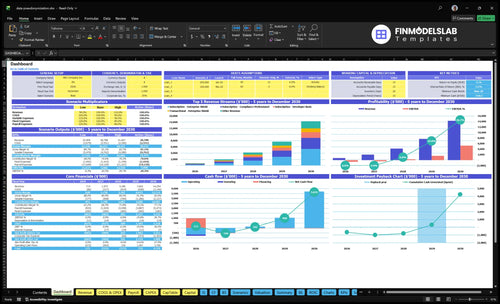

Data Pseudonymization Owner Income: $713k To $143M Revenue

A data pseudonymization service owner may have little to no distributable income in the first two years under these assumptions Revenue grows from $713k in Year 1 to $14254M in Year 5, while contribution margin improves from 800% to 855% after cloud, support, marketplace, and referral costs After listed payroll, marketing, and fixed overhead, the pre-tax owner income pool is about negative $592k in Year 1, negative $220k in Year 2, $731k in Year 3, $2324M in Year 4, and $6495M in Year 5, before reserves, taxes, debt service, and reinvestment

Owner income($592k) to $6.5mNet margin-93% to 37%Revenue for target pay$2.9mBusiness difficultyHard

Want to test your owner draw?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to stress-test owner income in the Data Pseudonymization Service model?

How much revenue does a data pseudonymization service need to pay the owner?

For the Data Pseudonymization Service, the Year 3 owner-pay target needs about $3.54M in annual revenue before reserves and taxes, assuming an 82.5% contribution margin. Here’s the quick math: ($1.99M payroll + $282k fixed overhead + $450k marketing + $195k owner pay) ÷ 82.5% = $3.54M. If the owner replaces the CTO role, payroll drops, so the revenue target falls too.

Cost stack

$1.99M payroll

$282k fixed overhead

$450k marketing

$195k owner pay

Revenue math

82.5% contribution margin

Divide costs by margin

Add reserves and taxes

CTO swap changes the total

How much can the owner of a data pseudonymization service make?

The owner of a Data Pseudonymization Service should expect low or negative take-home in Years 1–2, because the model shows -$592k in Year 1 and -$220k in Year 2 before taxes and reserves; see What Are The Operating Costs For Data Pseudonymization Service? for the cost side. Profit turns meaningful once recurring revenue covers payroll and security overhead, reaching $731k in Year 3, $2.324M in Year 4, and $6.495M in Year 5.

Owner take-home

Year 1: negative $592k

Year 2: negative $220k

Year 3: positive $731k

Owner pay must be separate from profit

Profit drivers

Build recurring subscription revenue

Fund payroll before owner distributions

Cover security and compliance costs

Run as a team-led service

Is a data pseudonymization service more profitable as consulting or managed service?

For a Data Pseudonymization Service, managed service is usually more profitable for predictable owner income because monthly retainers, setup fees, and usage charges repeat. Consulting can still pay well upfront, with enterprise setup fees often at $1,500 or even $10,000, but that cash is less steady. The best fit is usually hybrid pricing: retainers, implementation fees, and usage-based transaction revenue. One line: steady cash wins, but only if utilization and support stay under control.

Managed service wins on stability

Monthly revenue is easier to plan.

Retainers smooth owner cash flow.

Usage fees add upside.

Support costs must stay controlled.

Consulting pays faster, then fades

Setup fees can hit $1,500 to $10,000.

Revenue is less steady than retainers.

Enterprise sales cycles slow cash.

Hiring speed shapes scale and margin.

Data Pseudonymization Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see the six income drivers?

1

Recurring Retainers

$713K-$14.3M

Subscriptions lift revenue from $713K in Year 1 to $14.254M in Year 5, and the higher Enterprise Shield mix makes owner income more durable.

2

Sales Efficiency

8%-12%

Marketing budget scales from $120K to $1.2M, and trial-to-paid rising from 8% to 12% keeps that spend from leaking out.

3

Implementation Scope

$1.5K-$10K

One-time fees of $1.5K on Compliance Professional and $10K on Enterprise Shield add upfront cash and shorten payback.

4

Delivery Automation

80%-86%

Automated pseudonymization keeps variable cost low, so contribution margin (revenue after variable costs) stays near 80% to 85.5% as volume rises.

5

Labor Utilization

$760K-$4.21M

Payroll climbs from $760K to $4.21M, so how well the team stays busy decides how much growth turns into EBITDA.

6

Compliance Overhead

$23.5K/mo

Fixed overhead runs about $23.5K a month, and that cost load helps drive the minimum cash trough of negative $530K in Month 29.

Data Pseudonymization Service Core Six Income Drivers

Recurring Retainer Revenue

Recurring Retainer Revenue

Retainers are the cash base of a data pseudonymization service because they pay for monitoring, support, workflow maintenance, and compliance updates every month. In Year 1, pricing of $499 to $4,999 per month creates predictable MRR; by Year 5, $599 to $5,999 pushes average account value higher as the enterprise mix rises from 100% to 300%.

