How Much Does a Digital Entrepreneur Make? $100k Salary Case

Digital Entrepreneur Bundle

You’re estimating owner income for an online business, not a job salary or passive income promise In this five-year US planning model, the Founder/CEO salary is $100,000 per year, while operating profit after that salary moves from a -$166k Year 1 loss to about $163k in Year 2 before taxes, reserves, and distributions

Owner income$100kNet margin-13% to 4%Revenue for target pay$2.7MBusiness difficultyHard

Want to test your owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, reserves, and reinvestment, and this is not guaranteed salary, tax advice, or owner distribution advice.

Want to see owner income in the model?

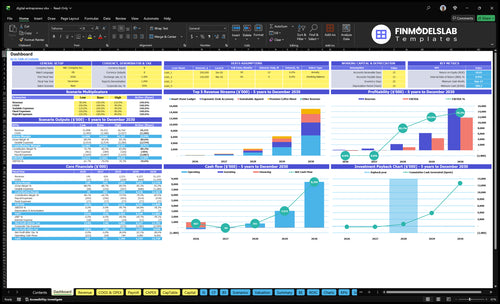

If you want owner income, the Digital Entrepreneur Financial Model Template shows revenue, margin, costs, reserves, and take-home assumptions. Revenue runs from $167k in Year 1 to $297M in Year 3, and salary-adjusted profit moves from -$166k to $182M.

Owner-income model highlights

Owner pay shifts with CAC

Revenue: $167k to $297M

Charts test CAC and repeat

How much revenue does a digital entrepreneur need to pay themselves?

For Digital Entrepreneur, desired owner pay is not the same as safe owner pay. This model includes a $100k Founder/CEO salary inside $768k fixed overhead and $1,775k Year 1 payroll, but $167k Year 1 revenue does not cover the cost base after marketing and variable costs. By Year 2, $769k revenue covers the $100k salary and leaves about $163k operating profit before tax and reserves.

Owner pay

$100k salary is built in

Year 1 revenue is $167k

Year 1 does not cover costs

Pay target is not safe cash

Safe cash

Year 2 revenue reaches $769k

Operating profit is about $163k

Hold cash for taxes first

Then fund inventory and reinvestment

What costs reduce digital entrepreneur income?

Digital Entrepreneur income drops fast when acquisition and labor rise, even if gross margin looks strong; see How Much Does It Cost To Open, Start, And Launch Your Digital Entrepreneur Business? for the startup-cost side. In Year 1, payment processing is 25%, with sourcing and manufacturing at 8%, fulfillment and packaging at 4%, and customer service and returns at 3%. Add $64k monthly fixed overhead, $50k marketing in Year 1, $120k in Year 2, and payroll rising from $1,775k to $2,825k, and CAC (customer acquisition cost), refunds, support, or contractors can wipe out owner income.

Main cost drains

25% goes to payment processing.

8% hits sourcing and manufacturing.

4% covers fulfillment and packaging.

3% goes to service and returns.

Profit squeeze points

$64k monthly overhead stays fixed.

Marketing jumps from $50k to $120k.

Payroll rises from $1,775k to $2,825k.

Refunds, support, and contractors can outrun revenue.

How much can a digital entrepreneur realistically make?

A What Is The Primary Goal Of Your Digital Entrepreneur Business? income can range from a funded $100k founder salary in Year 1 to about $163k profit in Year 2, but only if the model can carry early losses. Here’s the quick math: Year 1 needs cash to cover a -$166k operating loss plus $73k setup spend, while Year 2 reaches about $769k revenue before tax and reserves.

Realistic income

Year 1: $100k salary needs funding

Loss: -$166k operating gap

Setup: $73k before scaling

Year 2: $163k profit after salary

What drives upside

Year 3: $297M modeled revenue

Profit: $182M modeled upside

Watch: CAC and repeat orders

Improve: pricing, offer fit, execution

Digital Entrepreneur Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main income drivers?

1

Demand Scale

$50K-$600K

More marketing budget buys more traffic and sales, but cash still gets tight until repeat buyers and margin catch up.

2

Cost Load

175%-135%

Lower sourcing, fulfillment, processing, and service load leaves more of each sale as owner income.

3

Fixed Overhead

$64K/mo

A $64K monthly fixed base sets the break-even floor, so growth has to clear that before pay grows.

4

Repeat Rate

25%-55%

More repeat buyers stretch customer life and cut how often you have to buy the same revenue again.

5

Order Value

$6.5K-$10.2K

Higher order value lifts revenue per sale and helps fixed costs take a smaller bite.

6

Acquisition Cost

$35-$26

Lower acquisition cost shortens payback and protects cash while you scale.

Digital Entrepreneur Core Six Income Drivers

Audience Demand And Traffic Quality

Qualified Demand

Qualified demand sets the revenue ceiling. This model turns marketing spend into new customers, rising from 1,429 in Year 1 to 23,077 in Year 5, so traffic quality matters more than follower count. Here’s the quick math: 1,429 × $35 CAC ≈ $50k of spend in Year 1, and the plan only works if CAC falls to $26 as order volume climbs.

