How Much Does a Hookah Lounge Owner Make? $173M EBITDA Case

On these researched assumptions, hookah lounge owner profit starts from $173M in first-year EBITDA on $354M in revenue That equals a 489% EBITDA margin before owner taxes, debt service, reserves, reinvestment, and distributions By the fifth year, the model reaches $870M in revenue and $588M in EBITDA Treat this as planning cash flow, not a promised hookah bar owner salary

Owner income$1.73M-$5.88MNet margin48.9%-67.5%Revenue for target pay$78kBusiness difficultyMedium

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margin, payroll, debt, reserves, and how much cash the business keeps back. Not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the model?

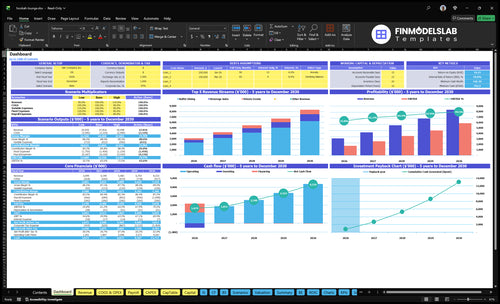

The dashboard shows revenue, EBITDA, cash, breakeven, payback, and owner take-home for Hookah Lounge. Open the Hookah Lounge Financial Model Template to see the assumptions behind covers, average order value, sales mix, COGS, variable costs, fixed costs, wages, capital expenses, and scenarios.

Owner-income model highlights

$354M Year 1 revenue

$173M Year 1 EBITDA

Minimum cash: $762k

Breakeven in Month 2

5-month payback

Is owning a hookah lounge profitable?

Yes, a Hookah Lounge can be profitable, but only with strong volume, tight lease control, and strict compliance. The model shows $173M Year 1 EBITDA, a $762k minimum cash need, Month 2 breakeven, 5-month payback, 1923% ROE, and 0.35% IRR. The catch is simple: smoking laws, city permits, ventilation, fire safety, late-night staffing, security, utilities, and rent can flip the math fast, and cutting payroll often means the owner works shifts.

Profit drivers

Month 2 breakeven is fast.

5-month payback is aggressive.

$173M Year 1 EBITDA is the upside.

1923% ROE shows high return potential.

Main risks

Smoking laws can block openings.

Permits and fire rules add delays.

Ventilation and utilities raise costs.

Owner shifts may replace passive income.

What hookah lounge profit margin should an owner watch?

For a Hookah Lounge, watch owner cash margin—the money left after all bills—not just gross margin; the listed Year 1 model shows 135% COGS, so gross margin is -35%, and you should sanity-check startup spend with How Much Does It Cost To Open A Hookah Lounge? before you price. After 30% marketing and supplies, $490k payroll, and $2.916M fixed costs, the cash picture is already strained.

Watch Cash Margin

135% COGS means -35% gross margin.

120% food ingredients drive most cost.

15% beverage ingredients add more pressure.

Track cash after payroll and fixed costs.

Add Every Cost

30% of revenue goes to marketing and supplies.

$490k payroll equals 138% of revenue.

$2.916M fixed costs equal 82% of revenue.

Add tobacco, charcoal, hoses, tips, bowls.

How much revenue does a hookah lounge need to pay the owner?

Owner pay only works after the Hookah Lounge clears fixed costs and payroll. At an 83.5% contribution margin, the model breaks even at about $78k per month before owner pay, with $243k in monthly fixed expenses and about $408k in monthly payroll, or $651k total fixed payroll load. Every extra $10k of monthly owner target pay needs about $12k more revenue before taxes and reserves, and the core case reaches Month 2 breakeven.

Owner pay math

$78k monthly break-even

$651k fixed payroll load

$10k pay needs $12k more revenue

Month 2 breakeven in the core case

What drives the target

83.5% contribution margin helps

$243k fixed expenses are monthly

Rent sits inside fixed costs

Keep reserves above owner pay

Hookah Lounge Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Guest Volume

1,560/wk

More covers push revenue and EBITDA faster, and the model starts at 1,560 weekly Year 1 covers.

2

Average Spend

$4.4K

Higher spend per guest lifts take-home without the same jump in labor, so small ticket gains matter.

3

COGS Load

135%

Food and drink cost pressure hits profit fast, so better margin flows straight to owner cash.

4

Payroll Mix

$490K

Payroll is a large cost block, so tighter staffing and shift control improve EBITDA and payback.

5

Fixed Overhead

$243K/mo

Rent, utilities, insurance, and security set the break-even line, so lower fixed burn raises cash.

6

Private Events

10%

Private events add higher-value hours and help fill slow periods, which lifts total take-home.

Hookah Lounge Core Six Income Drivers

Customer Volume And Table Turnover

Customer Volume And Table Turnover

When covers are weak, the room can still look busy and the owner can still miss cash. This model starts at 1,560 weekly covers in Year 1 and doubles to 3,120 weekly covers by Year 5, so income depends on how fast seats turn, not just how full the lounge feels.

