How Much Does A Makeup Artist Business Owner Make? $70K Pay Model

Makeup Artist Bundle

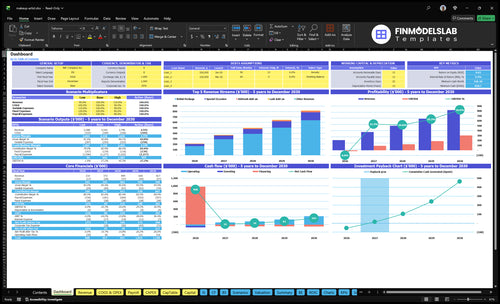

You’re not just asking what an artist earns per appointment you’re asking what the owner keeps after products, help, rent, marketing, and reserves In this five-year US model, the owner salary is $70,000 per year, while EBITDA moves from -$15,000 in Year 1 to $301,000 in Year 5

Owner income$70kNet margin81%→84%Revenue for target pay$264kBusiness difficultyHard

Want to test your own makeup artist income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on bookings, pricing, payroll, taxes, reserves, and seasonality.

Want to check owner income in the Makeup Artist financial model?

What makeup artist business expenses reduce profit margin?

In a Makeup Artist business, profit margin gets hit fastest by labor, supplies, and inventory—see the What Is The Estimated Cost To Open And Launch Your Makeup Artist Business? setup costs for the start-up side. Year 1 listed variable costs equal 195% of revenue, with 35% professional supplies, 45% retail inventory COGS, 90% freelance artist fees, and 25% transportation.

Big margin drains

195% of revenue goes to variable costs

90% freelance artist fees hit hardest

45% retail inventory COGS cuts margin

35% professional supplies still add up

Fixed cost pressure

$2,320/month fixed overhead before payroll

$135,000 Year 1 payroll total

$70,000 owner salary is included

$40,500 startup capex, before taxes

How much do bridal makeup artists make?

A Makeup Artist can earn more per booking from bridal work because Year 1 bridal packages are $450 versus $125 for special occasion jobs. Still, bridal is not automatically better: the model starts with 50% bridal services and shifts to 40% by Year 5 as occasion and retail mix grow, so profit depends on pricing discipline and utilization.

Bridal booking value

$450 bridal package in Year 1

$125 special occasion booking

Higher ticket lifts average booking value

Party size can raise the total sale

Profit drivers

Trial fees and deposits add margin

Travel and early-start fees matter

Assistant costs can cut profit fast

Seasonality changes utilization and owner pay

How much can a solo makeup artist make?

A solo Makeup Artist can model $70,000 in owner salary before taxes and reserves, but Year 1 still shows -$15,000 EBITDA, so cash is tight early. For the operating yardstick, track booking volume and margin together; What Is The Most Important Measure Of Success For Your Makeup Artist Business? matters because a full calendar helps, but margin pays the owner.

Modeled Income

$70,000 owner salary modeled

-$15,000 Year 1 EBITDA

880 visits in Year 1

2,080 visits by Year 5 with support

Capacity Limits

Travel cuts billable time

Weekends carry demand

Prep length caps volume

Team support lifts capacity

Makeup Artist Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six makeup artist income drivers?

1

Booking Volume

4-8/day

More daily bookings lift income fast because rent and core staff costs are fixed.

2

Booking Value

$125-$575

Pushing more work into the $450-$575 bridal package raises revenue per slot.

3

Service Mix

50%-40%

Bridal work pays best, so mix changes can swing income even when visit count stays flat.

4

Variable Costs

19.5%-16%

Supplies, inventory, freelancer pay, and transport eat less profit as that ratio falls.

5

Marketing

High

Better lead flow and close rates fill empty slots, which is pure profit after fixed costs are covered.

6

Overhead

-$15K-$301K

Fixed overhead is $2,320 a month, and owner income is salary plus the profit left after that.

Makeup Artist Core Six Income Drivers

Booking Volume And Calendar Utilization

Booking Volume And Calendar Utilization

Income here is driven by paid visits × operating days. In the model, that starts at 4 visits/day across 220 days = 880 paid visits, then scales to 8 visits/day across 260 days = 2,080 paid visits. That lift can raise revenue fast because fixed overhead and payroll do not rise one-for-one.

Here’s the quick math: one extra paid visit per day adds 220 visits/year at the base plan, or 260 visits/year at the higher-day plan. The catch is calendar friction: weekend clustering, travel gaps, cancellations, and owner burnout can push utilization down. If fixed costs are already covered, each extra booking feeds owner pay much more cleanly.

Fill More Paid Slots

Track booked visits per day, operating days, cancellation rate, and travel time between jobs. Use those inputs to forecast real capacity, not just inquiry volume. One clean rule: if the calendar looks full but paid visits are uneven, revenue quality is weaker than it looks.

Watch visits per day weekly.

Cut dead travel between appointments.

Limit weekend overload and burnout.

Use deposits to reduce cancellations.

