How Much Does A Decoy Duck Carving Artisan Make: $72K Year 1 Sales

Key Takeaways

Pricing lifts revenue fastest, but demand sets the ceiling.

Owner labor caps volume more than demand does.

Direct orders keep more cash than fee-heavy channels.

Fixed overhead and reserves can shrink take-home cash.

Owner income$26.7kNet margin-80.6% to 38.4%Revenue for target pay$72kBusiness difficultyHard

Want to test your own decoy carving income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed salary, tax advice, or owner distribution advice.

Want cleaner owner-income projections for Decoy Duck Carving Artisan?

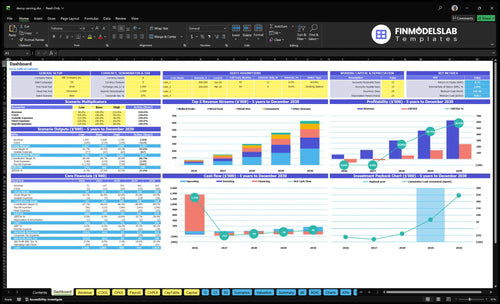

This dashboard shows revenue, assumptions, pricing, capacity, costs, payroll, reserves, and owner income; charts run from $72,000 in Year 1 to $627,200 in Year 5, with 956% Year 1 gross margin after direct materials; open the Decoy Duck Carving Artisan Financial Model Template.

Owner-income model highlights

Assumptions and pricing inputs

Capacity, costs, payroll

Base, low, high cases

How many duck decoys do I need to sell to pay myself?

If you want $70,000 in owner pay from Decoy Duck Carving Artisan, you need about 266 decoys a year, or 22 a month. The Year 1 plan sells 160 decoys, so it only supports about $26,748 before reserves, not a full owner salary.

Owner pay math

$450 price per decoy

266 units for $70,000

That equals 22 per month

Use owner pay, not salary

Year 1 reality

Plan sells only 160 decoys

Fixed overhead is $24,840

Apprentice labor is $13,500

Reserve cash still matters

How do you scale a duck decoy carving business?

Decoy Duck Carving Artisan scales by making more saleable pieces, raising price a bit, and adding trained help without hurting finish quality. Here’s the quick math: output climbs from 160 decoys in Year 1 to 1,280 in Year 5, while price moves from $450 to $490; that lifts annual sales from about $72,000 to $627,200. Owner take-home improves only if the extra labor from an apprentice, detail painter, and marketing help increases throughput more than it adds cost.

Scale math

160 units in Year 1

1,280 units in Year 5

$450 to $490 price range

About 8x unit growth

Team and margins

Add an apprentice for output

Use a detail painter for finish

Use marketing only if it sells more

Teaching stays secondary to take-home

Can you make a living carving duck decoys?

Yes, you can make a living as a Decoy Duck Carving Artisan, but the Year 1 model does not fund a $70,000 owner salary: owner-pay capacity is only $26,748 before reserves. The path in How Much To Start Decoy Duck Carving Artisan Business? reaches about $74,790 before reserves in Year 2, but only at 320 decoys, a $460 average price, repeat buyers, and production near 26 decoys per month.

Income math

Year 1 owner pay: $26,748

Year 2 owner pay: $74,790

Year 2 output: 320 decoys

Average price: $460

Viability checks

Target output: 26 decoys/month

Modeled revenue: $147,200

Owner salary goal: $70,000

Keep rework low

Decoy Duck Carving Artisan Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see what changes decoy carver income most?

1

Production Capacity

160-1.28K

Output jumps from 160 decoys in Year 1 to 1,280 in Year 5, so throughput drives the biggest revenue swing.

2

Price Mix

$450-$490

The same decoy line sells from $450 to $490, so a heavier mix of higher-priced orders lifts cash per piece.

3

Custom Demand

72K-627K

Stronger reputation helps win custom orders, and modeled revenue climbs from $72K in Year 1 to $627K in Year 5.

4

Channel Costs

5.2%-3.8%

Shipping, ads, and payment fees run from 5.2% of revenue down to 3.8%, so cleaner channels keep more margin.

5

Material Cost

$19.80-$10.80

Direct materials fall from about $19.80 to $10.80 per decoy, so waste control and supplier pricing protect profit.

6

Overhead Reserve

$24.84K

Fixed overhead is $24.84K a year, so cash stays tight until volume clears the shop's fixed load.

Decoy Duck Carving Artisan Core Six Income Drivers

Pricing And Product Mix

Pricing and Product Mix

Price is the biggest lever here. Revenue is units times price, so moving from $450 to $490 at 1,280 decoys adds $51,200 a year before any added selling costs. The disclosed Year 1 material cost is only $1,980, so small price changes can move owner income fast if demand holds.