Here’s the quick math: at the disclosed Year 1 weekly revenue of $681k, each extra 100 weekly covers at the Year 1 blended $4,365 spend adds about $227k a year before costs. What this hides is session length and weekday softness; a long stay in a peak seat can block two shorter, higher-value turns.

Track Covers Per Seat

Measure covers by day, hour, and table size. A seat that turns twice on Friday is worth more than one held too long on Tuesday, so track peak-hour capacity, wait times, and average session length by shift.

Test reservations, time limits, and pacing so turnover rises without hurting the guest experience. If extra covers come from off-peak hours, they help profit; if they crowd peak hours, they can lift labor and cut the owner’s draw.

1

Average Ticket And Session Pricing

Session Price and Ticket Mix

This driver is the price per session: $35 midweek and $50 weekend in Year 1, rising to $45 and $60 by Year 5. It matters because price lifts revenue without adding seats. The disclosed model says a $1 increase across 1,560 weekly Year 1 covers adds about $811k annual revenue before costs, so price moves can change owner pay fast.

Average ticket also includes upsells like premium flavors, fruit heads, food, nonalcoholic drinks, retail add-ons, and group packages. Count alcohol revenue only where licensing and local rules allow it. If higher prices hurt repeat visits or shrink basket size, take-home income can fall even when posted sales look better.

Lift Ticket Without Losing Demand

Track ticket by daypart, party size, and upsell attach rate. Compare weekday, weekend, and event checks separately. If weekend demand is strong, test that price first; if midweek is soft, use bundles or add-ons before discounting. One clean rule: protect margin before chasing volume.

Build a simple sheet with base session price, add-on price, and local alcohol rules. Test one change at a time so you can see if revenue is real or just mix shift. Watch gross sales, comps, and labor per cover; if labor rises faster than ticket, owner draw gets squeezed.

2

Gross Margin And COGS

Gross Margin and COGS

Gross margin here lives or dies on product cost control. Year 1 COGS are 135% of revenue, made up of 120% raw food ingredients and 15% beverage ingredients, then easing to 110% by Year 5. That means waste, over-portioning, and bad pricing hit owner pay fast.

Here’s the quick math: a 1-point COGS change on Year 1 revenue moves EBITDA by about $354k before tax effects. Put tobacco, charcoal, foil, hoses, tips, bowls, and beverage costs in COGS if they are product costs; keep rent, payroll, and compliance overhead out of it.

Track Product Cost Mix

Measure COGS by menu line and service period. Use food usage, beverage pour cost, and hookah supply counts to spot where margin leaks. If the lounge sells food and drinks together, separate product costs from labor so you can see true gross margin and protect cash for owner draws.

Split food, beverage, and hookah supplies.

Recount spoilage and comped items weekly.

Forecast COGS against sales mix.

3

Labor Model And Owner Role

Labor Mix and Owner Role

Year 1 payroll is $490k, or about $40.8k per month, across the manager, head chef, kitchen staff, servers, hosts, dishwashers, and cleaners. By Year 5 it rises to $845k ($70.4k per month) as staffing scales. If the owner works shifts, payroll can drop, but the owner’s time becomes part of the labor model.

Hired managers make income less hands-on, but they also take cash out before the owner pays themselves. The key inputs are manager coverage, server count, kitchen labor, coal runners, bartenders if licensed, and security. If coverage is thin, service slips; if staffing is heavy, profit gets squeezed.

Track Coverage Per Sales Day

Build the schedule from demand, not habit. Track labor by role, shift, and sales day, then compare payroll to covers and ticket size. Use the owner on peak shifts only if that lowers paid hours more than it raises fatigue or service risk.

Test whether one manager can cover the floor without breaking service. Watch labor creep in slow weeks, because a fixed $490k Year 1 payroll leaves little room for weak traffic. Add bartenders and security only when licensing, late hours, or events justify the cost.

4

Rent, Licensing, And Compliance Costs

Rent, Licensing, And Compliance Costs

Fixed costs are $243k per month before payroll, or $2.916M per year. That includes $15k rent, $35k utilities, $12k insurance, $900 security, and $1k accounting and legal. These costs hit cash every month, so they push break-even up fast and leave less room for owner draw when sales are uneven.

Compliance also matters because smoking rules, tobacco permits, ventilation, fire safety, and business licenses change by city and state. Leasehold improvements are $100k, and listed capital expenses total $510k, so the opening cash burden is already heavy. If a permit delay or code fix adds cost, the owner’s take-home drops before the lounge fully ramps.

Control The Fixed-Cost Stack

Track fixed spend as monthly cash burn and fixed cost per cover. Here’s the quick math: every extra $10k per month in overhead adds $120k per year to break-even. Keep each license, inspection, and renewal in one calendar, and tie any build-out spend to the permit path so you do not pay twice for delays or rework.