Better utilization lifts revenue before you add much fixed cost, so the goal is not just more leads. It’s more paid slots on the days you can actually work, with enough buffer to protect service quality and your own stamina.

1

Average Booking Value And Pricing Power

Pricing Power Raises Booking Value

Average booking value is the dollars collected per client visit, including base service, add-ons, retail, and travel. Here, Year 1 pricing is $450 bridal, $125 occasion, $60 airbrush, $30 lash, $40 retail, and $25 travel; by Year 5, those rise to $575, $160, $75, $40, $55, and $40. That higher ticket drops more cash to the owner because costs do not rise one-for-one with price.

The key inputs are service mix, add-on attach rate, retail sales per booking, and how often travel fees apply. A bridal booking moving from $450 to $575 adds $125, or 27.8%, before cost changes. One clean rate increase can lift profit fast if the portfolio, reviews, speed, reliability, and local positioning support it.

Track Blended Ticket and Attach Rate

Measure the blended booking value each month: total revenue divided by paid visits. Split it by bridal, occasion, add-ons, retail, and travel so you can see what actually lifts price, not just volume. If bridal stays flat but add-on and retail attach improve, owner income can still rise without adding many more bookings.

Watch for pricing drag when faster booking fills the calendar but lowers average ticket. Price increases only help if close rate stays healthy, so test new rates against inquiry volume and booked-client mix. If the business sells more lower-priced occasion work, use add-ons and travel fees to keep the average booking value strong.

2

Service Mix

Service Mix

Service mix is the split between bridal, occasion makeup, add-ons, retail, and related work like photoshoots or performance jobs. In the model, it starts at 50% bridal, 35% occasion, 10% add-ons, and 5% retail, then shifts by Year 5 to 40%, 40%, 12%, and 8%. Bridal can raise ticket size, but more occasion work can smooth the calendar and steady owner pay.

To estimate income from mix, track bookings by type, average ticket, add-on attach rate, retail attach rate, and the time each job takes. The key tradeoff is simple: more bridal can lift revenue per booking, while more occasion work can reduce empty days. If bridal jobs are heavy but uneven, cash can come in bursts instead of a steady weekly draw.

Track Margin by Service

Measure each service line on its own. Tag every booking as bridal, occasion, add-on, retail, photoshoot, or performance work, then compare revenue against the time and product used. A 40% bridal / 40% occasion mix can be healthier than a pure bridal book if it keeps the calendar fuller and reduces dead time between jobs.

Watch the attach rate on add-ons and retail closely. The Year 5 mix moves from 10% add-ons and 5% retail to 12% and 8%, and that matters because these sales add revenue without taking many extra booking slots. If local demand weakens for bridal, shift toward occasion work to protect utilization.

Bookings by service type

Add-on attach rate

Retail sales per client

Idle days between jobs

3

Product Costs And Subcontractor Fees

Product Costs And Subcontractor Fees

When variable costs run this high, each booking leaves less for the owner after product, freelance help, transport, and retail inventory are paid. In the model, Year 1 variable cost is 195% of revenue, so $100 booked can absorb $195 in costs before rent or payroll; Year 5 improves to 160%, but the margin is still pressured.

Track each booking’s mix: supplies, travel, retail stock, and subcontractor pay. The big risk is using assistants for larger parties without raising price enough, because that can grow sales but shrink take-home profit. Keep variable costs separate from fixed overhead so you can see whether a booking actually helps owner income.

Measure Margin Per Booking

Use booking value, travel, product usage, retail inventory, and freelance fees to cost every job. One clean rule: if a party needs extra artists, the quoted price must cover the added labor and still leave margin. Otherwise, the job can boost revenue but cut cash available for owner pay.

Test pricing by job type and log actual costs after each event. That gives you a real variable-cost rate instead of a blended guess. If the rate stays near 195% early on, the business is spending more in variable costs than it brings in per booking, so the fix is either higher pricing, better product control, or a tighter subcontractor plan.

4

Marketing And Booking Conversion

Booking Conversion

Marketing only helps income when it turns into paid jobs. In this model, fixed marketing and branding is $200/month, so the real test is cost per booked client, not views. Here’s the quick math: if fast follow-up, strong portfolio work, reviews, and vendor referrals lift the close rate, the same spend can buy more bookings and protect owner pay.

Watch the downside too. When replies are slow or the work looks generic, leads leak out and that $200 becomes sunk cost. The Year 3 0.5 FTE marketing coordinator and Year 5 1.0 FTE add fixed cost, so conversion has to improve before payroll expands. Better booking quality also supports higher pricing on bridal and special event work.

Track Cost Per Booked Client

Measure the inputs that actually drive bookings: leads by source, booked clients, close rate, and average booking revenue. Use this formula: cost per booked client = marketing spend ÷ booked clients. A stronger portfolio, more reviews, and faster replies should lower that cost and raise booked revenue without adding much fixed overhead.

Track reply time on every inquiry.

Compare close rate by source.

Test referral-heavy channels first.