What this estimate hides is intent quality. If clicks come from low-intent traffic, spend rises faster than orders, gross profit shrinks, and owner draw gets tighter. The best signals are email engagement, search intent, and repeat purchase intent because they lift conversion without forcing CAC up.

Track Intent, Not Just Traffic

Measure the inputs that predict paid efficiency: CAC, new customers, order volume, email clicks, repeat orders, and source mix. If one channel brings cheap visits but weak orders, cut it fast. For this model, the goal is simple: more qualified customers at $26 CAC, not just more sessions.

Test channels against one line: does this traffic buy again? If a source does not lift repeat intent, it is probably hurting owner income. Track source-level CAC, first-order conversion, and 60- to 90-day repeat rate before scaling spend.

Track CAC by channel weekly

Favor high-intent search traffic

Use email to lift repeat orders

Cut low-converting click sources fast

1

Monetization Model

Revenue Mix

Revenue mix matters here because each offer carries a different margin and support load. A weighted unit price of $5,415 in Year 1 rising to $6,395 in Year 5, with units per order moving from 12 to 16, can lift revenue fast, but only if the mix is profitable after sourcing, shipping, and service. Not every audience will buy every offer, so the owner’s take-home income depends on fit as much as volume.

Products, subscriptions, services, sponsorships, affiliates, and licensing all need separate math. A product sale may add gross profit, while an affiliate or sponsorship may add cash with little fulfillment, but also lower control. If support time, refunds, or packing labor rise faster than basket size, the higher headline revenue won’t translate into more owner pay.

Measure Margin by Offer

Track each stream by gross margin, support minutes, and cash collected per order. Here’s the quick math: if one offer sells well but needs more service or returns, it can pay less than a smaller, cleaner order. The owner should watch unit margin, attach rate, and order mix each month, not just top-line revenue.

Test offers by audience before scaling. Use a simple rule: keep only the streams that improve cash flow after fulfillment, payment fees, and customer care. Separate the P&L by stream so products, subscriptions, and commissions do not blur together, and so forecasted owner draw is based on real contribution, not blended averages.

2

Conversion Rate And Pricing

Pricing and Conversion

Conversion rate is the share of visitors who buy, and average order value (AOV) is what each order brings in. In this model, AOV rises from 6498 in Year 1 to 10232 in Year 5, so small price or upsell gains can lift owner income fast. The catch: higher price only helps if payment fees, refunds, sourcing, and support costs stay controlled.

Here’s the quick math: revenue equals traffic × conversion × AOV. If conversion slips, the price lift can vanish; if AOV rises but refunds rise too, cash flow can still tighten. The estimate hides the service load behind premium pricing, especially when customers expect fast help and easy returns.

Test price before scaling

Track conversion rate, AOV, upsell take rate, refund rate, and support cost per order together. Test one change at a time: price, bundle, or checkout add-on. If AOV rises but refunds or payment fees rise faster, take-home drops. Price should improve gross margin, not just top-line sales.

Set a weekly scorecard: visitors, orders, AOV, refund dollars, and customer service minutes per order. That shows whether a higher price is really improving owner pay. If a product needs more hand-holding after a price increase, bake that labor into the margin test before you scale it.

3

Customer Acquisition Cost

Customer Acquisition Cost

CAC is what it costs to win one new customer, so it sets how much of each sale survives into profit and owner pay. This model spends $50k in Year 1 at $35 CAC, or about 1,429 new customers; Year 2 rises to $120k at $32 CAC for 3,750 customers; Year 3 hits $250k at $30 CAC for about 8,333.

Here’s the quick math: lower CAC lets the business buy more demand with the same cash, but paid traffic is not free scale. Organic traffic still costs time, content, testing, and platform risk, and affiliate or partner commissions must be counted as acquisition cost too. If CAC rises faster than gross margin, take-home income gets squeezed fast.

Measure CAC by channel

Track marketing spend, new customers, blended CAC, and channel CAC by paid search, social, email, affiliate, and partners. Count commissions, creative, software, and agency fees in the same bucket so the number stays real. One clean rule: if a channel cannot show payback, it is not helping owner income.

CAC = total acquisition spend ÷ new customers

Include affiliate commissions

Test traffic quality, not clicks

Watch repeat purchase intent

If low-intent traffic lifts spend without enough orders, cash flow tightens and owner draws come later. Keep testing by channel, pause weak sources fast, and shift dollars toward the mix that brings the lowest-cost customers with the highest repeat rate.

4

Fulfillment Leverage And Operating Costs

Fulfillment Cost Stack

Online sales can look strong and still leave thin owner pay. Here’s the quick math: 8% sourcing + 4% fulfillment + 25% payment processing + 3% returns processing = 40% of revenue gone before fixed overhead. Add $64k a month in fixed expenses, or $768k a year, and order volume has to stay high just to keep cash flow steady.

