How Much Does a Fencing Academy Owner Make? $616k EBITDA Case

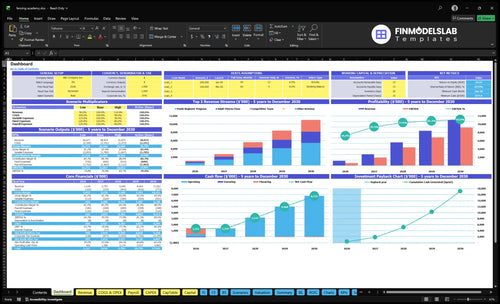

Using the researched assumptions, a fencing academy can support owner income once recurring enrollment, coach coverage, and facility use cover fixed overhead and payroll In the model, EBITDA is $616k on $1134M revenue in Year 1, or a 543% EBITDA margin By Year 5, EBITDA reaches $9212M on $11022M revenue, or an 836% margin Owner take-home is not the same as revenue or EBITDA it includes salary plus any distributions left after taxes, reserves, debt service, and reinvestment

Owner income$616kNet margin54% to 84%Revenue for target pay$157kBusiness difficultyMedium

Want to test your fencing academy income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How many students does a fencing academy need to support owner income?

A Fencing Academy should not use one universal student target; the working range starts at about 68 active fencers and becomes stronger at 216 active fencers when occupancy is high. For startup cost context, see How Much To Start Fencing Academy Business?; owner income gets realistic only after recurring tuition covers the $10k/month fixed overhead before payroll, plus coaches, marketing, equipment, and reserves.

Base Student Count

150 planned places at launch

45% occupancy target

150 × 45% = 67.5

About 68 active fencers

Owner Pay Test

240 planned places by Year 5

90% occupancy target

240 × 90% = 216 active fencers

Tuition must cover payroll and reserves

Does owner-operated coaching change fencing academy income?

Owner-operated coaching can lift early margin at a Fencing Academy because it can replace an $85k head coach cost, but it also ties growth to the owner’s hours. Once classes expand, the model needs more assistant coaches, tighter scheduling, and more work on sales, retention, and partnerships. It is not passive income, because safety, coach quality, and student retention still need daily management.

Owner-led margin

Removes the $85k head coach line.

Protects margin in early classes.

Helps if owner can teach well.

Works best at smaller scale.

Growth pressure

Assistant coaches grow from 10 FTE to 30 FTE.

Admin support grows from 0.5 FTE to 1.0 FTE.

Every new class can add owner hours.

Scheduling and safety still need oversight.

What fencing academy expenses reduce owner take-home most?

For a Fencing Academy, the biggest hit to owner take-home is the $10k in monthly fixed overhead plus payroll, so the first cut should be rent and staffing, not student pricing. If you’re mapping the launch path, How To Launch Fencing Academy? is the right place to line up those early costs. Here’s the quick math: payroll is $158k in Year 1 and $283k in Year 5, merchant fees stay at 30%, and early ramp-up capex totals $82k.

Fixed monthly drag

$7,500 lease each month

$950 utilities and internet

$550 insurance

$250 software, $600 cleaning, $150 affiliation

Variable cost pressure

Equipment inventory falls from 60% to 40%

Marketing falls from 80% to 30%

Merchant fees stay at 30%

Capex totals $82k early on

Fencing Academy Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What drives fencing academy owner income?

1

Active Enrollment

$1.1M-$11.0M

Keeping 150 to 240 planned places full drives the biggest top-line swing and protects owner take-home.

2

Revenue Mix

$150-$380

Shifting more volume into higher-priced programs lifts revenue per student without adding space.

3

Facility Utilization

45%-90%

Moving occupancy from 45% to 90% turns the same floor time into more billable hours and better margin.

4

Coaching Labor

$158K-$283K

Payroll rising from about $158K to $283K makes coach scheduling a direct profit lever.

5

Beginner Pipeline

80-120

The youth beginner flow seeds future upsells and keeps higher-value classes from going empty.

6

Overhead Control

$10K/mo

Holding fixed overhead near $10K a month preserves cash because these costs hit profit before owner pay.

Fencing Academy Core Six Income Drivers

Active Student Enrollment And Retention

Active Student Enrollment And Retention

Recurring enrollment is the income engine here. Revenue depends on how many youth, competitive, and adult students stay active, because planned places rise from 150 in Year 1 to 240 in Year 5 and occupancy rises from 45% to 90%. Better retention lifts tuition stability, keeps classes full, and protects owner draw. Weak retention leaves empty places and makes each new student cost more to replace.

Here’s the quick math: more active students spread fixed coaching, rent, and admin over more tuition dollars, so gross margin and cash flow improve. The risk is hiring coaches and adding floor time before enrollment supports them, which can push payroll up faster than revenue. One clean rule: do not add capacity until retention and fill rate prove the seats will stay paid.

