Heat Exchanger Cleaning Owner Income: $180K And $22M

Key Takeaways

Contract volume steadies income but strains crews and cash.

Higher job values only work when costs are priced in.

Full calendars lift margin; idle crews crush EBITDA.

Better customer mix boosts value, but one account is risky.

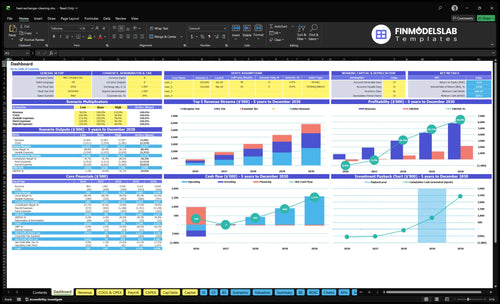

Owner income$180KNet margin37%Revenue for target pay$864KBusiness difficultyHard

Want to test your owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on demand, pricing, payroll, reserves, and financing.

How do recurring contracts and shutdown work change owner income?

For a Heat Exchanger Cleaning Service, recurring contracts make owner income steadier because Year 1 pricing starts at $3,500 Essential, $7,500 Pro, and $15,000 Enterprise per month. Here’s the quick math: as the mix shifts from 20% Enterprise in Year 1 to 30% in Year 5, the weighted monthly price rises from about $7,200 to about $9,810, so baseline cash improves. Shutdown and emergency work can add revenue fast, but it also brings overtime, fast mobilization, safety demands, and receivable risk.

Recurring contracts

Essential: $3,500 per month

Pro: $7,500 per month

Enterprise: $15,000 per month

Stabilizes baseline owner income

Shutdown work risk

Raises revenue during plant outages

Triggers overtime and fast mobilization

Increases safety and receivable risk

One large plant can swing cash flow

What is a realistic heat exchanger cleaning profit margin?

A realistic margin for a Heat Exchanger Cleaning Service is strong at the job level but much tighter after overhead; direct margin improves from 81% in Year 1 to 85% in Year 5. For the planning side, see How To Write A Business Plan For Heat Exchanger Cleaning Service? and treat labor, overtime, waste handling, safety compliance, insurance, mobilization, and equipment use as the real squeeze. On the provided numbers, $2,157M EBITDA on $5,844M revenue is about 36.9% EBITDA margin, while Year 1 is negative.

Job margin drivers

Consumables and waste disposal: 11% to 9%

Field travel and logistics: 8% to 6%

Direct margin rises from 81% to 85%

High-ticket work still needs tight cost control

Net income reality

Year 1 EBITDA is negative

Year 5 EBITDA is $2,157M

Year 5 revenue is $5,844M

That implies about 36.9% EBITDA margin

What revenue is needed to pay a heat exchanger cleaning business owner?

If you want a $180K owner salary in a Heat Exchanger Cleaning Service, the business has to cover direct costs, payroll, marketing, equipment, reserves, and fixed overhead first. The model shows $864K of Year 1 revenue still leaves -$294K EBITDA, and breakeven does not arrive until Month 10. It also runs at 81% to 85% gross margin after consumables and logistics, with room needed for $237K minimum cash and $332K capex.

Owner pay math

$180K modeled owner salary

$864K Year 1 revenue

-$294K EBITDA after staffing

Month 10 breakeven

Cash guardrails

81% to 85% gross margin

$252K monthly overhead before payroll

$237K minimum cash reserve

$332K capex reserve

Heat Exchanger Cleaning Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main income drivers?

1

Contract Volume

$864K-$5.8M

More contracts spread fixed overhead and sales cost across more work, so owner income rises fastest when volume climbs.

2

Job Value

$3.5K-$17K

Higher per-job pricing lifts revenue without adding the same amount of labor or travel.

3

Crew Utilization

2-10 FTE

Keeping the field team busy turns payroll into billable work and protects cash.

4

Direct Margin

81%-85%

Every point of direct margin drops straight to EBITDA once overhead is covered.

5

Fixed Overhead

$302K/yr

Rent, insurance, fleet, software, and training set the floor for monthly cash burn.

6

Tier Mix

20%-30%

Shifting more work into Pro and Enterprise raises average revenue and improves take-home.

Heat Exchanger Cleaning Service Core Six Income Drivers

Contract Volume

Recurring Contract Volume

Recurring cleaning contracts set the floor for owner income. Here’s the quick math: weighted monthly contract value starts near $7,200 in Year 1 and rises near $9,810 in Year 5, while revenue grows from $864K to $5.844M. More signed agreements lift cash flow and reduce volatility, so the owner can take a steadier draw.

The catch is capacity. More contracts can strain crews, equipment, and working capital, and replacement sales are costly, with CAC falling from $6,000 to $4,000 over the model period. If service frequency slips, retention drops and the recurring base gets weaker fast.

