How Much Do In-Home Daycare Owners Make? $45k Pay Plus Profit

In-Home Daycare Bundle

Using the researched assumptions, this in-home daycare can model $45k in owner pay plus business profit if enrollment holds Year 1 revenue is about $84k, with $18k EBITDA, meaning potential owner economic income of about $63k before taxes, reserves, and reinvestment By Year 5, revenue reaches about $197k with $119k EBITDA, but that assumes 12 modeled slots, 90% occupancy, higher tuition, and added staff Treat these as planning ranges, not guaranteed earnings

Owner income$63k-$164kNet margin19%-60%Revenue for target pay$84k-$197kBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on enrollment, tuition, staffing, taxes, reserves, and withdrawals. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see owner income in the In-Home Daycare model?

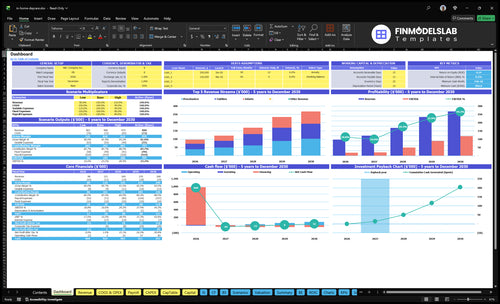

The screenshot covers the dashboard, assumptions, enrollment scenarios, tuition inputs, CACFP reimbursements, cost schedules, payroll by role, startup capex, cash flow, and owner income outputs in the In-Home Daycare Financial Model Template; charts run from $84k to $197k revenue, $18k to $119k EBITDA, with 31-month payback and Month 2 break-even. Open the model.

Owner-income model highlights

Owner income output chart

Revenue and EBITDA range

Capacity, pricing, staffing tables

Can you make a living running an in-home daycare?

Yes, you can make a living running an In-Home Daycare under this modeled case, but only if local tuition, enrollment, and licensed capacity hold; for the operating metric to watch, see What Is The Most Important Metric To Measure The Success Of In-Home Daycare?. Year 1 includes $45,000 Owner/Lead Caregiver pay, about $84,000 revenue, and $18,000 EBITDA, meaning operating profit before interest, taxes, depreciation, and amortization, so owner economic income is about $63,000 before taxes and reserves.

Living-wage drivers

Hold local tuition at plan

Fill licensed childcare capacity

Watch 60% occupancy pressure

Target 80%–90% occupancy strength

Cost reality

Owner pay: $45,000

Year 1 revenue: $84,000

Year 1 EBITDA: $18,000

Hiring help adds payroll

How much revenue can an in-home daycare make?

An In-Home Daycare makes money from paid enrollment, not just licensed capacity. In this model, Year 1 is 9 children at 60% occupancy, with about $68k in monthly tuition plus $250 CACFP reimbursement. By Year 5, 12 modeled slots at 90% occupancy reach about $164k in monthly revenue.

Year 1 revenue

9 slots at 60% occupancy

$1,500 infants

$1,300 toddlers

$1,100 preschoolers

Year 5 revenue

12 modeled slots

90% occupancy

About $164k monthly revenue

Exclude extras unless modeled

How can you increase in-home daycare income?

For In-Home Daycare, income goes up fastest when you fill more of the licensed slots, raise tuition over time, and move toward a better age mix. With occupancy rising from 60% in Year 1 to 90% in Year 5, and capacity growing from 9 to 12 slots, filled seats can rise from about 5.4 to 10.8 before any tuition increase. Assistant help can add room, but a full-time assistant can also add about $30,000 in salary, so care quality and licensing compliance come first.

Raise filled seats

Move occupancy from 60% to 90%.

Grow slots from 9 to 12.

Fill openings faster than rates change.

Protect quality to keep families enrolled.

Lift tuition mix

Raise infant tuition from $1,500 to $1,700.

Raise toddler tuition from $1,300 to $1,500.

Raise preschool tuition from $1,100 to $1,300.

Use assistants only if compliance stays solid.

