Lockout Tagout Training Owner Income: $125K Pay Plus Profit

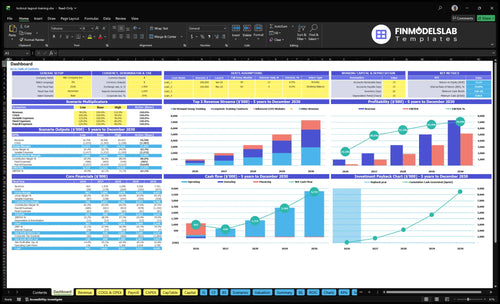

This model shows a US LOTO training company with revenue rising from $963k in Year 1 to $7301M in Year 5, with EBITDA rising from $214k to $5157M The modeled owner role is the Executive Director at $125k annual salary any distributions come after payroll, delivery costs, overhead, reserves, taxes, debt service, and reinvestment

Owner income$125kNet margin22%–71%Revenue for target pay$963kBusiness difficultyMedium

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the gap to your target pay from monthly revenue, gross margin, labor, fixed overhead, marketing, reserves, and debt service. Use it to see whether the current mix can fund a real owner paycheck.

!

Planning note: Research-based planning estimate only. Actual owner take-home depends on revenue, margin, payroll, taxes, debt, reserves, and timing. Not guaranteed salary, tax advice, or owner distribution advice.

Can you check owner income in the Lockout Tagout Safety Training model?

How many lockout tagout training classes are needed to pay the owner?

For Lockout Tagout Safety Training, the owner target is $125,000 a year, and the early plan only fills about 9 occupied days a month at 60% occupancy from 15 billable days. Add $6,750 of monthly overhead before payroll, or about $81,000 a year, and the plan needs roughly $206,000 in annual contribution before any owner payout. That means about 108 occupied training days a year, or around $1,907 of contribution per day, and this is not a guaranteed salary because taxes, cash reserves, and reinvestment can reduce distributions.

Capacity hurdle

15 billable days per month

60% occupancy equals 9 days

$6,750 fixed overhead each month

$206,000 annual owner-plus-overhead load

Pay reality

108 occupied days a year

About $1,907 contribution per day

$420,000 Year 1 payroll load

Taxes and reserves cut take-home

How much revenue can a lockout tagout training business make?

A Lockout Tagout Safety Training business can make about $963k in Year 1, scaling to $7.301M by Year 5 in the source model; see How To Start Lockout Tagout Safety Training Business? for the setup path. Revenue depends on client volume across industrial, manufacturing, maintenance, and facility accounts, but it’s not owner income because payroll, travel, materials, commissions, marketing, overhead, reserves, and taxes come out first.

Revenue Path

Year 1: $963k revenue

Year 2: $1.978M revenue

Year 3: $3.298M revenue

Year 5: $7.301M revenue

Contract Drivers

Corporate contracts rise from 10 to 30

Group training grows from 12 to 36

Advanced modules grow from 8 to 24

Profit depends on delivery cost control

What affects profit margins in a lockout tagout training business?

Lockout Tagout Safety Training margins are most sensitive to utilization, travel, staffing, and contract mix; if instructor time sits idle or travel spikes, profit drops fast even when sales look strong. In Year 1, direct costs run 40% materials plus 60% travel/per diem, then improve to 25% and 40% by Year 5, while sales commissions ease from 50% to 40% and marketing from 40% to 20%. For the operating drivers behind that, see What Are The 5 KPIs For Lockout Tagout Safety Training Business?

Margin drivers

Utilization is the top lever.

Travel/per diem starts at 60%.

Materials are 40% in Year 1.

Unused instructor time cuts take-home fast.

Cost pressure points

Sales commissions run 50% to 40%.

Marketing falls from 40% to 20%.

Fixed overhead stays at $81k per year.

Payroll grows from $420k to $885k.

Lockout Tagout Safety Training Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Client Volume

$963K-$7.3M

More contracts and group sessions drive revenue from Year 1 to Year 5, and EBITDA moves from $214K to $5.157M.

2

Billable Utilization

60%-85%

Higher occupancy turns the same instructor base into more paid days, so take-home rises without matching fixed cost growth.

3

Delivery Cost Control

6.5%-10%

Consumables and travel fall from 10.0% of revenue in Year 1 to 6.5% in Year 5, which protects margin.

4

Staffing Mix

$420K-$885K

Keeping the owner closer to sales and delivery delays hires, but extra FTEs can squeeze EBITDA if they come too early.

5

Training Price

$4.5K-$5.3K

Higher corporate contract pricing lifts revenue on every deal, and the effect compounds as volume scales.

6

Recurring Work

$1.2K-$4.0K

Repeat certification fees add steady income, which smooths cash flow when new contract timing slips.

Lockout Tagout Safety Training Core Six Income Drivers

Client volume

Client Volume

Client volume is the strongest revenue driver here because one site, plant, or facility can create multiple sessions plus add-on documentation work. In this model, corporate training contracts grow from 10 to 30, on-demand group training from 12 to 36, and advanced modules from 8 to 24, so more accounts can lift revenue fast if each account stays productive.

