How Much Can an Import Export Training Owner Make: $145K Plus

An import export training program owner can plan around a modeled $145,000 annual operator salary if they fill the executive director role, plus any later distributions the business can afford after reserves and reinvestment In the researched assumptions, revenue is $3818M in Year 1 and EBITDA is $2432M, so profit exists on paper before taxes, debt service, reserves, and owner distributions EBITDA margin moves from about 637% in Year 1 to 806% in Year 5 as occupancy rises from 45% to 85% These are planning scenarios, not promised take-home pay

Owner income$145K/yrNet margin63.7%Revenue for target pay$3.8M/yrBusiness difficultyHard

Want to test your owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual take-home changes with enrollment, pricing, payroll, taxes, debt, and reinvestment.

Want to check owner income in the forecast model?

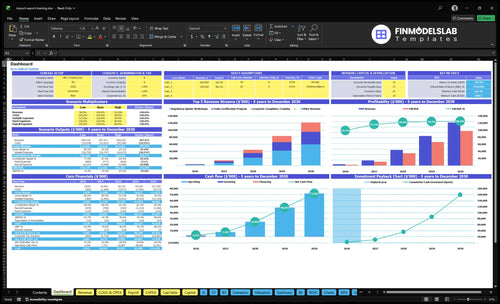

This screenshot shows the dashboard, enrollment, tuition, costs, reserves, and owner income tabs. Year 1–5 revenue runs from $3.818M to $121.538M, EBITDA from $2.432M to $97.951M, occupancy from 45% to 85%, and Month 1 breakeven; open the Import Export Training Program Financial Model Template.

Owner-income model highlights

Owner income output shown

Revenue and EBITDA rise

Occupancy assumptions to 85%

How much should an import export training program charge?

An Import Export Training Program should charge about $450 for the main trade fundamentals program, $350 for corporate compliance training seats, and $125 for regulatory update workshops in Year 1. By Year 5, those prices can rise to $550, $450, and $185 if employer-paid seats and private workshops lift revenue per sale. Retainer-style compliance education can smooth demand, but only if refund risk, instructor load, and marketing cost stay under control.

Year 1 pricing

$450 main program

$350 compliance seats

$125 update workshops

Price on income impact

Year 5 pricing

$550 main program

$450 compliance seats

$185 workshops

Lift price only if costs hold

How many students does an import export training program need to pay the owner?

An Import Export Training Program needs about 403 full $450 seats to pay a $145K owner salary when Year 1 contribution margin is 80%; to cover Year 1 payroll plus fixed overhead, it needs about 1,552 full $450 seats. Use scenario math, not a universal promise: required revenue = fixed costs + payroll + owner pay not already in payroll, divided by contribution margin; see How To Launch Import Export Training Program? for launch planning context.

Owner Pay Math

$145K owner salary target

80% Year 1 contribution margin

$181K revenue needed

403 equivalent full-price seats

Scale Drivers

$698K revenue for payroll and overhead

1,552 equivalent $450 seats

Watch conversion rate and refunds

Track instructor time and cohort fill

What are the main costs of an import export training program?

The main costs in an Import Export Training Program are 10% of revenue in Year 1 for direct delivery, plus another 10% for marketing and referrals, while fixed overhead runs $11,950 a month. For a margin view, see How Increase Import Export Training Program Profitability?; payroll is $415K in Year 1 and rises to $1,205M by Year 5, so the cost base gets heavy fast.

Direct delivery costs

6% LMS platform and licenses

4% external instructor commissions

Online modules protect margin

Live experts raise credibility, add risk

Fixed cost load

$11,950 monthly fixed overhead

10% marketing and referral costs

$415K payroll in Year 1

$1,355K startup capex total

Import Export Training Program Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see the main income drivers?

1

Paid Enrollment

45%-85%

Planning assumption: occupancy rising from 45% to 85% drives most take-home because more filled seats turn fixed costs into profit.

2

Tuition Mix

$125-$550

Higher-priced certification and compliance offers lift revenue per learner, with Year 1 prices at $450, $350, and $125.

3

Corporate Sales

$28K-$117K

Corporate training adds clean revenue as volume grows from 80 to 260 enrollments and pricing rises from $350 to $450.

4

Delivery Cost

8%-10%

Instructor commissions and platform costs run 10% to 8% of revenue, so small cuts flow straight to EBITDA.

5

Lead Efficiency

10%

Digital marketing plus referral fees stay at about 10% of revenue, so cheaper leads protect margin as sales scale.

6

Compliance Updates

64%-81%

Planning assumption: better curriculum credibility supports pricing power and repeat sales, which helps EBITDA margin move from 64% to 81%.

Import Export Training Program Core Six Income Drivers

Paid Enrollment

Paid Enrollment

Paid enrollment is the first cash driver because seats have to be sold before training can pay the bills. Track paid students, cohort fill rate, and conversion from leads to paid seats; if you count leads too early, revenue looks stronger than it is.