Review average booking revenue monthly.

What this estimate hides: paid traffic can look busy but still miss profit if it brings low-value clients or weak repeat demand. Tie marketing to booked work, not clicks, and cut any channel that fills the calendar with low-margin jobs. That is how the owner protects cash flow and keeps more profit available to pay themselves.

5

Overhead, Travel Model, And Reserves

Fixed Overhead, Travel, And Cash Reserve

Fixed overhead is $2,320/month before payroll, or $27,840/year. That includes $1,500 rent, $250 utilities, $80 insurance, $60 booking software, $30 website, $200 marketing, $150 accounting and legal, and $50 supplies. This cost sits under every booking, so owner pay only grows after the base load is covered.

Mobile work can trim rent, but it adds mileage and dead time between clients. Here’s the quick math: if travel is not priced into the booking, the business may look busy and still miss cash targets. The model also shows $859,000 minimum cash in Month 2, so profit draws should wait until the operating cushion is safely covered.

Track Cash Before Owner Pay

Build the reserve from the real inputs: studio rent, travel miles, drive time, booking count, and no-show rate. If you switch to more mobile visits, test the net change after gas, vehicle wear, and lost bookable hours. One clean rule: don’t take distributions until cash stays above the month-two floor and the overhead run rate is covered.

Watch cash per booked client and travel cost per visit every month. If a route cluster saves time, keep it; if scattered visits raise dead time, charge more or tighten service area. For this kind of business, the best reserve is not extra profit on paper, but enough cash to pay rent, software, and supplies without touching owner draw.

6

Makeup Artist Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high makeup artist income scenarios

Owner income scenarios

Owner income swings with visit volume, service mix, travel fees, and payroll. Year 1 is tight, Year 2 turns solid, and Year 5 shows the upside if the calendar stays full.

Shows how low, base, and high booking paths change owner pay.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Low Case is the slower earnings path, with Year 1 still at a loss.

Base Case is the modeled run-rate path, with Year 2 EBITDA at $94,000.

High Case is the stronger earnings path, with Year 5 EBITDA at $301,000.

Typical setup

Year 1 runs at 4 visits a day over 220 days, with $450 bridal, $125 occasion, 50% bridal mix, $2,320 monthly fixed overhead, and $135,000 payroll.

Year 2 runs at 5 visits a day over 230 days, with $480 bridal, $135 occasion, $28 travel fees, and $94,000 EBITDA.

Year 5 reaches 8 visits a day over 260 days, with $575 bridal, $160 occasion, $40 travel fees, and $301,000 EBITDA.

Cost drivers

4 visits/day

220 operating days

$450 bridal pricing

$125 occasion pricing

$135,000 payroll

5 visits/day

230 operating days

$480 bridal pricing

$135 occasion pricing

$28 travel fees

8 visits/day

260 operating days

$575 bridal pricing

$160 occasion pricing

$40 travel fees

Owner income rangeBefore owner reserves

$55,000Low Case

$164,000Base Case

$371,000High Case

Best fit

Use this to test a slow launch and whether the owner can cover payroll.

Use this as the core planning case for a stable year-two operating level.

Use this to test upside if the calendar stays full and pricing holds.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; owner economics before taxes may equal salary plus available EBITDA, less reserves.

The researched model uses a $70,000 annual owner salary Profit is separate: EBITDA is -$15,000 in Year 1, $94,000 in Year 2, and $301,000 in Year 5 If EBITDA is distributed, owner economics rise, but taxes, reserves, debt service, and reinvestment still reduce cash kept

The model reaches breakeven in Month 7 and payback in 28 months That assumes visits grow from 4 per day in Year 1 to 5 per day in Year 2, with operating days moving from 220 to 230 If bookings lag or payroll is hired too early, breakeven can slip

Not always, but this model includes a studio Fixed overhead is $2,320 per month, including $1,500 rent, $250 utilities, and $80 insurance A mobile setup may lower rent, but travel costs and dead time can rise The better choice is the one that fills more paid appointments profitably

Booking volume, average ticket, service mix, and labor cost drive profit fastest Year 1 variable costs total 195% of revenue, while fixed overhead is $2,320 per month before payroll Bridal pricing starts at $450, much higher than $125 for special occasion work, so mix matters

Raise owner pay after the calendar and margin prove it Start by increasing booked visits, protecting premium bridal pricing, charging travel fees, and keeping product and freelance costs in line The model’s owner salary is $70,000, but EBITDA only turns strongly positive after Year 1, reaching $94,000 in Year 2

About the author

Liam Foster

Business Idea Researcher

Liam Foster is a business idea researcher at Financial Models Lab, focused on the revenue and profit basics that early-stage founders need when preparing a simple business plan. He helps simplify business plans for non-finance readers by turning business model overviews into clear, practical insights. With a simple, confident approach, Liam breaks down revenue, expenses, and profit in a way that makes financial thinking easier to understand and use.

Choosing a selection results in a full page refresh.