How Much Fine Dining Restaurant Owners Make At $267k EBITDA

A fine dining restaurant owner can make meaningful money, but take-home depends on how much cash is left after food, beverage, labor, rent, overhead, reserves, and reinvestment In this researched model, Year 1 revenue is about $114M, with $267k EBITDA, or a 234% operating profit proxy before owner distributions By Year 5, revenue reaches about $245M and EBITDA reaches $1057M, but that is not the same as guaranteed owner pay The biggest swing factors are covers, average check, prime cost, staffing, rent, and whether the owner replaces paid labor or acts as an investor

Owner income$267k–$1.06MNet margin23%–43%Revenue for target pay$1.14M–$2.46MBusiness difficultyHard

Want to test your own owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, operating costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, reserves, and how much cash the business can safely keep on hand.

Want to check owner income in the model?

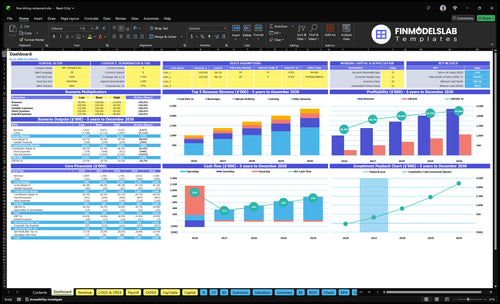

The screenshot shows revenue, EBITDA, owner-income proxy, margin, break-even, payback, and cash charts, with tabs for assumptions; open the Fine Dining Restaurant Financial Model Template.

Owner-income model highlights

$114M Year 1 revenue

$267k Year 1 EBITDA

$784k Month 2 cash floor

3 months to break-even

15 months to payback

What costs affect fine dining restaurant owner income?

If you’re asking what cuts owner income at a Fine Dining Restaurant, start with payroll and fixed costs; see How Much Does It Cost To Open A Fine Dining Restaurant? for the opening budget. In Year 1, payroll is $373k, food ingredients hit 100% of revenue, beverage ingredients are 40%, marketing is 20%, delivery platform fees are 20%, and fixed overhead is $1.296M a year, including $90k rent.

Cash flow hits

Payroll leads at $373k in Year 1.

Payroll rises to $621k by Year 5.

Food ingredients take 100% of revenue in Year 1.

Fixed overhead stays high at $1.296M yearly.

Margin risks

Beverage ingredients still run at 40%.

Marketing and delivery fees each take 20%.

Spoilage and comps cut owner take-home.

Cheap cuts can lower demand, so protect quality.

Does a chef-owner make more from a fine dining restaurant?

A chef-owner can take home more in a Fine Dining Restaurant if they replace a modeled $60k head chef wage, but that is labor pay, not extra owner profit. If the owner also closes management gaps, improves purchasing, and keeps service tight, the business can run better. But an investor-owner still has to fund paid leadership, including the $65k restaurant manager and kitchen payroll, and working more does not always raise net income.

Chef-owner pay

Can replace a $60k head chef role

Raises labor income, not passive profit

Protects service quality on busy nights

Works best if time stays focused

Owner tradeoff

Investor-owner funds a $65k manager

Kitchen payroll still has to be paid

Separate wages from ownership draws

Burnout can hurt consistency and growth

How much does a fine dining restaurant owner take home?

A Fine Dining Restaurant owner does not automatically take home EBITDA; EBITDA is the available-profit proxy before debt service, income taxes, reserves, payroll owner salary, and reinvestment. In this model, Year 1 shows $267k EBITDA on $1.14M revenue, while Year 5 shows $1.057M EBITDA on $2.45M revenue; for more context, see What Is The Most Critical Metric To Measure The Success Of Your Fine Dining Restaurant?.

Owner Take-Home

Use EBITDA, not guaranteed pay

Year 1 EBITDA: $267k

Year 5 EBITDA: $1.057M

Subtract taxes, debt, reserves first

Cash Levers

Payroll Year 1: $373k

Payroll Year 5: $621k

Staffing choices shape distributions

Revenue feels big; cash discipline pays

Fine Dining Restaurant Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What drives fine dining restaurant owner income most?

1

Guest Spend

$22-$32

Midweek checks start at $22 and weekend checks at $32, and a higher tab lifts profit without adding seats.

2

Seat Utilization

770/wk

Year 1 starts at 770 weekly covers, so Friday through Sunday fill rate drives most of the revenue.

3

Prime Cost

47%

Food at 10%, beverage ingredients at 4%, and labor keep the prime cost near 47%, which is the main cash swing.

4

Labor Model

9-16 FTE

Staffing rises from 9 FTE in Year 1 to 16 FTE by Year 5, so every added shift has to earn its keep.

5

Fixed Overhead

$10.8K/mo

Rent, utilities, insurance, and admin costs run about $10.8K a month, which sets the break-even floor.

6

Private Dining

10%

Catering stays at 10% of sales, and larger event bookings help spread fixed costs across more checks.