This income driver depends on active clients, monthly price, renewal rate, and support load. Churn is the risk: when accounts leave, cash gets less predictable, capacity planning gets harder, and owner reserves need to be larger to cover payroll, cloud costs, and compliance work.

Track Renewal Math Closely

Measure monthly recurring revenue by tier, renewal rate, and support hours per account. Here’s the quick math: more retained accounts at $599 to $5,999 a month raises cash flow without adding one-off sales pressure, but only if service time stays controlled. If support or compliance updates creep up, margin falls and owner pay gets squeezed.

Track churn by account tier.

Watch support hours per client.

Review enterprise mix monthly.

Forecast cash with renewals only.

1

Implementation Scope And Project Pricing

Implementation Scope Pricing

Scope drives cash and margin here. Setup fees run at $0, $1,500, and $10,000 by tier, and the price should track data sources, record volume, integrations, tokenization rules, testing, documentation, and compliance needs. Bigger projects can fund onboarding and security work, but they also consume senior engineer time, so owner income only rises if scope stays tight.

Here’s the quick math: a higher setup fee improves near-term cash flow and helps cover non-billable work, but long acceptance-testing cycles delay collection and can push payroll and cloud costs ahead of revenue. If the project needs multiple systems, custom rules, or heavy compliance review, the risk is lower gross margin and slower owner pay.

Price by scope, not by hope

Track three inputs on every deal: source count, record volume, and integration count. Then add separate line items for testing, documentation, and compliance review so the setup fee matches the actual delivery hours. The clean rule is simple: if scope grows, price must grow too.

Watch for margin leaks when enterprise deals look large but drag out. A $10,000 setup can still lose money if senior staff are stuck in rework or delayed sign-off. Build acceptance criteria before kickoff, define tokenization rules up front, and forecast owner cash around milestone billing, not just contract value.

2

Delivery Automation And Reusable Workflows

Reusable Workflow Automation

Reusable connectors, scripts, QA checklists, and data-mapping workflows cut delivery hours per client. That lifts margin because source costs improve from 200% of revenue in Year 1 to 145% of revenue in Year 5 after cloud, support, marketplace, and referral costs.

Here’s the quick math: $1.00 of revenue still carries $1.45 of source cost in Year 5, so this driver helps, but it doesn’t make delivery cheap. Founder time gets freed for sales and renewals, yet security review and client support still stay in the cost base.

Measure Hours Per Source

Track hours per client source, rework, and support tickets, plus client count, record volume, integrations, and QA cycles. Those inputs show whether automation is really cutting labor or just moving work into fixes.

Standardize the steps that repeat most, then reuse them by source type. If onboarding saves 4 hours but rework adds 1 hour, only 3 hours hit profit and cash flow; that’s the number that helps owner pay.

3

Privacy Engineering Labor Costs

Privacy Engineering Payroll

Privacy engineering labor is the main scale constraint because the work needs senior people who are costly and hard to replace. In the model, payroll rises from $760k annualized in Year 1 to $4,210M in Year 5, with $165k senior security engineers, $140k sales leads, and $125k specialists. As headcount grows, labor can outrun subscription revenue if delivery time is not tightly managed.

The key input is billable delivery time versus sales, management, and support time. If a senior engineer spends hours on demos, hiring, or client calls, gross margin falls and owner cash flow gets tighter. This driver affects how fast the business can scale, how much profit stays after payroll, and whether there is room for owner pay.

Headcount by role

Billable hours per week

Sales, support, admin split

Fully loaded pay per seat

Protect Billable Hours

Track billable hours, role mix, and utilization every week. Separate delivery labor from sales and admin so the real cost per client stays visible. Use the payroll model to forecast how many $165k engineers and $125k specialists the current pipeline can support before margin slips. If hiring runs ahead of booked work, cash burn rises before revenue catches up.

Set a simple rule: only add delivery headcount when paid work is already covering most of that seat. Keep scope tight, reuse playbooks, and push non-client work out of billable time. That protects gross margin and makes owner draws less volatile, because payroll growth then follows contracted revenue instead of hopes.

4

Infrastructure, Security, And Compliance Overhead

Security Overhead

Infrastructure, security, and compliance overhead is the fixed cost of running a safe pseudonymization platform. The base load is $235k per month, or $2.82M per year, before any variable cloud processing spikes. That level of overhead directly cuts free cash flow, so owner pay depends on keeping monthly recurring revenue above this floor.

Here’s the quick math: the monthly base includes $45k for certification maintenance, $22k for cybersecurity insurance, $35k for engineering tools, and $5k for legal counsel. The launch-period capital spend adds $140k upfront. What this estimate hides is the extra cost of secure environments, monitoring, and audit readiness when customer volume rises.

Control the fixed security load

Track this as a fixed-cost per month number, then split it by client count and data volume so you can see the true cost of each account. If one new enterprise client does not cover its share of compliance work and security tooling, it lowers margin even if revenue looks strong.