That only helps owner pay when travel, prep, and sales costs stay tight. A remote account with heavy custom work can add revenue but still cut take-home income if the instructor day is stretched too thin. The real win is better overhead absorption: more billable sessions spread fixed costs across more sales.

Track account yield

Measure accounts won, sessions per account, add-on documentation, travel hours, and custom prep hours. Here’s the quick check: if a new customer adds sessions but also adds long drives and custom builds, margin can shrink even when revenue rises.

Track revenue per account

Track travel and prep time

Price custom work separately

Protect delivery capacity

Watch acquisition cost closely

Focus on the mix that repeats. More recurring sites beat one-off jobs because the same setup can support more sessions, better utilization, and steadier cash flow without forcing the owner to work unpaid admin time.

1

Average training engagement price

Average Training Engagement Price

Pricing sets take-home because the same instructor day can produce different revenue. Here, corporate contracts move from $4,500 to $5,300, group training from $3,200 to $4,000, and advanced modules from $1,800 to $2,200. That adds $800, $800, and $400 per engagement for the same delivery slot, before travel and admin burden.

This price should reflect onsite delivery, class size, documentation, travel distance, procedure complexity, and whether the class trains supervisors or authorized employees. The big risk is discounting to win work while still carrying the full travel, prep, and paperwork load. When price holds, gross profit per day rises, and the owner has more room to pay themselves.

Price for the full delivery load

Track price per session, hours on site, travel miles, admin hours, and gross profit per instructor day. If two jobs use the same day, compare revenue per day, not just the quoted fee. A $4,500 contract that needs heavy travel can pay less than a $5,300 local one.

Raise price when class size is small, documentation is heavy, or the site is remote. Also price supervisor training above basic employee training when the scope is broader. If you need a discount, cut scope or travel costs too, or owner income gets squeezed.

2

Billable instructor utilization

Billable Instructor Utilization

If instructor days sit empty, payroll still runs and owner pay gets squeezed. This driver tracks how much of paid labor turns into booked delivery, not just total work. Here’s the quick math: 15 billable days at 60% occupancy equals 9 paid days; by Year 5, 22 days at 85% occupancy equals 18.7 paid days. That is a 47% lift in capacity.

The hidden drain is nonbillable labor: sales calls, travel, admin, curriculum prep, and follow-up. Those hours matter, but they do not invoice. If they grow faster than booked delivery, EBITDA margin, the profit left after payroll and overhead, falls and the owner sees less cash to draw. The key inputs are billable days, occupancy, instructor payroll, and travel or prep time.

Fill the Calendar First

Track booked delivery days versus total instructor workdays every month. Separate paid teaching days from sales, travel, prep, and follow-up, so you can see real utilization. A simple test is whether each instructor is moving from 9 paid days a month toward 18.7 without adding much dead time. If not, you’re carrying payroll through empty gaps.

Improve this by booking repeat sessions back-to-back, grouping nearby sites, and setting a minimum calendar fill before hiring more staff. Forecast labor as a percent of revenue, then watch whether occupancy stays near 85% as headcount rises. If occupancy slips, owner take-home drops fast even when the schedule looks full on paper.

3

Recurring refresher work

Recurring Refresher Revenue

Recurring refresher work matters because it turns one training sale into repeat revenue. For lockout/tagout safety training, the key inputs are repeat client count, refresher frequency, documentation fees, and advanced module upsells. Documentation fees can rise from $1,200 to $4,000, so the same client can drive much more revenue without a full new sale.

This driver improves owner income by smoothing monthly cash flow and lowering acquisition cost per dollar of revenue. The risk is simple: do not assume every client renews automatically. If follow-up after the first class is weak, refresher work drops, and the owner has to spend more time selling new accounts just to hold revenue flat.

Track renewals, not just new wins

Measure repeat-client renewal rate, documentation-fee attach rate, and advanced module upsell rate. Here’s the quick math: more renewals plus higher add-on fees means more revenue from the same client base, with less travel, sales time, and setup work per dollar earned.

Set renewal reminders after each class.

Track documentation fees by client.

Price refresher bundles clearly.

Flag accounts with no follow-up.

Keep the pipeline warm with post-class calls, updated training records, and scheduled refresher dates. If the first class is strong but the next touch is late, the business loses the easiest revenue to retain.

4

Delivery cost control

Delivery cost control

Delivery cost control is the gap between what a job bills and what it costs to show up, teach, and finish the paperwork. For this model, the cost stack includes onsite travel, lodging, mileage, printed materials, learning tools, insurance, and admin support. When direct costs improve from 100% of revenue in Year 1 to 65% in Year 5, more cash stays in the business and owner take-home rises.

The risk is taking remote jobs without charging for travel. That leaks margin fast, even before you pay the $6,750 monthly fixed overhead. Marketing and commissions also improve from 90% to 60%, so the business needs both cleaner delivery and tighter selling terms to protect profit.

