Owner income$185k

Owner income$185kHow Much a GRI Reporting Services Owner Can Make: $185K Plan

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$185k  Net margin2.8%–43.3%

Net margin2.8%–43.3% Revenue for target pay≈$6.6M

Revenue for target pay≈$6.6M Business difficultyHard

Business difficultyHard

A GRI sustainability reporting services owner can plan around the modeled $185,000 annual CEO / Managing Director salary, before taxes and any distributions Revenue is not owner income: in the first year, a $180,000 marketing budget at 125% of revenue implies about $144 million in revenue After 147% direct COGS, 163% variable expenses, $331,800 fixed overhead, and about $510,000 payroll including owner salary, operating profit is about $151,800 before tax, reserves, debt, and reinvestment The owner’s real take-home depends on client volume, project scope, delivery labor, utilization, and how much cash the firm keeps in the business

Owner income$185kNet margin2.8%–43.3%Revenue for target pay≈$6.6MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice, and it does not include tax filing advice or guaranteed earnings.

Want to see the owner-pay model?

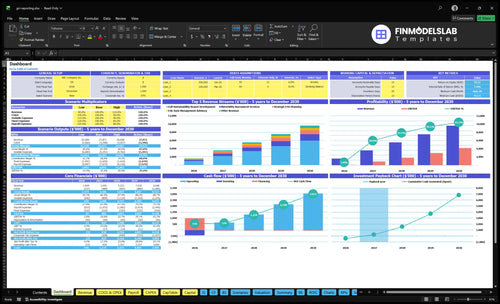

Dashboard: revenue, gross margin, payroll, fixed overhead, operating profit, owner pay, COGS, reserves, cash flow. Open the GRI Sustainability Reporting Services Financial Model Template.

Owner-income model highlights

- Owner salary: $185,000

- Fixed overhead: $331,800

- Direct COGS: 147%

- Variable expenses: 163%

- Assumptions: rates, hours, CAC

- Scenarios: pricing, staffing, retainers

- Planning tool, not promise.

Can a solo GRI consultant make more than a small firm owner?

A solo GRI consultant can usually keep higher margins because there’s no payroll stack, but a small firm owner can out-earn them only if added billable work covers the extra team cost. In the model, payroll alone is $385,000 for an owner at $185,000, one senior consultant at $125,000, and one junior analyst at $75,000. Delivery time is the choke point: a full report takes 85 hours in year one, while materiality work takes 35 hours.

Solo margin

- Less payroll means higher margin

- 85 hours limits report volume

- 35 hours still eats owner time

- Non-billable work cuts take-home

Small firm scale

- More engagements can lift revenue

- $385,000 payroll adds risk

- Training and quality control add drag

- Pricing and utilization must outrun payroll

How much revenue does a GRI reporting firm need to pay the owner?

GRI Sustainability Reporting Services needs about $122,000 in revenue to cover the modeled $185,000 owner salary inside $510,000 of payroll plus $331,800 of fixed overhead. Using the provided 690% contribution rate, that means $841,800 of annual contribution to break even before taxes. At $144,000 revenue, the model shows about $993,600 of contribution and roughly $151,800 left before taxes, reserves, debt, and reinvestment.

Revenue floor

- $122,000 covers overhead and payroll.

- $331,800 fixed overhead comes first.

- $510,000 payroll includes the owner.

- $185,000 is the modeled owner salary.

What $144,000 means

- $144,000 revenue yields $993,600 contribution.

- Less overhead and payroll leaves $151,800.

- That cash comes before taxes and reserves.

- Any shortfall hits owner pay fast.

What costs reduce GRI reporting business owner income?

For GRI Sustainability Reporting Services, the costs that cut owner income are the delivery inputs and payroll, not just rent and software. See How Much To Launch GRI Sustainability Reporting Services? for the launch-cost view. Direct COGS include third-party data provider licenses at 85% in year one and external verification and assurance at 62%, while variable operating costs add marketing and business development at 125% and project-specific legal and regulatory support at 38%. Fixed overhead is $27,650 a month, or $331,800 a year, and every point of margin loss reduces owner-pay capacity.

Direct cost drivers

- Third-party data licenses: 85%

- Verification and assurance: 62%

- Marketing and business development: 125%

- Project-specific legal support: 38%

Scale costs

- Fixed overhead: $27,650/month

- Fixed overhead: $331,800/year

- Payroll: owner $185,000, two seniors at $125,000 each

- Junior analyst salary: $75,000

Want the six income drivers at a glance?

1

85.3%Project Pricing

Year 1 direct costs are about 14.7%, so a $24.2K full report or $11.2K materiality job keeps most of the fee after delivery spend.

2

85-65hBillable Utilization

Dropping full-report work from 85 hours to 65 hours frees capacity, so the same team can bill more clients before adding headcount.

3

45%-32%Client Mix

The mix moves from 45% full reports to 32% by Year 5, so average ticket size and margin change with the project mix.