In-Home Daycare Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main income drivers?

1

Licensed Capacity

9-12 slots

More licensed seats raise monthly revenue first, because each extra child adds recurring tuition after the room is full.

2

Occupancy

60%-90%

Filling more of those seats is the next big swing, since tuition keeps coming in every billable day while many costs stay flat.

3

Tuition Rate

$1.1K-$1.7K

Higher tuition per child lifts revenue per slot, and the model already spans about $1.1K to $1.7K a month by age band.

4

Age Mix

Infant-heavy

A bigger infant share pulls income up, since infant tuition is highest and schedule mix changes how much each slot earns.

5

Staffing Model

1.0-2.5 FTE

Payroll is the main cost swing, because the owner starts at $45K and added staff let you grow only if enrollment keeps up.

6

Overhead Control

$810/mo

Fixed overhead is about $810 a month, and the gap between $18K year 1 EBITDA and $119K year 5 EBITDA shows why reserves matter before owner draws.

In-Home Daycare Core Six Income Drivers

Licensed Capacity And Usable Slots

Licensed Capacity

Licensed capacity is the legal ceiling on how many children you can keep at once. In this model, the cap is 9 slots in Year 1, 10 in Year 3, and 12 in Years 4 and 5, with the mix moving from 2 infants, 3 toddlers, 4 preschoolers to 3 infants, 4 toddlers, 5 preschoolers. That raises the revenue ceiling before pricing or cost choices matter.

Here’s the quick math: moving from 9 to 12 slots lifts the maximum seat count by 33%. What this estimate hides is the real-world cap from state rules, child-to-staff ratios, usable home space, and provider workload. More children are not automatically legal or wise if compliance or quality slips.

Measure Usable Slots First

Track legal slots, not just demand. A slot only counts if it fits the age ratio, the room, the schedule, and your own workload. If a child can’t be served safely and on time, that seat does not turn into reliable income, even when the waitlist looks full.

Check age ratios weekly.

Map every usable room.

Model revenue at 9, 10, 12 slots.

Block schedules that break ratios.

Use a simple capacity sheet tied to licensing notes, daily headcount, and peak-hour staffing. If the home only works at 9 slots before quality drops, don’t forecast 12 as cash you can spend. Extra slots help owner income only when they are legal, filled, and stable.

1

Occupancy And Paid Enrollment

Occupancy Lift

Occupancy is the fastest way to lift revenue in an in-home daycare because every filled slot adds monthly tuition without changing the home footprint. The model moves from 60% in Year 1 to 90% by Year 5, with capacity rising from 9 slots to 12 slots; that is a direct step-up in paid enrollment, revenue, and owner cash flow.

What this hides is churn and timing. Delayed start dates, vacations, and part-time schedules reduce paid enrollment even when a slot looks full on paper. Clear contracts, a waitlist, and firm start dates keep monthly tuition more stable, so the owner has less income wobble and less risk of skipping a draw.

Fill the Slots

Track occupancy by age group and by month, not just licensed capacity. Use this formula: occupied slots ÷ licensed slots. Also track the gap between enrolled and paid children, because tuition only counts when a family starts on time and stays active. Empty slots are lost tuition.

Licensed slots and age mix

Paid occupancy by month

Churn and delayed starts

Part-time and vacation holds

Waitlist fill speed

To improve it, keep a waitlist, confirm start dates in writing, and monitor churn by reason code. Test whether part-time schedules or vacation holds are hurting collections. A small change in fill rate can lift monthly revenue fast, while fixed home costs stay mostly flat.

2

Tuition Pricing

Monthly Tuition per Child

Tuition is the main revenue lever because the model charges a monthly fee per child, not a weekly rate. Year 1 pricing is $1,500 for infants, $1,300 for toddlers, and $1,100 for preschoolers; Year 5 rises to $1,700, $1,500, and $1,300. If enrollment holds, higher tuition lifts profit fast because most fixed costs do not rise with each price increase.

