Owner income≈$111M

Owner income≈$111MIs Owning a Drone Delivery Services Business Worth It Financially?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income≈$111M  Net margin91% to 94%

Net margin91% to 94% Revenue for target pay≈$120M

Revenue for target pay≈$120M Business difficultyHard

Business difficultyHard

Key Takeaways

- Dense routes lift contribution per delivery and per hour.

- Pricing and contracts set the ceiling for owner pay.

- Permissions and service areas must precede delivery forecasts.

- Uptime, staffing, and reserves protect cash and scale.

Owner income≈$111MNet margin91% to 94%Revenue for target pay≈$120MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the financial model?

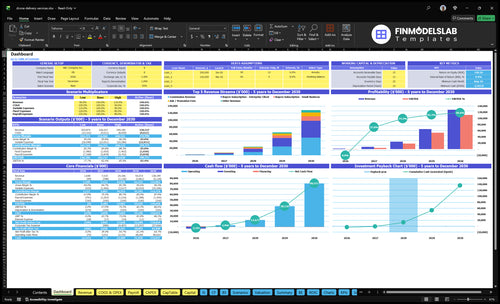

The Drone Delivery Service Financial Model Template shows why owner income needs a full model, not one delivery-fee guess; the dashboard tracks revenue, gross margin, operating costs, cash runway, and take-home. Charts show $645-$696 per order, direct cost falling from 90% to 60%, and marketing rising from $350,000 in Year 1 to $65 million in Year 5, with assumptions tabs for acquisition, mix, orders, AOV, fees, subs, costs, staffing, insurance, maintenance, compliance, marketing, reserves, and scenarios. Open the model.

Owner-income model highlights

- Buyer and seller inputs

- CAC and cost curves

- Distributable owner cash

Is a drone delivery service profitable as an owner operator?

Yes, a Drone Delivery Service can work as an owner operator, but only if route density, contracts, permissions, uptime, and controls hold. Early cash flow can look better because you skip payroll, yet the founder still has to handle monitoring, dispatch, customer support, seller onboarding, and issue resolution. In year 1, the model assumes 200 sellers from $100,000 of marketing at $500 CAC and 5,000 buyers from $250,000 of marketing at $50 CAC.

Early cash flow

- Skip payroll at the start.

- Founder absorbs ops workload.

- Use 200 sellers as the base.

- Track $500 CAC per seller.

Scale risk

- Year 5 reaches 5,000 sellers.

- Year 5 reaches 200,000 buyers.

- Higher scale lifts insurance and support.

- More scale also raises compliance load.

How many deliveries does a drone delivery service need to make money?

A Drone Delivery Service makes money when monthly deliveries cover fixed overhead, target owner pay, and any gap after subscription gross profit. Here’s the quick math: contribution per order = revenue per order × (1 − direct cost rate), so first-year contribution is about $587 per order ($645 × 91%) and year 5 is about $654 per order ($696 × 94%). Break-even deliveries per month = (fixed overhead + target owner pay − subscription gross profit) ÷ contribution per order.

Break-even inputs

- $645 first-year revenue per order

- $587 first-year contribution per order

- $696 year 5 revenue per order

- $654 year 5 contribution per order

What can stop scale

- Fixed overhead still has to be covered

- Subscription gross profit lowers delivery pressure

- Dense routes raise delivery efficiency

- Weather and safe monitoring limit volume

How much can a drone delivery business owner make?

A Drone Delivery Service owner can’t be valued from gross revenue alone: first-year order revenue is about $645, but listed direct costs run 90% before payroll and overhead. For deeper operating context, see What Is The Most Important Metric To Measure The Success Of Your Drone Delivery Service?, because take-home pay depends on salary, profit distributions, reserves, and missing cost lines.

Revenue math

- Year 1: about $645 per order

- $100 fixed commission included

- Year 5: about $696 per order

- $150 fixed commission included

Owner pay limits

- Direct costs: 90% in Year 1

- Direct costs: 60% in Year 5

- Salary is planned payroll, not profit

- Distributions need profit after reserves

Want to see what moves owner income?

1

$111KRoute Density

More routes per usable drone-hour spread fixed costs wider, so EBITDA grows from about -$4K in Year 1 to about $111K in Year 5.

2

$6.5-$7.0Pricing Mix

Each order earns about $6.45 to $6.96 in commission before subscriptions, so higher order value and more enterprise accounts lift take-home.

3

23%Service Area

Wider flight approval zones open medical routes, and medical supply rises to 23% of seller mix by Year 5.

4

1.5xFleet Uptime

Higher uptime lets each drone handle more repeat jobs, so daily delivery count can climb without the same payroll growth.

5

$685K-$1.1MStaffing Model

Payroll starts near $685K in Year 1 and reaches about $1.1M by Year 5, so staffing discipline has a big take-home effect.

6

$27.5K/moCash Reserves

Insurance, software, maintenance, and support run about $27.5K a month, so tighter reserves protect cash even when revenue grows.

