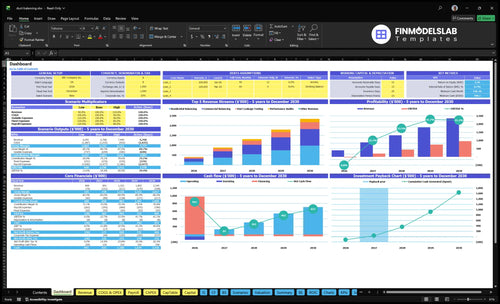

How Much HVAC Duct Balancing Owners Can Make At $23M Revenue

An HVAC duct balancing service owner can draw income only after the business covers field labor, vehicle costs, supplies, marketing, rent, insurance, software, and calibration In the researched base model, the company reaches breakeven in Month 8, with Year 1 EBITDA of -$30k on $408k revenue By Year 5, the model shows $965k EBITDA on $2345M revenue, before personal taxes, debt service, reserves, and owner distributions The clean one-liner: revenue is not owner pay

Owner income$85k baseNet margin-7% to 41%Revenue for target pay≈$207kBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner take-home depends on real demand, staffing, pricing, taxes, debt, and reinvestment needs.

Want to see the HVAC Duct Balancing Service forecast?

What affects profit margin in an HVAC duct balancing service?

For an HVAC Duct Balancing Service, profit margin is mostly driven by technician productivity, measured airflow time, system complexity, travel density, callback rate, and calibration. The Year 1 variable-cost mix is 8% field supplies, 10% vehicle fuel and maintenance, 5% referrals, and 3% payment processing, or 26% total before fixed overhead. Insurance, rent, software, and admin set the floor, and there is no single benchmark because scope and market mix change the math; see What Are Operating Costs For HVAC Duct Balancing Service?.

Margin drivers

Raise technician productivity.

Cut measured airflow time.

Reduce travel between jobs.

Lower callbacks with calibration.

Year 1 cost mix

8% field supplies.

10% fuel and maintenance.

5% referrals.

3% payment processing.

How much revenue does a duct balancing business need to pay the owner?

The HVAC Duct Balancing Service needs more than $408k in annual revenue to pay the owner cleanly. At that level, the model is still about -$30k EBITDA, so the $85k owner pay has to come from gross profit first, not from leftover cash. Salary, distributions, tax, debt repayment, and slow months should be separate buckets.

Pay first

$85k modeled owner salary

$552k fixed overhead per year

$12k Year 1 marketing

26% Year 1 variable costs

Cash reality

$408k revenue is still early

EBITDA stays near -$30k

Separate pay from distributions

Keep cash for slow months

Can an HVAC duct balancing service be profitable?

Yes, an HVAC Duct Balancing Service can be profitable, but the How To Launch HVAC Duct Balancing Service Business? model shows it is not profitable from day one: breakeven comes in Month 8, with Year 1 EBITDA at -$30k. The upside is real if paid jobs scale: Year 2 EBITDA reaches $202k and Year 5 reaches $965k.

Profit Drivers

Track completed paid work, not leads

Price for travel and technician time

Cover calibration, callbacks, and admin

Use energy savings up to 20%

Growth Limits

Expect Month 8 breakeven timing

Plan for -$30k Year 1 EBITDA

Grow into $202k Year 2 EBITDA

Add commercial jobs only if scheduling holds

HVAC Duct Balancing Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Job Volume

$408K-$2.345M

More completed jobs drive the top line from Year 1 to Year 5 and set the pace for owner take-home as EBITDA moves from -$30K to $965K.

2

Ticket Size

$300-$2.1K

A better mix of commercial balancing, leakage testing, and audits lifts the average project ticket, so each booking adds more cash to the owner.

3

Tech Productivity

4.5-5.5h

More billable hours per active customer and tighter crew use spread payroll across more work, which helps the business clear payback in 25 months.

4

Travel Density

8%-10%

Tighter routing can push fuel and maintenance toward the lower end of the 8%-10% direct cost band, keeping more gross profit in the company.

5

Callback Rate

5%-10%

Fewer callbacks avoid extra trips and labor, so the business protects the 5%-10% variable cost layer and keeps owner pay cleaner.

6

Overhead Buffer

$4.6K/mo

Fixed overhead is about $4.6K a month before wages, so cash control here protects the Month 8 break-even and the payback path.

HVAC Duct Balancing Service Core Six Income Drivers

Completed Jobs Per Week

Completed Jobs Per Week

This driver is the number of paid completed jobs finished each week. It matters because more jobs spread the $4,600 monthly fixed overhead across more invoices and raise schedule utilization. Count hours too: a 12-hour commercial job is not the same as a 4-hour residential job, so raw job count can hide weak economics.