The price has to fit the local market, hours offered, age group, care quality, meals, and schedule reliability. Here’s the quick math: a $200 monthly increase per enrolled infant adds $200 to revenue each month, with little added cost. What this estimate hides is churn risk. If families leave after a rate hike, the margin gain can disappear fast.

Track rates by age and retention

Measure tuition by child type, then compare it to local competitors and parent demand. The owner should track monthly tuition collected, enrollment held after rate changes, and any drop in paid days from delayed starts or schedule changes. A higher rate only helps take-home income when seats stay filled and cash stays recurring.

Use a simple check before raising prices: will the new rate still fit meals, hours, and reliability? If a family questions the increase, explain the added value in plain terms. One clean rule: raise price only when retention stays strong. That protects margin, cash flow, and the owner’s draw.

Track monthly tuition by age group

Compare rates to local market pricing

Watch churn after each increase

Review full-time versus part-time demand

Test price only when spots stay filled

3

Age Mix And Schedule Mix

Age Mix And Schedule Mix

Age mix changes both price and workload. Infants carry the highest modeled tuition at $1,500 to $1,700 per month, but they can use more ratio capacity and caregiver time. Preschoolers are lower at $1,100 to $1,300, yet they can support steadier group routines, so the same slot can produce different profit depending on who fills it.

Schedule mix matters just as much. Full-time care usually gives better revenue density than scattered part-time care, while extended hours can raise revenue but also add owner fatigue and backup-care risk. The real impact depends on licensing ratios and how stable the paid week stays across the month.

Track revenue per slot, not just enrollment

Measure monthly tuition by age group, then split it by full-time and part-time schedules. That shows where the money comes from and where labor gets squeezed. If infants rise but staffing hours rise faster, owner pay can drop even when gross revenue looks better.

Watch three numbers: paid weeks, child mix, and open hours. Keep the schedule simple when possible, because scattered part-time days and long extensions raise coverage risk. A clear contract and a steady weekly schedule protect cash flow better than chasing a few extra hours.

Track tuition by age band.

Separate full-time and part-time slots.

Check ratio pressure before adding infants.

Limit extended hours unless paid.

4

Staffing Model And Owner Labor

Owner Labor and Caregiver Staffing

Owner-operated care keeps payroll light, but it also caps how many children one adult can safely handle. This model starts with $45k annual pay for the owner/lead caregiver, so owner income depends on enrollment covering that draw before other labor is added.

Then staffing raises capacity, but it also adds fixed payroll. The plan assumes an assistant caregiver at $30k annual salary with 0.5 FTE in Year 2, 0.8 FTE in Year 3, and 1.0 FTE in Years 4 and 5, plus a part-time helper at $15k annual salary at 0.5 FTE in Years 4 and 5. More staff can lift revenue, but payroll tax, scheduling gaps, and backup coverage can cut take-home pay fast.

Staff to Capacity, Not Hope

Track paid enrollment per caregiver hour, not just headcount. The key inputs are slots filled, hours worked, and total payroll, including payroll tax. If tuition does not rise with added staff, profit per child falls and owner pay gets squeezed.

Use staffing only when the added labor supports more enrolled children or longer paid hours. Build the forecast around $45k owner pay first, then test whether the $30k assistant and $15k helper can be covered by stable occupancy, not by best-case months. One empty week can erase a small margin.

5

Operating Costs And Reserves

Keep Cost Load Low

This driver is the variable cost load from food, supplies, marketing, and cleaning, plus $810 per month in fixed costs for utilities allocation, insurance, licensing, training, software, property insurance allocation, and background checks. Year 1 costs run at 18% of revenue, then fall to 12% by Year 5. That lower cost base is what protects owner pay when enrollment dips.

Here’s the quick math: at $10,000 in monthly tuition, Year 1 variable costs are about $1,800, leaving $8,200 before fixed costs and owner pay. With fixed costs at $810, the business only has room for profit if pricing and enrollment stay steady. Cash gets tight fast if food waste, supply overbuying, or cleanup labor drift above plan.

