How Much Does An Equestrian Center Owner Make? $80k Planning Case

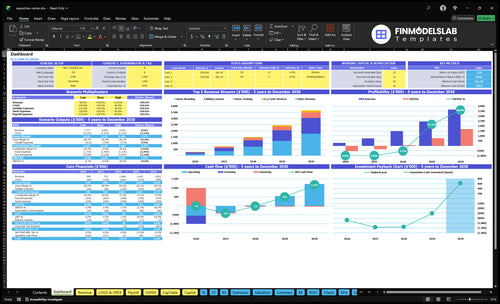

This five-year US planning view covers equestrian center profit from boarding, riding lessons, training, and add-on services The model includes $80,000 owner/operator pay, $455,000 startup capex, and $24,900 monthly fixed overhead, before personal taxes or guaranteed distributions

Owner income$80kNet margin-57% to 14%Revenue for target pay$946k-$1.17mBusiness difficultyHard

Can this center pay you?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Cash gets tight before the Month 30 trough of about -530000, so keep owner pay flexible.

Yes, an Equestrian Center can support an owner salary, but only if occupancy, lesson demand, and staffing cover the cost base; this model includes an $80k owner/operator wage from Year 1. Check What Is The Current Growth Trajectory Of Your Equestrian Center? because the same plan still reaches -$530k minimum cash in Month 30, so the salary is planned, not guaranteed.

Salary test

Protect $80k owner pay

Fill boarding capacity first

Keep lessons consistently booked

Watch cash through Month 30

Payroll risk

Owner-run can reduce admin load

Burnout can hide true labor cost

Manager-run needs more revenue

Non-owner payroll: $2,975k Year 1 to $530k Year 5

How do occupancy and lesson utilization affect owner income?

Occupancy drives income fast: at $1,200 per month in Year 1 and $1,400 by Year 5, one empty stall means about $14,400 to $16,800 less annual board revenue before care costs. Lesson utilization matters just as much, because lesson packages run $250 to $290 per month and active customers average 40 to 60 billable hours monthly. If stalls sit open or instructors sit idle, payroll and overhead stay put while income drops.

Occupancy impact

Year 1 board: $1,200 monthly

Year 5 board: $1,400 monthly

One stall: $14,400-$16,800 yearly

Care costs reduce margin further

Lesson utilization impact

Lesson packages: $250-$290 monthly

Active clients: 40-60 billable hours

Idle instructors still hit payroll

Reserve for weather and cancellations

Which costs most reduce equestrian center owner income?

If you’re trying to see what cuts into Equestrian Center owner income most, it’s the horse-care stack plus payroll. For a deeper cost view, see How Much Does It Cost To Open, Start, Launch Your Equestrian Center Business? Horse care alone — feed, hay, bedding, veterinary, farrier, tack, and equipment maintenance — runs at 200% of revenue in Year 1 and 160% by Year 5, before adding the rest of the business.

Horse-care costs

200% of revenue in Year 1

160% of revenue by Year 5

Feed, hay, bedding drive cost pressure

Veterinary and farrier add more drag

Overhead and payroll

Variable operating costs add 85% in Year 1

They still add 62% by Year 5

Fixed overhead is $249k per month

Payroll reaches $610k per year

Equestrian Center Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What drives owner take-home most?

1

Stall Occupancy

$144K-$168K

An empty stall can mean about $144K-$168K less annual revenue, so occupancy sets pre-tax owner take-home before reserves and extra draws.

2

Board Pricing

$250-$1.4K

Raising lesson and boarding rates from $250 to $290 and $1,200 to $1,400 lifts revenue across the base, and that flows into take-home after direct costs.

3

Lesson Volume

4.0-6.0h

Billable lesson hours per active customer rise from 4.0 to 6.0 a month, so more value comes from each rider without needing a full new client.

4

Training Use

10%-30%

Training mix grows from 10% to 30%, which shifts more revenue into a higher-ticket service and boosts owner take-home.

5

Labor Efficiency

71.5%-77.8%

Contribution margin improves from 71.5% to 77.8%, so tighter staffing and less overtime keep more of each dollar after direct costs.

6

Overhead Control

$25.9K/mo

Fixed costs run about $25.9K a month, so overhead control decides how fast cash reaches the owner after reserves are set aside.

Equestrian Center Core Six Income Drivers

Boarding Stall Occupancy

Boarding Stall Occupancy

Boarding occupancy is the share of stalls filled out of total stalls. It drives recurring revenue and spreads lease, taxes, insurance, utilities, manure removal, and maintenance across more horses. At $1,200 to $1,400 a month, one empty stall cuts annual revenue by $14,400 to $16,800; owner pay only improves after feed, bedding, labor, maintenance, and reserves are covered.