Track Contract Load

Measure contract count, weighted monthly value, renewal rate, and service frequency together. The useful formula is simple: contract volume × monthly value = baseline revenue. If new contracts raise sales but overload crews, profit and owner pay can fall even as top-line revenue grows.

Track revenue by active contract.

Watch renewal and churn monthly.

Match crew hours to schedule density.

Test frequency before discounting.

Forecast cash before adding accounts.

1

Average Job Value

Average Job Value

Average job value is the average invoice you collect for one heat exchanger cleaning job. It shifts with exchanger size, fouling severity, cleaning method, access, turnaround timing, mobilization, and risk tier. Tier prices start at $3,500, $7,500, and $15,000 per month in Year 1, then rise to $3,900, $8,300, and $17,000 by Year 5.

Higher average value helps only when the added price covers labor hours, waste disposal, travel, and safety work. Here’s the quick math: price minus direct cost drives cash and owner pay. A weak quote can still lift revenue, but if overtime or site handling rises faster, gross margin falls and take-home income shrinks.

Price by site risk

Build each quote from the job facts, not a flat rate. Measure realized average job value against direct cost so you know whether the extra ticket size is real profit or just more work. If access is tight or turnaround is short, add the cost before you send the quote, not after the crew is already on site.

Track price by risk tier.

Log labor hours and waste.

Requote sites after access changes.

Use those numbers to set minimums for shutdown work, add mobilization fees, and protect margin on hard-to-reach exchangers. That keeps average job value high enough to cover recurring field costs and leaves more cash for owner draws.

2

Crew Utilization

Crew Utilization

Utilization is the share of paid crew time spent on billable heat exchanger cleaning work. With staffing rising from 2 Senior Field Technicians in Year 1 to 10 in Year 5 at $85K each, annual field payroll reaches $850K. Full calendars spread payroll and equipment costs across more revenue, so owner take-home only improves when crews stay busy.

Idle labor drags EBITDA, but overtime can backfire through fatigue, safety risk, and rework. The main inputs are scheduled shutdowns, active jobs, travel time, and billable hours. One empty week still carries the same fixed labor and equipment burden, so margin can fall fast even when sales look strong.

Fill Shutdown Weeks First

Track utilization by technician each week: billable hours, overtime, and rework. Here’s the quick math: if the crew is paid but not billing, profit shrinks fast, so book plant shutdown work first and fill gaps with nearby preventive jobs. Keep the schedule dense, but stop before overtime turns into quality loss.

Use the shutdown calendar as the planning tool. Compare planned jobs to crew capacity and $85K salaries, then watch for weak months early. If utilization drops, slow hiring or tighten scheduling; if it runs too hot, add crew before fatigue raises rework and delays cash collection.

3

Direct Job Margin

Direct Job Margin

Direct job margin is the cash left after cleaning consumables, waste disposal, field travel, and technician logistics. In Year 1, consumables and disposal run 11% of revenue and travel/logistics run 8%, so direct margin lands at 81%. By Year 5, those costs ease to 9% and 6%, pushing direct margin to 85%.

That 4-point lift matters because it is the pool that still has to cover payroll, marketing, insurance, rent, safety training, fleet maintenance, and owner pay. One-line math: if direct costs creep up on a job, take-home income drops before the owner sees it. Waste handling and mobilization can swing job profit fast.

Price the Job, Not the Hour

Build quotes from separate cost lines: consumables, disposal, travel, and logistics. Then compare quoted margin with actual margin after each job closes. A margin target of 81% to 85% only works if the field team keeps those direct costs inside the estimate.

Track long-drive jobs and special waste jobs first, because they are the fastest margin leaks. If mobilization or disposal keeps overrunning, raise the price, narrow the scope, or cut travel distance. That protects cash flow and leaves more gross profit for owner draw.

4

Equipment And Compliance Overhead

Equipment Load

This driver is the cost of keeping cleaning gear, vehicles, and safety systems ready to bill. Launch capex totals $332K: $150K service vehicles, $85K hydro-blasting units, $45K ultrasonic systems, $25K diagnostic tools, $15K racking and safety gear, and $12K IT. If that gear sits idle, owner take-home drops because revenue has to cover the asset base first.

Monthly fixed overhead is $252K for rent, insurance, fleet, software, safety training, utilities, and telecom. Here’s the quick math: if billable work does not keep crews and equipment busy, that cost stays flat while profit shrinks. The key input is utilization, meaning how much of the fleet and tools are on paid jobs, not parked in the yard.

Track Utilization

Track billable days per truck, tool downtime, and compliance spend per job. Tie each job to the equipment used, travel time, safety checks, and cleanup cost, then compare that to the contract price. If a job does not cover its share of the $252K/month overhead, it hurts owner pay even if the invoice looks fine.