To improve owner income, test pricing against the full overhead stack: cloud processing, secure environments, monitoring, access controls, audit prep, insurance, legal review, and vendor tools. Keep a tight log of certification renewals and security reviews, because delays or control gaps can push costs above the $235k monthly base and delay profit draws.

5

Sales Efficiency, Retention, And Expansion

Sales Efficiency, Retention, And Expansion

This driver is about how much it costs to win a customer and how long that customer keeps paying. In the model, CAC falls from $1,500 in Year 1 to $1,100 in Year 5, a 26.7% drop. Lower acquisition cost helps owner income, but only if renewals and expansion keep cash coming after the first sale.

Here’s the catch: marketing spend rises from $120k to $12M, so scale can strain cash even when efficiency improves. The model also shows free-trial share rising from 120% to 180% and trial-to-paid conversion improving from 80% to 120%. If enterprise sales cycles run long, working capital can tighten before owner pay does.

Track Payback, Not Just Spend

Measure CAC, trial volume, trial-to-paid conversion, renewal rate, and expansion revenue by cohort. Here’s the quick math: a $400 CAC drop per customer only helps if payback improves as marketing scales. Tie each channel to cash collected in the first 90 to 180 days, not just lead counts.

CAC by channel

trial-to-paid conversion by cohort

renewal and expansion rate

marketing spend versus cash payback

sales cycle length in days

Watch enterprise timing closely. If renewals slip or account expansion starts late, cash gets stuck in long onboarding and approval loops, and that can delay owner draws. Set a minimum payback rule, then cut channels or trial steps that do not lift paid conversion or retention.

6

Data Pseudonymization Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income changes fast as trial conversion, pricing mix, and enterprise sales scale. Low, base, and high cases show how fixed payroll and support costs shape the pool.

A quick view of how owner income changes as revenue and margins scale.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is the lower earnings case, with Year 1 revenue at $713k and a negative pre-tax owner income pool.

This is the modeled middle case, using Year 3 revenue of $4.186M and a $731k owner income pool.

This is the stronger earnings case, with Year 5 revenue of $14.254M and a $6.495M owner income pool.

Typical setup

The model starts with about 80% contribution margin, $120k marketing, $760k annualized payroll, and $282k fixed overhead.

The model assumes about 82.5% contribution margin, steadier trial conversion, and a mix that still leans on the mid-tier plan while enterprise share rises.

The model assumes about 85.5% contribution margin, more enterprise mix, higher prices, and enough scale to spread fixed payroll and compliance costs.

Cost drivers

Trial conversion

developer mix

paid acquisition

fixed payroll

support overhead

Trial-to-paid conversion

plan mix shift

recurring subscription pricing

support and compliance payroll

fixed overhead

Enterprise mix

higher prices

trial conversion

support and compliance scale

fixed cost absorption

Owner income rangeBefore owner reserves

-$592kNegative pool

$731kModeled pool

$6.495MUpside pool

Best fit

Use this to stress-test a weak launch, slower conversion, and early fixed-cost drag.

Use this as the main planning case for budgeting, hiring, and cash timing.

Use this to test upside capacity when enterprise deals close faster and the client base scales cleanly.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution targets.

The owner may take little or nothing in the first two years under this model The pre-tax owner income pool is about negative $592k in Year 1 and negative $220k in Year 2, then rises to about $731k in Year 3 before taxes, reserves, debt service, and reinvestment

The model does not comfortably fund owner distributions until after the early ramp-up Minimum cash reaches negative $530k in Month 29, which means outside funding or deferred owner pay may be needed The business turns more attractive in Year 3, when revenue reaches $4186M and the pre-tax income pool is about $731k

The model treats security and compliance costs as core operating costs, not extras It includes $45k per month for certification maintenance, $22k for cybersecurity insurance, and $5k for legal and regulatory counsel Whether a specific certification is legally required depends on clients, contracts, and regulated data types

Retainer mix, labor, and security overhead move profitability the most Contribution margin improves from 800% to 855%, but payroll grows from $760k annualized to $4210M Enterprise mix also matters because higher-tier monthly pricing rises from $4,999 in Year 1 to $5,999 in Year 5

A hybrid model fits the assumptions best Monthly retainers create predictable revenue, setup fees add onboarding cash, and transaction pricing captures data volume The source model uses monthly prices from $499 to $5,999, setup fees from $0 to $10,000, and transaction charges from $001 to $0002 depending on tier

About the author

George Lawson

Small Business Advisor

George Lawson is a small business advisor at Financial Models Lab who focuses on startup cost planning for local business owners preparing to launch. He studies common expenses, revenue drivers, and launch requirements to help turn a business idea into a basic, workable plan. George also writes about pricing and profitability basics in a practical, plain-spoken way, with a focus on helping readers make smarter decisions before they open their doors.

Choosing a selection results in a full page refresh.