How Much Does a Handicraft Store Owner Make on $498K Year 1 Sales?

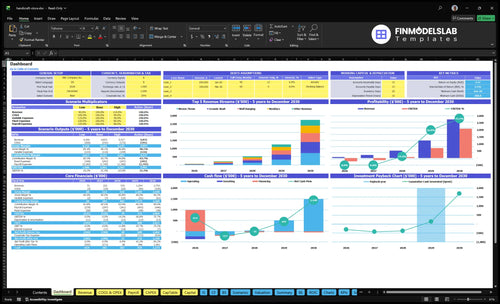

You’re trying to turn handmade retail sales into real owner income, not just busy weekends This five-year planning view separates $498K in Year 1 revenue, gross margin, rent, payroll, reserves, and owner take-home before taxes, financing terms, and personal distributions

Owner income$174K/moNet margin75.7%Revenue for target pay$2.8MBusiness difficultyHard

Want to test your own owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Handicraft Store model?

Year 1 revenue: $498K. Payroll: $2,065K. Fixed overhead: $582K. Operating profit: about $192K before distributions.

Owner-income model highlights

Owner take-home drivers

Revenue, mix, and COGS

Test assumptions by scenario

Dashboard to cash flow

How much can a handicraft store owner pay themselves?

A Handicraft Store owner can pay themselves about $65,000/year if they actively work as the store manager; see How To Write A Business Plan For A Handicraft Store? for the plan structure behind that choice. In the Year 1 model, $498,000 revenue and $192,000 operating profit equals a 38.6% operating margin before owner distributions.

Owner Pay

Pay $65,000 if managing daily operations

Take distributions after taxes and reserves

Fund debt payments before extra withdrawals

Reinvest before scaling inventory or workshops

Cash Limits

Manager hire keeps $65,000 in payroll

That wage is not owner income

Reserves reduce cash dollar for dollar

Workshops add upside, labor, and capacity strain

What profit margin does a handicraft store need?

A Handicraft Store needs enough margin to pay artisans, cover card fees, rent, payroll, shrink, slow stock, and reserves. If you’re building the plan, How To Write A Business Plan For A Handicraft Store? belongs in the margin section, because on $498K revenue, every 10 margin points adds about $49.8K a year.

Margin stack

Pay makers first.

Cover transaction fees next.

Keep room for rent.

Protect payroll and reserves.

What moves it

Wholesale buying lifts margin dollars.

Consignment splits cut store take.

Private-label goods can mark up more.

Slow inventory ties up cash fast.

Does a handicraft store make more owner-operated or with staff?

A Handicraft Store usually pays the owner more when the owner also fills the $65K store manager role, but that setup limits hours, workshops, buying, merchandising, and local events. A staffed model lowers owner labor, yet Year 1 payroll is $2065K with a manager, sales associates, a workshop instructor, a marketing coordinator, and admin support. Multi-channel growth through workshops, online orders, custom pieces, and gift bundles can raise sales capacity, but it also adds fulfillment time, marketing cost, and inventory risk.

Owner-run model

Owner captures the $65K manager role.

Take-home can be higher.

Hours stay capped.

Workshops and events get squeezed.

Staffed growth model

Year 1 payroll is $2065K.

Includes manager and sales staff.

Adds workshop, marketing, admin help.

More sales channels add cost and risk.

Handicraft Store Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What drives handicraft store owner income?

1

Foot Traffic

3.5%

Year 1 gets about 4,420 monthly visitors, and a 3.5% buyer rate decides how much of that traffic turns into revenue.

2

Order Value

$96

With about 1.7 units per order and a weighted item price near $56, small basket changes move take-home fast.

3

Gross Margin

91.8%

Year 1 only gives up about 8.2% of revenue to artisan payouts and POS fees, so gross margin stays strong before fixed costs.

4

Payroll Load

$264.7K

Year 1 payroll is about $206.5K and rent is $3,800 a month, so fixed costs can erase gains if sales lag.