Build Reserves Before Pay

Reserve cash before taking extra draws. Startup capex is about $23,000 from $5,000 playground equipment, $3,000 furniture, and $15,000 safety systems, plus smaller setup items. If that cash is not set aside, owner pay gets interrupted when a repair, license renewal, or slow month hits.

Track monthly cost %, fixed cost cash, and reserve balance separately. A simple rule is to pay the business first: cover the $810 fixed load, fund reserves, then take draws. If food, supplies, or cleaning costs creep up, cut them before cutting your reserve.

Watch cost % every month.

Keep reserve cash untouched.

Delay draws until reserves rebuild.

6

In-Home Daycare Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high owner income cases

Owner income scenarios

Owner income moves with occupancy, tuition, and staffing. Higher fill rates lift revenue, but labor and compliance costs rise too.

Lean, base, and high owner-income paths by occupancy and staffing.

Scenario

Lean CaseRamp-up

Base CaseStable

High CaseMature

Launch model

This is the lower earnings path from Year 1, when the home runs at 60% occupancy across 9 slots.

This is the modeled middle path from Year 3, with 10 slots filled to 80% occupancy.

This is the stronger Year 5 path, with 12 slots at 90% occupancy and a fuller staff.

Typical setup

Year 1 brings about $84,000 revenue, $18,000 EBITDA, and about $63,000 owner economic income before taxes and reserves, with the owner carrying most of the care load.

Year 3 brings about $135,000 revenue, $49,000 EBITDA, and about $94,000 owner economic income as staffing and compliance costs rise.

Year 5 brings about $197,000 revenue, $119,000 EBITDA, and about $164,000 owner economic income, but labor and compliance get heavier.

Cost drivers

60% occupancy

9 slots

tuition mix

food and supplies

fixed overhead

80% occupancy

10 slots

assistant caregiver

tuition growth

compliance costs

90% occupancy

12 slots

more staff

wage pressure

compliance load

Owner income rangeBefore owner reserves

$63,000Lean case

$94,000Base case

$164,000High case

Best fit

Use this to stress test the business if enrollment starts slow or staffing stays owner-heavy.

Use this as the main operating plan if enrollment stays steady and the assistant role keeps coverage smooth.

Use this to test upside if the home stays near full and the staffing plan holds without breaking margins.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions.

The model includes $45k in annual owner pay from Year 1 It also shows $18k EBITDA in Year 1 and $119k by Year 5, so possible owner economic income ranges from about $63k to $164k before taxes, reserves, debt, and reinvestment Actual take-home depends on enrollment, pricing, costs, and cash timing

The core model shows break-even in Month 2 and a 31-month payback period That assumes the planned tuition, 60% Year 1 occupancy, $810 in monthly fixed costs, and the modeled payroll plan If enrollment starts slower or startup costs run higher, cash pressure lasts longer

An LLC does not create more daycare earnings by itself Income still comes from paid children, tuition rates, occupancy, and cost control The model’s $84k Year 1 revenue and $18k EBITDA come from operations, not entity type Ask a qualified professional about liability, tax treatment, and licensing fit

Capacity, occupancy, tuition, staffing, and recurring costs drive profit the most In this model, occupancy rises from 60% to 90%, capacity grows from 9 to 12 slots, and EBITDA grows from $18k to $119k Payroll is the main tradeoff because help can support growth but cuts margin

Start with the $45k target owner pay, then treat extra draws as available only after bills, payroll, reserves, and reinvestment EBITDA is $18k in Year 1 and $49k in Year 3, but that is not automatic cash in your pocket Use monthly cash flow before increasing draws

About the author

Maya Bennett

Independent Business Researcher

Maya Bennett is an independent business researcher who writes practical guides on small business money management for local business owners planning their first venture. She helps readers organize business assumptions into a clear plan, with a focus on revenue and profit examples that make each step easier to follow. Her work is calm, structured, and geared toward turning an idea into a basic business plan.

Choosing a selection results in a full page refresh.