How Much Demolition Owners Make: $150K Pay, No Extra Draw

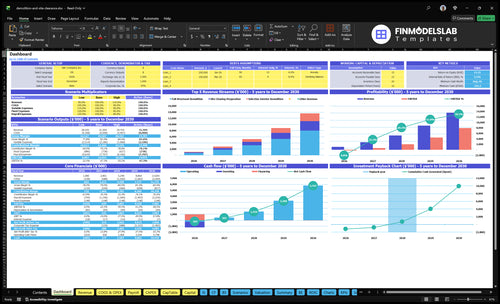

Under these researched assumptions, the demolition business owner can plan for a $150,000 annual operator salary, but not extra profit distributions in the modeled years Revenue rises from $180,000 in Year 1 to $230 million in Year 5, while job-level contribution margin improves from 701% to 768% Still, after listed payroll, fixed overhead, marketing, and variable job costs, operating profit remains negative, from about -$734,000 in Year 1 to about -$210,000 in Year 5 So the real answer is $150,000 of planned owner pay, funded by the model, with $0 modeled surplus owner draw before taxes

Owner income$150kNet margin70% to 77%Revenue for target pay$420k to $460kBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Demolition Service forecast?

Demolition Service margins are driven mostly by disposal fees, hauling distance, fuel, maintenance, labor productivity, job scope, permit burden, project insurance, bonding, and subcontractor pricing. If you’re pricing a job, start with How Much Does It Cost To Start The Demolition Service Business? because the same cost stack usually decides profit. In the model, disposal moves from 120% to 100% of revenue and fuel plus maintenance from 100% to 80%, and at $230 million revenue, every 1 point of cost is about $22,953 of owner cash.

Big cost drivers

Disposal fees hit margin fast.

Hauling distance pushes truck cost up.

Fuel and maintenance move with miles.

Labor productivity changes crew hours.

What to control

Job scope can widen fast.

Permit burden adds time and cost.

Insurance and bonding raise fixed overhead.

Higher prices help only with tight estimates.

Can an owner-operated demolition business make more money by scaling?

Yes—a Demolition Service can make more money by scaling, but only when each added crew, machine, and truck produces contribution above its full cost. The model can grow from $180,000 revenue to $230 million, but payroll also climbs from $687,500 to $172 million, so scaling without tight estimating and safety control can eat the upside. Owner-operated jobs can protect cash early; crew-led and multi-crew work add capacity only if utilization stays high.

Early stage

Owner-operated work protects cash.

One crew keeps payroll lower.

Simple jobs are easier to control.

Safety and pricing stay tight.

Scaling stage

More crews add capacity.

Insurance and equipment costs rise.

Estimating gets harder fast.

Profit grows only above full cost.

How much do demolition company owners take home?

In this Demolition Service model, owner take-home is $150,000 as CEO Operations Manager salary, with $0 extra owner draw because operating profit is negative after listed costs; for the growth constraint, see What Is The Biggest Challenge Facing Demolition Service Growth?. Treat take-home as cash after job costs, overhead, equipment obligations, reserves, and reinvestment, not project revenue.

Owner cash

Modeled salary: $150,000

Extra owner draw: $0

Operating profit: negative

Project revenue is not take-home

Year 5 math

Revenue: $230 million

Contribution margin: 768%

Payroll: $172 million

Excludes taxes and debt service

Demolition Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six owner-income drivers?

1

Project Volume

$180K-$230M

More jobs and a higher average ticket lift revenue fast, and the $25K-$110K marketing budget feeds the pipeline; revenue is not owner take-home until direct costs and overhead are covered.

2

Job Mix

701%-768%

Changing the mix between full demo, selective interior work, and site clearing moves margin fast because the scopes do not pay the same per crew hour.

3

Payroll

$687.5K-$172M

Payroll is the biggest swing cost, so better output per labor dollar is what keeps extra revenue from disappearing.

4

Disposal Costs

10%-12%

Lower tipping, haul, and fuel spend keep more of each project dollar after direct job costs.

5

Equipment Use

$545K

Keeping the excavator, trucks, and attachments busy spreads the $545K equipment base across more billable work and eases financing pressure.

6

Overhead

$147.6K

The $147.6K fixed overhead load hits every month, so lean admin and compliance protect owner cash.

Demolition Service Core Six Income Drivers

Project Volume And Average Ticket

Project Volume and Average Ticket

Completed jobs and average contract value set the revenue ceiling before costs. In this model, marketing spend divided by CAC drives customer growth from 10 acquired customers in Year 1 to 611 in Year 5, while revenue per acquired customer rises from about $18,000 to $37,560 as the mix shifts toward full structural demolition and site clearing.

That only helps if each job price covers labor, debris removal, equipment, insurance, bonding, and downtime. More volume with thin tickets can still leave the owner short on cash, because busy crews do not pay the bills if gross margin gets squeezed by low pricing or scope gaps.