Fine Dining Restaurant Core Six Income Drivers

Average Guest Spend And Beverage Mix

Average Guest Spend

Average guest spend is the fastest way to lift revenue per cover. In Year 1, modeled AOV is $22 midweek and $32 on weekends, rising to $26 and $36 by Year 5. That extra $4 per guest matters because it lands before labor, rent, or other fixed costs, so higher checks can increase owner pay if service still feels worth it.

Here’s the quick math: every extra $1 of spend adds $1 of revenue per cover. Tasting menus, wine pairings, cocktails, and premium add-ons can push the check up, but they also raise service expectations. If the experience slips, guests may reject the price, and the owner loses both revenue and repeat business.

Price the Check, Not Just the Plate

Track spend by daypart and by add-on. Use these inputs: covers, midweek vs. weekend mix, average check, and beverage attach rate. Beverages are modeled at a 200% sales mix across all five years, so they are a core revenue lever, not an afterthought.

Measure AOV by service period.

Test pairings against guest value.

Watch service speed and complaint rates.

Protect margin with clean pricing.

If premium items raise spend but slow the room or feel forced, cash flow can suffer even with higher sales. Price must match execution, because the owner only keeps the upside after staffing, prep, and service costs stay under control.

1

Covers And Seat Utilization

Covers Drive Demand

Covers are the demand engine. In Year 1, weekly covers total 770, then rise to 1,790 by Year 5. Sunday grows from 220 to 420, while Monday moves from 60 to 120. More covers lift revenue and help spread fixed labor and rent over more checks.

Fine dining can’t chase table turns like casual dining without hurting pacing, service, and reviews. More covers only help owner pay if the room stays full at a pace the kitchen and floor can handle. The model shows revenue rising from $114M to $245M because both covers and average check increase.

Measure Seat Utilization

Seat utilization means how much of the dining room sells across each service window. Track covers by day, no-shows, turn time, and booked-versus-seated counts. Those inputs show whether demand is real cash or just reservations that never land.

Watch Sunday and Monday cover trends.

Price around peak-time demand.

Use deposits for high-risk bookings.

Keep pacing tight enough for reviews.

If cover growth comes with worse service, the revenue gain can vanish in comps, refunds, and weak repeat visits. The best seat plan raises weekly covers without forcing the team to rush the meal.

2

Prime Cost Control

Prime Cost Control

Prime cost means food, beverage, and labor costs combined. In this model, Year 1 prime cost is disclosed at 467%, with 140% food and beverage COGS plus $373k payroll on $114M revenue; by Year 5 it improves to 379%. Lower prime cost leaves more cash for rent, overhead, debt service, and owner draw.

Here’s the quick math: prime cost = food and beverage cost + payroll. The key inputs are covers, menu mix, average check, ingredient cost percent, spoilage, and labor hours per shift. Cut quality too hard and demand can slip, which can erase the savings through weaker repeat visits and reviews.

How to tighten prime cost

Track prime cost by daypart and station, not just at month end. Watch food cost per dish, labor hours per cover, spoilage, comps, and voids. Menu engineering can push margin toward dishes guests already buy, while portion control and purchasing discipline protect cash. Kitchen scheduling should follow booked covers, not habit.

Daily: food cost and labor hours

Weekly: spoilage and comp rate

Per shift: covers per labor hour

Monthly: margin by menu item

If labor runs ahead of covers or ingredient costs rise faster than menu prices, owner pay gets squeezed fast. Protect the guest experience first, then remove waste, overstaffing, and low-margin items that don’t pull their weight.

3

Labor And Service Model

Labor and Service Cost

Labor is the ceiling on owner pay in a service-heavy restaurant. Modeled payroll starts at $373k in Year 1 and rises to $621k in Year 5, with a $65k restaurant manager, $60k head chef, plus line cooks, server baristas, and dishwashers. If covers and check average do not grow with staffing, labor eats cash flow before profit reaches the owner.

Service roles like sommeliers, hosts, managers, and pastry talent can lift the guest experience, but only if the volume supports them. Here’s the quick math: payroll grows about 67% from Year 1 to Year 5, so each added FTE must earn its keep through more covers, better check size, or both. Owner time should be priced as wages first, then the rest is profit.

Track Labor per Cover

Measure staffing against covers, service periods, and check average, not just headcount. The key inputs are labor hours by role, covers by daypart, and payroll by month. If you add premium service staff, set a target for revenue per cover that pays for them. Otherwise, labor turns into a fixed drag on owner income.

Track labor hours per cover.

Match FTEs to covers.

Price owner hours as wages.

Test staffing by daypart.

What this estimate hides: more service polish can improve reviews and repeat visits, but it also raises wage pressure. If staffing grows faster than demand, cash flow tightens fast. So keep a weekly view of payroll, covers, and average check, and cut shifts that do not lift guest spend or service quality.

4

Occupancy And Fixed Overhead

Occupancy And Fixed Overhead

Occupancy and fixed overhead are the bills that hit before demand does. In this model, rent is $7,500 per month or $90,000 per year, and total fixed overhead is $1,296,000 per year, including utilities, insurance, POS base fee, website maintenance, cleaning, accounting, and legal.