Product mix matters because not every decoy should carry the same price. Better craftsmanship, finish quality, species detail, and provenance can justify a higher tier for collectors and hunters. If price climbs ahead of proven demand, sell-through slows, cash gets stuck, and the owner’s draw falls even when the spreadsheet shows more revenue.

Track Price Realization

Test price by buyer segment, not by guess. Track average selling price, sell-through rate, and quote-to-order rate for custom buyers, collectors, and hunters. Raise price only on models with proof of demand, like repeat orders or short lead times. If the higher tier slows orders, keep a lower-priced line so cash keeps moving.

Use the premium line to protect margin. Put the best finish, signature work, and species detail on the highest-priced decoys, then keep simpler pieces for volume. At 1,280 units a year, each $1 of realized price adds $1,280 of revenue, so even small mix shifts change owner income fast.

Track price by model.

Watch discounting and returns.

Measure close rate by segment.

Keep a low-friction entry tier.

1

Production Capacity And Owner Labor

Monthly Decoy Output

When the owner can only make 13 decoys a month in Year 1 and must scale to 107 a month by Year 5, production becomes the main ceiling on income. That is a 8.2x jump in throughput, and every unit still has to be carved, painted, finished, photographed, packed, and shipped. If any step slows, revenue rises on paper but owner pay does not.

The key input is hours per decoy, plus rework rate and on-time ship rate. A small drop in quality can cut take-home fast through refunds, extra labor, and missed delivery dates. One clean line: more units only help if the maker can keep quality steady.

Protect Maker Hours

Track output by stage so you know where time goes. Measure carve time, paint and finish time, photo time, and pack and ship time for each decoy. That shows whether growth is blocked by art work, admin work, or shipping work, and it helps you price and plan around the real labor cost.

Log hours per decoy.

Count reworks each month.

Watch late shipments closely.

Cap backlog before quality slips.

If the owner is still doing every step alone, growth can strain cash flow because the business makes money only when finished units leave the shop. The fix is simple: forecast output from available maker hours, not from demand alone. That keeps owner draws tied to real capacity, not wishful volume.

2

Direct Cost And Gross Margin

Direct Cost per Decoy

Each decoy’s direct cost includes wood, glass eyes, paint, finishing oils, and abrasives. The model shows unit cost at $1,980 in Year 1 and $1,080 in Year 5. Against a $450 to $490 sale price, that means the direct cost line can wipe out gross profit before overhead or owner pay.

Keep packaging and shipping recovery in variable selling costs, not direct materials. That split shows whether the problem is carving efficiency or sales-channel cost. If the direct cost stays above the selling price, more units only burn more cash, even if the shop is busy.

Track Unit Cost Hard

Measure cost per finished decoy by model, not as one blended number. The source note says gross margin rises from 956% to about 978%, but that should be checked against the stated cost and price inputs before anyone uses it in a draw plan. Here’s the quick math: if cost is $1,980 and price is $450, gross profit is -$1,530 per unit.

Track wood, eyes, paint, oils.

Log scrap, rework, and waste.

Separate shipping and packaging recovery.

Test price before scaling volume.

If the Year 1 unit cost stays above selling price, cut waste, redesign the build, or raise price before adding volume. That’s what protects cash flow, fixed overhead coverage, and the owner’s ability to take money out of the business.

3

Sales Channel Economics

Channel Mix and Net Cash

Sales channel choice changes how much of each duck decoy sale reaches the owner. The model already takes 11% of Year 1 revenue for payment processing and 25% for shipping packaging, before booth fees, commissions, or travel. Direct custom orders usually keep more cash than commission-heavy channels.

Here’s the quick math: a higher sticker price does not help if the channel takes too much off the top. Net revenue is what pays the owner, so compare each channel by cash left after fees, not by orders booked. Shows can still work when higher prices and repeat buyers cover booth and travel costs.

Track Net per Channel

Measure net cash per decoy by channel: selling price minus payment processing, packaging, commissions, booth fees, and travel. If a channel can’t clear those costs, it is shrinking owner pay even when sales volume looks strong. Use separate tracking for direct custom orders, shows, and any commission-based outlet.

Log fees by channel.

Allocate booth costs per sale.

Test price lift against travel.

4

Reputation And Custom Demand

Custom Demand Premium

Custom commissions and collector demand can lift the average selling price or speed up sell-through. The model uses one annual average price, so the upside shows up when price moves from $450 to $490 or when backlog clears faster. At 1,280 decoys a year, that price step adds $51,200 of revenue before added costs. Do not count resale appreciation as operating income.

The premium depends on a recognizable carving style, accurate species detail, clean finish, signature, reviews, and repeat buyers. That matters because owner income rises only if the market pays more for the piece or buys it sooner. If custom work stretches lead times, cash flow can improve or stall depending on how well deposits and delivery timing are handled.