Track Stalls, Churn, and Care Time

Measure occupied stalls, waitlist, churn, and care hours per horse. If churn rises or care time jumps, margin falls fast because the same fixed overhead gets split across fewer boarders. One clean test is to forecast profit at current occupancy and again with one or two empty stalls so you can see the cash flow hit before it shows up in payroll.

Track monthly occupied stalls.

Watch waitlist and churn.

Price for full care costs.

Cap care hours per horse.

1

Board, Lesson, And Training Pricing

Board, Lesson, And Training Pricing

Pricing is the fastest revenue lever because it raises monthly income per horse and per rider without adding another stall or lesson slot. Moving board from $1,200 to $1,400 adds $2,400 per horse per year; lessons from $250 to $290 add $480 per rider per year; training from $600 to $700 adds $1,200 per client per year.

What matters is mix, not just sticker price.Attach rate means how many clients buy a second service, and that lifts revenue per client when board, lessons, training, and a la carte services stack together. But if higher rates hurt retention, the gain can vanish fast, and owner pay only improves when extra revenue beats added care and labor.

Track mix, then move rates

Track revenue per boarded horse and per rider source, plus attach rate for lessons, training, and a la carte add-ons. Here’s the quick math: a $200 board increase, $40 lesson increase, and $100 training increase each lift annual revenue in a straight line, but only if churn stays low.

Boarded horses and rider counts

Lesson, training, add-on attach rates

Care, labor, and arena time per client

Churn, renewals, and waitlist depth

Test price changes on new clients first, then renewals. Watch churn, waitlist depth, and service hours per client; if demand softens or care load rises faster than cash, hold rates flat. The clean rule is simple: raise prices only when local market, care quality, trainer reputation, and facility condition support the higher net margin.

2

Lesson Program Volume

Lesson Volume

Lesson revenue comes from lesson count, lesson mix, and price. At $250 to $290 per month, each active rider adds $40 more revenue, or about 16%. If the calendar has open slots, instructor time, arena time, and payroll still cost money, so empty lessons hit margin and owner pay fast.

The real limit is schedule quality, not just more riders. Active customers can average 40 to 60 billable hours monthly, but only if school horses, tack, and insurance can support that load. Push horses too hard and vet costs, replacement risk, and reputation damage rise before the extra revenue reaches the owner.

Fill the Schedule, Not Just the Barn

Track fill rate, cancellation rate, instructor utilization, and billable hours per horse. Here’s the quick math: monthly lesson revenue = active customers × price. A move from $250 to $290 helps, but better schedule density helps more when payroll and arena time are already fixed.

Watch no-shows by time slot.

Cap school horse hours.

Use waitlists to refill gaps.

Rotate horses before fatigue shows.

Protect the school herd. Overworked horses create hidden costs that cut take-home income through more care spend, more cancellations, and weaker rider trust. If onboarding is slow or make-up lessons pile up, revenue gets less recurring and cash flow gets choppier.

3

Training And Premium Programs

Premium Training Revenue

Training adds higher-margin revenue on top of boarding when clients buy $600 to $700 monthly packages, plus clinics, camps, and specialty coaching. In your assumptions, training allocation rises from 100% to 300%, so this line can move fast. The win is real only if trainer capacity, horse availability, and schedule fill stay tight.

Here’s the quick math: more training hours raise sales, but they also raise incremental payroll, insurance, arena wear, equipment use, and admin time. If those costs climb faster than package revenue, owner pay gets squeezed even when top-line revenue looks strong.

Protect Training Margin

Track sold packages, trainer hours, horse hours, and the full cost per session. Price by capacity, not hope. If clinics or camps need extra staff or more arena time, bake that into the rate before you sell it.

Watch three breakpoints: trainer reputation, horse count, and booking density. A full calendar with weak margins still hurts cash flow. One clean rule: if a new premium client needs more labor than a standard client, their price should cover it.

Measure fill rate by trainer.

Track cost per booked hour.

Limit overuse of school horses.

Count admin time in the rate.

Review capacity before adding camps.

4

Labor Efficiency And Owner Role

Labor Efficiency and Owner Pay

Labor efficiency is the main take-home lever here. The model shows total payroll moving from $3775k in Year 1 to $610k in Year 5, with $80k tied to the owner/operator role and non-owner payroll rising from $2975k to $530k. Owner hours can protect cash early, but only if they don’t mask weak profit.

This driver includes barn care, lesson coverage, training support, and admin time. Here’s the quick math: if the owner replaces too many paid roles, reported margin looks better than the real business, and burnout risk goes up fast. Separate owner working wages from business profit, then pay distributions only after labor is fully covered.

Track Hours by Role

Track labor by function each week: lessons, horse care, training, and admin. Compare owner hours to non-owner payroll at $530k by Year 5, and keep the $80k owner role in the model as a real cost, not free labor. That makes cash flow and owner pay easier to trust.

