MSA Service Owner Income: $175k Pay, Month 9 Break-Even

You’re hiring before the model fully turns profitable, so owner income needs a cash view, not just a revenue view In this five-year US planning case, the owner role is modeled at $175,000 per year, with revenue growing from $912,000 in Year 1 to $4288 million in Year 5 The model reaches breakeven in Month 9, but distributions depend on reserves, taxes, debt, and cash policy

Owner income$175kNet margin-16% to 35%Revenue for target pay$505kBusiness difficultyHard

Want the six MSA income drivers?

1

Price per Study

$9K-$12.7K

A Year 1 MSA study at $9,000 can reach about $12,720 by Year 5, so higher rates flow straight into owner income after fixed costs.

2

Billable Load

22-30h

Active customer hours rise from 22 to 30 per month, so the same account base produces more revenue without a matching jump in overhead.

3

Client Mix

60%-70%

The $45K-$85K marketing budget has to keep enough MSA Study Services in the pipeline, because that mix carries the strongest price per hour.

4

Margin Control

70%-78%

Travel, lab fees, commissions, and subcontracting keep contribution margin in the 70% to 78% range, and that is what funds take-home.

5

Fixed Overhead

$11.6K/mo

Monthly fixed overhead is $11,600, so cash has to clear a steady hurdle first; EBITDA is not automatically distributable cash because taxes and reserves still matter.

6

Team Scale

1-5 FTE

Scaling the senior consultant from 1 to 5 FTE, and the technician from 1 to 3 FTE, lets revenue grow faster than the owner's own hours.

Want to test your MSA owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the MSA forecast?

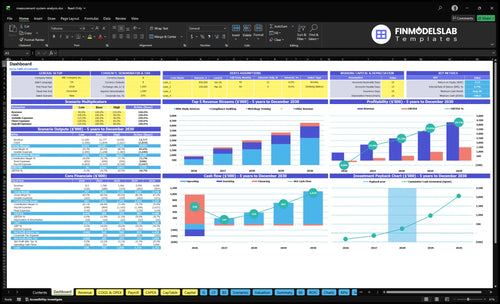

The screenshot shows the planning layer behind owner income tabs, dashboard, assumptions, revenue build, direct costs, payroll, fixed overhead, marketing, capex, cash flow, scenarios, and outputs for Measurement System Analysis Service; revenue runs from $912,000 to $4.288 million, EBITDA from -$144,000 to $1.489 million, with breakeven in Month 9 and payback in 33 months. Open the Measurement System Analysis Service Financial Model Template to test pricing, utilization, subcontractors, reserves, and owner pay.

Owner-income model highlights

Owner pay is modeled

Revenue and EBITDA range

Test key assumptions

How much to charge for measurement system analysis services?

For Measurement System Analysis Service, price MSA consulting by hours, complexity, onsite work, report depth, and client urgency. A solid Year 1 planning rate is $225/hour for MSA Study Services, $250/hour for Compliance Auditing, and $200/hour for Metrology Training, which puts a 40-hour study at $9,000, a 24-hour audit at $6,000, and a 16-hour training job at $3,200. By Year 5 planning, those same model examples rise to $12,720, $8,120, and $4,800, but these are owner-income planning assumptions, not universal market rates.

Year 1 rates

$225/hour for MSA studies

$250/hour for audits

$200/hour for training

$9,000 for 40 hours

Year 5 examples

$12,720 for a study

$8,120 for an audit

$4,800 for training

Plan rates, not market quotes

How many measurement system analysis projects per month to pay the owner?

Using the stated unit economics, a Measurement System Analysis Service needs about 3 MSA projects per month to pay a $175,000 owner salary, or about 5 projects per month to cover owner pay, fixed overhead, and Year 1 marketing; see How Increase Measurement System Analysis Service Profitability?. The 23 and 48 project targets only work if contribution is about $630 per study, not the stated $6,300.

Quick math

Owner pay: $14,583/month

Study revenue: 40 × $225 = $9,000

Contribution: $9,000 × 70% = $6,300

Owner-only need: $14,583 / $6,300 = 2.3 studies

Real caveats

Add fixed overhead: $11,600/month

Add Year 1 marketing: $3,750/month

Total need: $29,933 / $6,300 = 4.8 studies

Capacity, travel, reporting, and subcontractors can shift this fast

What costs reduce MSA service owner take-home?

Your take-home gets squeezed first by the 30% variable-cost stack in a Measurement System Analysis Service: 12% travel and field per diem, 5% lab verification, 5% sales commissions, and 8% project subcontracting, which leaves a 70% contribution margin. Then fixed costs and payroll cut deeper, so gross margin is not the same as owner take-home; see What Are The Operating Costs For [BusinessName]? for the full cost lens.

