How Much Feng Shui Consulting Owners Make: $85k Pay, $0 Profit

Feng Shui Consulting Service Bundle

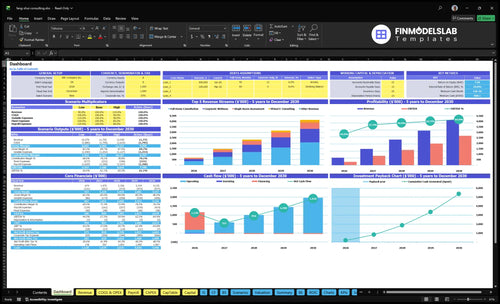

You’re trying to see whether a US feng shui consulting service can pay the owner from real client work, not just show revenue Using the researched first-year model, revenue is $112,400, modeled lead consultant pay is $85,000, and operating profit is negative after staff, marketing, fixed costs, and delivery costs This is planning math, not tax, legal, debt, benefits, or compensation advice

Owner income$7.1k/moNet margin-764% to -203%Revenue for target pay$674kBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Taxes, financing, and personal spending are outside the calculator.

Increase income by selling more full-home and corporate packages, because they carry larger project values than virtual work. Use virtual sessions to cut travel and support load, but not as the main revenue mix. CAC drops from $150 in Year 1 to $120 in Year 5, a 20% improvement, so referrals and local search need to stay efficient. Watch payroll creep: Year 5 payroll reaches $322,500, so add admin or junior support only when it lifts paid capacity more than it costs.

Raise project value

Sell full-home packages first.

Push corporate work for bigger tickets.

Use virtual only for lighter jobs.

Shift mix toward high-value projects.

Protect margin

Lower CAC from $150 to $120.

Lean on referrals and local search.

Track payroll at $322,500 in Year 5.

Hire only when capacity rises more.

What feng shui consulting business expenses reduce owner take-home?

Owner take-home gets squeezed mostly by payroll and overhead, not by delivery costs alone; see What Are Operating Costs For Feng Shui Consulting Service?. In year 1, variable costs are 29% of revenue, and fixed costs include $3,850 per month in overhead, $12,000 in marketing, and $107,500 in payroll, so higher sales do not turn into owner income one for one.

Main cost drains

15% contractor consultant fees

3% materials and report printing

6% travel costs

5% referral commissions

Owner take-home impact

$46,200 yearly fixed overhead

$85,000 lead consultant role

0.5 admin coordinator adds payroll load

Low delivery costs still don’t save margin

How much should a feng shui consultant charge?

For Feng Shui Consulting Service, charge by deliverable, client segment, credentials, and close rate, not a generic hourly target. In Year 1, the pricing math supports $150/hour for full home work, $175/hour for a single room, $125/hour for virtual consulting, and $200/hour for corporate wellness, which maps to $1,800, $700, $375, and $4,000. By Year 5, rates can move to $175, $200, $150, and $250 per hour, but higher prices only work if conversion and referrals hold.

Year 1 pricing

$150/hour full home work

$175/hour single room work

$125/hour virtual consulting

$200/hour corporate wellness

Package math

$1,800 full home package

$700 single room package

$375 virtual package

$4,000 corporate package

Feng Shui Consulting Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Pricing

$1.4K

Planning case only: higher rates lift revenue per hour and push take-home up fast.

2

Booked Volume

80 cust

More booked clients spread the $46.2K fixed base and add profit after CAC.

3

Operating Costs

$46.2K

The fixed base and variable fees eat owner profit if they creep up.

4

Owner Capacity

$85K

The modeled owner role pay is the ceiling until work is delegated and hours stay billable.

5

Service Mix

40/30/20/10

A bigger share of virtual and corporate work changes hours, price, and margin.

6

Lead Conversion

$150 CAC

Lower CAC turns the $12K marketing budget into more booked work and better cash.

Feng Shui Consulting Service Core Six Income Drivers

Pricing And Average Project Value

Project Pricing and Average Value

Pricing matters here because each client is time-heavy, so revenue per project has to carry delivery work and owner pay. The current mix gives a weighted average project value of $1,405 from 40% full home at $1,800, 30% single room at $700, 20% virtual at $375, and 10% corporate at $4,000.

Higher fees lift income only if they do not weaken conversion or referral flow. If price rises but CAC (customer acquisition cost) stays flat and referrals hold, owner profit improves. If price climbs and close rates fall, booked work drops fast because the business is service-heavy and each lost sale removes both revenue and future referral value.