Payroll must be kept separate from owner draw. The forecast lists payroll at $1,775k in Year 1 and $445k by Year 5, so don’t let that line get mixed into profit available to the owner. If returns or payment fees rise, take-home can drop fast even when gross margin still looks fine.

Track the True Order Cost

Measure contribution margin, the cash left after variable costs, on every order. Split one-time setup costs, recurring tools, transaction fees, and labor so owner pay is not overstated. One clean rule: if the order does not cover its share of fixed costs, it is not funding the owner.

Track order-level cost by channel.

Watch refunds and returns monthly.

Test payment fees against 40%.

Keep fixed spend near $64k monthly.

Separate payroll from owner draw.

5

Retention And Repeat Revenue

Retention And Repeat Revenue

Retention steadies owner pay because repeat orders cut dependence on paid customer acquisition. In this model, repeat customers rise from 25% of new customers in Year 1 to 55% in Year 5, while repeat customer life extends from 8 to 18 months. That usually means more revenue comes from customers already acquired, so cash flow is less choppy.

The main inputs are repeat order rate, average order value, and support cost. With repeat orders moving from 0.4 to 0.8 per month, the same customer can generate more gross profit before churning. Subscriptions, memberships, email retention, communities, and repeat offers can lift lifetime value, but refunds and service load can still pull down owner take-home.

Track Repeat Orders

Measure repeat revenue by customer group, not just total sales. Track repeat share, months to second order, repeat order frequency, refund rate, and support tickets per buyer. Then test which offer keeps people buying without adding too much service cost. Owner income improves when repeat sales stay high and the cost to serve stays flat.

Watch repeat share monthly.

Price memberships for margin.

Test post-purchase email flows.

Limit refunds and support strain.

Here’s the quick math: if retention lifts from 25% to 55%, the business leans less on new paid traffic and more on lower-cost repeat sales. That helps profit and draw stability, but only if ongoing support staffing stays ahead of complaint volume and returns do not erase the gain.

6

Digital Entrepreneur Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner pay is tight early because marketing, payroll, and inventory eat cash before repeat demand builds. The upside case only works if acquisition stays efficient and repeat buying climbs.

Low, base, and high owner income paths.

Scenario

Low CaseCash strain

Base CaseRepeat demand

High CaseExecution difficulty

Launch model

This is the downside path where owner income stays constrained.

This is the modeled middle path where owner pay starts to become realistic.

This is the upside path where stronger demand can create meaningful owner income.

Typical setup

Year 1-level revenue and heavy marketing keep EBITDA near negative $212k, so the founder salary depends on outside cash and there is no safe distribution base.

By Year 2, the model shows $120k marketing, $32 CAC, and EBITDA close to breakeven before turning positive later, so owner income depends on repeat orders and cost control.

Year 3 turns strongly profitable with EBITDA around $1.11M, but it needs $250k marketing, a larger payroll, and better repeat demand to hold the pace.

Cost drivers

Marketing spend

payroll load

CAC

variable costs

fulfillment

Marketing efficiency

repeat orders

payroll growth

product mix

fulfillment costs

Repeat buyers

CAC

marketing scale

payroll expansion

product mix

Owner income rangeBefore owner reserves

No safe drawCash strain

Near break-evenModest pay

$1.1M+Scale upside

Best fit

Use this to test survival when cash stays tight and scale is slow.

Use this as the main planning case for a stable but still cash-tight run rate.

Use this to test what happens if growth and repeat demand both stay strong.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution advice.

In this model, the founder salary is planned at $100,000, but the business shows a $166k operating loss after payroll, marketing, fixed overhead, and variable costs Year 1 revenue is about $167k, marketing spend is $50k, and setup costs total $73k That salary needs funding support, not just operating profit

Distributions become more realistic when the business has profit after salary, taxes, reserves, and working capital In the researched case, Year 2 produces about $769k in revenue and $163k in operating profit after the $100k founder salary That profit is before taxes and reserves, so distributing all of it would be aggressive

Not always, but this model uses paid marketing as a major growth driver Marketing rises from $50k in Year 1 to $250k in Year 3, while CAC improves from $35 to $30 Organic traffic can reduce cash spend, but it still costs time, content production, testing, and platform risk

The biggest drivers are CAC, repeat purchases, AOV, payroll, and variable cost rates In this model, AOV rises from $6498 to $84 by Year 3, repeat customers rise from 25% to 45%, and variable costs fall from 175% to 153% of revenue Those shifts help profit scale after fixed costs are covered

Separate planned salary from distributions This model includes a $100,000 founder salary, but extra owner pay should come only after the business covers marketing, payroll, fixed overhead, taxes, reserves, and working capital A practical rule is to review cash after each month or quarter before taking profit out

About the author

Daniel Brooks

Practical Business Analyst

Daniel Brooks is a practical business analyst at Financial Models Lab, where he writes about small business budgeting and estimating what a new business can realistically earn. He creates clear, beginner-friendly content for people planning to open a physical location, with a focus on realistic assumptions, break-even explanations, and what it really takes to get a business off the ground.

Choosing a selection results in a full page refresh.