Interior Design Owner Income: $100K Salary Plus Profit Upside

Key Takeaways

Bigger projects lift revenue without adding many clients.

Scope clarity protects margin more than higher rates.

Billable hours beat busy work for owner take-home.

Leads must fit budget, or marketing waste grows.

Owner income$100kNet margin88%–91%Revenue for target pay$209kBusiness difficultyHard

Want to test your interior design owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to see how owner income is modeled?

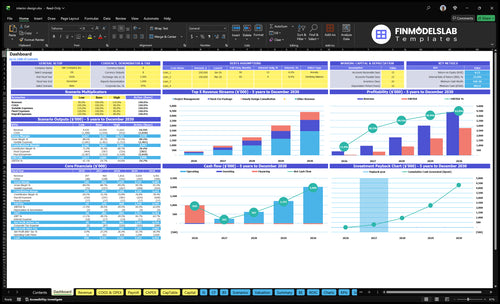

The dashboard shows revenue assumptions, pipeline, service mix, payroll, overhead, cash flow, scenarios, and owner take-home. Open the Interior Design Financial Model Template.

Owner-income model highlights

Owner take-home output

Sales, margin, profit

Scenario-driven planning support

Can an interior design business owner make good money?

Yes, an Interior Design business owner can make good money if pricing, project size, close rate, and overhead support the owner-pay model; see What Is The Most Critical Measure Of Success For Your Interior Design Business? for the core metric lens. Here’s the quick math: with a 73% contribution margin, $130,000 payroll, and $77,400 fixed overhead, first-year break-even is about $284,000 in revenue before extra owner distributions.

Owner Pay Math

Model includes $100,000 lead designer salary

Break-even revenue is about $284,000

Contribution margin needs to hold at 73%

Fixed overhead totals $77,400

Take-Home Levers

Attach paid project management more often

Sell fixed-fee design packages

Build qualified referral channels

Control payroll as revenue grows

Solo interior designer business income versus studio owner income?

A solo Interior Design owner can protect margin, but income caps out fast because billable hours get eaten by admin, sourcing, and site visits. In this model, Year 1 starts with a $100,000 lead designer and a $60,000 junior designer, and the stated $130,000 payroll only helps if staff time turns into paid work above fully loaded cost. Year 2 adds a project manager and marketing/admin support, so payroll pressure rises before utilization catches up.

Solo owner cap

Billable hours set the ceiling.

Admin work cuts paid time.

Sourcing takes unpaid effort.

Site visits slow throughput.

Studio owner shift

Year 1 payroll starts at $130,000.

One lead designer earns $100,000.

One junior designer earns $60,000.

Profit improves on paid utilization.

How much revenue does an interior design business need to pay the owner?

For an Interior Design owner to pay a $100,000 salary and cover first-year overhead and payroll, the business needs about $284,000 in revenue before any extra distributions. Here’s the quick math: $207,400 of payroll plus fixed overhead divided by a 73% contribution margin. If the owner wants money above salary, add that target, plus reserves and taxes, to the numerator.

Base revenue target

$284,000 covers salary and overhead

$207,400 is the modeled cost base

73% is the contribution margin

Salary comes before owner distributions

What raises the target

Add distributions above salary

Add reserves and taxes

Higher payroll lifts the revenue need

Direct costs above 12% push it up

Interior Design Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see what drives interior design owner income?

1

Project Mix

$600-$3K

More work in the $3,000 project stream raises revenue per client and owner income faster than $600 consults.

2

Hourly Rates

$120-$170

Moving rates from $120 to $170 lifts every billed hour, so owner pay rises without more headcount.

3

Overhead FTE

$77.4K

The $77,400 fixed base and extra FTE can eat profit fast, so lean staffing protects take-home.

4

Utilization

5-25h

More billable hours per job spread fixed time over more revenue and push more cash to the owner.

5

Acquisition Cost

$500-$400

Lower CAC from $500 to $400 makes each win cheaper, which helps cash and payback.

6

Vendor Margin

9%-12%

Keeping subcontractor and photography costs near 9% to 12% protects margin on each project.

Interior Design Core Six Income Drivers

Average Project Value

Average Project Value

Average project value is the revenue you earn per client job, so the mix matters. Moving from $600 consultations to $1,950 fixed-fee package equivalents or $3,000 project management lifts income fast; one $3,000 project equals five $600 consults in top-line revenue. By Year 5, those modeled examples rise to $810, $2,610, and $4,250.

