How Much Does A Donut Shop Owner Make? $70K Salary Plan

Donut Shop Bundle

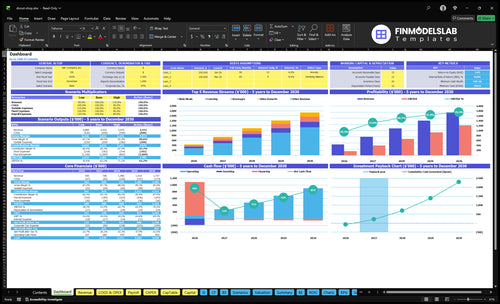

Under the researched assumptions, a donut shop owner can plan around a $70K annual salary, or about $58K per month, before personal taxes The modeled shop generates about $475K in Year 1 revenue and $168K in EBITDA By Year 5, revenue reaches about $1734M with $1222M in EBITDA Owner pay still depends on debt service, reserves, reinvestment, and whether the owner pulls distributions

Owner income$70KNet margin35.4%Revenue for target pay$475KBusiness difficultyHard

Want to test your donut shop owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on demand, margin, payroll, reserves, and debt service.

Want to check owner income in the Donut Shop model?

This dashboard in the Donut Shop Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions—open the model.

Owner-income model highlights

$70K owner salary

Revenue, EBITDA, breakeven

13% COGS, 5% variable

$363K overhead, $135K payroll

Is owning a donut shop profitable without the owner working daily?

If the owner is not there daily, the Donut Shop usually needs a paid manager or production lead, so profit gets thinner fast. The current owner-operated model already assumes a $70K Head Chef Owner salary at 10 FTE, and that cost does not cover absentee leadership. Scaling can improve revenue, but it also adds payroll, so higher take-home only works with systems, capacity, reserves, and tight margin control.

Owner pay risk

$70K owner salary is built in

10 FTE is the base model

Absentee owner needs extra leadership

That cost is not provided

Scale pressure

Assistant rises from 10 to 15 FTE

Service staff rises from 05 to 10 FTE

Driver rises from 05 to 10 FTE

Catering lead reaches 05 FTE

How much does a donut shop owner make per year?

A Donut Shop owner in this model makes a $70K annual salary before personal taxes; for the operating metric behind that pay, see What Is The Most Critical Measure Of Success For Your Donut Shop?. That salary is not the same as owner distributions, because debt service, taxes, reserves, and reinvestment reduce cash available.

Modeled owner pay

$70K salary before personal taxes

Role: Head Chef Owner

Staffing: 10 FTE

Salary differs from distributions

Profit capacity

Year 1 revenue: $475K

Year 1 EBITDA: $168K

Year 5 revenue: $1.734M

Year 5 EBITDA: $1.222M

What is a good profit margin for a donut shop?

For a Donut Shop, a good profit margin is one that still leaves room after waste and labor; this model shows 35.4% EBITDA in Year 1, or $168K on $475K revenue. If you want the startup cost context, see How Much Does It Cost To Open A Donut Shop?

Year 1 margin

35.4% EBITDA margin

$168K EBITDA in Year 1

$475K Year 1 revenue

Ingredients run at 10%

Margin drivers

Paper supplies are 3%

Fuel and vehicle costs are 3%

Event fees and marketing are 2%

Watch waste, labor, rent, and underpriced catering

Donut Shop Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six donut shop income drivers?

1

Customer Volume

465/wk

Weekly covers start at 465 in Year 1, and the $18 midweek and $22 weekend tickets decide how fast owner take-home grows.

2

Margin Mix

13% COGS

Food and beverage cost set the gross margin, so every point of waste cuts cash left for the owner.

3

Labor Load

$135K

Year 1 wages total $135K, and tighter staffing is what turns sales into take-home instead of payroll.

4

Fixed Overhead

$363K

Fixed overhead hits before profit does, so this cost base sets how much volume the shop needs to stay ahead.

5

Add-on Sales

12%/13%

Beverages and catering add margin-heavy sales, and those small tickets can lift owner income fast.

6

Channel Capacity

1.4K/wk

Sales and capacity expand weekly covers toward about 1.4K by Year 5, which raises profit without the same jump in fixed cost.

Donut Shop Core Six Income Drivers

Customer Count And Average Ticket

Customer Count and Ticket Size

465 weekly customers plus a $18 midweek AOV and $22 weekend AOV tells you this income driver is about both traffic and basket size. With 195 weekday buyers and 270 Friday-to-Sunday buyers, the simple math is 195 × $18 + 270 × $22 ≈ $9.5K per week before add-ons. More visits only improve owner pay if labor, waste, and prep capacity stay controlled.

