How Much Does a Day Spa Owner Make? $300k Year 1 EBITDA Case

Day Spa Bundle

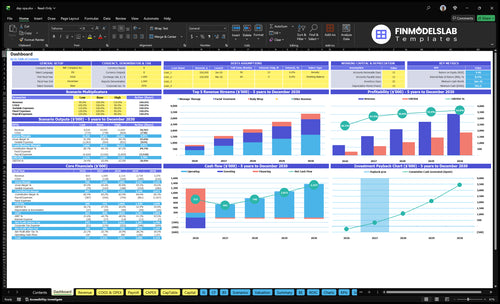

In this researched planning case, a day spa produces about $300k of Year 1 EBITDA on roughly $105 million of revenue EBITDA means operating profit before interest, taxes, depreciation, and amortization, so it is not the same as spendable owner income By Year 5, the model reaches about $339 million in revenue and $185 million in EBITDA, driven by 65 daily visits, 305 open days, and a $17075 blended visit value Actual owner pay depends on staffing, rent, debt, reserves, reinvestment, and how much work the owner personally covers

Owner income$300kNet margin28.5%Revenue for target pay$1.05MBusiness difficultyHard

Want to test your own spa owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. The output excludes personal taxes and one-time opening costs. Target pay gap equals owner income minus target owner pay.

Need to see the full Day Spa forecast and owner income?

For a Day Spa, the owner’s role changes cash fast: if the owner covers management, front desk, or services, the business keeps more cash. A semi-absentee setup lowers daily work, but it adds payroll, including a $75k spa manager from Month 1 and $335k in Year 1 wages. Here’s the quick math: scaling works better when visits rise from 25 to 65 per day, but less owner labor helps scalability more than short-term cash.

Owner-led cash

Owner covers key daily roles

Keeps payroll lower early

Protects short-term cash

Fits slower visit volumes

Staffed scale

$75k manager starts Month 1

$335k Year 1 wages add up

Less owner labor, more scale

Cash tightens before demand grows

How much revenue does a day spa need to pay the owner?

A Day Spa needs about $526k in annual revenue to support a $150k pre-tax owner-pay target. At $138 per visit and 305 operating days, that works out to about 13 visits per day. That pay still comes after payroll, rent, marketing, reserves, and other operating costs.

Revenue target

$526k annual revenue target

$150k pre-tax owner pay

$138 average revenue per visit

305 selling days used

Daily run rate

About 13 visits per day

Pay comes after fixed costs

Keep payroll and rent in check

Build reserves before owner draw

How much can a day spa owner make?

A Day Spa owner can make about $300k in modeled EBITDA in Year 1 and $1.85M by Year 5, but that’s operating profit, not guaranteed salary; for the core driver, see What Is The Most Important Metric To Measure The Success Of Your Day Spa?. Owner take-home comes after reserves, debt, taxes, and reinvestment.

Model upside

Year 1 revenue: $1.05M

Year 1 EBITDA: $300k

Year 5 revenue: $3.39M

Year 5 EBITDA: $1.85M

What drives it

Target 65 daily visits

Reach $170.75 blended revenue per visit

Build repeat-client bookings

Control payroll, rooms, and overhead

Day Spa Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What drives day spa owner income most?

1

Treatment Utilization

25-65/day

More visits spread fixed costs and lift owner income fast; the model scales from 25 to 65 visits a day.

2

Ticket Mix

$138-$171

A higher service mix and add-on spend move revenue per visit up fast, so each booking pays more.

3

Labor Margin

23%-32%

Staff pay starts at $335K in Year 1, so keeping booked hours high protects margin as volume rises.

4

Repeat Bookings

High

Repeat visits keep the schedule full without extra ad spend, which supports the jump to 35 to 65 daily visits.

5

Retail Add-ons

$25-$37

Add-ons and retail rise from $25 to $37 per visit, and that flows through with low product cost.

6

Cash Reserve

$256K

About $256K in annual fixed overhead and a $562K minimum cash need decide how long the spa can keep building profit.

Day Spa Core Six Income Drivers

Treatment-Room Utilization

Treatment-Room Utilization

Utilization sets the revenue ceiling. Here, Year 1 assumes 25 visits per day across 305 operating days, or 7,625 visits; Year 5 rises to 65 visits per day, or 19,825 visits. At the Year 1 math, each missed visit is about $138 in lost revenue before costs, so empty rooms hit owner pay fast.

Do not treat an open room as an earning room. What matters is booked treatment time, plus no-shows, provider gaps, room turns, and peak-hour demand. If prime-time slots stay thin, revenue stalls even when the spa looks busy, and fixed costs like rent and wages take a bigger bite of profit.

Track booked hours, not open hours

Measure utilization by room and by provider hour, then compare it with available hours. Track booked hours, no-show rate, provider gaps, room turns, and prime-time demand. That shows whether growth is real or just more hours on the calendar.