5

Weekend Spike

3.5x

Saturday traffic is 280 vs 80 on Monday in Year 1, so stock-outs or overbuying around the weekend can cut profit.

6

Extra Channels

High

Workshops, online orders, custom work, events, and corporate gifts add revenue without depending only on walk-in traffic.

Handicraft Store Core Six Income Drivers

Foot Traffic And Conversion

Foot Traffic to Buyer Orders

Foot traffic only helps owner income when visitors become buyers. In Year 1, the model assumes 4,420 monthly visitors from 1,020 weekly visitors, with peak days at 280 on Saturday and 220 on Sunday. At 35% conversion, that supports about 155 new buyer orders per month before repeat sales. Traffic growth lifts revenue, but only if margin and staffing stay in control.

By Year 5, conversion rises to 75% in the model, so the same traffic base would produce far more orders. Still, higher traffic can hurt cash flow if labor, shrink, and artisan payouts rise faster than gross profit. The owner’s take-home pay improves only when each extra visit turns into enough margin dollars to cover fixed costs and payroll.

Measure Conversion and Peak Coverage

Track the full path: visitors, conversion rate, average order value, and labor per open hour. Conversion rate is the share of visitors who buy. On busy weekends, compare 280 on Saturday and 220 on Sunday against staff coverage so service stays fast. If checkout lines or empty shelves show up, the traffic gain may not reach profit.

Count visitors by day

Measure buyer conversion weekly

Match staff to peak hours

Watch gross profit per order

Test small changes first: better signage, sharper product stories, and cleaner displays can raise conversion without adding rent. If conversion rises but payroll rises faster, owner draw will not improve. The goal is simple: more buyers per visitor, not just more people in the door.

1

Average Order Value And Product Mix

Product Mix and AOV

When shoppers add higher-ticket throws, wall décor, custom pieces, or gift bundles, the store earns more revenue per visit without needing the same jump in transactions. The model uses ceramic bowls at $55, necklaces at $42, woven throws at $75, wall hangings at $62, and workshop classes at $48, with a weighted product price of $5,635 and AOV near $9,580 at 17 units per order.

Owner pay improves only if the extra basket dollars keep strong gross profit. Here’s the quick math: if artisan payouts take 50% and POS and transaction fees take 32%, only 18% of sales is left before fixed costs and payroll. Bigger baskets help cash flow, but weak margin still leaves the owner short.

Raise Basket Size Without Losing Margin

Track AOV by category, not just store average. Watch how many orders include throws, wall décor, or bundles, and compare gross profit dollars per basket. If 17-unit baskets lift revenue but the added items are low margin, the owner can sell more and still take home less.

Test bundles against single-item sales.

Price custom work by labor time.

Forecast fees on each basket.

Protect cash before owner draws.

Use the mix to protect cash flow. Forecast owner pay only after subtracting artisan payouts, payment fees, and payroll. If a higher AOV comes from slow-moving stock, cash gets tied up and pay lags even when revenue looks strong.

2

Gross Margin And Artisan Terms

Gross Margin After Artisan Payouts

When you sell handcrafted goods, owner income depends on what stays after artisan payouts and POS (point-of-sale) plus transaction fees. Using the disclosed inputs, 50% of revenue goes to artisans and 32% goes to fees, so the business keeps about 18% contribution before rent, payroll, and owner pay. On $498K revenue, each 1 percentage point of margin is worth about $4,980 a year.

The model text says 950% and 918%, but those figures do not match the stated inputs. What matters is margin dollars: wholesale, consignment, local artisan payouts, and private-label goods should be compared by how much cash they leave after fees, not by markup percentage alone.

Track Margin Dollars, Not Markup

Build the forecast from revenue, payout %, payment fees, and product mix. For each category, calculate cash left after artisan share and fees, then compare that to handling, shelf space, and labor. If a line sells well but leaves weak dollars, it can raise revenue and still cut owner pay.