This helps pay fixed overhead and owner draw with fewer closes, but only if delivery cost stays in line. The upside comes from larger room packages, renovations, whole-home work, and small commercial scopes. The risk is selling premium scope without enough capacity or a clean budget fit, which can stretch labor, delays cash, and cut profit.

Raise Scope, Not Just Volume

Track average revenue per project by service type, then watch which scopes move clients above $600. Ask for budget early, price the real scope, and compare proposals against delivery capacity before you sign. If the work needs more revisions, site visits, or vendor coordination, the project value has to cover that load or owner pay drops.

Track value by service line.

Screen budget before proposal.

Price for scope creep.

Protect capacity on premium jobs.

1

Pricing Model And Fee Structure

Pricing Discipline

Your take-home rises when the firm charges for the real work, not just the first concept. In this model, consultations at $120 to $135, project management at $150 to $170, and fixed-fee packages at $130 to $145 per modeled hour set the floor for revenue quality. If scope is loose, extra revisions, vendor coordination, and site visits can wipe out margin fast.

Scope First, Price Second

Quote from a clear scope: number of rooms, revision rounds, site visits, and who handles vendors. That keeps the math clean on hourly billing, flat fees, retainers, or percentage-of-project pricing. One clean rule: if the work is open-ended, the price should be open-ended too. Track billed hours, change orders, and the gap between estimated and actual time.

Track revision hours by project.

Price extra visits before work starts.

Bill vendor coordination separately.

2

Billable Utilization And Owner Capacity

Billable Utilization

If the owner spends too much time on sourcing, admin, revisions, vendor calls, sales calls, and travel, effective hourly income drops. The key inputs are billable hours, service mix, and time per job. In this model, consultations move from 5 to 6 hours, project management from 20 to 25, and fixed-fee packages from 15 to 18, so the same revenue supports more owner pay only when unpaid time shrinks.

Utilization means the share of time that earns money. If the owner fills more of the week with paid design, client planning, and billable project work, take-home income rises without needing the same jump in sales. But if hiring only adds payroll and does not free the owner from low-value work, profit falls and cash gets tighter.

Protect Owner Hours

Measure billable utilization by service each week. Here’s the quick math: if a job needs 25 modeled hours but 5 hours are unpaid, only 80% of the work earns revenue. Track actual hours versus the model for consultations, project management, and fixed-fee packages, then flag any creep in revisions, travel, or vendor follow-up.

Set scope before the proposal is signed, then route admin and coordination to support staff only when it frees the owner for paid design or sales. The goal is simple: more billable hours, fewer unpaid hours, and a higher return on the owner’s week.

3

Procurement Margin

Procurement Margin

Procurement margin is the spread on furnishings, fixtures, and accessories after vendor discounts, freight, receiving, returns, damages, backorders, and admin time. Keep it separate from design fees so you can see whether product sales really add to owner income. If markup only matches the vendor discount, the owner can still lose money once handling and cash timing are counted.

Track Landed Cost and Markup

Measure landed cost on every order: product cost plus freight, receiving, and any rework. Run a working-capital check before large orders so client deposits and payment timing cover the cash outlay. The goal is simple: markup should pay for handling, cash lag, and admin effort, not just the vendor discount.

Separate product and design invoices.

Track returns and damage write-offs.

Review backorders before placing orders.

Approve large buys only after cash check.

4

Client Acquisition And Close Rate

Client Acquisition And Close Rate

Owner income rises when qualified inquiries turn into signed projects at a sensible CAC (customer acquisition cost). With a $15,000 Year 1 marketing budget and $500 CAC, that’s about 30 customers; at $70,000 and $400 CAC, it’s about 175 customers. The real driver is not traffic volume. It’s whether the lead can afford the scope and actually closes.

This income driver includes inquiries, proposal close rate, and referral quality. Builders, real estate agents, and past clients usually shorten payback because trust is already there. Vanity traffic hurts cash flow if it fills the pipeline with people who want a room refresh but need a full-service project. When close rate slips, revenue slows and the owner’s draw gets squeezed.

Track Lead Quality Fast

Measure each source by qualified inquiries, proposal-to-close rate, and CAC. If a channel sends cheap leads but they cannot afford the project, cut it. Use a simple source log, then compare budget by channel against signed projects and average project size so you can see which leads actually pay the bills.

Ask every lead where they heard about you, then separate referrals from builders, real estate agents, and past clients from paid traffic. Those referrals usually close faster and improve cash flow. The test is simple: if more spend does not raise signed projects, the marketing budget is just buying noise.