Billable truck days

Hydro-blast hours used

Ultrasonic hours used

Safety training cost

Fleet downtime

Job margin by method

Use a monthly capacity plan so the expensive gear stays on paid work. That means matching vehicle count, shutdown timing, and compliance scheduling to booked contracts, not hoped-for demand.

5

Customer Mix

Customer Mix

Customer mix is the share of Enterprise, Essential, shutdown, and emergency work in the book. When Enterprise rises from 20% in Year 1 to 30% in Year 5, while Essential falls from 45% to 25%, weighted monthly contract value climbs from about $7,200 to $9,810, which supports revenue growth and steadier owner pay.

Here’s the risk: shutdown cleaning and emergency calls can price higher, but they also bring scheduling pressure, overtime, site compliance, and slower receivables. If one facility starts controlling the calendar, cash flow gets lumpy fast, so the real test is not just revenue, it’s how much of that revenue turns into cash on time.

Track mix by segment

Measure the book by customer type, job type, and collection speed. Track Enterprise %, Essential %, shutdown and emergency share, monthly contract value, and days to collect. That shows whether growth is improving revenue quality or just adding noisy, hard-to-serve work.

Cap one site’s calendar share.

Price overtime and compliance upfront.

Watch receivables after emergency work.

Test mix shifts in the forecast before you accept more high-pressure jobs. If higher-price work raises overtime or delays payment, owner draw can fall even when sales rise.

6

Heat Exchanger Cleaning Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: compare low, base, and high owner-income outcomes using model-backed assumptions

Owner income scenarios

Owner income swings with ramp speed, staffing, and overhead. Early months can miss payback, while later years can fund salary and leave room for profit draw.

Low, base, and high cases show how scale changes owner pay.

Scenario

Low CaseRamp Risk

Base CaseModel Case

High CaseScale Upside

Launch model

The low case assumes an early ramp, with Year 1 at $864K revenue and negative EBITDA.

The base case assumes the model reaches Year 3 scale, with $3.038M revenue and positive EBITDA.

The high case assumes full-year scale in Year 5, with $5.844M revenue and strong EBITDA.

Typical setup

This looks like 2 technicians, $120K marketing, 81% direct margin, and the owner only taking salary if cash funds it.

This is the funded operating plan: 6 technicians, 83% direct margin, $180K owner salary, and enough volume to cover overhead.

This is the mature setup: 10 technicians, 85% direct margin, $180K owner salary, and enough spread to absorb overhead and reserves.

Cost drivers

Year 1 revenue ramp

81% direct margin

$120K marketing

2 technicians

fixed overhead

Year 3 revenue scale

83% direct margin

6 technicians

overhead coverage

owner salary

Year 5 revenue scale

85% direct margin

10 technicians

overhead spread

equipment reserve

Owner income rangeBefore owner reserves

$0 - $180,000Salary at risk

$180,000Funded salary

$180,000+Profit upside

Best fit

Use this to stress-test cash burn, hiring pace, and whether the owner can pay themselves in year one.

Use this as the core planning case for hiring, pricing, and cash needs.

Use this to test upside if utilization stays high and the team keeps growing without margin slip.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; EBITDA is before personal taxes, debt, and owner draws.

The model includes a $180,000 annual CEO and Operations Lead salary That is not the same as free cash Year 1 EBITDA is -$294K on $864K revenue, so distributions are not supported in the early ramp By Year 5, EBITDA reaches $2157M on $5844M revenue before taxes, debt service, reserves, and owner distributions

The model reaches breakeven in Month 10 and payback in 41 months The cash low point is Month 18, with a $237K minimum cash need That means the owner can see operating traction before the business has fully repaid startup investment and working capital needs

Not always, but early-stage field involvement can protect margins and job quality Year 1 staffing includes 2 Senior Field Technicians, 1 Sales and Account Manager, 1 Administrative Support role, and the owner-operator role at $180K If the owner stays out of the field, supervision, scheduling, and technician productivity must be stronger

Direct margin, crew utilization, and contract mix move profit the most Direct costs start at 19% of revenue, made up of 11% consumables and waste disposal plus 8% field travel and logistics Fixed overhead adds $252K per month before payroll, and launch equipment totals $332K

A mix with recurring maintenance and selected shutdown work is usually stronger than chasing only emergency jobs The model shifts from 45% Essential, 35% Pro, and 20% Enterprise in Year 1 to 25%, 45%, and 30% by Year 5 That improves average contract value while keeping some revenue predictable

About the author

Owen Clarke

Small Business Consultant

Owen Clarke is a small business consultant at Financial Models Lab who writes about everyday business finance and business plan basics for founders building a simple plan before investing money. He focuses on realistic assumptions and startup costs, bringing a practical founder perspective to help readers make grounded, real-world decisions.

Choosing a selection results in a full page refresh.