more leads

Measure active monthly clients, renewal rate, lost clients, and proposal hours by offer type. A lead only helps if it becomes repeat work, because one-off digitization does not offset steady selling costs. Separate new business from renewal work so you can see which contracts build predictable revenue.

Use CAC against recurring revenue, not just booked revenue. If commissions stay at 45% of revenue and proposal hours keep climbing, qualify harder and cut weak-fit leads sooner. The goal is simple: more renewing accounts, less churn, and fewer hours spent replacing lost work.

Production labor cost

Production labor cost

Owner pay comes from the spread between client price and the labor needed to deliver the work. In this model, direct operator wages and benefits use 90% of revenue in Year 1 and 70% in Year 5, so early margin is thin and any underpriced manual review hits take-home fast.

Here’s the quick math: salaried data entry operators add $120,000 in Year 1 and $800,000 in Year 5, while QA specialists add $55,000 and $275,000. If labor grows faster than contract value, gross margin compresses and less cash is left for owner pay, taxes, and overhead.

How to protect margin

Track labor cost as a share of each tier, not just total payroll. Use client pricing, operator hours, subcontractor rates, supervisor time, and QA hours to test whether a job still pays enough after rework and review.

Price manual-heavy work separately and set limits on unbilled QA. If a contract needs more review than planned, raise the rate or cut scope fast. The goal is simple: keep delivered labor below what the customer pays so owner cash stays positive.