Track ticket, not just wins

Track completed jobs, average ticket by job type, and CAC by channel. The key question is simple: does each acquired customer still cover the full job cost stack after labor, haul-off, fuel, insurance, bonding, and overhead? If not, more leads just scale losses.

Use a floor price for each scope. Full structural work can support a much larger ticket than selective work, so break out pricing by scope and test the mix monthly. One clean rule: if a job cannot clear direct costs and a fair share of fixed overhead, don’t book it just to keep the crew moving.

Track revenue per completed job

Compare CAC to contract value

Price by scope, not hope

Reject low-margin volume

1

Job Mix And Scope Control

Job Mix And Scope Control

Your income here depends on how much work is full structural demolition versus selective interior work, and how tightly each job is scoped. At $180/hour for 160 hours, a Year 1 full structural job bills $28,800; selective interior work at $120/hour for 40 hours bills $4,800. Bigger tickets only help if cleanup, access, salvage, permits, and change orders stay inside the bid.

The key inputs are job type, estimated labor hours, permit and cleanup scope, salvage credits, and change-order rate. A small scope miss on a large job can wipe out margin because labor and crew time keep running while billing stalls. If the scope is tight, the owner can turn higher-ticket projects into real take-home pay; if it drifts, revenue rises and cash still disappears.

Tighten the Scope Before You Price

Track every bid with the same scope sheet: demo type, labor hours, access limits, debris removal, salvage terms, permit duty, and excluded items. Then compare planned hours to actual hours and measure change orders as a share of contract value. That tells you which jobs are truly profitable, not just bigger on paper.

Protect margin by pricing scope risk up front. If a job needs hard access, cleanup, or permit work, build that into the quote instead of hoping it stays simple. The best jobs are not the biggest ones; they are the ones where scope stays fixed and the crew can finish without unpaid extras.

2

Labor Productivity And Crew Utilization

Labor Productivity

This driver covers crew size, billable time, overtime, rework, safety delays, and how well labor is matched to booked work. Payroll is the biggest pressure point here, rising from $687,500 in Year 1 to $172 million in Year 5. If crews are staffed before the backlog is real, gross margin drops and owner distributions can vanish even when revenue grows.

The owner’s income depends on keeping each crew busy on billable work and avoiding paid downtime. Safety is margin protection, not optional overhead: one shutdown, a bad sequence, or a rework loop cuts cash fast. The clean metric is billable hours per crew plus gross profit per job; both have to hold up before paying out profit.

Crew Utilization Control

Track labor by project, not just by pay period. Compare planned hours to actual hours each week, then flag overtime, idle time, and repeat fixes. If the schedule is thin, shrink the crew before payroll outruns booked jobs. That matters because labor waste hits margin twice: first in wages, then in slower job turnover.

Use a simple rule: every job must show expected crew hours, safety time, and rework allowance before it starts. Then review gross profit per job after completion and cut the work types that burn labor. If utilization slips, the fix is tighter scheduling and smaller crews, not hoping volume will cover it.

3

Disposal, Hauling, And Dump Fees

Disposal, Hauling, And Dump Fees

Disposal is not a small pass-through cost in demolition; it can decide whether a fixed-price bid makes money. In this model, material disposal fees run 120% of revenue in Year 1 and 100% in Year 5, so a bad dump estimate can wipe out owner pay fast. The key inputs are debris volume, material type, sorting, trucking distance, tipping fees, and recycling options.

Here’s the risk: if scope changes add more haul-off than the bid assumed, gross margin drops before labor or equipment even move. Quote with a disposal cushion, spell out exclusions for hidden debris and special materials, and tie change orders to actual truckloads so cash and profit stay aligned.

Price It By Load, Not Guesswork

Track tons, yards, truck trips, tipping fees, and haul miles on every job, then compare the estimate to actuals by project type. That shows which scopes are cash-positive and which need a higher rate or tighter exclusions. On $230 million revenue, even a small disposal miss can cut owner distributions hard, so build the cushion into every quote.

Use a standard dump-fee sheet, get written site conditions, and stop work if debris mix changes. One clean line helps: if you cannot measure the load, you cannot price the load.

4

Equipment Utilization And Financing

Equipment Utilization And Financing

For this demolition model, owned machines only pay off when jobs keep them busy enough to cover repairs, fuel, maintenance, depreciation, and loan payments. Listed gear totals $545,000 for a heavy excavator, skid steer loader, and demolition attachments. If equipment sits between projects, cash drains fast and owner pay gets squeezed even when revenue looks strong.

The key split is depreciation versus cash. Depreciation is an accounting cost; loan principal and interest hit cash each month. Also, fuel and maintenance are modeled at 100% of revenue in Year 1 and 80% in Year 5, so underused equipment can turn a good bid into weak take-home income.

Track Utilization Before You Add Debt

Measure each machine by billable hours, downtime, repair spend, and cash payments per job. If a machine is not helping projects finish faster or at lower cost, it is likely a cash drag. The owner should forecast monthly debt service and fuel against booked work, not hoped-for revenue.