Track covers and basket mix

Watch weekday vs. weekend covers, ticket by daypart, and repeat morning buyers. Office orders, dozen boxes, and coffee can lift revenue base, but they should not add overtime or spoilage. If Friday-Sunday already drive 270 of 465 weekly customers, staff those peak hours first and test small ticket lifts before adding menu items or labor.

1

Gross Margin And Waste Control

Gross Margin And Waste Control

This driver is the share left after food and supply costs. Year 1 COGS is 13%, split into 10% food ingredients and 3% beverage paper supplies, so gross margin starts at 87%. If ingredients fall to 8% and paper supplies to 2% by Year 5, gross margin rises to 90%, and that extra margin flows to owner pay if sales hold steady.

The main leak points are flour, sugar, fillings, toppings, frying oil, packaging, spoilage, and overproduction. Here’s the quick math: every 1 point cut in COGS adds 1 point to gross profit. What this hides is batch timing; if product is made before demand is known, waste can erase the gain even when pricing looks fine.

Tighten Waste, Raise Margin

Track recipe cost by item, then compare it with actual waste each week. Price for the real cost of toppings, oil, cups, and bags, and use small-batch production so slow movers do not sit. Preorder planning for office orders and busy days helps because a sold item beats a trashed one every time.

Measure ingredient cost per recipe.

Count spoilage and overproduction.

Use preorder data for batch size.

Check inventory before each shift.

Keep a simple target: hold Year 1 COGS near 13%, then push it down with better pricing, tighter buys, and fewer extras that do not sell. If food ingredients move from 10% toward 8% and paper supplies from 3% toward 2%, more cash stays in the business and owner distributions improve.

2

Labor Efficiency And Owner Role

Labor Efficiency And Owner Role

Labor is the take-home gate. Year 1 payroll totals $360K: $70K Head Chef owner, $40K kitchen assistant, $125K service window staff, and $125K driver. The owner’s labor is not free if it replaces market-rate management later, so the real test is whether that payroll supports enough gross profit to pay overhead and still leave a draw.

This driver includes production hours, counter coverage, delivery prep, and manager payroll. Year 2 adds a catering lead, so labor pressure rises as volume grows. If scheduling is tight, EBITDA holds up and owner distributions stay available; if hours drift or management gets added too early, take-home cash gets squeezed fast.

Track Labor by Shift and Role

Measure labor by role, not just by payroll total. Track hours per cover, labor per order, and who is on during early production, service window peaks, and delivery runs. If the owner is covering a manager job, assign a market wage to that time so profit is not overstated. That keeps the forecast honest.

Use staffing plans that match demand by daypart. One clean rule: schedule to sales, not habit. If counter coverage or delivery prep runs over, cut waste elsewhere before you add headcount. The win here is simple: tighter shifts protect EBITDA, and EBITDA is what funds owner pay.

3

Rent And Fixed Overhead

Fixed Overhead

Rent and fixed overhead are the monthly bills you pay before one more donut sells. The model shows $3,025 per month in fixed overhead, including $1,500 kitchen rent, $350 insurance, $400 maintenance, $100 POS, $150 permits, $300 accounting and legal, $150 utilities, and $75 software; the model also lists $363K per year.

Here’s the quick math: sales have to cover fixed overhead before the owner sees profit. High-traffic sites can lift revenue, but if rent or recurring fees rise faster than daily sales, owner take-home gets squeezed. Low overhead gives more room for draw and less pressure on every cover.

Keep the monthly hurdle low

Run the site test with daily sales, average ticket, and the fixed-cost line items above. If a location needs too much volume just to cover rent, the owner’s pay gets thinner even when the shop looks busy.

Track every recurring charge by category and cap it fast. One clean rule: if fixed overhead rises, sales must rise too. Keep software, permits, accounting, and maintenance lean, and compare each site’s rent to its expected daily covers.

4

Coffee, Beverages, And Product Mix

Coffee and Product Mix

Coffees, drinks, specialty donuts, dozen boxes, seasonal items, and combos lift average order value (AOV) without adding a full new customer. In Year 1, the mix is 12% beverages, 10% sides and desserts, and 13% catering. With midweek AOV at $18 and weekend AOV at $22, owner income rises only when each add-on clears its own packaging, labor, and waste cost.