Year 1 cost stack

12% travel and field per diem

5% lab verification

5% sales commissions

8% project subcontracting

Cash drains that hit take-home

$11,600/month fixed overhead

$45,000 year-one marketing

$517,500 year-one payroll

$175,000 owner pay inside payroll

That fixed overhead equals $139,200 a year, before marketing and payroll. Capex also ties up cash in reference standards, mobile lab equipment, workstations, a vehicle, and a digital audit toolkit, and rework plus unpaid reporting time can still leak margin even when revenue looks strong.

Key Takeaways

Higher project rates drive most owner income growth.

Billable hours protect the $175,000 take-home target.

Audit-driven clients support premium, repeatable work.

Margins improve from 70% to 78% with discipline.

Compare lean, base, and high-performance MSA owner-income cases

Owner income scenarios

Owner income shifts with billable hours, service mix, and payroll. Year 1 stays cash tight, Year 3 opens room for draws, and Year 5 has the most upside.

Low, base, and high owner income cases for planning.

Scenario

Low CaseDownside

Base CaseBaseline

High CaseUpside

Launch model

Lower earnings path where cash stays tight and owner pay remains conservative.

Modeled case where income turns on after Month 9 breakeven and cash starts to support owner draws.

Stronger earnings path with the most room for owner pay and reserve-funded distributions.

Typical setup

Year 1 model: $912,000 revenue, about 70% contribution margin, $517,500 payroll, $45,000 marketing, and -$144,000 EBITDA, so owner pay stays at the modeled $175,000 level.

Year 3 model: $2.492 million revenue, about 74% contribution margin, $900,000 payroll, $65,000 marketing, and $537,000 EBITDA, which can support salary plus reserve-funded distributions.

Year 5 model: $4.288 million revenue, about 78% contribution margin, $1.255 million payroll, $85,000 marketing, and $1.489 million EBITDA, but take-home still depends on taxes, financing, depreciation, and reserve policy.

Cost drivers

billable hours

payroll load

marketing spend

negative EBITDA

slow cash build

higher volume

service mix

payroll growth

marketing spend

EBITDA cushion

top-line growth

stronger margin

larger payroll

marketing scale

reserve policy

Owner income rangeBefore owner reserves

$175,000 salaryCash tight

Salary plus reserve drawsReserve-funded

Salary plus distributionsUpside case

Best fit

Use this to stress-test launch cash and keep owner pay conservative until utilization improves.

Use this for the main operating plan once demand and staffing are stable.

Use this to test upside if project flow stays strong and owner draws rise from retained cash.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Measurement System Analysis Service Core Six Income Drivers

Project Pricing Power

MSA Project Pricing Power

Project pricing power raises owner income because much of the delivery cost is semi-fixed once travel and analysis time are set. A $225/hour rate on a 40-hour MSA study is $9,000; at $265/hour and 48 hours, the same work reaches $12,720. Each $10/hour increase on a 40-hour study adds $400 revenue before variable costs.

The upside is strongest on complex studies, multi-site work, regulated manufacturers, and executive-ready reports. The risk is simple: not every client will pay premium fees without proof, speed, and audit-ready documentation, so weak scope control can turn price gains into rework and margin loss.

Price for proof, not just hours

Track realized hourly rate, proposal win rate, and hours spent on travel, analysis, and rework. If premium pricing is not sticking, show the buyer what they get: clear methods, clean documentation, and fast delivery. That is what supports higher owner pay.

Quote by study complexity

Charge extra for multi-site work

Track scope creep by project

Measure report turnaround time

Use audit-ready templates

For regulated accounts, tie price to compliance risk and documentation load. If a client wants faster delivery or executive-ready reporting, price that extra effort up front so the margin stays intact and cash flow stays clean.

Billable Utilization

Billable Utilization

Owner income rises when more of the month is sold as paid analysis, onsite study execution, training, auditing, or reporting. The key source metric is billable hours per active customer, which grows from 22 in Year 1 to 30 in Year 5, so the same client base can produce more revenue without a matching jump in overhead.

Here’s the quick math: MSA studies move from 40 to 48 hours, compliance audits from 24 to 28 hours, and training from 16 to 20 hours. Unpaid sales calls, proposals, travel, admin, and rework cut usable capacity, and that can block the $175,000 owner pay target even when demand is steady.

Track Paid Hours, Not Just Projects

Track billable versus non-billable hours by customer and by service line. If repeat accounts are strong, you should see more time in paid work and less leakage into travel, admin, and rework.

Log hours by active customer.

Split paid and unpaid time.

Watch repeat work share.

Pack onsite visits tightly.

Use scheduling to protect deep-work blocks for analysis and reporting. If utilization slips, the fix is usually more billed hours per customer, tighter scope, or fewer wasted handoffs.