Retention And Fill-Rate Control

Track active students, churn, trial-to-member conversion, and monthly occupancy by program. Split the data by youth, competitive, and adult groups so you can see which segment is leaking revenue. If occupancy is still below 45%, focus on re-enrollment, make-up classes, and beginner follow-up before spending more on ads.

Set a simple target for each class block: keep seats filled enough that tuition covers coaching time with room for owner pay. Test reminders, attendance checks, and short retention offers for students who miss two sessions in a row. If fill rate improves, marketing as a share of revenue should fall and take-home income should rise.

1

Pricing, Membership Structure, And Revenue Per Student

Revenue Per Student

Revenue per student starts with the monthly tier. Youth tuition moves from $180 to $220, competitive team from $320 to $380, and adult fitness from $150 to $190. That lifts monthly revenue by $40, $60, or $40 per member before lessons, gear, or camps. More revenue per fencer gives the owner more room for coach pay, rent, and draw.

But price only helps if retention stays strong. Higher revenue per student can come from class frequency, private lessons, equipment packages, and camps, but weak outcomes or thin demand can raise churn and marketing spend. The real test is simple: does the new price raise monthly cash without hurting fill rate or repeat attendance?

Price By Tier, Not By Guess

Track monthly revenue per active student, tier mix, lesson attach rate, package sales, camp sign-ups, and churn. Revenue is usually tuition + add-ons - discounts, so the owner should know which offers actually raise take-home income and which ones just add work.

Use the price moves as a check on demand. Youth pricing rises 22.2% from $180 to $220, competitive team rises 18.8%, and adult fitness rises 26.7%. Do not raise prices blindly; match them to coach quality, local demand, retention, and training outcomes. If conversion or renewal slips after a change, the market is telling you the price is too high.

Measure revenue per active fencer.

Watch churn after each price change.

Track private lesson attach rate.

Test camp and gear package sales.

2

Facility Utilization And Schedule Capacity

Facility Utilization

Utilization turns rent into revenue. If planned places rise from 45% in Year 1 to 90% in Year 5, the same floor can carry much more tuition without a rent jump. With billable days moving from 24 to 26 per month, that is about 8% more sellable schedule time, which lifts gross margin and leaves more cash for owner pay.

Schedule Capacity Checks

Track booked slots, attendance rate, billable days, and revenue per square foot. Test evening classes, weekend clinics, and camp periods, since they add high-value hours without adding rent. The goal is fuller strips and cleaner flow, not packed rooms. Overcrowding can hurt safety and retention, which then pushes coach time up and cash flow down.

Measure fill by session and daypart.

Watch safe strip spacing.

Price peak slots higher if demand holds.

3

Coaching Labor Model And Owner Teaching Capacity

Coach Payroll and Owner Teaching Load

Payroll is the big margin lever here. The model shows a $85k head coach salary, assistant coach cost rising from $52k at 10 FTE to $156k at 30 FTE, and admin cost rising from $21k to $42k. If enrollment and lesson volume do not cover that jump, gross profit falls fast and the owner’s pay gets squeezed.

Owner teaching can save cash, but only if owner time is priced honestly. If the owner is filling coach hours that could have been sold or delegated, the “savings” may be fake. Specialized coaches can support a stronger competitive program, but they need enough students and enough billable lessons to justify their labor cost.

Track Teaching Capacity Against Demand

Measure student count, lesson hours, coach load, and owner teaching hours every month. Here’s the quick math: if payroll rises before enrollment, retention, and private lessons rise too, owner draw gets hit first. Build staffing from booked hours, not hope.

Use a simple rule: add assistant coaches only when class fill, private lessons, and competitive-team volume can pay for them. If owner teaching is needed to stay open, price that time as a real labor cost, not free labor. That keeps the model honest and protects cash flow.

4

Beginner Pipeline, Youth Programs, And Camps

Beginner Pipeline

Beginner classes are the front door to recurring tuition. This driver works only if leads turn into trials, trials into members, and members into repeat buyers of private lessons, camps, and team spots. Planned places rise from 80 to 120 youth, 30 to 60 competitive, and 40 to 60 adult, so fill rate matters more than top-line traffic.

Early growth is expensive because marketing starts at 80% of revenue and should fall toward 30% as retention improves. If that drop does not happen, owner pay gets squeezed even when classes look busy. What this hides: weak trial conversion or fast churn can make every new lead cost more than the student is worth over time.

Track Leads to LTV

Track three numbers monthly: lead-to-trial rate, trial-to-member rate, and member lifetime value. Lifetime value means the total tuition and add-on revenue one student brings before they leave. Compare it with marketing cost per member so you know if growth is paying back cash, not just adding enrollments.

Count leads by source.

Log trials by age group.