For this program, occupancy rises from 45% in Year 1 to 85% in Year 5. That matters because more filled seats spread the $11,950 monthly overhead and payroll across more tuition, which lifts profit and gives the owner more room to pay themselves. Empty seats are lost margin.

Track Paid Seats First

Measure only students who have paid and completed onboarding. Then separate individual buyers from employer-paid learners, since corporate seats usually move faster and improve cash flow. Here’s the quick math: if fill rate rises, fixed costs stay flat while revenue climbs, so owner income improves faster than content spend.

Paid seats by cohort

Lead-to-paid conversion rate

Occupancy by program

Employer-paid learner count

Watch the gap between sign-up and payment. If onboarding takes too long, cash comes in late and refunds or no-shows can distort profit. Payment confirmed beats interest shown.

1

Tuition And Package Mix

Pricing Mix

Pricing is the fastest way to lift revenue per learner. Year 1 pricing is $450 for the main trade program, $350 for corporate compliance training, and $125 for regulatory update workshops. By Year 5, those rise to $550, $450, and $185. A better mix raises cash per seat, which helps cover fixed overhead and leaves more room for owner pay.

Bundled offers can push average revenue higher when they combine fundamentals, customs documentation examples, and advanced compliance topics. Keep claims tight: use completion badges or internal credentials as education outcomes only, not legal certification promises. If the mix drifts too far toward low-price workshops, revenue per student drops and break-even gets harder.

Price the Bundle

Track revenue per learner by program, not just total enrollments. The key test is whether more sales move from $125 workshops into $350-$550 courses, because that raises gross profit without needing the same jump in headcount. Here’s the quick math: higher-ticket seats improve take-home income faster than adding more low-price seats.

Test bundle pricing against standalone pricing, then watch attach rate, refund rate, and upgrade rate from workshops to core programs. Keep the offer tied to defined topics and materials so scope stays controlled. That protects margin, cash flow, and the owner’s ability to pay themselves.

2

Corporate Training Sales

Corporate Training Contracts

Corporate training sells to US importers, exporters, logistics teams, and compliance departments that need customs and trade basics. It raises revenue per sale and cuts reliance on one-off enrollments. Price per seat moves from $350 in Year 1 to $450 in Year 5, a 28.6% lift, so better deal size can improve owner pay if delivery stays tight.

Here’s the quick math: corporate revenue = contracts × seats × price. The catch is scope creep. Private workshops can add extra sessions, custom materials, and support time, which pushes labor cost up and weakens margin. One clean contract with defined sessions and limits usually protects cash flow better than a custom deal that keeps expanding.

Price and Scope Control

Track contracts sold, seats per contract, and billable scope such as sessions, materials, and support hours. Price by seat and state what is excluded. If the buyer wants a private workshop, cap revisions and post-training support in the contract so the sale stays profitable and cash comes in before delivery work starts.

To improve take-home income, compare close rates for importer, exporter, logistics, and compliance buyers. Then test whether group seats close faster than individual seats. Prepaid corporate contracts help fund payroll and fixed overhead sooner, but long onboarding or open-ended edits can erase the margin even when sales volume looks strong.

3

Instructor And Delivery Cost

Instructor And Delivery Cost

Delivery cost is the cut that pays the LMS and outside instructors before profit. With 6% of revenue for LMS and 4% for instructor commissions in Year 1, delivery gross margin is 90%; by Year 5, LMS falls to 4% and margin lifts to 92%. That extra 2 points gives the owner more cash for overhead and draw.

The mix matters. Self-paced modules scale with little added labor, live cohorts add expert cost, and hybrid sits in the middle. The risk shows up when a senior expert is needed for every session, because delivery cost stops falling as enrollment grows and each new seat adds less profit.

Control The Delivery Mix

Track the share of self-paced, live, and hybrid delivery, plus the LMS fee and instructor commission rate. Here’s the quick math: delivery cost equals LMS % + instructor commission %, so a move from 10% to 8% of revenue directly adds margin.

Cap expert-led sessions.

Reuse recorded lessons.

Price live support separately.

Review delivery cost monthly.

Forecast margins by course format.

If live cohorts need senior staff every time, the owner’s take-home drops fast even when sales look strong. Keep expert time for premium sessions and use self-paced content for the base program so margin scales with enrollments.

4

Marketing Efficiency

Marketing Efficiency

Marketing efficiency is the gap between what you spend to get a student and the cash that student leaves after refunds and sales labor. In Year 1, digital marketing is 8% of revenue and affiliate referrals are 2%, so total acquisition spend is about 10%. If that ratio rises, owner take-home drops fast because acquisition cost comes off the top before fixed overhead and profit draw.

The key inputs are paid students, channel mix, conversion to paid seats, refund rate, and sales labor. Net revenue after acquisition cost, refunds, and sales labor is the number that matters. Seats pay the owner, not clicks.

Track Cost per Paid Seat

Measure cost per paid seat by channel: partner referrals, webinars, email nurture, and digital ads. By Year 5, marketing falls to 6% while referrals rise to 4%, keeping total acquisition spend near 10%. That mix only helps if the lead turns into a paid seat and stays paid through onboarding.