If lead flow is thin, technicians sit idle and owner pay drops even when the calendar looks full. The goal is paid, billable work that clears direct costs. Once pricing covers labor, travel, and rework, higher weekly completions improve cash flow and the owner’s take-home before tax.

Track Paid Work, Not Activity

Track completed jobs by type, hours, and location. Use a weekly report for paid jobs, billable hours, drive time, and callbacks. That shows whether the team is filling the week with profitable work or just chasing estimates.

Push density by booking jobs in clusters and reserving full days for longer commercial work. If completions rise but profit does not, pricing is too low or labor is too heavy. If the schedule stays light, the fix is lead flow and routing, not faster dispatch.

Count paid jobs only.

Separate residential and commercial hours.

Track travel and callback time.

Watch idle technician days.

1

Average Project Ticket

Average Project Ticket

Your take-home income rises when each job is priced to match the work, not just the visit. For duct balancing, the average project ticket should reflect hours, number of vents, system complexity, reporting, and commercial documentation. If you price a complex job like a simple one, busy weeks can still produce thin profit.

Year 1 examples show the spread: $500 for residential balancing, $2,100 for commercial balancing, $420 for duct leakage testing, and $300 for a performance audit. By Year 5, pricing rises to $145/hour for residential and $195/hour for commercial, so mix matters as much as volume.

Price by Job Complexity

Track billable hours per job, price per service line, and job mix. A 12-hour commercial balancing job should not be priced like a 4-hour residential call. Here’s the quick math: higher-ticket commercial work usually needs more testing, more reporting, and more admin time, so the invoice must cover labor and non-billable paperwork.

Use pricing rules that protect margin: charge more when vent count, documentation, or system complexity rises. Watch for underpricing signals like full schedules but weak cash flow. If average ticket is too low, labor and travel eat the margin, and owner pay gets squeezed even when the crew stays busy.

2

Labor Productivity

Labor Productivity

Labor productivity is how much billable work the crew completes per paid hour. In duct balancing, that matters because the model carries a $65k lead technician and a $45k junior technician, so slow testing or rework turns payroll into lost margin. Faster, accurate testing protects gross margin per job and leaves more cash for owner pay.

The key risk is unpaid labor from poor procedures. If a job needs a repeat visit, the team loses capacity twice: once on the first visit and again on the callback. Track billable-hour ratio, repeat visits, and time spent on testing versus fixing errors, because those inputs decide whether the crew is earning or just staying busy.

Track Billable Hours

Measure billable hours by technician, not just completed jobs. Build a simple standard for airflow checks, documentation, and final signoff so the team can move fast without cutting quality. The goal is fewer unpaid hours and more of each shift tied to invoiced work, which raises profit and the owner’s take-home income.

Watch repeat visits like a margin leak. If training is weak, callbacks eat labor, delay new jobs, and reduce the number of paid appointments the crew can fit in a week. Tight job checklists and faster testing protect cash flow because the same payroll dollars produce more revenue.

3

Route Density

Route Density

Route density is how tightly jobs are grouped by area, so less time gets burned driving and more time gets billed. In this HVAC duct balancing business, travel cost starts at 10% of revenue in Year 1 and improves to 8% by Year 5, so tighter routes directly protect gross margin and owner pay.

Here’s the quick math: clustered appointments raise the billable-hour ratio and cut windshield time (paid time spent driving). Schedule residential calls by zip code and keep longer commercial jobs in full-day blocks. Wide service areas push overtime up, add fuel and maintenance cost, and leave less profit to draw.

Cut Drive Time

Track drive minutes per job, billable hours per day, and fuel plus maintenance as a % of revenue. If drive time rises, you are buying unbillable labor and weakening cash flow. The goal is simple: keep technicians on paid work, not on the road.

Group homes by zip code.

Batch commercial jobs by day.

Watch overtime before it grows.

If the service map gets too wide, margins turn thin fast. A cleaner route plan usually lifts income more than a small price increase, because it protects each paid hour already sold.

4

Callback Rate

Callback Rate

Callback rate is the share of completed balancing jobs that need a return visit. In duct balancing, each callback adds unpaid labor, fuel, and schedule gaps, so a job that looked profitable on the first invoice can still hurt owner income after the fact.

The owner’s take-home drops when repeat visits crowd out billable work. Track callbacks with completed jobs, return-visit hours, miles driven, and root cause by job type. Incomplete diagnostics can erase profit, so close each job with measured airflow, documentation, and final customer signoff.

Cut Repeat Visits

Use callback rate = callbacks ÷ completed jobs and review it by technician and service type. A high rate usually means weak testing, rushed documentation, or bad handoff at closeout. Fix the step that creates the repeat visit, not just the symptom.