Use that data to protect the highest-value slots first. Fill late afternoons, weekends, and short-gap openings with the right service length, and keep the schedule tight enough that each room turn creates another paid visit instead of dead time.

Booked hours by room

No-shows by time slot

Provider gaps between visits

Room turn minutes

Prime-time demand by day

1

Average Ticket And Service Mix

Average Ticket and Service Mix

When your visit mix shifts toward higher-priced services, revenue per visit rises fast. In Year 1, the blended service ticket is $113, based on 50% massage at $110, 35% facials at $125, and 15% body wraps at $95. Add-ons and retail add $25 per visit, so total revenue is $138 per visit before costs.

That matters because higher ticket can lift owner pay, but only if supplies, provider wages, and service time stay under control. The model says Year 5 rises to $17075 per visit, but the real test is margin per hour, not just price. Upsells help more than discounts when they raise basket size without adding much labor.

Track Mix, Then Price to Margin

Measure the share of massage, facial, and body wrap visits, plus add-on rate, retail dollars per visit, and average service time. Use those inputs to test whether a higher-ticket service actually earns more after product cost and provider pay. One clean rule: if a service fills the schedule but cuts margin, it hurts owner income.

Track revenue per visit, gross margin, and provider minutes per dollar earned. Also watch how often staff sell extras without discounting the core service. Good upsells should raise cash in the door and leave enough after labor and supplies to support rent, reserves, and owner draw.

Service mix by visit type

Add-on dollars per guest

Retail attach rate

Time per service

Margin per booked hour

2

Provider Productivity And Labor Margin

Provider Productivity

Labor margin is what’s left after provider pay and commissions. In Year 1, wages total $335k for the manager, lead therapist, two massage therapists, esthetician, receptionist, and marketing coordinator, and commissions add 70% of revenue. The key inputs are revenue per provider hour and booked visits per provider; if those stay low, owner take-home gets squeezed fast.

This is the main swing factor between a full calendar and real profit. Adding staff before demand creates idle payroll, while tighter scheduling lifts EBITDA because the same labor base supports more paid visits.

Track Labor Margin Weekly

Track each provider’s booked hours, visits, and revenue per hour against the $335k wage base. Split out commissions so you can see true labor cost, not just salary. If output per staffed hour is weak, cut open shifts, cross-train staff, or delay hiring until demand fills the calendar.

One clean rule: pay for booked work, not empty chairs. When booking density rises, labor margin improves and more cash can flow to owner pay instead of payroll.

3

Repeat Bookings And Memberships

Repeat Bookings and Memberships

For a day spa, repeat clients keep the schedule full and cut the need for paid marketing. The model’s visit count rises from 25 average daily visits in Year 1 to 65 by Year 5, so the business needs a steady stream of rebooked guests to fill that gap. One more repeat visit is not just revenue; it also improves room use and makes staffing more predictable.

Packages and memberships can smooth cash flow if the price covers provider time, product use, and any perks. The risk is discounting too hard: prepaid sales may look good in cash, but if the package price is below true service cost, gross margin drops and owner pay gets squeezed. Watch rebooking rate, visit frequency, prepaid liability, redemption timing, and client churn.

Price for the repeat, not the one-off

Here’s the quick math: if members come back more often, you spend less to fill the calendar and spread fixed labor across more visits. The owner wins when repeat visits lift booked hours without adding idle payroll. A strong membership should support steady capacity use, not just create cheaper visits.

Track a few inputs every month: rebook rate, average visits per client, package redemption speed, and churn by service type. If redemptions bunch up in one month, cash flow can look strong while labor gets tight later. If a package discount does not cover service cost, stop it fast.

Measure rebook rate after each visit

Price above labor and product cost

Watch prepaid liability by package

Test churn by client cohort

4

Retail, Upgrades, And Add-On Sales

Retail, Upgrades, And Add-On Sales

Add-on and retail sales are the easiest way to raise revenue per guest without adding rooms. At 7,625 visits and $25 per visit, Year 1 add-on and retail revenue is about $190,625; at $37 per visit and 19,825 visits, it reaches about $733,525. One clean line: more ticket, same room count.

This driver includes upgrades, retail products, attachment rate, average add-on dollars, product turns, shrink, and staff recommendations. Retail is not pure profit because COGS starts at 30%, so every $100 sold leaves about $70 before shrink and selling labor. If attachment slips, owner pay falls even when traffic holds.

What to track and test

Measure it by provider and by service. Track attachment rate, average add-on dollars, retail units per visit, product turns, and shrink. Here’s the quick math: with 30% COGS, a $100 retail sale leaves $70 gross profit before labor and waste. If recommendations rise but ticket does not, the script is weak.