A premium site can lift traffic, but it also raises the monthly nut. Owner pay improves only when sales per seat outrun rent, repairs, décor upkeep, and service systems; if they don’t, fixed costs eat cash fast and leave little room for profit draw.

Hold The Fixed Nut Down

Track fixed costs as a share of monthly sales, then compare them to covers and average check. Here’s the quick math: if occupancy rises but seat sales do not, margin gets squeezed before food cost or labor changes can help.

Watch rent, utilities, and insurance monthly.

Review POS, website, and cleaning fees.

Match location cost to seat revenue.

Set a hard limit for non-variable spend, then test whether the site’s demand justifies it. If repairs, décor upkeep, or service systems keep climbing, the owner’s take-home falls even when the room looks full.

5

Private Dining And Events

Private Dining And Events

Private dining and events turn slow nights into booked revenue. In this model, catering is at 100% of sales across all five years, so each corporate dinner, buyout, tasting event, or minimum-spend booking adds top-line sales before costs. The upside comes when these bookings use empty seats and existing kitchen capacity, not when they crowd out regular guests.

The key inputs are event count, guest count, average spend, deposit timing, and labor hours. A full room can lift revenue per cover, but if prep load or service slips, the extra sales can hurt repeat business and owner pay through lower margins.

Book Slow Nights First

Track event revenue, deposit rate, labor hours, and whether events hit a minimum spend. A minimum-spend booking means the party must spend at least a set amount, which protects margin. If a Thursday private dinner needs extra cooks or a complex menu, price that work in before you confirm the date.

Fill low-demand nights first.

Use deposits to protect cash.

Limit menu changes and prep spikes.

Measure profit per event, not sales.

6

Fine Dining Restaurant Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income scenarios without promising distributions

Owner income scenarios

Weekly covers, menu pricing, and payroll drive take-home pay here. Low, base, and high cases show how ramp speed changes what the owner keeps after reserves, debt, taxes, and reinvestment.

Scenario view of owner take-home at different volume and pricing levels.

Scenario

Low CaseEarly ramp-up

Base CaseStabilized operations

High CaseScaled demand

Launch model

This is the lower earnings path, based on Year 1 volume and pricing.

This is the modeled middle path, using Year 3 volumes and pricing.

This is the stronger upside path, built on Year 5 demand and pricing.

Typical setup

Weekly covers stay at 770, with $22 midweek AOV and $32 weekend AOV, and EBITDA holds near $267k.

Weekly covers rise to 1,110, AOV steps to $24 midweek and $34 on weekends, and EBITDA reaches about $679k.

Weekly covers reach 1,790, AOV moves to $26 midweek and $36 on weekends, and EBITDA climbs to about $1.057M.

Cost drivers

770 weekly covers

$22/$32 AOV

60% food mix

20% beverages

$373k payroll

1,110 weekly covers

$24/$34 AOV

58% food mix

20% beverages

10% catering

1,790 weekly covers

$26/$36 AOV

56% food mix

14% delivery

larger staffing

Owner income rangeBefore owner reserves

$267kRamp-up

$679kStabilized

$1.057MScale-up

Best fit

Use this to test slow traffic and thin owner take-home in the opening year.

Use this for a normal run-rate once the dining room, staffing, and menu mix settle.

Use this to test what owner income looks like if demand stays strong and the room keeps filling.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. Owner take-home is shown after reserves, debt, taxes, and reinvestment.

In the modeled case, the owner-income proxy is $267k Year 1 EBITDA on $114M revenue, growing to $1057M EBITDA on $245M revenue by Year 5 That is before debt service, income taxes, reserves, reinvestment, and any formal owner salary

The model shows break-even in Month 3, with 3 months to breakeven and 15 months to payback That timing depends on the assumed 770 weekly covers in Year 1, $22 midweek AOV, $32 weekend AOV, and enough cash to survive the Month 2 minimum cash need of $784k

You can pay yourself through salary, distributions, or both, but they mean different things Salary is pay for work in the restaurant Distributions are profit taken out after costs and reserves The model’s $267k Year 1 EBITDA is not automatic take-home because taxes, debt, and reinvestment still come first

Covers, average check, prime cost, payroll, and rent move profit the most Year 1 assumes 770 weekly covers, 140% food and beverage COGS, $373k payroll, and $90k annual rent A small miss in covers can hurt quickly because fixed overhead still runs every month

Improve revenue per cover while keeping service tight In this model, beverages are 200% of sales, catering is 100%, and weekend AOV starts at $32 versus $22 midweek Wine pairings, private dining, and better slow-night utilization can help, but only if labor and food waste stay controlled

About the author

Jack Bennett

Business Model Writer

Jack Bennett is a business model writer at Financial Models Lab, where he explains startup planning and business model economics in clear, practical language. He focuses on the money questions new founders ask when comparing business ideas, with an eye on how small businesses operate day to day. Jack’s writing helps readers understand the numbers behind real business operations without heavy finance jargon, making complex decisions feel more manageable and grounded.

Choosing a selection results in a full page refresh.