Watch churn after 60 days.

Price camps for repeat signups.

Protect team spots first.

If youth fills faster than adults, shift spend and class times there. If competitive spots convert better, hold a higher bar for entry and keep coaching hours tied to the most profitable students. The goal is not more sign-ups alone; it is more recurring revenue per square foot and lower cash burn each month.

5

Overhead, Equipment, Insurance, And Reserves

Overhead, Equipment, Insurance, And Reserves

This driver is the academy’s $10,000 monthly fixed overhead before payroll: $7,500 lease, $950 utilities, $550 insurance, $600 cleaning, $250 software, and $150 affiliation. Add the $82,000 early capex for strips, scoring gear, rental gear, buildout, signage, and office tech, and cash pressure shows up fast even if EBITDA looks healthy.

Owner pay depends on what’s left after replacements and reserves. If gear wears out or the room needs refreshes, distributable cash falls before profit does. One clean rule: EBITDA is not spendable cash when the business must keep equipment safe, insured, and current.

Control Fixed Cash Burn

Track overhead as a share of monthly revenue, then compare it to class occupancy and tuition collected. Here’s the quick math: the listed fixed items total $10,000 per month, so every weak month hits cash hard before any coach pay. Keep a reserve for equipment replacement instead of treating all surplus as owner draw.

Measure wear on strips, scoring gear, and rental gear, and forecast replacement before failure. If cash planning ignores the $82,000 buildout and refresh cycle, EBITDA can look strong while the owner still has to skip pay to fund repairs, insurance, or a new tech purchase.

6

Fencing Academy Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high fencing academy owner-income cases

Owner income scenarios

Owner income moves with class occupancy, program mix, and pricing. EBITDA rises fast as the academy fills, but payroll and fixed overhead still cap what reaches the owner.

Low, base, and high cases for owner take-home capacity.

Scenario

Low CaseLean case

Base CaseBase case

High CaseUpside case

Launch model

This is the lower earnings path with slower fill and tighter owner draw.

This is the modeled middle path with steady demand and a normal owner draw.

This is the stronger earnings path with near-full classes and the largest owner draw.

Typical setup

Year 1 uses 150 places at 45% occupancy, with $1.134M revenue, $616k EBITDA, $158k payroll, and about $120k fixed overhead.

Year 3 scales to 230 places at 75% occupancy, with $5.640M revenue, $4.391M EBITDA, $231k payroll, and about $120k fixed overhead.

Year 5 reaches 240 places at 90% occupancy, with $11.022M revenue, $9.212M EBITDA, $283k payroll, and about $120k fixed overhead.

Cost drivers

Occupancy

youth enrollment

tuition pricing

payroll

fixed overhead

Occupancy

program mix

tuition pricing

assistant coach staffing

fixed overhead

Near-full occupancy

premium pricing

team growth

equipment sales

coach staffing

Owner income rangeBefore owner reserves

$85k + limited drawLean income

$85k + steady drawCore income

$85k + larger drawUpside income

Best fit

Use this to stress-test cash needs if classes fill slowly.

Use this as the main planning case for a stable operating year.

Use this to test upside if demand stays strong and add-on sales hold.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In this planning model, the academy produces $616k EBITDA on $1134M revenue in Year 1 and $9212M EBITDA on $11022M revenue in Year 5 Owner income may include the $85k head coach salary plus distributions Taxes, reserves, debt service, and reinvestment come out before cash is truly spendable

The model shows break-even in Month 1 and payback in Month 1, but that depends on hitting the launch assumptions Year 1 includes 45% occupancy, $1134M revenue, and $10k monthly fixed overhead If enrollment ramps slower or coach payroll starts early, owner pay can be delayed

You don’t have to, but it changes the math The model includes a $85k head coach role, one assistant coach in Year 1, and 05 administrative FTE If you teach, you may capture salary as owner income If you hire out coaching, you gain scale but carry more payroll risk

Occupancy, coach payroll, and fixed rent usually move the margin most This model moves from 45% to 90% occupancy, while fixed overhead stays at $10k per month Payroll rises from $158k to $283k, but revenue grows from $1134M to $11022M, which expands EBITDA margin

The best mix is recurring tuition first, then add-ons that do not overload coach hours Youth tuition starts at $180 per month, competitive team pricing at $320, and adult fitness at $150 Equipment sales rise from $1,200 to $4,000, but memberships and filled classes usually create steadier owner income

About the author

Gregory Ford

Launch Planning Specialist

Gregory Ford is a launch planning specialist at Financial Models Lab who helps first-time entrepreneurs judge whether a business idea is financially realistic. He focuses on operating cost estimates and turns broad business questions into clear planning assumptions and practical next steps. Gregory writes about opening and running small businesses in a straightforward, easy-to-understand way.

Choosing a selection results in a full page refresh.