Track Mix Before Raising Rates

Measure project mix, close rate, referral volume, and CAC together. One clean test is to raise the fee on the most time-heavy package first, then watch whether booked projects and referral leads stay steady over 30 to 60 days.

Track average project value monthly.

Separate home, virtual, corporate.

Watch conversion after each price change.

Keep referrals from dropping.

Clear deliverables can support a higher fee because clients see what they get. The risk is simple: if a higher price trims close rate, average project value may rise on paper but monthly take-home income can still fall.

1

Monthly Booked Client Volume

Monthly Booked Client Volume

Monthly booked client volume is the number of paid projects closed each month. With $12,000 in marketing and $150 CAC (customer acquisition cost), the model supports 80 first-year customers. That is the volume engine behind owner pay: if bookings stay below that pace, revenue may not cover labor, admin, and overhead.

Here’s the quick math: break-even needs about 166 first-year customers at the same project value and cost structure. This driver is capped by capacity, since full home work takes 12 billable hours and corporate work takes 20. Seasonal demand, follow-up, report writing, and travel can cut paid utilization fast.

Track Bookings Against Capacity

Measure booked clients by month, by service type, and by source. Compare bookings to available billable hours, not just lead count. If the mix shifts toward full home or corporate work, volume may look fine while capacity runs out, and owner draw still gets squeezed.

Keep a simple control sheet: inquiries, close rate, CAC, billable hours per job, and paid utilization. If bookings rise but utilization falls, the business is buying growth that does not reach take-home pay. A steady monthly target beats a spike that overloads admin and travel.

2

Residential, Virtual, And Commercial Mix

Service Mix and Owner Pay

Service mix changes owner income because each booking has a different ticket and time load. A $1,800 full-home job takes 12 billable hours ($150/hour), a $700 single-room job takes 4 hours ($175/hour), a $375 virtual job takes 3 hours ($125/hour), and a $4,000 corporate job takes 20 hours ($200/hour) before direct costs.

Virtual grows from 20% of customers in Year 1 to 35% in Year 5, so travel may fall but average revenue per client can drop if volume does not rise. Corporate stays at 10%, and it brings the highest project value, but it also comes with more expectations and more owner time. The key test is simple: does each mix choice raise cash left after labor and travel?

Track Revenue per Owner Hour

Track mix by revenue, billable hours, and travel time, not just customer count. If virtual bookings fill weak weeks, they can help cash flow; if they replace higher-value home or corporate work, owner pay falls. Use a monthly scorecard for revenue per owner hour and compare each service type on the same basis.

Set a minimum $ per hour by service.

Protect $4,000 corporate slots.

Use $375 virtual to fill gaps only.

3

Lead Generation And Conversion

Lead Conversion and CAC

Lead generation only pays when inquiries turn into paid consultations at a cost below contribution profit. Here, CAC (customer acquisition cost) drops from $150 in Year 1 to $120 in Year 5, while annual marketing spend rises from $12,000 to $35,000. That can lift volume, but it also raises the risk of buying low-quality leads.

The model implies customers rise from 80 to 2,917, so owner income depends on close rate, average project value, and how much referral work costs. Referrals at 5% of revenue are not free. If a lead source cannot beat that cost after follow-up, it cuts cash flow and owner pay.

Track source, close rate, and payback

Measure inquiry source, close rate, CAC, and average project value on the same dashboard. Here’s the quick math: if spend rises but consultations do not close, marketing becomes overhead, not growth. Track paid consultations separately from free inquiries, and cut any source where 5% referral fees or ad spend push CAC above contribution profit.

Test one change at a time: message, offer, or follow-up speed. If the same source brings more leads but lower-priced work, owner income can still fall. The goal is simple: fewer wasted inquiries, higher conversion, and a lead mix that funds payroll, overhead, and a profit draw.

4

Operating Costs And Margin

Operating Costs and Margin

Fixed overhead and payroll decide how much consulting revenue reaches owner pay. Here that means $3,850 a month in shared studio rent, insurance, software, utilities, accounting, legal, and marketing tools, plus payroll rising from $107,500 to $322,500. Variable costs start at 29% of revenue and improve to 23% by Year 5, so margin only improves if support costs stay tied to booked work.

The key inputs are revenue, variable cost rate, fixed overhead, and payroll. If support is hired before client volume covers it, margin can turn negative fast, and owner income gets squeezed even when sales grow. The quick math is simple: revenue has to pay its share of overhead first, then payroll, then owner draw.

Track margin before you hire

Watch monthly gross margin after variable costs, then compare it with fixed overhead and payroll. A clean check is whether current client volume covers $3,850 in overhead plus the next payroll step. If not, delay hiring and use part-time or contractor help so owner pay comes from profit, not cash strain.