Use separate lines for accounting depreciation, loan payments, and maintenance. That keeps owner draw honest. If fuel and maintenance are already absorbing 80% to 100% of revenue, any idle time or repair spike should trigger a pricing review or a rental-versus-own check before more equipment is financed.

5

Overhead, Insurance, Permits, And Compliance

Overhead, Insurance, Permits, And Compliance

Fixed overhead is $12,300 per month and base general liability insurance is $2,500 per month, so the business starts with $14,800 per month before payroll and marketing. That is $177,600 per year in baseline load. If booked work slips, owner pay gets squeezed fast because these costs do not wait for the next project.

Project-specific insurance and bonding add 30% of Year 1 revenue and 22% of Year 5 revenue. On every $100,000 of revenue, that is $30,000 early on and $22,000 later. Licenses, permits, safety programs, estimating time, and admin work protect the business from job-stopping risk, but they cut operating profit if they are not built into pricing.

Match Overhead To Booked Work

Track booked revenue, permit count, bonding cost, and estimator/admin hours by job. If a project needs heavy compliance time or extra bonding, price it as part of the contract, not as hidden overhead. One line matters here: overhead must match booked work.

Price permits and safety work upfront.

Track insurance as a percent of revenue.

Watch admin hours per bid.

Delay hires until work is booked.

If booked work falls below the fixed load, cash flow tightens and owner draw drops even when the schedule looks busy. The clean test is simple: can gross profit cover $14,800 per month before payroll and marketing, plus the project insurance and bonding load? If not, the bid is too thin.

6

Demolition Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high demolition owner-income cases

Owner income scenarios

Owner income shifts fast here because revenue, payroll, equipment, and fixed overhead move together, so each growth path still has a different funding gap.

Low, base, and high cases show how cash pressure changes as the demo business scales.

Scenario

Low CaseDownside

Base CaseBase

High CaseUpside

Launch model

This is the down-side case where early jobs stay small and payroll plus overhead eat most of the gross profit.

This is the modeled middle case with steadier job flow and a larger crew.

This is the stronger-growth case with much larger revenue and a bigger operating team.

Typical setup

Year 1 uses $180,000 revenue, a 701% contribution margin, $687,500 payroll, $147,600 overhead, $25,000 marketing, and $150,000 owner salary, which still leaves a large operating loss.

Year 3 lands at $802,500 revenue, a 734% contribution margin, about $1.29 million payroll, and $60,000 marketing, but operating profit after owner pay is still negative at about $912,000.

Year 5 reaches $230 million revenue, a 768% contribution margin, $172 million payroll, and $110,000 marketing, yet operating profit is still about negative $210,000.

Cost drivers

Early revenue

heavy payroll

fixed overhead

owner salary

marketing spend

Higher job volume

larger crew

marketing

payroll scale

fixed overhead

Revenue scale

payroll load

marketing

equipment use

project staffing

Owner income rangeBefore owner reserves

($734,000)Funding gap

($912,000)Funding gap

($210,000)Upside gap

Best fit

Use this to stress-test cash needs if launch volume stays low and payroll is front-loaded.

Use this as the core planning case for lender, cash, and hiring decisions.

Use this to test whether higher volume can finally absorb the labor and equipment base.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

This model supports a planned $150,000 CEO Operations Manager salary, but no extra owner distribution Revenue grows from $180,000 in Year 1 to $230 million in Year 5, and contribution margin improves from 701% to 768% Payroll and overhead still absorb the cash, so surplus owner draw is $0 in the modeled years

It does not break even within the five-year model under the listed assumptions Operating profit after the $150,000 owner salary is about -$734,000 in Year 1 and about -$210,000 in Year 5 The gap narrows as revenue reaches $230 million, but payroll, marketing, and overhead still exceed contribution profit

Not always, but this model assumes major owned equipment from the start Listed startup capex includes a $350,000 heavy excavator, $75,000 skid steer loader, and $120,000 in demolition attachments That is $545,000 before any debt payments Renting can reduce upfront cash, but may raise job-level costs if utilization is high

Payroll, job mix, and debris costs drive the biggest swings Payroll rises from $687,500 to $172 million across the model, while disposal runs 120% to 100% of revenue Fuel and maintenance add another 100% to 80% Small misses in estimating debris, labor hours, or equipment use can wipe out owner draw

Improve contribution per crew before adding more staff In Year 5, $230 million of revenue at a 768% contribution margin creates about $176 million before payroll, overhead, and marketing That still is not enough for surplus distributions The cleanest levers are tighter scope, higher utilization, controlled disposal, and slower hiring

About the author

Paul Wells

Practical Finance Writer

Paul Wells is a practical finance writer for Financial Models Lab who focuses on cost-to-open estimates and monthly expense breakdowns that help founders avoid common launch mistakes. He simplifies business plans for non-finance readers and brings a grounded, founder-minded perspective to startup cost research.

Choosing a selection results in a full page refresh.