Measure Incremental Profit

Track beverage attach rate, meaning how often a drink gets added, plus combo rate and spoilage by SKU. Price each add-on for the extra cup, lid, prep minute, and cleanup. If a new item does not raise gross profit per ticket, cut it. That keeps cash flow cleaner and protects owner draw when traffic slows.

Watch attach rate weekly.

Test one seasonal item.

Drop slow, wasteful SKUs.

5

Wholesale, Catering, And Capacity

Wholesale and catering can grow revenue

Wholesale and catering can lift sales, but they only help owner pay if the order still carries margin after prep, delivery, and discounts. Here’s the quick math: catering grows from 13% of sales in Year 1 to 25% in Year 5, so the channel mix gets much heavier. If production gets tight, extra volume can crowd out walk-in sales and squeeze cash flow.

Price every preorder for labor and miles

Track preorders, office orders, prep time, delivery miles, discount rate, and vehicle cost per order. Year 1 fuel and vehicle operating costs are already 3% of sales, before you add labor and packaging. The catering lead begins in Year 2 and reaches 0.5 FTE, so staff for it early or the owner ends up covering the gap.

Measure margin per catering order.

Watch prep hours per event.

Cap discounts before they spread.

6

Donut Shop Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and strong donut shop income scenarios

Owner income scenarios

Owner income moves with daily covers, ticket size, and catering mix. Labor, rent, reserves, and any debt service decide how much cash can reach the owner.

Shows how traffic, pricing, and catering change owner take-home.

Scenario

Low CaseDownside case

Base CaseCore case

High CaseUpside case

Launch model

Traffic runs below plan, so owner income stays tight and may depend on salary only.

The modeled shop supports the owner salary and some added cash, but not a big payout.

Stronger traffic and a bigger catering mix can lift owner income well above salary.

Typical setup

Daily customers come in below the modeled path, AOV stays weak, catering stays small, and rent, labor, and ingredients still need to be paid.

Year 1 revenue is about $475K, EBITDA is $168K, and breakeven lands in Month 3 with the $70K owner salary built in.

Year 5 reaches about $1.734M revenue and $1.222M EBITDA, with higher covers, stronger weekend pricing, and more catering supporting salary plus distributions.

Cost drivers

Fewer daily customers

weaker AOV

lower catering share

fixed rent and labor

reserve pressure

Modeled traffic path

$18 midweek and $22 weekend AOV

Month 3 breakeven

steady wages and rent

controlled reserves

Higher daily covers

$1.734M Year 5 revenue

$1.222M EBITDA

stronger catering mix

reinvestment and staffing

Owner income rangeBefore owner reserves

Salary onlySalary only

Salary plus modest distributionsModest distributions

Salary plus larger distributionsLarger distributions

Best fit

Fits founders stress-testing thin traffic, slower pricing, and delayed catering.

Fits planners using the Year 1 operating case and testing if take-home can extend beyond salary.

Fits owners modeling a scaled shop with stronger volume, tighter operations, and extra cash for payouts.

!

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or guaranteed distributions.

The modeled owner salary is $70K per year, or about $58K per month, before personal taxes That is separate from business profit Year 1 also shows about $168K in EBITDA on $475K in revenue, but distributions depend on reserves, debt service, taxes, and reinvestment needs

The model reaches breakeven in Month 3 Payback is shown at 16 months, with minimum cash of $765K in Month 2 Treat those as planning outputs, not promises, because sales pace, buildout costs, payroll timing, and debt terms can move the actual break-even point

Yes, reserves should come before extra owner draws The plan already includes a $70K owner salary, $135K total Year 1 payroll, and $363K fixed overhead EBITDA is not the same as free cash because taxes, loan payments, equipment replacement, and slow weeks can absorb cash fast

Customer count, average ticket, labor, waste, and fixed overhead drive owner income most The base year uses 465 weekly customers, $18 midweek AOV, $22 weekend AOV, and 13% COGS If traffic rises but staffing, waste, or delivery costs rise faster, owner take-home can still fall

Raise profitable volume before adding complexity In this model, catering grows from 13% to 25% of sales, beverages hold near 10% to 12%, and ingredient cost improves from 10% to 8% The cleanest levers are preorders, coffee attach rate, tight batching, and labor schedules matched to the morning rush

About the author

Oliver Pierce

Startup Cost Researcher

Oliver Pierce is a startup cost researcher at Financial Models Lab, where he writes practical guides for people planning their first business. He focuses on break-even planning and on comparing business ideas by cost and effort, with a clear, realistic approach to small business planning. His work is aimed at non-finance readers and is written to make business planning easier to understand and use.

Choosing a selection results in a full page refresh.