Drone Delivery Service Core Six Income Drivers

Route Density And Delivery Volume

Route Density and Volume

If a route is thin, each flight burns time on launch, monitoring, and repositioning instead of paid drops, so revenue per operating hour falls. Dense routes raise deliveries per drone per day and completed deliveries per operating day, which improves owner pay only after fixed overhead is covered.

Here’s the quick math: first-year contribution is about $587 per order after listed direct costs, and Year 5 is about $654. More volume helps only when capacity, weather windows, payload limits, and service-area limits still allow it. If staff time rises faster than delivery revenue, take-home gets squeezed.

Improve Route Fill

Track route fill by zone, not just total orders. Use deliveries per drone per day, completed deliveries per operating day, and contribution per order as the core scorecard, then push demand toward the densest streets and time blocks. The goal is simple: more paid drops in the same operating day, with less unpaid repositioning.

- Measure idle time between flights.

- Track weather loss by operating day.

- Watch battery turnaround and maintenance downtime.

- Cap routes by payload and service area.

Build forecasts with blocked hours included, so you do not promise volume you cannot fly. If a lane needs more labor than it produces in delivery contribution, cut it fast and keep drones on the routes that cover overhead first.

1

Pricing And Contract Revenue

Pricing and Contract Revenue

This driver sets the ceiling for owner pay. Revenue per drone delivery is about $645 in year 1 and $696 in year 5, so pricing mix matters as much as delivery volume. The inputs are buyer AOV, commission rate, seller subscriptions, buyer subscriptions, and minimum-volume contracts. If delivery fees stay too low to cover operator labor and reserves, cash draws get risky fast.

Here’s the quick math: buyer AOV rises from $5,450 to $6,820, but the variable commission rate falls from 100% to 80%. Seller monthly subscription value moves from $5,300 to $6,272. Buyer subscriptions range from $999 to $19,900 in year 1 and $1,299 to $24,900 in year 5, which helps smooth cash flow.

Protect Revenue Per Delivery

Track revenue per delivery, not just order count. Split it into commission, subscription, and contract minimums, then test each segment by AOV and margin. One clean rule: every contract should cover operator labor, insurance, and reserve funding before owner pay. If not, the sale adds revenue but weakens cash.

Use minimum-volume contracts to reduce swings and protect monthly cash. Watch for buyer plans that look big on paper but fail to renew. If the weighted fee drops while AOV rises, check whether the commission cut is worth the stability. Keep pricing tied to the lowest profitable delivery, not the fastest sales win.

2

Regulatory Permissions And Service Area

FAA Permissions and Service Area

FAA status sets the ceiling on income because it controls where the drones can fly and how many routes can run. BVLOS approval can expand capacity, but only inside approved zones and operating rules. If the service area is thin or split by restrictions, completed deliveries drop, fixed costs stay put, and owner take-home falls.

Model this with approved zones, restricted routes, operating days, weather loss, operator requirements, and compliance costs. The key question is simple: do approved routes match dense customer demand? If they do, revenue per operating day improves. If not, planning too much volume before permissions are set can overstate cash flow and profit.

Model the Approved Map First

Track the share of demand inside approved zones, then compare it with route capacity. Use a simple forecast: expected deliveries = approved operating days × usable routes × completion rate. That keeps revenue tied to what is actually permitted, not hoped for. One clean rule: no approval, no volume assumption.

- Map approved and restricted areas.

- Count weather-lost operating days.

- Price compliance into route margins.

- Update volume after FAA changes.

What this estimate hides is delay risk. If permission timing slips, cash inflow can lag while operator time, software, and compliance spend keep running. So the owner should forecast income only after service-area limits, operator rules, and approved routes are documented.

3

Fleet Utilization And Uptime

Fleet Utilization And Uptime

Fleet utilization is the share of drones that are actually completing paid flights. The income link is revenue capacity minus replacement reserves, so a bigger fleet only helps if each drone gets enough paid trips. If drones sit in charge, repair, or weather hold, staff, software, insurance, and depot costs still run, and cost per delivery rises.

Track drones in service, battery turnaround time, charging limits, maintenance downtime, weather downtime, and payload capacity. One clear rule: idle drones do not pay the bills. Low uptime cuts completed deliveries and can shrink owner pay even when demand is strong.

Measure Uptime by Drone, Not Fleet Size

Use deliveries per drone per day as the core check, then break downtime into charge, repair, and weather. Forecast capacity as active drones × usable flight windows × paid flights, then subtract reserve drones and battery swaps. That shows how much revenue the fleet can really carry before overhead hits owner income.

Keep spare drones, spare batteries, and repair cycles in the plan so reserves are funded before profit is paid out. If charging or maintenance keeps pushing flights into the next day, missed windows hit cash flow fast. The fix is tighter uptime control, not just buying more drones.

- Track downtime by cause.