4

$331.8KStaffing Leverage

Fixed overhead is $331.8K a year and owner salary is $185K, so staffing has to cover that base before take-home rises.

5

10%-35%Advisory Revenue

Strategic ESG planning rises from 10% to 35% by Year 5, which adds repeat advisory work and steadier income.

6

$12KSales Efficiency

With first-year CAC at $12K, the marketing funnel has to convert cleanly or new-client growth gets expensive.

GRI Sustainability Reporting Services Core Six Income Drivers

Average Engagement Pricing And Report Complexity

Scope Price Discipline

When the client says “just a report,” that can turn into 85 hours × $285 = $24,225 if it includes data cleanup, stakeholder input, disclosure mapping, revisions, and management review. The shorter 45-hour × $425 = $19,125 strategy project earns a higher rate, but less total revenue. So the owner’s income rises when scope is tight and the fee matches the real work.

Here’s the quick math: a high hourly rate does not protect margin if hours collapse or rework grows. One loose scope can push unpaid executive edits and extra reviews onto the firm, which cuts gross profit per client and slows cash available for owner pay. One clean scope beats one “premium” rate with hidden labor.

Price the Work, Not the Label

Track the inputs that drive complexity: stakeholder engagement, data collection, disclosure mapping, revisions, and management review. Those are the hours that move gross margin. If the scope includes cleanup and executive edits, the fee should reflect it before work starts.

- Log hours by task type.

- Separate report and advisory scopes.

- Price revision rounds upfront.

- Flag data cleanup as billable.

- Review margin after every client.

1

Billable Utilization And Capacity

Billable Hours

Owner pay rises when more qualified time turns into paid work. In year 1, service work can range from 18 hours for regulatory compliance consulting to 85 hours for full report development. Here’s the quick math: the same fee buys more margin when non-billable time like proposals, research, billing, and admin stays low.

85 hours can fall to 65 hours by year 5 with better templates and trained analysts. That improves capacity and take-home income, but pushing utilization too hard can cause burnout or rushed quality, especially when the owner is also selling and doing final review.

Track Paid Hours, Not Just Busy Time

Measure billable hours, non-billable hours, and utilization each month. Use this input set:

- Paid client hours

- Proposal and sales hours

- Review and revision hours

- Admin and billing hours

- Analyst support hours

To raise owner income, move research, data cleanup, and draft prep to trained staff, then keep the owner on pricing, client control, and final sign-off. If utilization climbs without support, cash flow may look strong while quality and retention slip.

2

Client Mix And Reporting Demand

Client Mix Drives Fee Quality

The first-year mix index is weighted toward 450% full report development, 250% materiality assessment, 200% data management advisory, 150% regulatory compliance, and 100% strategic planning. That mix lifts revenue per client, but it also raises documentation burden and review time, which can squeeze gross margin if the fee does not cover extra hours.

By year five, the mix shifts toward recurring advisory, with 400% data management advisory and 350% strategic planning. That usually improves owner take-home because the work repeats more and the delivery load is lighter, but cash can still lag if procurement cycles are long and signed work takes weeks or months to start.

Track Mix, Not Just Leads

Measure the mix by service line and by stage. Count active clients in report build, materiality, compliance, data readiness, and planning, then track days from scope to signature, repeat work share, and time spent on revisions. That shows whether the book is moving toward higher-margin advisory or staying stuck in one-off report work.

- Split revenue by service line.

- Track procurement cycle length.

- Watch repeat-client share.

- Flag delayed cash early.

Best-fit clients already need reporting support, data readiness, and governance help. If demand is real but procurement runs long, the income hit shows up in cash flow first, then owner pay.

3

Staffing Leverage And Subcontractor Margin

Staffing Leverage and Subcontractor Margin

Staffing changes owner income through capacity, margin, and management load. The modeled first-year payroll is $510,000: $185,000 for the CEO / Managing Director, $125,000 each for two senior consultants, and $75,000 for one junior analyst. That mix adds delivery power, but it only improves owner pay if billed work grows fast enough to cover payroll and still leave profit.

Senior consultants expand review and advisory capacity, and the junior analyst supports data collection and disclosure work. Subcontractors can keep the team flexible, but they usually cut gross margin and add quality-check time. The risk is hiring before signed work exists. If utilization and project pricing do not cover the added cost, cash gets tight and the owner’s draw gets squeezed.

Track Payroll Against Signed Work

Measure staffing against booked revenue, not hoped-for pipeline. Keep a rolling 90-day view of billable hours by role, then compare it with the $510,000 annual payroll base. One clean test: if senior consultant time is being used for low-value admin or rework, owner income drops because expensive labor is not reaching the client at a high enough rate.

Track billable utilization by role.

Track subcontractor gross margin per job.

Track rework and review hours.

Track signed backlog before hiring.

Use subcontractors for spikes, not as a blanket fix. Price in quality checks, revision time, and management overhead so the extra capacity actually improves profit. If demand is uneven, push more data collection and disclosure support to the junior analyst first, and hold senior hiring until signed work supports it.

