What expenses reduce handyman business profit margin?

The biggest margin killers in a Handyman Service are technician labor, materials, marketing, fuel, and fixed overhead. In Year 1, direct technician labor is 120% of revenue, then 100% in Year 5, while materials and supplies run 70% to 60%; for startup cost context, see How Much Does It Cost To Open, Start, And Launch Your Handyman Service Business?. Add $4,850/month fixed overhead, payroll rising from $250,000 to $703,000, and $180,000 in launch capex, and owner take-home gets squeezed fast.

A Handyman Service owner makes $90,000/year in founder salary in this staffed model, but early years are cash-heavy, with EBITDA (earnings before interest, taxes, depreciation, and amortization) at -$230,000 in Year 1, -$215,000 in Year 2, and -$33,000 in Year 3. For context, track owner pay beside What Is The Most Important Metric To Measure The Success Of Your Handyman Service?, because profit turns only after Month 32.

Owner Pay

$90,000 annual founder salary

Not an employee wage model

Cash loss lasts three years

Breakeven hits Month 32

Profit Upside

$204,000 EBITDA in Year 4

$715,000 EBITDA in Year 5

Staffed with founder and technicians

Owner labor can replace payroll

How much revenue does a handyman business need to pay the owner?

A Handyman Service needs about $36,900 in monthly revenue to cover a $250,000 Year 1 payroll that includes the owner, plus $4,850 in fixed overhead and $1,250 in monthly marketing. Here’s the quick math: ($20,833 + $4,850 + $1,250) ÷ 0.73 = about $36,900 before capex. If owner pay is $100,000, the revenue need rises a bit, and revenue still isn’t the same as take-home salary.

What drives the need

$20,833 monthly owner-inclusive payroll

$4,850 fixed overhead each month

$1,250 marketing budget monthly

73% contribution margin in Year 1

What this hides

270% direct and variable costs total

100,000 owner pay lifts the target

Revenue is not personal salary

Capex is excluded from this estimate

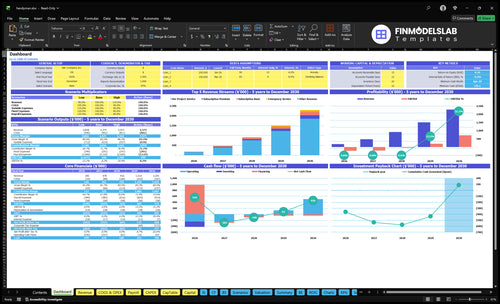

Handyman Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see what drives handyman owner income?

1

Billable Utilization

32 mo

More billable hours per tech spread payroll and vans across more jobs, which is what gets you to break-even and owner take-home.

2

Average Rate

$60-$120

Hourly price sets the top line fast, and the Year 1 rate range shows how one pricing move can swing income without adding headcount.

3

Service Mix

81%-84%

A better mix of basic, premium, project, and emergency work lifts gross margin, so more revenue survives as profit.

4

Labor Model

$250K-$703K

Payroll is the biggest swing item, and tighter staffing keeps labor from eating the revenue you need for EBITDA and owner pay.

5

Overhead Control

$4.85K/mo

Fixed overhead stays in the monthly burn even when jobs slow, so keeping it lean protects cash and makes break-even easier to hit.

6

Repeat Demand

$150-$110

Repeat jobs and denser scheduling cut CAC over time, and that lowers the cost to fill the calendar with paid work.

Handyman Service Core Six Income Drivers

Billable Utilization

Billable Utilization

Billable utilization is the share of technician time that gets paid. It includes repair hours, not estimates, travel, admin, or schedule gaps. In Year 1, the model uses 10 hours for basic subscription work and 40 hours for per-project work. More paid hours at the same hourly rate raise revenue without the same jump in overhead.

If fixed overhead is $4,850 per month, every extra billable hour helps cover it faster and leaves more room for owner pay. Low route density is the main risk because it wastes technician time between jobs. One clean line: empty calendar slots are expensive.

Raise Paid Hours per Tech Day

Track billable hours by service type, plus travel time, admin time, and schedule gaps. The key ratio is paid hours versus available hours. Here’s the quick math: more paid repair time, with the same hourly rate, lifts revenue and contribution margin without adding fixed costs at the same pace.

Measure paid hours by job type.

Flag travel and estimate time.

Group nearby jobs.

Review idle gaps weekly.

Keep an eye on the split between basic subscription work at 10 hours and per-project work at 40 hours. That mix drives capacity, cash flow, and how fast the owner can take profit out. If route density stays thin, payroll gets paid before the schedule does.

1

Average Rate And Job Ticket

Average Rate And Job Ticket

Average job ticket is the revenue per completed repair, and it moves owner pay fast. With rates at $60 basic, $75 premium, $90 per-project, and $120 emergency in Year 1, even small price gains lift gross profit if close rate holds. By Year 5, those rise to $65, $80, $95, and $125, so the business can keep pace with wage and cost pressure without adding many more jobs.

