Dog Food Formulation Consulting Owner Income: $148M Year 1 EBITDA

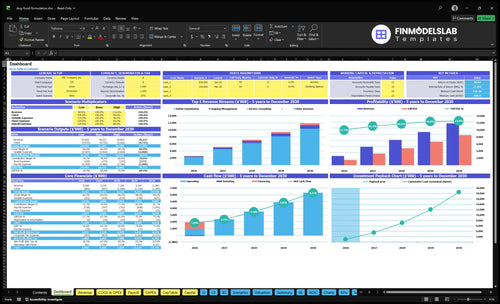

You’re modeling owner income from a dog food formulation consulting business, so revenue alone isn’t the answer In this researched five-year model, revenue grows from $2588M in Year 1 to $11863M in Year 5, with EBITDA from $1477M to $8540M before taxes, debt service, reserves, and owner distributions Actual take-home depends on pricing, client volume, formulation complexity, compliance support, reserves, and whether the owner fills the $185,000 Chief Veterinary Nutritionist role

Owner income$1.48M to $8.54MNet margin57% to 72%Revenue for target pay$2.59M to $11.86MBusiness difficultyHard

Want to estimate your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to test the forecast for Dog Food Formulation Consulting?

Can a dog food formulation consulting business scale?

It can scale, but expert capacity is the hard limit in Dog Food Formulation Consulting. The model only gets bigger when workflow, documentation, subcontractor review, and client success support cut the owner out of every bottleneck. With 1 associate nutritionist in Year 2, then 15 in Year 3, 20 in Year 4, and 30 in Year 5, revenue grows from $2588M to $11863M and EBITDA from $1477M to $8540M.

What drives scale

Workflows reduce review time

Documentation standardizes repeats

Subcontractors add capacity

Client support cuts revisions

What can slow it

Owner stays primary technical reviewer

Liability rises with volume

Compliance adds more checks

Revision time delays delivery

What profit margin can dog food formulation consulting earn?

Dog Food Formulation Consulting can keep a strong margin if delivery stays light: Year 1 gross margin is 82% after 8% software and 10% subcontractors, and contribution margin is 74% after another 5% referral commission and 3% payment processing. For the cost base, see What Are Operating Costs For Dog Food Formulation Consulting?; fixed overhead is $4,550 per month, and Year 1 payroll starts at $185,000 for the chief nutritionist, $32,500 for client success coverage, and $75,000 for the marketing lead. Reserves still come before owner distributions.

Margin math

82% gross margin in Year 1

74% contribution margin in Year 1

Software and subcontractors take 18%

Referrals and processing take another 8%

Cash pressure

$4,550 monthly fixed overhead

$292,500 Year 1 payroll

Chief nutritionist is $185,000

Keep reserves before owner payouts

How many dog food formulation clients do I need?

For Dog Food Formulation Consulting, use client economics, not salary averages: at $1,438 blended Year 1 revenue per client, a $2.588M Year 1 revenue goal needs about 1,800 blended client-equivalent units. See the KPI setup in What Are The 5 KPIs For Dog Food Formulation Consulting Business?; the client count changes fast if you add larger packages, repeat retainers, or commercialization support.

Client math

$1,250 initial consultation revenue

50 hours at $250 blended rate

40% buy ongoing management

15% buy ad-hoc consulting

Break-even lens

26% direct and variable costs

$1,064 contribution per blended client

Before payroll, marketing, overhead, reserves

$2.588M ÷ $1,438 ≈ 1,800 clients

Dog Food Formulation Consulting Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Project Pricing

$200-$300

Initial consults run $250 to $300 per hour and ongoing work runs $200 to $240, so price sets the ceiling on owner take-home.

2

Client Volume

$2.6M-$11.9M

Revenue rises from $2.588M in Year 1 to $11.863M in Year 5, so more active clients drive the biggest jump in cash flow.

3

Retainer Mix

40%-60%

Ongoing management grows from 40% to 60% of the mix, and that recurring work makes income steadier and less dependent on one-off jobs.

4

Delivery Margin

74%-83%

Direct costs stay near 17% to 26% of revenue, so every point of margin loss hits operating profit fast.

5

Owner Utilization

1.8-2.3h

Billable hours per active customer rise from 1.8 to 2.3 a month, so better use of time lifts revenue without much extra overhead.

6

Overhead Control

$4.6K

Fixed overhead is about $4,550 a month, and the model still needs an $841K cash floor in Month 2, so reserve discipline protects take-home pay.

Dog Food Formulation Consulting Core Six Income Drivers

Project Pricing

Project Pricing

Higher dog food formulation fees lift owner income only when the price matches complexity, compliance support, revisions, and commercialization work. On a 5-hour initial project, $250/hour brings in $1,250; at $300/hour, it becomes $1,500. That $50 increase adds $250 before delivery costs.

The risk is underpricing revision-heavy formulas. If scope expands but the fee stays flat, expert review time eats margin and lowers the owner’s draw. One clean rule: charge more when the recipe needs more back-and-forth, label support, or launch help.