4

Recurring Advisory Revenue

Recurring Advisory Revenue

Retainers smooth income between annual report cycles by tying fees to reporting readiness,

The risk is selling vague advice that does not renew. If clients cannot point to a clear reporting output, cash gets lumpy, fixed overhead stays under pressure, and owner pay becomes harder to draw with confidence. One line says it all: no visible output, no sticky retainer.

Improve Retainer Renewal

Track retainer revenue per client, renewal rate, and hours per retainer. A simple test: if the monthly fee does not cover the work needed for readiness, governance, and disclosure support, you are just reselling project labor with a softer name.

Sell each retainer with a concrete output, such as a gap log, KPI pack, or disclosure draft. That keeps the service visible, protects margin, and makes it easier to forecast cash and owner income before the next annual report cycle.

5

Pipeline Efficiency And Sales Cycle Economics

Sales Cycle Economics

This driver covers referral flow, proposal conversion, follow-up time, and marketing spend. When the pipeline is proposal-heavy, the owner’s income gets squeezed by unpaid selling time and slow cash turns. With a $180,000 first-year marketing budget and $12,000 CAC (customer acquisition cost), the model implies about 15 clients; by year five, $520,000 at $7,800 CAC supports roughly 67 clients if spend scales cleanly.

Here’s the quick math: lower CAC means more cash left for delivery, and fewer owner hours stuck in sales means more billable work. The risk is low close rates on long proposals, which can delay cash and drag take-home pay even when demand is real.

Cut Unpaid Selling Time

Measure proposals sent, close rate, sales-cycle days, and owner hours spent on pursuit work. If referrals and proposal conversion improve, utilization rises because less time is wasted on unpaid selling. A simple check is whether each $1 of CAC produces enough client gross profit to cover delivery and still pay the owner.

- Track owner sales hours weekly

- Separate referrals from cold leads

- Test proposal-to-close rate

- Forecast CAC by channel

What this estimate hides: if the pipeline fills with low-fit prospects, CAC can look fine while cash flow stays tight. Favor fewer, better-qualified proposals, because faster closes turn marketing spend into billable work sooner and protect owner draw.

6

Compare lean, base, and high owner-pay scenarios

Owner income scenarios

Income shifts as client mix, CAC, and staff leverage change. The low case protects cash, the base case mirrors Year 1, and the high case reflects later-year scale.

| Scenario | Low CaseCash tight | Base CaseModeled base | High CaseUpside case |

|---|---|---|---|

| Launch model | Owner income stays at the low end because sales stay uneven and cash only supports the planned salary when it can. | Owner income follows the first-year model, with the CEO salary covered and only limited room for extra draw. | Owner income lifts as advisory mix, lower CAC, and staff leverage improve margins and free up more profit. |

| Typical setup | Revenue stays near the early model, CAC remains at $12,000, the CEO does most delivery, and the $331,800 annual fixed overhead leaves little room for extra draw. | Revenue is $1.609 million in Year 1, EBITDA is $45,000, gross margin after direct COGS is about 85.3%, and fixed overhead runs $331,800 a year. | By Year 5, revenue reaches $9.598 million, EBITDA reaches $4.160 million, CAC falls to $7,800, and direct COGS drops to 11.3% from 14.7% in Year 1. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $185,000 salary onlySalary only | $185,000 salarySalary covered | Salary plus distributionsHigher upside |

| Best fit | Use this to stress-test a slow sales start and tight cash. | Use this as the core planning case for a normal launch year. | Use this for an upside plan with stronger sales and more leverage. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- GRI Sustainability Reporting Services Porter's Five Forces Analysis

- GRI Sustainability Reporting Services BCG Matrix

- GRI Sustainability Reporting Services Business Model Canvas

- What Are The 5 KPI Metrics For GRI Sustainability Reporting Services Business?

- GRI Sustainability Reporting Services Business Plan Template in Pre-Written Word

- How Increase Profitability Of GRI Sustainability Reporting Services?

- What Are Operating Costs For GRI Sustainability Reporting Services?

- GRI Reporting Business Startup Costs: $277k Monthly Overhead

- GRI Sustainability Reporting Services Financial Model Template in Excel

- How To Start A GRI Sustainability Reporting Firm In 6 To 12 Weeks

- How To Write A Business Plan For GRI Sustainability Reporting Services?

- GRI Sustainability Reporting Services Marketing Mix

- GRI Sustainability Reporting Services Marketing Plan

- GRI Sustainability Reporting Services Business Proposal

- GRI Sustainability Reporting Services PESTEL Analysis

- GRI Sustainability Reporting Services Pitch Deck Example Editable PPTX

- GRI Sustainability Reporting Services Business SWOT Analysis

- GRI Sustainability Reporting Services Value Proposition Canvas

Frequently Asked Questions

The model starts with a $185,000 CEO / Managing Director salary before taxes In the first year, implied revenue is about $144 million if $180,000 marketing spend equals 125% of revenue After direct costs, variable expenses, fixed overhead, and payroll, profit is about $151,800 before reserves and distributions