Log hours by job.

Cap owner fill-in shifts.

Test staffing before growth.

5

Facility Overhead And Maintenance Reserves

Facility Overhead And Maintenance Reserves

When overhead is mostly fixed, every empty stall and slow month hits owner pay fast. The model shows $249k/month in facility overhead, including $15k lease or mortgage, $25k property taxes, $15k insurance, $3k utilities, $1k manure removal, and $12k maintenance. That is about $2.988M a year before owner pay.

Deferred repairs can make reported profit look better than cash reality. The $455k build for stalls, fencing, arena footing, horses, equipment, systems, and inventory means wear will keep showing up, so the owner needs a reserve before taking draws. One clean rule: if the next fix protects safety, horse care, or uptime, it belongs in cash planning now.

Track The Repair Reserve

Measure fixed overhead as a share of monthly revenue and keep a separate reserve for repairs and replacements. If revenue drops, that reserve is what keeps the business from paying the owner with borrowed cash. The key inputs are occupied stalls, lesson and training sales, actual repair spend, and the timing of big replacements.

Log every repair by asset.

Age stalls, footing, and systems.

Forecast 12 months of upkeep.

Fund reserves before owner draws.

Watch for the cash gap between profit and upkeep. A month can look healthy on paper while footing, fencing, and equipment still need work. If reserve funding slips, the owner’s pay becomes the shock absorber, and that’s when maintenance gets deferred and the next month gets more expensive.

6

Equestrian Center Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income cases

Owner income scenarios

Owner pay changes fast here because fixed costs and payroll are heavy before the barn fills. The scenarios show when pay may be paused, covered, or supported by reserve-backed distributions.

Low, base, and high owner pay cases for an equestrian center.

Scenario

Low CaseCash is tight

Base CaseSalary covered

High CaseReserve-backed upside

Launch model

Lower earnings path with thin margin and tight cash.

Modeled operating case with steady owner salary coverage.

Stronger earnings path after breakeven and cash build.

Typical setup

Year 1 revenue stays below about $834k, and cash can fall to about -$530k by Month 30, so owner pay may be paused or partial.

About $946k Year 1 revenue covers fixed costs, payroll, variable costs, and the $80k owner/operator role, with breakeven around Month 30.

Higher volume and a better service mix cover the $80k owner/operator role and can support reserve-backed distributions after core obligations are funded.

Cost drivers

Low fill rate

heavy payroll

fixed facility costs

owner pay deferral

weak cash buffer

Balanced lesson mix

boarding growth

full owner salary

standard staffing

breakeven timing

Higher boarding mix

stronger training revenue

better pricing

lower CAC

reserve build

Owner income rangeBefore owner reserves

No pay to partial payCash first

$80,000 salaryCore salary

Reserve-backed distributionsUpside case

Best fit

Use this to stress-test slow demand, weak conversion, or a long ramp to breakeven.

Use this as the working plan if demand is steady and the schedule fills as modeled.

Use this to test upside after breakeven when cash reserves and funding terms can support extra owner draws.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In this planning case, the owner/operator role is set at $80,000 pre-tax per year That pay is not guaranteed because the model also shows a -$530,000 minimum cash position in Month 30 Extra draws should wait until the center covers payroll, $24,900 monthly fixed overhead, care costs, and reserves

Owner draws depend on cash flow, not just sales This model reaches its lowest cash point in Month 30, even with an $80,000 owner/operator wage included That means early profits should likely fund working capital, repairs, debt service if used, and horse-care reserves before discretionary distributions

Boarding helps because it creates recurring monthly revenue In the assumptions, boarding rates run from $1,200 to $1,400 per month, while lesson packages run from $250 to $290 Lessons can scale, but boarding spreads the $24,900 monthly fixed overhead across occupied stalls and reduces reliance on seasonal lesson volume

Occupancy, lesson utilization, payroll, facility debt, and reserves drive owner pay One empty boarding stall can reduce annual revenue by $14,400 to $16,800 before care-cost savings Payroll also matters because staffing rises from $377,500 in Year 1 to $610,000 in Year 5, including the owner/operator role

Start with break-even revenue before owner draws In Year 1, the model needs about $834,000 to cover non-owner payroll, fixed overhead, and variable costs before owner pay Adding the $80,000 owner role lifts the target to about $946,000, using a 715% contribution margin

About the author

Paul Wells

Practical Finance Writer

Paul Wells is a practical finance writer for Financial Models Lab who focuses on cost-to-open estimates and monthly expense breakdowns that help founders avoid common launch mistakes. He simplifies business plans for non-finance readers and brings a grounded, founder-minded perspective to startup cost research.

Choosing a selection results in a full page refresh.