Price by scope, not hope

Track hourly rate, project hours, revision count, and whether the job needs compliance or commercialization support. The goal is to keep each fee above the time it will really take, so owner pay rises with complexity instead of disappearing into unpaid rework.

Test higher rates on the hardest work first. What this estimate hides is the revision burden, so price the likely back-and-forth up front.

Quote revision caps up front.

Separate compliance review fees.

Reprice launch support yearly.

1

Client Pipeline

Client Pipeline

The pipeline is the flow of pet food startups, product teams, private-label sellers, and reformulation clients into paid work. Owner income rises when more of those leads turn into billable projects, because cash comes from active clients, hourly work, and repeat contracts.

Year 1 marketing spend is $45,000 with $150 CAC (customer acquisition cost, or what it costs to win one client). By Year 5, spend rises to $100,000 and CAC falls to $125, but paid CAC alone does not explain revenue. Referrals, repeat clients, and larger contracts must carry volume, or the owner ends up with too much review time and not enough take-home profit.

Improve Pipeline Quality

Track lead source, close rate, average contract value, and revision hours by client type. Low-fit clients can burn expert review time, so one weak lead can hurt margin more than its fee helps it. The useful measure is not just leads, but qualified leads that convert to work fast and need fewer rework cycles.

Use a simple filter before selling: fit for formulation work, willingness to pay, and likely repeat need. Here’s the quick math: if marketing spend rises but CAC only drops from $150 to $125, growth still depends on referrals, retainers, and bigger projects. That protects gross margin and keeps owner pay from being eaten by unbillable screening.

2

Retainer Revenue

Retainer Revenue

Retainer revenue turns one-off dog food formulation work into steadier cash flow. Here’s the quick math: at 15 hours per participating customer, the ongoing work is worth $3,000 in Year 1 at $200 per hour, and $3,600 in Year 5 at $240 per hour. The mix shifts from 40% ongoing management in Year 1 to 60% in Year 5, so more income comes from label reviews, ingredient swaps, compliance questions, reformulation support, and pipeline planning.

That matters because higher retention means less monthly pressure to refill the project pipeline. The owner’s take-home income gets smoother, and billing is less tied to new launches. What this estimate hides: if retention is weak or work stays outside the retainer scope, the business still gets lumpy and the owner spends more time selling than serving.

Track Retainer Hours Closely

Price the retainer around the actual service mix, not a vague support promise. Track retained customers, hours used, and hours by task so you can see whether label reviews, substitutions, and reformulation requests are eating the margin. One clean formula: retainer revenue = active customers × 15 hours × hourly rate.

Raise rates as the work gets more compliance-heavy. If the service moves from light check-ins to deeper ongoing management, the extra time should show up in the price. That protects gross margin and keeps recurring revenue strong enough to cover owner pay without chasing new projects every month.

3

Delivery Margin

Delivery Margin

Delivery margin is the gap between client revenue and the cost to actually deliver the dog food formula work. In Year 1, direct delivery costs are 18% from 8% software and 10% subcontractors, and total variable load rises to 26% after 5% referral fees and 3% payment processing.

Here’s the quick math: at a 26% variable load, each $1 of revenue leaves $0.74 before fixed overhead and owner pay. The risk is treating gross revenue as take-home cash before specialist review and compliance support; the model lists Year 5 total variable load at 175%, which would wipe out margin if that input is correct.

Protect the delivery spread

Measure delivery margin by project, not just by month. Track client count, hourly fee, software spend, subcontractor review cost, referral fees, payment fees, and revision time. If revisions push variable load above 26%, owner pay drops fast because less revenue is left to cover overhead and profit draw.

Track software as a revenue percent.

Track subcontractor review hours.

Track referral and payment fees.

Track revision time per project.

Set scope rules before work starts. Cap revision rounds, separate compliance support from the base fee, and price specialist review so it is fully covered. If referral and payment fees stay at 8% combined, the margin still depends on keeping subcontractor rework and software use tight.

4

Owner Utilization

Billable Hours per Client

This driver is the ceiling on owner income because expert review, client calls, documentation, revisions, and admin time only scale so far. At 18 billable hours per active customer in Year 1 and 23 by Year 5, a fuller calendar raises revenue, but only if those hours stay paid and tied to active clients.

Initial consultations take 50 hours, ongoing management 15, and ad-hoc consulting 20, so the mix matters as much as volume. If expert review gets rushed, quality slips and rework eats owner pay; if workflows cut nonbillable admin, the same hours produce more take-home cash.

Protect Review Time

Track billable hours per active client, nonbillable admin, and rework hours. The simple test is whether each added client lifts cash without pushing expert review into rush mode. One clean rule helps: protect review time before you book extra calls.

Use the Year 1 to Year 5 range as a capacity check, not a goal to cram more work into the same day. At 18 to 23 billable hours per client per month, a higher load should come with tighter scope, better templates, and clear turnaround rules so owner income rises without quality risk.