This driver depends on service mix, call conversion, minimum charges, and whether the market accepts flat-rate repair pricing. The main risk is simple: overpricing lowers bookings. If labor and materials stay controlled, higher effective pricing flows straight into gross profit, cash available for overhead, and the owner’s draw.

Track Rate by Job Type

Measure realized rate, not just quoted rate. Track completed jobs, average ticket, close rate, discounts, callback credits, and materials as a share of revenue. If the basic plan sells at $60 but discounts pull the realized rate down, the headline price does not help income.

Test minimum charges on small repairs and flat-rate pricing on repeatable jobs where local demand supports it. A clean rule is to protect margin first: raise price only when demand is stable and crews stay booked, then watch bookings, conversion, and owner cash draw each week.

Track quoted vs. realized price.

Watch close rate by service type.

Set minimum charges for small jobs.

Use flat rates for repeatable work.

Flag booking drops after price tests.

2

Service Mix And Materials Margin

Service Mix And Materials Margin

Income changes by job type because each service uses different labor hours, rates, and material loads. In Year 1, per-project work models 40 billable hours at $90, while emergency work models 20 hours at $120. Materials and supplies run 70% of revenue in Year 1, so the same top line can still leave thin profit if the mix skews to parts-heavy repairs like drywall, fixtures, or minor carpentry.

The owner’s take-home income rises when the mix shifts toward jobs with stronger labor spread and tighter material control. By Year 5, materials drop to 60% of revenue, but poor tracking can erase that gain. Track revenue, hours, labor, and material cost by job type; otherwise, you can stay busy and still end up with low gross margin and weak cash for pay draws.

Measure Job Margin By Service

Use job-level margin reports, not just monthly sales. Split subscription visits, repairs, and emergency calls, then compare hours booked, material spend, and gross profit on each one. The quick check is simple: if a job type needs lots of parts and time, it should carry a higher price or it will drag owner income.

Track labor hours by job.

Track parts by ticket.

Flag 70% material jobs.

Price emergency work higher.

Watch gross margin by service.

3

Labor Model And Technician Leverage

Technician Payroll Discipline

Direct technician labor is the main brake on owner income. Payroll rises from $250,000 in Year 1 to $703,000 in Year 5, while direct technician labor runs at 120% to 100% of revenue. That means booked work has to cover wages first, or gross margin goes negative before overhead and owner pay.

The inputs are booked hours, route density, hourly rate, and callback rate. If hiring comes before demand, EBITDA (earnings before interest, taxes, depreciation, and amortization) turns negative fast. Idle hours are expensive.

Hire on booked work, not hope

Track booked hours per technician, plus drive time and rework. Use staffing triggers tied to confirmed work, not future leads. When route density is weak, paid time leaks into travel and admin, and labor stays above the revenue it should support.

Watch booked hours weekly.

Cap overtime before hiring.

Cut callbacks fast.

Compare payroll to booked work.

Only add headcount when recurring jobs can cover the next wage step, including the move from $250,000 to $405,000, $503,000, $653,000, and $703,000. That protects cash flow and keeps room for owner draw instead of turning growth into a payroll problem.

4

Overhead And Cost Control

Overhead Load

Overhead is the cost stack that keeps running when the calendar has gaps. With $4,850 per month in fixed costs for rent, utilities, insurance, software, accounting, supplies, and website hosting, the business must cover $58,200 a year before owner pay. Add marketing at 50% to 40% and vehicle fuel and maintenance at 30% to 20%, and thin months can wipe out profit fast.

One clean rule: if booked work slips, fixed costs still hit the bank account. Repairs, tools, slow months, and callbacks need cash reserve support, or the owner ends up funding the business from personal income. That’s where overhead hurts most: before breakeven, it can crush take-home pay even when jobs are still coming in.

Control the Cost Stack

Track the monthly spend that matters: fixed overhead, marketing as a share of sales, fuel and maintenance, and reserve cash. Use those numbers to set a hard cap on what the business can carry before owner draw gets squeezed. If overhead rises faster than booked work, cash flow weakens first and profit follows.

$4,850 fixed overhead target

50% to 40% marketing range

30% to 20% fuel and maintenance range

Reserve for repairs and callbacks

Here’s the practical move: review these costs every month, not just at tax time. Cut any spend that doesn’t create booked jobs, and keep enough reserve to cover slow weeks without missing rent or payroll-related bills. If overhead stays flat while revenue grows, owner income has room to rise.

