How Much Can A Luxury Limo Service Owner Make At $204/Hour?

A luxury limo service owner can plan around a $150,000 first-year founder salary in this model, but that is not guaranteed take-home Here’s the quick math: first-year pricing averages about $204 per booked hour, and direct plus variable costs total 26% of revenue, leaving a 74% contribution margin before fixed overhead, salaried payroll, debt service, reserves, and taxes Based on listed fixed costs, known salaries, and the annual marketing budget, break-even is about $119 million in first-year revenue before vehicle debt and replacement reserves These are researched planning assumptions, not salary promises, tax advice, or guaranteed earnings

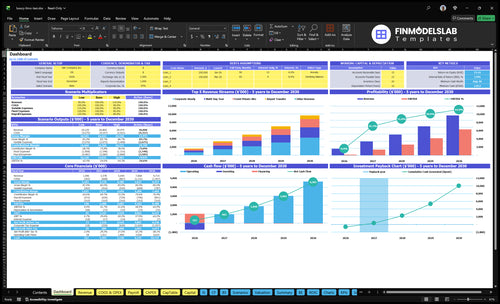

Owner income$150kNet margin12%Revenue for target pay$1.27MBusiness difficultyHard

Want to test your owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It shows pre-tax owner income, not guaranteed salary, tax advice, or owner distribution advice. Actual results move with bookings, margins, payroll, taxes, debt, and reinvestment.

Want to see the full Luxury Limo Service financial model?

What limo business expenses compress owner income most?

For Luxury Limo Service, owner income gets squeezed most by fixed payroll and fleet overhead, not just fuel. If you want the cost setup in context, see How Much Does It Cost To Open And Launch Your Luxury Limo Service Business?; the core load is 26% of Year 1 revenue in direct and variable costs, plus $25,800 per month in fixed expenses. That fixed stack includes $10,000 for fleet and liability insurance, $7,000 for storage and detailing rent, and at least $420,000 a year in salaries, so a 1-point margin shift on $119M revenue moves profit by about $11,900 before debt, reserves, and taxes.

How does the owner role change limo business income?

If you owner-drive and owner-dispatch early, Luxury Limo Service can keep more cash in the bank, but the model already assumes a $150,000 CEO and Founder salary, 9% chauffeur direct compensation, and a $75,000 Senior Chauffeur. So the owner role changes near-term cash flow more than modeled income, unless those payroll costs are actually removed. Bigger fleet growth can lift revenue, but only if booked hours per vehicle rise faster than added overhead.

Owner-driving

Protects early cash flow

Can delay paid driver hires

Can reduce near-term payroll

Only helps if hours stay booked

Owner-dispatching

Can delay admin hires

Model already includes $65,000 Lead Dispatcher

Model already includes $90,000 Operations Manager

More fleet means more overhead risk

Luxury Limo Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Booked Utilization

8-30 hrs

More booked hours spread the fixed fleet and office cost across more revenue, so this is the biggest swing on owner take-home.

2

Premium Rates

160-280/hr

Year 1 pricing runs from $160 to $280 per hour, so mix and rate discipline move margin fast.

3

Vehicle Reserves

$118K

The model bottoms at $118K cash in Month 8, so reserve timing and vehicle funding decide how much owner cash survives expansion.

4

Chauffeur Pay

9%-7%

Direct chauffeur compensation falls from 9% to 7% of revenue, but added dispatch and service staffing still needs tight control.

5

Insurance Load

$10K/mo

Fleet and liability insurance is $10K a month, and fuel plus vehicle costs add another 10% to 8% of sales, so small volume dips hit cash hard.

6

Client Mix

$750

Year 1 CAC is $750, and the customer mix shifts over time, but Year 2 to Year 5 mix shares need normalization before you trust the forecast.

Luxury Limo Service Core Six Income Drivers

Booked utilization per vehicle

Booked Utilization Per Vehicle

Booked utilization means paid, profitable hours, not just an open calendar. For Year 1, the model points to 6,525 billable hours and about $204 of revenue per booked hour. If you miss that pace, owner cash gets squeezed fast because the business still carries $25,800 in monthly fixed costs plus salaried payroll.

Break-even is about 5,833 booked hours per year before vehicle debt and reserves. That means empty airport waits, deadhead miles, and unpaid standby time do not help pay the owner. Here’s the quick math: more booked hours spread fixed cost over more revenue, so take-home pay rises only when paid hours stay high and the vehicle stays on revenue work.

Measure Paid Hours, Not Calendar Time

Track booked hours per vehicle, billed hours, and revenue per booked hour each week. Split out airport transfers, corporate hourly, and event work so you can see where paid time is dense and where it leaks. If one vehicle is calendar-full but booked-hour light, the fleet looks busy but owner income still lags.