5

Payroll And Overhead Control

Payroll and Overhead Control

Take-home starts after fixed costs get paid. In this model, fixed overhead is $6,450/month or $77,400/year, and Year 1 payroll is $130,000, so the business must cover at least $207,400/year before direct costs, reserves, and reinvestment. If revenue misses that floor, owner pay shrinks fast.

Adding a junior designer can improve speed, quality, and client response, but it lowers margin until pricing and utilization catch up. One clean rule: if the extra staff time does not create more billable work or higher-value projects, payroll becomes a cash drag instead of an income lift.

Track the cost floor every month

Measure monthly revenue against $6,450 of overhead and $130,000 of payroll, then add direct costs, reserves, and reinvestment before planning owner pay. Use the same view for each project so you can see whether the team is covering its cost base or just staying busy.

Track billable hours by role

Watch revision and site-visit time

Separate payroll from project profit

Check cash before adding staff

If hiring helps the lead designer sell more paid design work or finish jobs faster, keep it. If not, hold staffing steady, tighten scope, and protect the margin that funds owner income.

6

Interior Design Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and premium interior design owner-income scenarios

Owner income scenarios

Owner income swings with staffing, billable time, and project mix. Lean solo keeps overhead light; the base case uses a $100,000 lead-owner salary; the premium studio needs more revenue to support a bigger team.

See how staffing and project mix change owner pay.

Scenario

Lean SoloLean solo

Base BoutiqueBase boutique

Premium StudioPremium studio

Launch model

The owner stays hands-on, keeps hiring light, and relies on billable design work for most income.

The business runs with a lead-owner salary and a small support team, with profit covering only modest extra pay.

The studio adds more project management and fixed-fee work, so revenue can support a larger owner payout.

Typical setup

A lean solo practice keeps overhead low, uses fewer staff, and leaves owner pay tied to project flow and small distributions.

Year 1 uses a $100,000 lead-owner salary, $130,000 payroll, $77,400 fixed overhead, and about 73% contribution margin, so break-even sits near $284,000 revenue before extra distributions.

This case shifts toward 48% to 50% project management and fixed-fee mix, a $55,000 to $70,000 marketing budget, lower CAC, and expanded payroll, which raises the revenue needed to fund owner income.

Cost drivers

Solo billable time

lower overhead

fewer staff

limited distributions

uneven project flow

Lead-owner salary

73% contribution margin

$77.4k fixed overhead

$130k Year 1 payroll

moderate support staff

More project management mix

more fixed-fee packages

larger marketing budget

lower CAC

expanded payroll

Owner income rangeBefore owner reserves

$60,000 - $90,000Lean pay band

$100,000 - $150,000Core pay band

$150,000 - $250,000Upside pay band

Best fit

Use this to stress-test a solo path with light overhead and thin distributions.

Use this if you want a realistic owner-pay plan built around the modeled Year 1 setup.

Use this to test a scaled studio with stronger demand and a larger owner payout.

!

Planning note: Ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In this model, the owner-operator baseline is the $100,000 lead designer salary Extra pay depends on profit after payroll, $77,400 annual fixed overhead, direct costs, marketing, reserves, and taxes First-year break-even is about $284,000 revenue before extra owner distributions, using a 73% contribution margin

Owner pay is supportable once revenue covers payroll, fixed overhead, and variable costs The model starts with $130,000 Year 1 payroll and $6,450 monthly fixed overhead, so early ramp-up needs tight cash control If projects close slowly or collections lag, owner distributions should wait

Not always Staff can raise capacity, but only if their hours turn into paid project work The model starts with one lead designer and 05 junior designer, then adds project management and admin support later Payroll can reduce margin until utilization, pricing, and client volume catch up

The biggest drivers are project value, fee structure, billable utilization, procurement margin, client acquisition, and overhead control A $3,000 project management scope creates far more revenue than a $600 consultation But payroll, rent, software, marketing, and reserves decide how much profit is safe to take home

The best pricing model is the one that matches scope risk and protects paid time Hourly billing works for open-ended advice, while flat fees need tight scope control Project management can be strong in this model, rising from $3,000 per scope in Year 1 to $4,250 in Year 5

About the author

Victor Shaw

Practical Business Analyst

Victor Shaw is a practical business analyst at Financial Models Lab who writes about small business budgeting and estimating what a business can earn. He helps aspiring small business owners build realistic assumptions, understand break-even points, and compare business opportunities with greater clarity. His work focuses on simple, credible financial analysis that turns rough ideas into grounded expectations for real-world decision-making.

Choosing a selection results in a full page refresh.