Test payout rates by category.

Separate private-label from consignment.

Track fee drag by payment type.

Price for margin dollars, not markup.

Use the same rule in every buying call: more sales only help when contribution rises faster than fixed costs. That keeps the store’s growth tied to real cash for payroll, rent, and owner draws.

3

Rent, Payroll, And Local Overhead

Rent, Payroll, And Local Overhead

Fixed overhead is $4,850 per month for rent, utilities, insurance, and licenses, and it sits on top of product costs. Add $172K per month in Year 1 payroll, and the store needs steady sales just to keep owner pay in reach. High rent or long store hours raise the sales floor; if traffic dips, profit can vanish fast.

Here’s the quick math: $3,800 rent plus $550 utilities, $320 insurance, and $180 licenses equals $4,850 before one item sells. Staffing can lift capacity, but it also turns slow months into cash pressure. For reading profit, split fixed costs from product costs so you can see what’s left for owner draw.

Track The Load Before Owner Pay

Watch sales per open hour against rent + payroll. If staffing or store hours rise, check whether extra sales cover the added cash burn, not just the extra labor. A longer schedule only helps if the added volume keeps gross profit ahead of the $176,850 monthly recurring load from overhead plus payroll.

Track rent as a % of sales.

Track payroll by open hour.

Test staffing against peak traffic.

Separate fixed and product costs.

What this estimate hides: payroll is the biggest swing factor. If sales soften, the owner may have to delay pay, cut hours, or reduce staffing before the store can support a draw. The cleanest control is a monthly forecast that shows when fixed overhead is covered and when owner income starts.

4

Inventory Turnover And Cash Flow

Inventory Turnover

Inventory turnover is how fast stock turns into cash, usually measured as cost of goods sold ÷ average inventory. In a handmade-goods store, slow bowls, necklaces, throws, wall hangings, and class supplies can trap cash, especially when items miss the season or get damaged. That cuts the money left for owner draws, even when the income statement still shows profit.

The cash test is simple: if new buying does not lift sales fast enough, cash sits on the shelf. Fast turnover frees cash for replenishment and distributions; slow turnover raises the risk of markdowns, shrink, and seasonal write-offs. Keep reserves for seasonal swings, vendor deposits, and refill buys before taking profit out.

Track Sell-Through, Then Buy Less

Measure turnover by category, not just total store value. Track sell-through rate (units sold ÷ units received), days on hand, and how much cash sits in each mix bucket. If bowls move faster than throws or wall hangings, reorder bowls sooner and trim the slower lines. That keeps working capital from getting stuck in dead stock and protects margin dollars.

Set a cash floor before owner pay. Hold enough for replenishment, shrink, and seasonal gaps, then draw from what remains. One clean rule: buy only what you can reasonably sell before the next seasonal reset. If inventory rises while cash falls, the store may look fine on paper but still starve the owner’s take-home income.

5

Added Revenue Channels

Added Revenue Channels

Added revenue channels can lift owner pay when they add more margin dollars than they add in labor, marketing, packaging, and fulfillment. Workshops are already 150% of the sales mix at $48 per class unit, so classes are part of the core model, not side income. Online orders, custom commissions, local events, gift bundles, and corporate gifts can widen sales beyond walk-in traffic, but each one brings service risk.

The key question is simple: does the channel leave enough cash after artisan payouts, payroll, rent, and overhead? A channel can grow revenue and still hurt take-home income if it ties up inventory, needs extra staff, or creates slow-pay receivables. Here, the best channel is the one that increases contribution without overloading the team or freezing cash in stock.

Track Margin By Channel

Measure each channel on net profit per order, not just sales. Here’s the quick math: track units, average order value, labor minutes, packaging cost, shipping or event fees, and refund risk. For workshops, watch bookings, seat fill, and instructor hours so the $48 class price still leaves room for profit after delivery costs.