Stress-test the model before signing space. Check the city’s smoking, ventilation, and fire rules, then compare rent, utilities, and insurance against expected covers. If fixed costs stay at $243k per month, the business needs strong weekly volume just to clear overhead, so the owner should cap nonessential spending and protect cash for the first months of operation.

5

Operating Hours, Events, And Repeat Visits

Late-Night Covers and Events

Weekend covers are 900 of 1,560 weekly covers, but weekend revenue is only $45k of $681k because tickets are higher. That means the income driver is not just traffic; it’s the mix of late-night, reservation, and event checks. Private events at 10% of sales can add meaningful top-line revenue, but only if they fill dead hours and don’t cannibalize normal seat turns.

Added hours only help if the extra sales cover labor, security, utilities, cleaning, and permit limits. Here’s the quick math: if a late-night block adds revenue but also adds staffed hours and cleanup, the owner keeps less cash unless the ticket size and event fee are high enough. One weak night can erase the margin from several good dinner shifts.

Track Dayparts and Repeat Visits

Measure revenue by daypart: weekday, weekend, late-night, and private event. Track covers, average check, and labor hours for each block so you can see which hours pay for themselves and which ones just add payroll. Reservations and loyalty traffic matter most when they lift midweek utilization without heavy discounting.

Use a simple rule: keep the event deposit, minimum spend, and staffing plan tied to the expected check. If repeat visits are strong, protect them with a clean booking process and consistent service. If onboarding or event setup is slow, no-shows and low turn rates will hit cash flow fast.

Track covers by hour.

Compare check size by day.

Price event minimums above added costs.

Watch labor and cleanup per shift.

6

Hookah Lounge Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high owner-income cases

Owner income scenarios

Owner income changes with weekend traffic, average cover, and staffing load. Breakeven lands in Month 2, minimum cash dips to $762k, and compliance risk can change take-home.

Low, base, and high cases show how earnings shift as traffic and staffing scale.

Scenario

Low CaseBreakeven Month 2

Base CaseCash floor $762k

High CaseCompliance risk

Launch model

Year 1 is the lean case, with lower cover counts and the weakest modeled earnings.

Year 3 is the modeled base case, with stronger traffic and a better spread of fixed costs.

Year 5 is the stronger-earnings case, with the busiest traffic and the highest modeled earnings.

Typical setup

Midweek traffic is light, weekends carry most sales, and the $490k payroll plus annual fixed overhead still pressure cash.

Weekend volume is steadier, staffing has scaled to support more sales, and payroll reaches about $695k.

Friday to Sunday demand is heaviest, staffing is at full buildout, and payroll reaches about $845k.

Cost drivers

Weekday traffic

weekend check size

payroll load

rent and utilities

sales mix

Cover growth

average order value

payroll scaling

food and beverage mix

fixed overhead

Peak-night traffic

higher check size

event mix

full payroll

compliance controls

Owner income rangeBefore owner reserves

$1.73MBreakeven path

$3.53MSteady path

$5.88MUpside case

Best fit

Use this to stress-test the launch month and cash needs.

Use this as the core planning case for Year 3 operations.

Use this to test what happens if the lounge runs near full capacity.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Owner take-home starts with business cash flow, not a fixed paycheck This model shows $173M in first-year EBITDA on $354M revenue, but that is before owner taxes, debt service, reserves, and reinvestment If the lounge keeps cash for repairs, permits, inventory, or growth, distributions will be lower

This model reaches breakeven in Month 2 and shows a 5-month payback That result depends on opening volume, lease timing, permits, staffing, and launch cash The model also requires $762k of minimum cash, so early breakeven does not remove the need for a strong cash cushion

Not always, but the model includes a restaurant manager at $75k per year from the start Removing that role may improve reported profit, but only if the owner works those shifts That can turn payroll savings into unpaid owner labor, so it’s not the same as passive income

Customer volume, average ticket, payroll, rent, and COGS move profit the most Year 1 has 1,560 weekly covers, a $4365 blended average ticket, 135% COGS, $490k payroll, and $243k monthly fixed costs Smoking rules, permits, and ventilation can also change costs by market

Fill more peak-hour tables before adding fixed costs In Year 1, every 100 added weekly covers at the $4365 blended ticket adds about $227k in annual revenue before costs Private events also matter because they are modeled at 10% of sales, but added hours must cover labor, security, and utilities

About the author

Philip Stone

Business Model Writer

Philip Stone is a business model writer at Financial Models Lab, focused on the economics behind day-to-day business operations. He explains startup planning in plain language, helping aspiring small business owners think through the money questions new founders ask. With a clear, grounded approach, he helps readers compare business opportunities realistically and choose ideas that fit their goals without getting lost in heavy finance jargon.

Choosing a selection results in a full page refresh.