Watch refund rate and sales labor with the same eye as ad spend, because a cheap lead that needs heavy follow-up can still hurt margin. Measure cash collected per enrolled student, not lead volume, and cut any channel that adds traffic but weak paid-seat conversion.

Paid seats by channel

Refunds by cohort

Sales labor hours

Acquisition spend as revenue %

Net revenue per student

5

Curriculum Credibility And Updates

Curriculum Credibility

Current lessons protect revenue because buyers pay more when the training feels current, practical, and led by people with real trade compliance experience. Here’s the quick math: stronger content supports pricing, referrals, employer trust, and lower refund risk, while stale content can slow conversions and corporate renewals.

This driver includes refreshed lessons, practical documentation examples, and instructor review time. It is educational content maintenance, not regulatory advice. The key inputs are update cadence, refund rate, corporate renewal rate, and the share of sales tied to employer trust. A $110K director of curriculum salary is material, and curriculum FTE rising to 20 later means poor content control can hit cash flow fast.

Refresh to Protect Margin

Track how often customs topics change, how fast lessons are updated, and whether buyers ask for practical examples like shipping docs, tariff codes, and audit-ready records. If the content is current, sales calls get easier and refunds stay lower. If onboarding or lesson review slips, renewal risk rises and owner pay gets squeezed.

Use a simple control list: last update date, instructor compliance background, refund rate, and corporate renewal rate. Tie each course release to a documented review so the team knows what changed and why. The goal is to keep conversion and renewals high enough to cover curriculum payroll and still leave profit for the owner.

6

Import Export Training Program Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high owner income scenarios

Owner income scenarios

Owner income rises as occupancy, pricing, and delivery scale improve. The lean case is an operator path, while base and high cases show how growth can support more cash for pay, reserves, and reinvestment.

Compare lean, base, and high owner income paths.

Scenario

Lean CaseLean case

Base CaseBase case

High CaseHigh case

Launch model

Owner income follows the opening-year model, with lower occupancy and a salary-first draw.

Owner income tracks the Year 3 model, with steadier volume and a scaler's role.

Owner income follows the strongest model, with higher occupancy and an executive-style role.

Typical setup

Year 1 runs at 45.0% occupancy, $3,818,000 revenue, and $2,432,000 EBITDA, with the owner acting as an operator on a $145,000 salary and near 90% gross margin.

Year 3 runs at 72.0% occupancy, $44,122,000 revenue, and $34,671,000 EBITDA, while the owner scales sales, curriculum, and delivery capacity.

Year 5 runs at 85.0% occupancy, $121,538,000 revenue, and $97,951,000 EBITDA, with the owner focused on strategy, cash, and reinvestment.

Cost drivers

45.0% occupancy

$3.818M revenue

63.7% EBITDA margin

90% gross margin

$145K owner salary

72.0% occupancy

$44.122M revenue

78.6% EBITDA margin

22 billable days

expanding FTEs

85.0% occupancy

$121.538M revenue

80.6% EBITDA margin

22 billable days

executive focus

Owner income rangeBefore owner reserves

$145,000Salary first

Salary plus upsideScaled operator

Salary plus distributionsUpside case

Best fit

Best for founders stress-testing a lean operator draw before any distribution plan.

Best for owners using base case planning before taking excess cash out.

Best for owners testing what the business can support once growth funds payroll, reserves, and reinvestment first.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The modeled owner can plan around a $145,000 annual salary if they serve as executive director Extra take-home depends on distributions after reserves, taxes, debt, and reinvestment The business shows $3818M in Year 1 revenue and $2432M in EBITDA, but EBITDA is not the same as cash paid to the owner

The model shows breakeven in Month 1 and payback in Month 1 That result depends on the researched assumptions, including 45% Year 1 occupancy, $3818M revenue, and minimum cash of $899K If enrollment ramps slower, corporate sales slip, or refunds rise, breakeven can move later

No, but replacing founder teaching has a cost The model includes external instructor commissions at 4% of revenue and senior trade compliance staff from 10 FTE in Year 1 to 50 FTE in Year 5 The owner can move toward sales, curriculum, and quality control, but it is not hands-off

Paid enrollment, tuition, corporate training sales, delivery cost, marketing efficiency, and curriculum credibility drive profit Year 1 delivery costs are 10% of revenue, marketing plus referrals are another 10%, and fixed overhead is $11,950 per month Small changes in fill rate matter because payroll starts at $415K

Self-paced online delivery usually protects margin best, but live or hybrid training can support higher prices and employer trust In this model, LMS cost falls from 6% to 4% of revenue while instructor commissions stay at 4% The best format is the one that fills cohorts, controls expert time, and keeps content current

About the author

Michael Porter

Entrepreneurship Researcher

Michael Porter is an entrepreneurship researcher at Financial Models Lab who helps founders opening a new small business turn big questions into clear planning steps. He focuses on expense and revenue planning for the first year, keeping attention on useful numbers and realistic expectations. His work gives business plan writers practical guidance without sugarcoating the challenges ahead.

Choosing a selection results in a full page refresh.