Protect margin by making every return visit visible in the job file, then compare it to labor hours and route cost. If callbacks rise, forecast lower paid capacity and lower owner draw. Better airflow readings and signed completion notes keep revenue quality higher.

5

Overhead And Reserves

Overhead and Reserves

When fixed costs are already $4,600 per month before payroll and marketing, owner pay only works if the service can cover that base first. Here’s the quick math: $2,500 rent + $600 insurance + $350 software + $450 utilities and internet + $200 calibration + $500 accounting and legal. Treat EBITDA as profit on paper, not cash you can spend yet.

Capex (big purchases that last more than one year) also hits cash hard: a $45k service van and $367k of tools and setup items. If reserves and reinvestment come first, the owner avoids starving the business for working cash. What this estimate hides: payroll, marketing, and replacement timing can push actual cash needs higher than the monthly overhead line.

Protect Cash Before Owner Draw

Track overhead as a monthly cash rule, not just a P&L line. Keep a simple log for rent, insurance, software, utilities, calibration, and professional fees, then add planned capex and reserve needs before any draw. If EBITDA looks healthy but cash is tight, the business still can’t safely pay the owner.

$4,600 fixed overhead monthly

$45k van, $367k tools/setup

Separate reserves from profit draws

Fund replacement before owner pay

6

HVAC Duct Balancing Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high owner-income planning cases

Owner income scenarios

Owner income changes with mix, crew size, and marketing efficiency. The lean case shows a Year 1 ramp, while the base and high cases show what larger commercial volume can support.

Compare early ramp, scaled operator, and mature crew income paths.

Scenario

Low Caseearly ramp

Base Casescaled operator

High Casemature crew

Launch model

This is the lower earnings path, where Year 1 ramp and negative EBITDA leave the owner dependent on the modeled GM salary.

This is the modeled middle path, where Year 3 scale supports salary plus profit draw.

This is the stronger earnings path, where Year 5 scale and a larger crew support a bigger owner draw.

Typical setup

Year 1 revenue is $408k with -$30k EBITDA, breakeven lands in Month 8, and the owner may only draw the modeled general manager salary.

Year 3 revenue reaches $1.322M with $443k EBITDA, a larger crew, and a stronger commercial mix that can support owner pay above salary alone.

Year 5 revenue reaches $2.345M with $965k EBITDA, $36k marketing, lower CAC, and a larger technician team.

Cost drivers

Residential-heavy mix

$12k marketing

$150 CAC

4.5 billable hours

one van and fixed overhead

More commercial jobs

$24k marketing

$135 CAC

5.0 billable hours

larger crew

$36k marketing

$125 CAC

5.5 billable hours

larger technician team

commercial-heavy mix

Owner income rangeBefore owner reserves

Modeled salary onlysalary only

Salary plus profit drawsalary plus draw

Salary plus strong drawlarger owner draw

Best fit

Use this to stress-test cash safety during launch and any delay in reaching breakeven.

Use this for a steadier operating plan with more commercial work and clearer owner compensation room.

Use this to test upside if the business reaches mature-year volume, staffing, and commercial mix.

!

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In the researched model, the owner may take the modeled $85k general manager salary if they fill that role, but distributions depend on profit and cash EBITDA is -$30k in Year 1, $202k in Year 2, and $965k in Year 5 before taxes, reserves, debt service, and reinvestment

The model reaches breakeven in Month 8 and payback in 25 months That early period still needs cash because minimum cash is $796k in Month 2 The first-year EBITDA is -$30k, so owner draws should stay conservative until job volume and collections stabilize

Yes, the model includes dedicated tools and calibration costs Startup capex includes a $45k service van, $85k precision air multimeters, $12k commercial flow hoods, and a $45k duct blaster system It also budgets $200 per month for equipment calibration services

Residential work starts as 70% of the mix in Year 1 and falls to 50% by Year 5, while commercial balancing rises from 15% to 35% Commercial jobs use 12 billable hours at $175 per hour in Year 1, compared with residential at 4 hours and $125 per hour

Protect owner pay by pricing to the scope, clustering routes, controlling callbacks, and keeping overhead in line with completed jobs Year 1 variable costs total 26% of revenue, including 10% vehicle fuel and maintenance Fixed overhead is $4,600 per month before payroll, marketing, reserves, and taxes

About the author

Liam Foster

Business Idea Researcher

Liam Foster is a business idea researcher at Financial Models Lab, focused on the revenue and profit basics that early-stage founders need when preparing a simple business plan. He helps simplify business plans for non-finance readers by turning business model overviews into clear, practical insights. With a simple, confident approach, Liam breaks down revenue, expenses, and profit in a way that makes financial thinking easier to understand and use.

Choosing a selection results in a full page refresh.