How Much Green Building Construction Owners Make: $180K Plus EBITDA

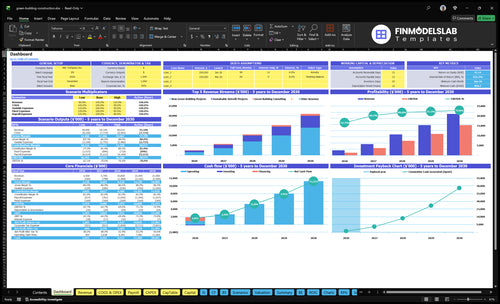

A green building construction owner can model take-home as a $180,000 owner salary plus any distributions the business can safely pay after overhead, reserves, debt service, and reinvestment In the researched base case, annual revenue starts at $25M in Year 1 and reaches $210M in Year 5 EBITDA is modeled at $1319M in Year 1 and $15313M in Year 5, but that is company operating profit before owner distributions, taxes, and financing effects The clean takeaway: revenue is large, but owner take-home depends on collections, project margin, and how much cash must stay in the business

Owner income$1.5M–$15.5MNet margin53%–73%Revenue for target pay$342kBusiness difficultyHard

Want to test your own owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income can change with revenue mix, job margin, payroll, debt service, taxes, and reinvestment. Not guaranteed salary, tax advice, or owner distribution advice.

How does owner income change in the full forecast?

How much can a green building construction owner take home?

For Green Building Construction, the owner’s modeled take-home starts with a $180,000 annual salary, not total project revenue; see What Is The Current Growth Rate Of Green Building Construction? for market context. Company EBITDA, meaning profit before interest, taxes, depreciation, and amortization, grows from $1.319M in Year 1 to $15.313M in Year 5, but distributions depend on cash needs.

Take-home math

Owner salary: $180,000/year

Year 1 EBITDA: $1.319M

Year 3 EBITDA: $7.375M

Year 5 EBITDA: $15.313M

What can reduce it

Hold cash for reserves

Cover debt service

Fund retainage gaps

Reinvest in crews and capacity

What affects green building construction profit margins?

Green building construction margins get squeezed fast when sustainable materials take 75% of revenue and specialized subcontractor labor takes 65%; if you want a quick benchmark, start with What Is The Estimated Cost To Open Green Building Construction?. Here’s the short read: profit depends on tight estimates, certified material pricing, and disciplined change orders, because rework and schedule slips can cut owner distributions even when revenue grows.

Main cost pressure

75% revenue: sustainable materials

65% revenue: subcontractor labor

40% cost control: sales and marketing

10% cost control: travel and logistics

Margin protection

Use accurate job costing

Lock certified material pricing

Track labor productivity and bids

Control scope and progress billing

Does a green building construction owner make more by scaling?

Yes—Green Building Construction can make more as it scales, but only if completed and collected revenue grows faster than added overhead. In the model, revenue rises from $25M to $210M while payroll rises from $465k to $1,175M and fixed overhead stays at $1,692k. Owner-operator stays lean, but a managed team adds architects, project managers, engineers, marketing, admin, and R&D, so capacity rises and so does execution risk.

Where scaling helps

Revenue can reach $210M.

Payroll starts at $465k.

Fixed overhead stays at $1,692k.

More roles add project capacity.

What can hurt returns

Working capital needs can jump.

Hiring mistakes can cut margin.

Quality control gets harder.

Backlog may not convert to cash.

Green Building Construction Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers that matter most?

1

Annual Volume

$2.5M-$21M

More completed projects push revenue from $2.5M to $21M, and that scale is what turns into owner profit.

2

Deal Size

High

Bigger contract tickets raise revenue without the same fixed cost base, so each job can throw off more cash.

3

Gross Margin

86%

Materials at 7.5% and subcontract labor at 6.5% leave an 86% gross margin before other costs, so overruns hit hard.

4

Labor Efficiency

$465K-$1.18M

Payroll rises from $465K to $1.18M as the team scales, so labor discipline keeps margins from leaking.

5

Overhead

$169K/yr

Fixed overhead is about $169K a year, so trimming non-job costs protects EBITDA as revenue grows.

6

Cash Reserves

$895K

Month 1 minimum cash is $895K, and revenue only helps distributions after it is billed and collected.

Green Building Construction Core Six Income Drivers

Annual Project Volume

Annual Project Volume

More completed and collected projects raise revenue and owner distributions. Here, revenue is modeled from $25M in Year 1 to $210M in Year 5, or 8.4x growth across new builds, retrofits, and consulting. The catch is simple: signed contracts do not pay until milestones are billed and collected.

Volume only helps when delivery stays tight. If crew capacity, permitting, or quality control slips, work-in-progress (WIP) ties up cash and delays payment. So the owner’s income depends on finished jobs, clean closeouts, and fast collections, not just more wins on paper.