Revenue by channel, weekly and monthly

Margin dollars per order, after direct costs

Labor minutes per order or booking

Packaging and fulfillment cost per sale

Inventory days tied up by each channel

Start with channels that reuse current stock and staff time, like online orders and gift bundles. Be careful with custom commissions and corporate gifts; they can raise ticket size but also stretch lead times, service work, and cash flow. If a channel needs extra labor or holds inventory too long, price it higher or keep it small.

6

Handicraft Store Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and strong owner income scenarios

Owner income scenarios

Owner income shifts fast in this store because traffic, conversion, repeat buys, and payroll all move together. The model stays loss-making early, then turns positive as volume builds.

Low, base, and high cases show how owner take-home changes as the store scales.

Scenario

Low CaseDownside case

Base CaseBreakeven path

High CaseUpside case

Launch model

This is the weak start case, where the store still burns cash in Year 1.

This is the modeled case where the store gets to its first profit year.

This is the stronger earnings path if traffic, repeats, and basket size keep compounding.

Typical setup

Year 1 revenue is about $72k and EBITDA is about -$231k, so payroll, rent, and launch spending absorb the early cash.

Year 3 revenue reaches about $533k and EBITDA turns positive at about $76k as conversion and repeat buying improve.

By Year 5, revenue reaches about $2.753M and EBITDA is about $2.084M, but the model needs more staff and inventory to keep up.

Cost drivers

Traffic and conversion

artisan payouts

payroll growth

rent and utilities

POS fees

Visitor growth

conversion rate

repeat customers

product mix

payroll scale

Weekend traffic

repeat orders

units per order

labor buildup

inventory pressure

Owner income rangeBefore owner reserves

-$231kLoss year

$76kFirst profit

$2.084MScale risk

Best fit

Use this to test how much cash cushion you need if demand starts slow.

Use this as the main planning case for owner pay and cash use after launch.

Use this to stress test capacity, hiring, and stock control as demand accelerates.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution policy.

In the Year 1 planning case, the handicraft store keeps about $192K in operating profit before owner distributions, taxes, debt, and reserves That comes from about $498K in revenue, 50% artisan payouts, 32% transaction fees, $582K fixed overhead, and $2065K payroll Owner take-home depends on role, reserves, and cash needs

Owner income stabilizes only after traffic, repeat orders, and inventory turns become predictable The model starts with 4,420 monthly visitors, 35% conversion, and 150% repeat customers in Year 1 By Year 2, conversion rises to 42% and repeat customers to 200%, but payroll also rises from $2065K to $2495K

Not always, but this model assumes staff from the start Year 1 payroll includes a $65K store manager, 15 sales associate FTEs, 05 workshop instructor FTE, 05 marketing coordinator FTE, and 08 admin FTE If the owner fills the manager role, that wage may become owner pay if hired out, it remains payroll

Sales conversion, average order value, payroll, rent, and artisan payout terms matter most In Year 1, the store has a $9580 AOV, 918% contribution after artisan payouts and transaction fees, $3,800 monthly rent, and $172K monthly payroll Small margin changes matter because 1 percentage point on $498K revenue is about $50K

Raise margin dollars without adding fixed cost too fast For this handicraft store, that means improving conversion above 35%, lifting the $9580 AOV with higher-ticket items, keeping rent at $3,800, and making workshops earn their labor cost Online sales and custom orders help only if fulfillment time and inventory cash stay under control

About the author

Charles Bryant

Business Plan Writer

Charles Bryant is a business plan writer at Financial Models Lab who helps founders make sense of startup costs and choose realistic business ideas. He focuses on founder-friendly business numbers, with clear guidance on operating expense planning and startup planning without heavy finance jargon. Charles writes from a practical founder perspective, making complex decisions feel manageable for readers who want useful, realistic insight before they start a business.

Choosing a selection results in a full page refresh.