Track attachment by therapist

Watch average add-on dollars

Review units sold per visit

Check product turns monthly

Flag shrink and spoilage fast

Train staff to offer one upgrade and one home-care item on each visit, then test price and bundle mix. The goal is a higher ticket without more rooms, but not at the cost of dead inventory. If product turns slow or shrink rises, cash gets tied up and owner draws get tighter.

5

Fixed Overhead, Rent, And Reserves

Fixed Overhead And Reserves

Fixed overhead cuts distributable income even when bookings look strong, because these costs hit every month whether rooms are full or not. Here, monthly fixed costs total $213k, so owner pay only comes after that layer is covered. With $250k build-out and a $562k minimum cash need in Month 6, the business has to protect cash, not just chase sales.

Track monthly fixed costs, cash balance, and reserve runway in separate lines. If owner draws come out of working capital, the spa can look profitable on paper but still run short on cash. One clean rule: profit is not pay until reserves are funded.

Protect Cash Before Draws

Use a monthly cash plan built around the $213k overhead base and the reserve target for Month 6. Keep rent, utilities, cleaning, payroll support, software, and insurance under review, since each fixed dollar lowers owner take-home income. The inputs that matter most are fixed cost total, monthly bookings, gross margin, and the cash reserve floor.

Track fixed cost per month.

Separate reserves from profit.

Delay owner pay if cash is tight.

Test overhead before adding staff.

At this cost level, a strong sales month still does not mean free cash. If overhead rises faster than booked visits, working capital gets squeezed and the owner’s draw should stay low until the reserve gap closes.

6

Day Spa Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high day spa income scenarios

Owner income scenarios

Lower visits, weaker retail attach, and more idle payroll push owner income down; higher throughput and stronger add-on sales lift it.

Compare downside, base, and upside income paths for a day spa.

Scenario

Low CaseDownside case

Base CasePlan case

High CaseUpside case

Launch model

This is the lower earnings path when traffic and retail attachment run below plan.

This is the modeled middle case with 25 daily visits and the Year 1 pricing mix.

This is the stronger earnings path when demand, pricing, and throughput all move up.

Typical setup

Visits fall below 25 a day, add-on and retail sales soften, and payroll stays ahead of demand, so owner distributions stay thin.

At 25 visits a day and 305 operating days, average revenue is $138 per visit, Year 1 revenue is about $1.05M, EBITDA is about $300k, breakeven lands in Month 4, and payback is 19 months.

At 65 daily visits and 305 operating days, revenue per visit reaches about $170.75, annual revenue is about $3.39M, and EBITDA is about $1.85M, with enough scale to cover rent, marketing, reserves, payroll, and the owner role.

Cost drivers

Fewer visits

weaker retail attach

idle payroll

fixed rent load

marketing spend

25 daily visits

$138 per visit

305 open days

$300k EBITDA

Month 4 breakeven

65 daily visits

higher ticket

stronger retail attach

leaner idle payroll

reserve funding

Owner income rangeBefore owner reserves

Under $300k EBITDAThin draw

Around $300k EBITDAModeled draw

Near $1.85M EBITDAStrong draw

Best fit

Use this to stress-test the business if demand starts slowly or staffing is too heavy.

Use this as the core operating plan and the cleanest lender-style baseline.

Use this to test upside, hiring pace, and cash capacity once the spa is running at scale.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution targets.

This planning case shows about $300k of Year 1 EBITDA on $105 million of revenue By Year 5, EBITDA reaches about $185 million on $339 million of revenue That is business operating profit before personal taxes, debt service, reserves, reinvestment, and owner distributions

The model reaches breakeven in Month 4 and payback in 19 months That assumes 25 average daily visits in Year 1, 305 operating days, and a $138 blended visit value If bookings ramp slower or payroll starts too early, breakeven can move out fast

Not always, but this model includes one full-time spa manager at $75k per year from launch Removing or delaying that role can raise short-term owner cash if the owner can manage operations The tradeoff is time, consistency, and whether the owner can still grow bookings

Booked visits, average ticket, payroll, rent, and reserves drive owner salary most In Year 1, the model uses 25 daily visits, $138 revenue per visit, $335k of wages, and $213k of monthly fixed overhead Small changes in utilization or labor timing can move owner take-home materially

Fill more appointment slots before adding fixed cost The model grows from 25 to 65 daily visits over five years, while revenue per visit rises from $138 to $17075 The cleanest profit gains come from repeat bookings, higher add-on sales, tight staff schedules, and rent discipline

About the author

Christopher Ward

Practical Finance Writer

Christopher Ward is a practical finance writer at Financial Models Lab, where he focuses on cost-to-open estimates that help readers avoid common launch mistakes. He breaks down business plans into clear, usable language for non-finance readers, with a focus on monthly expense breakdowns and the practical decisions that matter before launch. His work is aimed at people weighing whether a business idea truly makes sense.

Choosing a selection results in a full page refresh.