Track Billed, Collected Volume

Measure projects completed, dollars billed, and dollars collected every month. That tells you whether volume is turning into cash the owner can actually take home. A big signed job still misses pay if it sits in WIP or waits on a milestone invoice.

Watch crew load, permit cycle time, and rework rate. If starts rise faster than field capacity, margin and cash both get squeezed. Keep the forecast tied to milestone billing, then compare it with collections so higher volume turns into real distributions.

Completed projects

Billed milestones

Collected cash

Crew capacity

Permit delays

Rework and closeout speed

1

Average Contract Value

Average Contract Value

Average contract value is the average size of each signed job. Here, that can range from $15M to $140M for new green buildings, $800k to $60M for sustainable retrofits, and $200k to $10M for consulting. Bigger jobs can lift revenue per contract and cut sales work per dollar earned, but only if scope stays tight and margins hold.

Here’s the quick math: fewer, larger contracts can reach the same revenue with less selling effort. But larger custom sustainable homes, energy-efficient commercial buildouts, and retrofit contracts usually bring more complexity, retainage (cash the client holds back until milestones are done), and subcontractor risk, so owner pay improves only when billing, change orders, and job cost control stay on track.

Track Size, Margin, and Cash

Measure average contract value by service line, then compare it with gross margin, change-order rate, and days to collect cash. A bigger contract helps only if the added revenue is collected on time and does not pull the job into delay, rework, or margin erosion.

Use these inputs: project type, signed contract value, billings by milestone, retainage, and subcontractor cost. If contract size rises while margin falls, take-home income usually drops even though top-line revenue looks stronger.

Average contract value by job type

Gross margin after direct costs

Retainage and collection timing

Change-order rate per project

2

Gross Margin On Green Building Projects

Gross Margin On Green Builds

Gross margin is what turns project revenue into gross profit before overhead and owner pay. On these jobs, the modeled structure uses 75% sustainable materials and 65% specialized subcontractor labor, with an 86% gross margin before variable expenses. That only holds if estimates are tight and scope stays locked.

Here’s the quick math: when revenue passes $10M, even a small slip from missed estimates, weak change orders, or labor overruns can erase a lot of EBITDA. One bad material substitution or low installer productivity can cut the owner’s draw fast because there is less gross profit left to cover overhead.

Protect Margin In The Bid And Build

Track the inputs that move margin: material markup, subcontractor bids, installer output, and change order capture. If the bid assumes one product and the job uses another, the margin loss shows up immediately in gross profit and later in owner income.

Compare estimate vs. actual job cost.

Lock change orders before extra work starts.

Measure crew productivity weekly.

Rebid specialty labor when scope changes.

Watch gross margin by project, not just for the month. If margin slips by 2 points on a large contract, the dollar hit can be material enough to delay payroll, lender covenants, or owner distributions.

3

Labor Efficiency And Subcontractor Costs

Labor Efficiency And Subcontractor Costs

When specialized crews miss schedule or run over budget, owner income drops fast because labor is the biggest variable cost here. With specialized subcontractor labor modeled at 65% of revenue, every $10M of project sales carries about $6.5M in direct labor cost before overhead and owner pay. Delays, rework, and scarce certified labor cut EBITDA and shrink distributions.

This driver includes crew hours, subcontract bids, certified labor availability, and rework. Track labor cost as % of revenue, on-time milestone delivery, and change-order recovery; if those slip, cash stays trapped in jobs instead of reaching the owner. Internal payroll is also modeled from $465k to $1,175M, so staffing control matters as much as sales.

Lock Crew Cost And Schedule

Price the job from the labor plan up. Build each bid around scope, certified crew time, and finish dates, then compare actual labor to budget every week. For energy-system installers, green building engineers, and project managers, even a small slip in productivity can wipe out margin and reduce the cash available for owner draws.

Use three controls: labor cost per phase, rework hours, and milestone on-time rate. Keep subcontractors booked early, require clear bid scope, and charge for extra work fast. Better scheduling and bid control can lift EBITDA without needing more sales.

4

Operating Overhead

Operating Overhead

Operating overhead is the fixed cost stack paid before owner distributions. Here it is modeled at $1.692M a year, including $96k rent, $18k design software, $12k insurance, $6k certifications, $96k utilities, $36k supplies, and $24k R&D material testing. Payroll is separate, so this line mostly hits operating profit and the cash left for the owner.

Higher overhead means more collected project revenue is needed before the owner can pay themself. One clean rule: the bigger the fixed base, the harder it is to protect take-home in slow project months. If revenue slips or billing gets delayed, overhead still gets paid.

Protect The Fixed Base

Estimate overhead from monthly rent, software, insurance, certifications, utilities, supplies, and testing spend. Track each item against budget, then compare total overhead with collected revenue, not just signed contracts. If billing lags, overhead pressure shows up in cash flow before it shows up in backlog.