5

Overhead And Reserves

Overhead And Reserves

Fixed overhead is $4,550 per month before any owner pay, and that includes $600 insurance, $450 portal hosting, $2,200 studio rent, $150 platform license, $800 legal and accounting, and $350 utilities and internet. Add $45,000 in Year 1 marketing, or about $3,750 per month if spread evenly, and the cash drain gets real fast. That lowers immediate take-home even when sales look healthy.

Reserves come first, then owner distributions. If Month 2 cash need is $841k, the business cannot treat paper profit as spendable cash, especially during hiring or capex-heavy periods. The key input is not just revenue, but how much cash stays after fixed overhead, marketing, and operating runs. One bad draw can turn a busy month into a liquidity problem.

Protect Cash Before You Pay Yourself

Track monthly fixed overhead, marketing cash burn, and ending cash before any draw. Use a simple rule: reserve enough to cover fixed overhead plus the next planned spend cycle, then pay the owner from what remains.

Watch three numbers each month: $4,550 base overhead, $45,000 annual marketing, and the $841k Month 2 cash need. If hiring starts or equipment spend rises, hold distributions back until reserves are rebuilt.

Forecast cash before owner pay

Separate reserve and operating accounts

Delay draws during hiring spikes

6

Dog Food Formulation Consulting Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and growth owner income scenarios

Owner income scenarios

Owner income shifts with billable hours, staffing, and marketing spend. The same consulting model can stay lean at launch or scale fast as repeat work grows.

Low, base, and high owner income paths at a glance.

Scenario

Low CaseLean launch

Base CaseCore plan

High CaseUpside run

Launch model

This is the lower owner-income path, with Year 1 staying close to launch scale and tighter take-home after overhead.

This is the modeled mid-case, with income building as ongoing management and ad-hoc work carry more of the book.

This is the stronger earnings path, with a larger recurring base and higher owner take-home potential if utilization stays high.

Typical setup

Year 1 revenue is $2.588M and EBITDA is $1.477M, with $45,000 marketing, 100% initial consultations, and a 1.0 nutrition lead plus a 0.5 client success role.

Year 3 revenue is $7.185M and EBITDA is $4.809M, with $75,000 marketing, 50% ongoing management, and a 1.5 FTE associate nutritionist added.

Year 5 revenue is $11.863M and EBITDA is $8.540M, with $100,000 marketing, 60% ongoing management, 25% ad-hoc consulting, and a 3.0 FTE associate nutritionist.

Cost drivers

Marketing spend

payroll load

software and subcontractors

fixed overhead

referral and processing fees

Repeat client mix

staffing ramp

marketing spend

billable hours per active customer

software and subcontractors

Recurring client mix

marketing spend

larger payroll

billable hours per active customer

lower software and subcontractor share

Owner income rangeBefore owner reserves

$1.48M EBITDA proxyLower income band

$4.81M EBITDA proxyCore income band

$8.54M EBITDA proxyUpside income band

Best fit

Use this to stress-test a slower launch or a year with weaker client ramp.

Use this as the default plan for budgeting, hiring, and owner draw decisions.

Use this to test what happens if repeat work and staffing scale cleanly.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The researched model shows $1477M in Year 1 EBITDA and $8540M in Year 5 EBITDA, but that is not guaranteed owner pay If the owner fills the Chief Veterinary Nutritionist role, the model also includes $185,000 payroll for that seat Distributions should come only after reserves, taxes, debt service, and reinvestment

The model reaches breakeven in Month 3 and payback in Month 4 That assumes Year 1 revenue of $2588M, a 74% contribution margin after direct and variable costs, and $4,550 in monthly fixed overhead before payroll and marketing If client conversion slows, breakeven moves later

Yes, credibility matters because clients often need help aligning formulas and labels with Association of American Feed Control Officials guidance The model includes subcontractor review at 10% of revenue in Year 1, falling to 65% by Year 5 If the owner lacks deep compliance skill, specialist costs should stay in the forecast

Pricing, client volume, retainers, delivery margin, owner capacity, and reserves drive profit Year 1 contribution margin is 74%, based on 18% software and subcontractor costs plus 8% referral and payment fees Ongoing management allocation rises from 40% to 60%, which improves recurring revenue and reduces pipeline pressure

Use project pricing for defined formulation work and retainers for ongoing support The researched rates start at $250 per hour for initial consultations, $200 for ongoing management, and $225 for ad-hoc consulting Fixed packages work best when they include revision limits, compliance scope, and clear handoff documents

About the author

Alex Morgan

Small Business Advisor

Alex Morgan is a small business advisor at Financial Models Lab, where he helps online business beginners plan before launch by breaking down startup costs, common expenses, revenue drivers, and key launch requirements. He focuses on pricing and profitability basics, explaining business costs in clear, practical language without unnecessary jargon so readers can make more confident decisions.

Choosing a selection results in a full page refresh.