Staffing and Subcontractor Leverage

Staffing and Subcontractor Leverage

This driver is about how many Senior Quality Consultants and Metrology Technicians you can deploy without letting rework cut into margin. The model scales from 1 to 5 FTEs for senior staff and 1 to 3 FTEs for technicians, while subcontracting drops from 8% to 4% of revenue. That adds capacity, but every added hand also adds review time and quality-control risk.

Here’s the quick math: wages are $135,000 per senior consultant, $85,000 per technician, plus $95,000 for business development and $55,000 for an admin coordinator. The model’s revenue range rises from $912,000 to $4.288 million, but owner income only improves if the team keeps work accurate and billable. If quality slips, rework and client loss can erase the margin gain fast.

Track capacity before you add headcount

Measure billable hours, review hours, and subcontractor share by project. If senior staff spend too much time checking others’ work, the extra capacity is fake and cash flow looks better than it is. The key inputs are staffed FTEs, wage load, subcontractor cost, and the hours lost to QA review.

Watch billable hours per FTE.

Track rework on every file.

Cap subcontracting to needed gaps.

Require sign-off before delivery.

Keep subcontractors for overflow or niche tasks, and keep the owner at 1 FTE on client oversight. That protects margin and helps the business pay the owner more consistently, instead of turning growth into hidden labor cost.

Recurring and Repeat Work

Repeat Work

Recurring measurement system analysis work closes sales gaps and smooths owner pay. If active customers grow from 22 to 30 billable hours per month, that is a 36% lift in hours per account before pricing changes. More annual reviews, training refreshers, and supplier quality audits also spread fixed selling time over more revenue.

Here’s the quick math: repeat clients cut marketing CAC from $2,500 to $2,000, a $500 drop per customer. That helps cash flow and raises the share of revenue that can reach profit and owner draw. What this hides: not every MSA project turns into a retainer, so retention has to be tracked by account and service line.

Track Repeat by Service Line

Measure repeat rates for MSA studies, annual reviews, training refreshers, and supplier quality audits separately. That tells you which offers create steady work and which ones stay one-off. If repeat hours rise but CAC does not fall, the owner may have more work without better income quality.

Use a simple forecast: active customers × billable hours × hourly rate. Then compare it with the month’s sales pipeline and unpaid proposal time. Protect margin by keeping rework low and making renewal asks part of every closeout. One clean rule: if a client needs the same audit twice, turn it into a review plan.

Track hours by account.

Separate study and retainer work.

Watch CAC by source.

Log renewal dates early.

Price reviews before scope grows.

Client Mix and Compliance Urgency

Compliance-Driven Mix

When more clients are under audit deadlines or corrective action plans, pricing usually gets firmer and repeat work becomes more likely. For this model, MSA Study Services rises from 60% to 70%, Compliance Auditing from 40% to 60%, and Metrology Training from 20% to 40%. Audits carry the highest Year 1 rate at $250 per hour, so the mix shift can lift revenue per booked hour and owner draw.

The inputs are active customers, audit timing, customer corrective actions, regulated quality needs, and hours sold by service line. Standards like ISO 9001 and IATF 16949 matter because they make urgency real. What this estimate hides: demand is not automatic; sales still depend on credibility, referrals, proof of work, and fast delivery.

Track Deadline-Driven Work

Watch the share of hours tied to audit deadlines and corrective actions, then price those jobs as urgent, not generic. Here’s the quick math: if higher-urgency work shifts booked hours toward the $250 per hour audit rate, revenue per consultant hour rises before travel or rework costs. That can support steadier cash flow and a bigger owner paycheck.

Use a weekly tracker for mix by service line, close rate by referral source, and repeat work by account. If the urgent mix is rising but win rates are flat, the bottleneck is trust, not demand. Keep proof of work, report speed, and deadline response time tight, because those are the levers that turn compliance pressure into paid hours.

Cost Structure and Margin Protection

Margin Protection

This driver is the gap between billed revenue and what it costs to deliver the study. You need billed revenue, travel miles, lab-verification fees, commissions, subcontractor hours, and monthly overhead to estimate it. In Year 1, 12% travel, 5% lab verification, 5% commissions, and 8% subcontracting leave a 70% contribution margin; by Year 5, those costs fall to 10%, 3%, 5%, and 4%, lifting margin to 78%.

The fixed load is $11,600 per month from insurance, software, office, standards database, admin, and IT. So if revenue is weak or rework rises, that overhead eats profit fast. Here’s the quick math: on $100,000 monthly revenue, Year 1 leaves $70,000 before fixed costs, or $58,400 after them.

Stop margin leakage

Track travel hours, lab-check spend, subcontractor use, and rework on every job. The goal is simple: protect the quoted scope, because rushed reports and poorly planned travel can wipe out pricing gains.

Cap travel before pricing.

Bill change orders fast.

Review reports before release.

Measure rework by project.

Use job-level margin tracking, not monthly averages. If travel or rework runs above plan on one project, fix the estimate or raise the fee on the next one.