Review rent and software monthly.

Watch utilities and supplies drift.

Hold testing spend to budget.

Compare overhead to collected cash.

Use a hard monthly review and pause nonessential fixed spend until cash is in. With payroll scaling from $465k to $1.175M, keeping overhead tight is what stops fixed costs from crowding out owner distributions.

5

Construction Cash Flow And Owner Reserves

Construction Cash Timing

Profitable jobs can still leave the owner short on cash if money sits in deposits, material prepayments, retainage, or slow collections. For this model, the key input is cash timing, not just booked profit. With $895k minimum cash in Month 1 and $240k of launch capex, owner pay has to wait until bills, debt service, and reserves are covered.

Here’s the quick math: even a strong margin does not become spendable until progress payments clear. If a client withholds retainage or pays late, the owner’s draw drops fast because working capital is doing the heavy lifting. Strong cash control makes profit usable; weak control turns it into trapped earnings.

Track Cash Before Draws

Measure cash on hand, days sales outstanding, retainage due, and the gap between progress billing and cash collected. Also track the reserve floor against the $895k minimum cash target, then hold owner distributions until that floor stays intact after capex and debt service.

Use billing terms that match project spend: deposits up front, milestone invoices during the job, and fast follow-up on collection. Test whether larger prepayments or tighter retainage terms improve free cash. If collections slip, owner pay should slow before payroll or vendor trust does.

6

Green Building Construction Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high-growth owner-income outcomes

Owner income scenarios

Owner income shifts with project mix, staffing, and overhead in this model. Lean years protect cash, while high-growth years can lift earnings but add hiring and quality-control strain.

Low, base, and high owner income cases for a green building contractor.

Scenario

Low CaseCash risk

Base CasePlan case

High CaseGrowth upside

Launch model

This is the lower-earnings path, where collected revenue lands below plan and owner pay gets squeezed by margin pressure.

This is the modeled path, where revenue scales across new builds, retrofits, and consulting under the planned cost structure.

This is the stronger-earnings path, where backlog and project capacity rise fast and owner income can move above plan.

Typical setup

Fewer projects close, retrofit demand is choppier, the $180k founder salary target stays in place, and distributions stay tight to protect cash.

Revenue follows the model's mix of projects, gross margin before variable costs stays near the planned 86%, variable expenses run at 5%, and payroll grows from $465k to $1.175M as EBITDA rises from $1,319k to $15,313k.

More work flows through the pipeline, but the business also needs more hiring, bigger reserves, and tighter quality control to keep delivery on track.

Cost drivers

Lower collected revenue

fixed owner salary target

tighter gross margin

lean distributions

cash reserve pressure

Project mix growth

86% gross margin

5% variable expenses

$1.692M fixed overhead

payroll scaling

Larger backlog

higher project capacity

more hiring

reserve build

quality-control load

Owner income rangeBefore owner reserves

Below $180k targetTight earnings

Near $180k targetTarget case

Above $180k targetUpside, more risk

Best fit

Use this to stress-test survival if bookings slip or clients delay payments.

Use this as the main planning case for budgets, hiring, and lender conversations.

Use this to test upside if demand stays strong and the team can handle more volume.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution targets.

The modeled founder salary is $180,000 per year That is separate from distributions, which depend on available cash after overhead, reserves, debt service, and reinvestment In the base case, EBITDA ranges from $1319M in Year 1 to $15313M in Year 5, but EBITDA is not automatic take-home

The researched model shows breakeven in Month 1, with a one-month payback period That result depends on early revenue conversion, collections, and the $895k minimum cash need If projects are delayed or deposits are weak, the owner may need to hold more cash before taking distributions

Yes, reserves matter in construction because profit and cash do not move together Material prepayments, progress billing gaps, retainage, and launch capex can absorb cash This model includes $240k in early capex and a $895k minimum cash need, so owner distributions should come after working capital is protected

The biggest drivers are completed revenue, project margin, payroll, and cash timing The model uses 14% direct job costs, 5% variable expenses, $1692k annual fixed overhead, and payroll rising from $465k to $1175M Cost overruns, rework, and slow collections can reduce owner take-home quickly

Start with a target salary, then test whether revenue, margin, overhead, reserves, and cash collections support it In this case, the owner salary is $180,000, Year 1 revenue is $25M, and Year 1 EBITDA is $1319M Still, distributions should be modeled separately from salary and profit

About the author

Oliver Pierce

Startup Cost Researcher

Oliver Pierce is a startup cost researcher at Financial Models Lab, where he writes practical guides for people planning their first business. He focuses on break-even planning and on comparing business ideas by cost and effort, with a clear, realistic approach to small business planning. His work is aimed at non-finance readers and is written to make business planning easier to understand and use.

Choosing a selection results in a full page refresh.