- Measure flights per drone daily.

- Fund repairs before owner draws.

- Stress-test weather and battery delays.

4

Staffing And Operations Model

Staffing And Operations

If the founder handles dispatch, customer service, seller onboarding, incident handling, and basic operations, payroll stays low, but the savings are partly hidden owner labor. Once you hire operators, support staff, and technicians, short-term take-home drops. The model only works when payroll is covered by deliveries, because route density and completed orders pay for the team.

One clean rule: staffing is a cash test, not a headcount test. Watch payroll per operating day, deliveries per operator, support tickets, and technician hours. Under-hiring pushes late deliveries, refunds, and churn; over-hiring lowers owner pay before volume can absorb it.

Track Labor Against Volu me

Start with a weekly staffing sheet. Match each hire to a volume trigger, then compare completed deliveries against payroll per operating day. If the route plan cannot keep the team busy, the founder should stay in the loop longer and keep payroll light. The goal is simple: avoid paying for idle capacity.

Use the first-year contribution math as your guardrail: about $587 per order after listed direct costs, rising to about $654 in Year 5. Staffing only improves owner income when that contribution can absorb labor and still leave cash for the owner. If service levels slip, the hidden cost shows up as refunds and churn, not just wages.

5

Insurance, Maintenance, Software, And Reserves

Insurance, Maintenance, And Reserves

Recurring overhead lowers what the owner can take home, even when delivery margins look good. If per-delivery direct costs drop from 90% to 60% of order value by moving insurance from 30% to 20%, drone energy and minor parts from 40% to 25%, and payment fees from 20% to 15%, more cash stays in the business.

That cash still has to cover annual insurance, software, depot rent, maintenance reserve, battery replacement, fleet replacement, compliance spend, and a cash buffer. If the owner gets paid before those buckets are funded, one repair or approval delay can turn paper profit into a cash crunch.

Fund Reserves Before Owner Draws

Set a reserve rule before any payout. Track reserve cash against monthly deliveries, repair spend, and software and rent bills, so you can see when fixed overhead starts eating distributable income. Cash reserve planning is not optional leftover profit planning.

- Ring-fence repair cash first

- Pay owner only after reserves

- Review battery and fleet needs monthly

- Stress-test low-volume months

Watch cash, not just profit. If the business cannot cover the next battery swap, software bill, or compliance cost, owner pay is already too high.

6

Compare lean, base, and high-scale owner-income cases

Owner income scenarios

Owner income swings with route density, order value, seller and buyer mix, and staffing. The same network can be near break-even at launch and strong at scale.

| Scenario | Low CaseLaunch risk | Base CaseManaged growth | High CaseScale-ready |

|---|---|---|---|

| Launch model | This is the lower earnings path, where launch volume and cash flow stay tight. | This is the modeled middle path, with steadier orders and better operating control. | This is the stronger earnings path, with scale volume and better unit economics. |

| Typical setup | Revenue is thin, order density stays low, direct costs run near 90% of listed levels, and the founder covers most operations. | The business gets more active subscription months, better repeat orders, and tighter labor control, so income improves without a full staffing spike. | The model uses Year 5-style CAC, 5,000 acquired sellers, 200,000 acquired buyers, $696 per order revenue, 60% listed direct costs, and heavy marketing. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$4,000 - $0Launch band | $4,284 - $17,967Growth band | $53,524 - $110,956Scale band |

| Best fit | Use this to stress-test launch months with weak density and founder-heavy coverage. | Fits a controlled growth plan with better repeat use and tighter staffing. | Tests upside from large buyer volume, stronger monetization, and a heavier growth budget. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Drone Delivery Service Porter's Five Forces Analysis

- Drone Delivery Service BCG Matrix

- Drone Delivery Service Business Model Canvas

- 7 Essential KPIs for Drone Delivery Service Profitability

- Drone Delivery Service Business Plan Template in Pre-Written Word

- 7 Financial Strategies to Increase Drone Delivery Service Profitability

- How Much Does It Cost To Operate A Drone Delivery Service?

- Drone Delivery Startup Costs: $1235M First-Year Operating Floor

- Drone Delivery Financial Model Template in Excel

- How To Start A Drone Delivery Service: 3–6 Month Pilot Plan

- How to Write a Drone Delivery Service Business Plan

- Drone Delivery Service Marketing Mix

- Drone Delivery Service Marketing Plan

- Drone Delivery Service Business Proposal

- Drone Delivery Service PESTEL Analysis

- Drone Delivery Service Pitch Deck Example Editable PPTX

- Drone Delivery Service Business SWOT Analysis

- Drone Delivery Service Value Proposition Canvas

Frequently Asked Questions

Owner pay depends on cash left after operations, not gross orders The provided assumptions support about $645 revenue per order in the first year and $696 in Year 5, before payroll and overhead Listed direct costs fall from 90% to 60%, but missing staff, depot, debt, and reserves prevent a fixed salary estimate