Set a floor for each vehicle at 5,833 annual booked hours on the supplied cost base, then forecast around that number. The fix is simple: tighten minimums, reduce unpaid wait time, and push more hours into paid bookings. What this estimate hides is vehicle debt and replacement reserves, which will raise the real cash break-even.

1

Premium pricing and package mix

Premium pricing and package mix

Price has to match the job, not just the car. Year 1 segment rates are $180 corporate hourly, $160 airport transfer, $220 event private hire, and $280 multi-day tour, with booking values of $1,440, $400, $1,320, and $7,000. If the quote ignores vehicle class, chauffeur level, minimum booking length, wait time, or gratuity, margin drops fast.

Higher-value event and multi-day work can lift owner take-home income because one booking brings more revenue into the month, but only if chauffeur hours, cleaning, fuel, and vehicle wear stay below price. The risk is simple: a full calendar with underpriced packages can still produce weak cash flow if direct trip costs outrun the rate.

Price each package to protect margin

Track revenue and direct cost by trip type, not just by month. Compare booking value, chauffeur hours, wait time, cleaning, fuel, and vehicle wear for each segment, then raise rates or set minimums where the margin is thin.

Bill wait time clearly.

Set minimum booking lengths.

Separate gratuity from base price.

Test higher rates on premium jobs.

One clean rule helps: if a package cannot cover its direct trip costs, it is not premium pricing. That is the line between busy revenue and income the owner can actually pay themselves from.

2

Vehicle financing and replacement reserves

Vehicle debt and replacement reserves

Debt service, down payments, depreciation, and replacement reserves decide how much booked profit turns into owner cash. The model already includes $10,000 per month for fleet and liability insurance and 10% of Year 1 revenue for fuel and vehicle direct costs, but it does not set a vehicle payment or reserve. That gap can make accounting profit look stronger than cash.

Here’s the quick math: at a 74% contribution margin, each extra $100,000 of annual debt service or reserve needs about $135,100 of revenue to cover it. If revenue is below that level, owner pay gets squeezed fast because the cash drain happens before distributions.

Track cash, not just profit

Build a monthly schedule for vehicle loan principal, interest, and replacement reserve contributions. Then compare it with booked hours and hourly rates so you know how much each vehicle must earn before owner draw. One clean rule: if a vehicle cannot cover its monthly debt and reserve load, it is not paying for itself.

Track days off-road, repair spend, and replacement timing by unit. Keep a reserve target per mile or per vehicle year, and test pricing on long bookings, since idle time and underpriced hours make the reserve harder to fund.

3

Chauffeur payroll and staffing model

Chauffeur Pay and Coverage

Keep chauffeur payroll separate from owner pay. In Year 1, direct chauffeur compensation is modeled at 9% of revenue, plus a $75,000 Senior Chauffeur role for fleet oversight, while owner salary is a separate $150,000. If bookings rise faster than staffed hours, overtime and part-time coverage can push labor up fast and squeeze the cash left for owner draw.

What this estimate hides is service risk. If you cannot cover booked hours with reliable drivers, cancellations and weak reviews can cut repeat demand, which hurts revenue twice: fewer completed trips and lower future bookings. One missed high-value client can matter more than a week of small jobs.

Track Staffing Before You Scale

Measure booked chauffeur hours, overtime hours, part-time fill rate, and trips covered per driver. Here’s the quick math: payroll stays manageable only if added revenue covers the 9% chauffeur cost and the fixed $75,000 oversight role before owner salary. Define gratuity policy and service standards up front so pay does not drift with every job.

Track completed bookings per chauffeur

Cap overtime before margin slips

Test part-time backup coverage

Log cancellations and review scores

4

Insurance, licensing, maintenance, and compliance

Insurance and compliance costs

The cash hit here is bigger than the insurance bill. Commercial limo insurance, permits, airport access, inspections, detailing, tires, repairs, and safety checks all cut distributable cash. The supplied fixed load is $10,000 per month for insurance plus $7,000 per month for storage and detailing rent, or $204,000 a year before fuel and repairs.

Fuel and vehicle direct costs are modeled at 10% of Year 1 revenue. These are market-dependent planning inputs, not legal or insurance advice, and missing them makes owner take-home look better than cash reality. One clean rule: if the fleet cannot cover these bills from booked margin, the owner’s draw is too high.

Track the real cash burn

Build the forecast by vehicle and by month, not as one annual lump. Track $10,000 insurance, $7,000 rent, permits, airport access fees, inspection dates, detailing, tires, repairs, and fuel at 10% of Year 1 revenue. That tells you if each booked hour is funding the fleet, not just creating paper profit.