Build a monthly forecast with revenue, variable cost %, payroll, and fixed costs. Recheck it when the mix changes, because variable costs fall from 29% to 23% over time, but that gain disappears if staff costs jump too soon. Track operating margin and cash flow together, since paper profit does not pay the owner if payroll lands first.

5

Owner Capacity And Delegation

Owner Capacity And Delegation

Owner capacity is the hard cap on how many paid consults the business can deliver, because each job also needs prep, visits, reporting, and follow-up. In this model, a full home takes 12 billable hours, a single room takes 4, virtual takes 3, and corporate takes 20, so the real input is not demand alone but paid output per owner hour.

Delegation can lift revenue, but it also adds payroll before profit shows up. Admin support starts at 0.5 FTE and junior consultant support begins in Year 2 at 0.5 FTE, so the owner needs enough booked work to cover those wages plus fixed overhead before take-home income improves.

Track paid output per owner hour

Measure booked jobs, service mix, and owner hours each month. The key test is whether templates, workshops, and follow-up sessions raise billable hours per owner hour instead of just adding admin. If a service takes more time than it earns, the owner gets busier but not richer.

Use delegation only after the pipeline can fund it. A simple rule: add support when the owner is spending too much time on prep and reporting, but keep an eye on payroll so the extra 0.5 FTE actually frees enough billable work to cover the added cost.

6

Feng Shui Consulting Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income swings with customer count, project mix, and fixed payroll. The same overhead can keep pay tight until volume clears break-even.

Lean, base, and scale cases show when pay stays tight or opens up.

Scenario

LeanLean

BaseBase

ScaleScale

Launch model

A smaller launch with fewer closes keeps owner income under pressure.

The modeled launch keeps owner pay at salary-only levels.

A stronger launch reaches break-even volume and starts to create room beyond salary.

Typical setup

Fewer customers and a weaker close rate leave the same overhead and payroll to cover a thinner revenue base.

The base model uses 80 first-year customers at $1,405 each, $112,400 revenue, 29% variable costs, $46,200 fixed overhead, $12,000 marketing, and $107,500 payroll, which leaves the modeled $85,000 owner salary with no profit draw.

Volume rises toward 166 customers or $233,400 revenue, which covers the modeled cost base before profit distributions.

Cost drivers

Fewer customers

Lower close rate

Same overhead

Payroll load

Marketing spend

80 customers

$1,405 average project value

29% variable costs

$46,200 fixed overhead

$107,500 payroll

166 customers

$233,400 revenue

Same fixed overhead

Higher utilization

Distribution timing

Owner income rangeBefore owner reserves

Below modeled salaryLean case

Modeled salary onlyBase case

Break-even before distributionsScale case

Best fit

Use this to stress-test slow lead flow, weak conversion, and owner pay pressure.

Use this as the source model and day-one planning anchor.

Use this to test when growth can fund staff and reserves before owner distributions.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Part-time income depends on booked projects, not a fixed wage In the source model, the average first-year project value is $1,405, with full home work at $1,800 and virtual work at $375 A part-time owner with low overhead can keep more cash, but the staffed model shown here loses money despite an $85,000 lead consultant salary

Under the researched assumptions, it does not reach operating break-even during the five-year model First-year break-even revenue is about $233,400, versus $112,400 modeled revenue By Year 5, revenue grows to about $414,896, but payroll also rises to $322,500, so operating profit remains negative

Credentials can help pricing, but the model does not assign a dollar premium to certification What matters financially is whether higher fees hold conversion In Year 1, the model uses $150 per hour for full home work, $175 for single room work, $125 for virtual work, and $200 for corporate wellness

Booked volume, pricing, and payroll timing move profitability the most The first-year model has 80 customers, a $1,405 weighted average project value, and 29% variable costs Still, $46,200 in fixed overhead and $107,500 in payroll create a large operating loss, so hiring pace matters

Reinvest only after the core booking engine works In this model, marketing rises from $12,000 in Year 1 to $35,000 in Year 5, while CAC improves from $150 to $120 Before adding staff or studio costs, test whether each dollar spent lowers CAC, raises project value, or frees paid owner time

About the author

Jonathan Bell

First-Time Founder Guide Writer

Jonathan Bell is a Financial Models Lab writer focused on launch budget planning, helping aspiring small business owners estimate startup needs before opening. As a first-time founder guide writer, he explains business costs in simple language and offers simple launch planning insights that help readers compare business opportunities realistically and make grounded real-world decisions.

Choosing a selection results in a full page refresh.