Track Price, Backlog, and Repeat Buyers

Track custom order share, repeat buyers, average selling price, and weeks of backlog. Here’s the quick math: if reputation lifts price by $40 per decoy, every 100 units adds $4,000 of revenue before fees and labor. If demand is stronger but the finish slips, the premium can vanish fast.

Use a simple monthly scorecard: quote rate, close rate, delivery time, and buyer reviews. Keep the species detail and finish consistent, because that is what supports the premium. Faster sell-through helps cash come in sooner, while weak reviews push buyers back to the $450 level.

Log repeat buyer rate.

Track weeks of backlog.

Test small price increases.

Protect finish quality every order.

5

Overhead, Reserves, And Reinvestment

Fixed overhead trims cash

Even if the decoy itself looks highly profitable, $2,070 per month in fixed shop overhead still hits cash before owner pay. That is $24,840 per year for workshop rent, utilities, insurance, internet, phone, software, professional fees, and property taxes.

The real input is cash left after those bills, not gross margin alone. If sales slow, the overhead does not slow with them, so owner-income projections can overstate what can safely be drawn.

Fund reserves before owner draw

Build a reserve for tool replacement, inventory, photography, travel, and slow months. Here’s the quick math: if fixed overhead stays at $24,840 per year, every dollar not reserved is a dollar that can disappear when a bill hits or orders dip.

Track overhead paid each month

Ring-fence reserve cash

Review owner draw after reserves

Measure reserve funding as a separate line, not as leftover cash. If you skip it, the spreadsheet can show healthy profit while the bank balance cannot support reinvestment or a stable draw.

6

Decoy Duck Carving Artisan Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high decoy carving income scenarios

Owner income scenarios

Owner income moves with unit volume, price, and staffing load. Early years are thin because fixed overhead and labor sit ahead of sales; the later model only works if production scales cleanly.

Compare conservative, expected, and scaled owner income paths.

Scenario

Low CaseDownside case

Base CaseMiddle case

High CaseUpside case

Launch model

This is the lower earnings path, built from Year 1 output and pricing.

This is the modeled middle path, built from Year 2 scale.

This is the stronger earnings path, built from Year 5 scale.

Typical setup

About 160 decoys at $450 each drives $72,000 of revenue, with $24,840 fixed overhead and about $26,748 of owner-pay capacity before reserves.

About 320 decoys at $460 each drives $147,200 of revenue and about $74,790 of owner-pay capacity before reserves.

About 1,280 decoys at $490 each drives $627,200 of revenue and about $429,702 of owner-pay capacity before reserves, but staffing and execution get hard.

Cost drivers

160 decoys

$450 price

$72,000 revenue

$24,840 fixed overhead

starter staffing

320 decoys

$460 price

higher output

moderate labor

steady overhead

1,280 decoys

$490 price

high output

heavier staffing

execution risk

Owner income rangeBefore owner reserves

$26,748Conservative income

$74,790Model year 2

$429,702Scaled income

Best fit

Use this to test slow sales, thin cash, and a small shop setup.

Use this as the main planning case for steady demand and normal execution.

Use this to test what happens if production, hiring, and sales all work cleanly.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

A part-time decoy carver’s income depends on output and overhead In the researched Year 1 case, 160 decoys at $450 create $72,000 revenue and about $26,748 owner-pay capacity before tax and reserves If your part-time setup avoids the $2,070 monthly shop overhead, take-home can improve, but only if quality and sales stay steady

The model shows limited owner-pay capacity in Year 1 and stronger capacity by Year 2 Year 1 supports about $26,748 before reserves, while Year 2 reaches about $74,790 before reserves at 320 decoys sold If the owner books a $70,000 master-carver salary in Year 1, the business shows a loss

You do not need custom orders, but they can help The model uses one average price per year, starting at $450 and rising to $490, across mallard drake, wood duck, pintail hen, canvasback, and greenwing teal decoys Custom demand matters because it can raise price, reduce unsold inventory, and stabilize backlog

Price and production volume usually move profit the most Year 1 sales are $72,000 from 160 decoys, while Year 5 sales reach $627,200 from 1,280 decoys Materials are modest at $1980 per decoy in Year 1, but fixed overhead, staffing, sales fees, and reserves decide how much cash reaches the owner

Start with target owner pay, real production capacity, and net cash per decoy In Year 1, a $450 decoy has about $1980 of direct materials and $2340 of variable selling costs, leaving about $40680 before fixed overhead and labor Premium pricing needs visible craftsmanship, clean finish, accurate species detail, and buyers who value the work

About the author

Marcus Cole

Business Operations Writer

Marcus Cole is a business operations writer for Financial Models Lab who researches how small businesses launch, operate, and earn money. He focuses on first-year business costs and simple business projections, helping local business owners move from a side project to a real business. His work guides readers from an idea to a basic business plan.

Choosing a selection results in a full page refresh.