$17,000 fixed monthly base

Airport access and permit costs

Inspection and re-inspection timing

Tires, repairs, and detailing cash

Fuel as 10% of revenue

Update the model before paying yourself. If a market raises access fees or repair cycles, owner income drops fast even when bookings stay strong. Keep a cash reserve for compliance and maintenance so distributable cash reflects real fleet cost, not just booked revenue.

5

Recurring client mix and acquisition cost

Recurring client mix

Repeat corporate, hotel, event planner, venue, and airport transfer accounts keep the calendar fuller and cut idle time. With a Year 1 mix of 40% corporate hourly, 35% airport transfer, 20% event private hire, and 5% multi-day tour, income is steadier when clients rebook instead of forcing the owner to chase one-off rides.

Here’s the quick math: $150,000 of marketing at $750 CAC means about 200 acquired customers in Year 1. Discount bookings can help fill gaps, but if they don’t cover chauffeur, vehicle, and overhead costs, they raise activity without improving owner take-home pay.

Track repeat mix vs CAC

Measure revenue by account type, not just total bookings. The key check is whether each job leaves enough cash after direct ride costs, because low-price filler can look busy while profit stays thin.

Track repeat bookings by account type.

Compare CAC to first-year profit.

Set minimum price floors for discount jobs.

Push rebookable accounts first: corporate travel, hotels, and planners. They lower the cost per booking and make cash flow more predictable, which helps the owner pay themselves on time.

6

Luxury Limo Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: Compare owner income sensitivity across low, base, and high luxury limo service cases

Owner income scenarios

Owner pay moves with weighted bookings, average rate, and fleet use. Insurance, vehicle payments, and staffing keep pay tight until volume clears break-even.

Low, base, and high cases show how booking volume changes founder pay.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Lower bookings and weaker utilization keep owner pay below the founder salary and make draws vulnerable to debt service and reserves.

Modeled volume covers the founder salary, but leaves little cash for owner distributions after debt service and reserves.

Higher bookings and better utilization create owner upside after salary, once fixed costs spread across more hours.

Typical setup

Volume stays below 75 weighted bookings per month, rates stay soft, and fixed costs like insurance and vehicle payments absorb most gross profit.

Around 75 weighted bookings per month, with the modeled mix of corporate, airport, event, and tour work, supports the $150,000 salary.

Each extra 10 weighted bookings per month adds about $159,600 annual revenue and about $118,100 operating profit before debt, reserves, and taxes.

Cost drivers

Booked hours

average rate

vehicle payments

insurance

reserves

Fleet size

booked hours

average rate

chauffeur coverage

operating margin

More bookings

higher rate

larger fleet

stronger utilization

lower unit marketing cost

Owner income rangeBefore owner reserves

Below $150,000Low income

$150,000Salary covered

Above $150,000Upside case

Best fit

Use this to stress test cash strain if demand comes in below plan.

Use this as the core operating case for staffing, dispatch, and marketing.

Use this to test added fleet capacity, chauffeur coverage, and cash needs in growth.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

In this planning model, the owner salary is $150,000 in the first year before personal taxes That pay is supported only if the business reaches about $119M in revenue before vehicle debt and replacement reserves Below that, the owner may need to defer salary or reduce distributions

Break-even depends on booked hours, not time alone With the supplied Year 1 costs, the model needs about $99,000 in monthly revenue, or roughly 75 weighted bookings per month at $1,330 per booking Vehicle debt, replacement reserves, and slower onboarding would push break-even higher

You need enough paid utilization to cover fixed costs, payroll, and fleet costs The model does not provide fleet count, so the cleaner test is revenue per vehicle: booked hours per vehicle multiplied by about $204 per booked hour One underused limousine can lose money faster than a small, tightly booked fleet

The biggest pressure points are vehicle financing, insurance, storage, payroll, marketing, and maintenance The supplied fixed costs include $10,000 per month for fleet and liability insurance and $7,000 for storage and detailing facility rent The model also includes a $150,000 first-year marketing budget and at least $420,000 in known salaries

A stronger mix has repeat corporate, airport, event, and multi-day bookings priced above chauffeur and vehicle cost Year 1 assumes 40% corporate hourly, 35% airport transfer, 20% event private hire, and 5% multi-day tour The warning is simple: recurring demand is good only when it protects margin, not when discounts fill idle hours

About the author

Oliver Pierce

Startup Cost Researcher

Oliver Pierce is a startup cost researcher at Financial Models Lab, where he writes practical guides for people planning their first business. He focuses on break-even planning and on comparing business ideas by cost and effort, with a clear, realistic approach to small business planning. His work is aimed at non-finance readers and is written to make business planning easier to understand and use.

Choosing a selection results in a full page refresh.