Charge travel, not surprises

Track cost by job: miles driven, lodging nights, printed packets, training kits, insurance allocation, and admin hours. Use those inputs to set a travel fee or a higher onsite rate. If a client wants a remote site, quote the full delivery cost up front so the class still covers labor, overhead, and owner pay.

Track miles and nights.

Price travel separately.

Log admin time per job.

Reuse training materials.

Review margin by client.

5

Owner role and staffing mix

Owner role and staffing mix

Owner-led delivery can protect margin early, because one more class sold does not add another salary. But this model shifts fast: the staffing plan includes a $125k Executive Director, $85k Lead LOTO Instructors, a $75k EHS Sales Manager, and $50k Administrative Coordinators, with payroll rising from $420k in Year 1 to $885k in Year 5. If demand is not repeatable, that fixed load can cut deeply into owner pay.

The key inputs are billable delivery days, class occupancy, and how much work stays on the owner’s desk. Capacity improves when billable days move from 15 per month in Year 1 to 22 in Year 5, while occupancy rises from 60% to 85%. If quality slips or seats stay empty, headcount just adds overhead, not take-home income.

Hire only when utilization is real

Track billable days per instructor, class occupancy, and payroll as a share of revenue. Add a trainer only when repeat demand already fills most of that role’s month, not when one large account looks good on paper. Keep the owner in sales and key delivery early, because that protects margin and cash.

Forecast the jump from $420k payroll to $885k before you hire. If utilization stays near 15 billable days or occupancy lingers around 60%, staffing becomes fixed overhead instead of growth capacity. The goal is more delivery seats, not more idle salary.

Review fill rate every month.

Price for travel and prep.

Document repeat client renewals.

Keep owner time on sales.

6

Lockout Tagout Safety Training Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: compare lean, base, and high lockout tagout training owner income outcomes

Owner income scenarios

Owner pay moves with billable days, occupancy, and how much profit stays after payroll and reserves. These are planning estimates, not promised earnings.

Low, base, and high owner income cases for planning.

Scenario

Low CaseLow case

Base CaseBase case

High CaseHigh case

Launch model

Owner income stays tight because launch volume runs below plan.

Owner income follows the source model at the planned operating pace.

Owner income scales with mature-year utilization and stronger client growth.

Typical setup

Occupancy stays under 60%, billable days run below 15 a month, new contracts land slower, and distributions stay small after reserves.

The model uses 60% occupancy, 15 billable days a month, $963k revenue, $214k EBITDA, $420k Year 1 payroll, and $6,750 monthly fixed overhead.

The mature case reaches 85% occupancy, 22 billable days a month, $7.301M revenue, $5.157M EBITDA, and $885k payroll, leaving more room for distributions after reserves.

Cost drivers

Under 60% occupancy

fewer billable days

slower contract wins

smaller module upsell

tighter owner draw

60% occupancy

15 billable days

$963k revenue

$214k EBITDA

$420k payroll

85% occupancy

22 billable days

$7.301M revenue

$5.157M EBITDA

$885k payroll

Owner income rangeBefore owner reserves

Salary only, small drawLow case

Salary plus modest drawBase case

Salary plus larger drawHigh case

Best fit

Use this to stress-test cash and owner pay if sales take longer to ramp.

Use this as the most likely planning case for budgets, hiring, and lender decks.

Use this to test upside if the calendar fills faster and reinvestment still leaves cash for the owner.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions.

Certification documentation can add revenue when clients need proof of training completion In the model, documentation fees rise from $1,200 in Year 1 to $4,000 in Year 5 The bigger effect is trust: strong records support repeat facility work, but they still add admin time, software use, and quality-control steps

The model reaches breakeven in Month 2 and payback in 11 months, but that depends on funding and early sales execution Minimum cash need is $829k in Month 2, so the startup must cover payroll, capex, travel, and overhead before collections smooth out Breakeven is not the same as owner distributions

You likely need hired instructors if the goal is more than an owner-led training practice The model starts with 2 Lead LOTO Instructors and grows to 6 by Year 5 That lifts capacity from 15 to 22 billable days per month, but it adds payroll, scheduling pressure, supervision, and quality-control risk

Virtual delivery may reduce travel and materials, but the provided model does not break out virtual classes separately The modeled cost base includes travel/per diem at 60% of revenue in Year 1, falling to 40% by Year 5 If virtual work replaces onsite travel, margin can improve, but pricing and client acceptance matter

The best niche is one with repeat facility needs, enough staff to train, and clear documentation requirements In this model, corporate contracts grow from 10 to 30 and carry higher pricing, from $4,500 to $5,300 A narrow industrial focus can help, but only if it improves close rates, utilization, and renewal work

About the author

Edward Fisher

Practical Business Analyst

Edward Fisher is a practical business analyst at Financial Models Lab, focused on small business budgeting and estimating what service businesses can realistically earn. He writes break-even explanations and other planning content for founders who want optimistic growth ideas grounded in realistic assumptions and cost-aware decision-making.

Choosing a selection results in a full page refresh.