5

Repeat Demand And Scheduling Density

Repeat Demand and Route Density

Repeat demand and scheduling density means the same customers book routine checks, subscriptions, and follow-on repairs, so crews spend less time chasing leads, driving between jobs, and handling unpaid admin. The key inputs are repeat-customer count, jobs per account, travel minutes, and CAC. In the model, CAC falls from $150 in Year 1 to $110 in Year 5, which lifts cash flow because each booked job carries more margin.

This driver works best with property managers, real estate investors, and recurring home-maintenance routes. Subscription basic allocation rises from 300% to 450%, and premium from 100% to 250%, so more revenue comes from planned visits instead of one-off calls. If routes stay dense, owner pay improves; if jobs spread out, travel and idle time eat profit fast.

Build Dense Recurring Routes

Track repeat booking rate, jobs per account, and travel minutes per stop. One clean metric is revenue per route hour: more repeat work should push that up without adding much overhead. If a route adds jobs but not density, the extra miles and admin can erase the gain. The goal is simple: fill the day with nearby booked work, not scattered one-offs.

Price subscriptions so routine visits cover base labor, then use per-project and emergency work to lift ticket size. Compare CAC, route fill, and gross margin by customer type each month. When recurring accounts book again faster, the business gets steadier cash and the owner can draw profit sooner instead of waiting for new lead flow.

6

Handyman Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare handyman owner income scenarios without promising outcomes

Owner income scenarios

Owner income swings hard here because payroll, fixed overhead, and launch capex eat cash before the business scales. The later cases only work once staffing and demand are steady.

Compare owner income across the early ramp, breakeven, and mature staffed cases.

Scenario

Low CaseCash-heavy

Base CaseNear breakeven

High CaseDistribution-capable

Launch model

The early ramp case keeps founder pay in place while EBITDA stays at -$230,000.

The modeled case reaches Month 32 breakeven timing, but Year 3 EBITDA is still -$33,000.

The stronger case turns cash-generative, with Year 4 EBITDA at $204,000 and Year 5 EBITDA at $715,000.

Typical setup

Year 1 includes a $90,000 founder salary, about $250,000 payroll, $58,200 of annual fixed overhead, and $180,000 of launch capex.

Payroll reaches $503,000, marketing budget rises to $50,000, and the business is close to covering itself but not ready for strong distributions.

Payroll moves to $653,000 to $703,000, the team is fully staffed, and owner distributions can start after reserves and reinvestment.

Cost drivers

Founder salary $90,000

payroll $250,000

fixed overhead $58,200

launch capex $180,000

EBITDA -$230,000

Month 32 breakeven

Year 3 EBITDA -$33,000

payroll $503,000

marketing budget $50,000

Year 4 EBITDA $204,000

Year 5 EBITDA $715,000

payroll $653,000 to $703,000

mature staffing

reserves first

Owner income rangeBefore owner reserves

Salary onlyLoss phase

Near break-evenBreakeven zone

Distribution windowScale-up window

Best fit

Use this to stress-test the opening year when cash is tight and owner distributions should wait.

Use this as the core planning case for steady operations with limited owner draws.

Use this to test upside once demand is steady and the business can fund growth plus owner pay.

!

Planning note: These ranges are researched planning assumptions based on the model, not guaranteed earnings, salary promises, tax advice, or distributions.

This model pays the founder a $90,000 annual salary, but the company has negative EBITDA until after Month 32 EBITDA moves from -$230,000 in Year 1 to $204,000 in Year 4 and $715,000 in Year 5 Extra owner distributions depend on cash, reserves, debt, and reinvestment

The researched model reaches breakeven in Month 32, with a 32-month payback period That timing reflects $180,000 of launch capex, $250,000 of Year 1 payroll, and $4,850 in monthly fixed overhead If bookings ramp slower, the owner needs more cash cushion

No, but this model is built as a staffed handyman company It starts with a founder, one lead technician, and two technicians, then grows to eight field staff by Year 5 Hiring increases capacity, but payroll rises from $250,000 to $703,000, so utilization has to keep up

Billable utilization, pricing, labor cost, and overhead drive owner take-home Year 1 gross margin is 810% after direct labor and materials, but fixed overhead, payroll, marketing, vehicles, and capex still create -$230,000 EBITDA Better route density and repeat work help turn hours into cash

Start with salary, then add distributions only after reserves are funded This model uses a $90,000 founder salary, a $145,000 minimum cash point, and Month 32 breakeven Treat EBITDA as capacity, not automatic take-home, because vans, tools, callbacks, taxes, and growth spending still need cash

About the author

Andrew Brooks

Business Model Writer

Andrew Brooks writes about business model economics and the day-to-day realities of running a new venture for Financial Models Lab. As a business model writer, he helps founders planning a physical location work through startup planning and the money questions that come up before opening, without heavy finance jargon. His work focuses on showing what it really takes to turn an idea into a workable business.

Choosing a selection results in a full page refresh.