How Much Medical Equipment Owners Can Make: $577k First-Year Model

A medical equipment business owner can make about $577k in first-year pre-tax owner-income capacity in this researched model, before debt service, taxes, payroll not provided in the data, and replacement reserves The model assumes $855k in first-year revenue, 10% direct and refurbishment cost of goods, 9% variable expenses, and $1152k in fixed overhead By the fifth model year, revenue rises to $2210M under the traffic, conversion, repeat order, and pricing assumptions, but that is a planning case, not guaranteed owner pay What this estimate hides: inventory, damaged equipment, collections timing, and fleet replacement can hold cash inside the business

Owner income$577kNet margin-41%Revenue for target pay$1.15MBusiness difficultyHard

Want the six main income drivers?

1

Sales Mix

$855K

The Year 1 mix of beds, wheelchairs, oxygen units, monitors, and crutches drives the $855K revenue base, and a better mix lifts cash fast.

2

Utilization

1.1x

At 0.8% visitor conversion, orders average 1.1 units, and repeat buyers are 25% of new customers, so better use of traffic and assets raises revenue without much overhead.

3

Margin Control

81%

Gross margin is about 90% and contribution margin is 81%, so acquisition cost and refurbishment discipline decide take-home.

4

Delivery Efficiency

9%

Logistics and sales commissions start near 9% of sales, so fewer trips and fewer handoffs keep more margin in the business.

5

Payroll Control

$435K

Year 1 fixed overhead plus salary load is about $435K, so staffing discipline decides how fast EBITDA turns positive.

6

Cash Timing

$158K

Minimum cash hits about $158K in Month 17, so reserves and debt terms matter as much as profit on paper.

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Not guaranteed salary, tax advice, or owner distribution advice.

Want to pressure-test Medical Equipment's owner income?

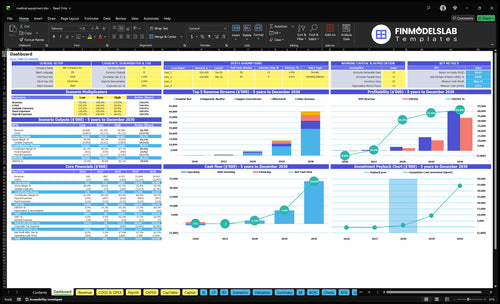

This dashboard shows revenue, gross margin, operating costs, EBITDA-style profit, cash flow, and owner income; open the Medical Equipment Financial Model Template to check it. Charts also show $855k first-year revenue, 90% gross margin, $1.152m fixed costs, and $577k pre-tax owner-income capacity as a planning step, not the main promise.

Owner-income model highlights

Owner take-home output

$855k revenue chart

90% gross margin

$1.152m fixed costs

Traffic, pricing, debt tabs

What medical equipment business margins matter most?

For Medical Equipment, the margin that matters most is owner take-home: first-year gross margin is about 90% after 8% direct equipment acquisition and 2% rental refurbishment, and contribution margin is about 81% after 5% logistics and 4% marketing and commissions. If you’re mapping startup dollars, see How Much Does It Cost To Open And Launch Your Medical Equipment Business? Rentals work only when utilization stays high; downtime, delivery, cleaning, repairs, depreciation, and replacement reserves can wipe out the edge.

Gross margin drivers

90% first-year gross margin

8% equipment acquisition cost

2% rental refurbishment cost

Sales lift profit if warranty risk stays low

Net margin risks

81% contribution margin

5% logistics cost

4% marketing and commissions

Downtime can erase rental gains

How much revenue does a medical equipment business need to pay the owner?

If the owner wants $150k in pay, Medical Equipment needs about $1.61M in revenue before taxes, debt, payroll, reserves, and reinvestment, using a first-year contribution margin of 81%. Here’s the quick math: ($150k + $1.152M) / 0.81 = about $1.61M. Revenue alone does not guarantee cash, because timing on inventory, debt service, and working capital can still squeeze the business.

Revenue math

81% contribution after variable costs

$150k owner pay target

$1.152M fixed costs assumed

$1.61M revenue needed

Cash reality

Debt service lowers cash fast

Payroll is not provided here

Reserves still need funding

Reinvestment can delay owner draw

How does owner role change medical equipment business income?

Owner-operated Medical Equipment can look more profitable because the owner is doing sales, delivery, repairs, billing, and management, so labor is not shown as a separate cost. But that is not the same as true profit when you scale. Once you add staff, storage, insurance, compliance work, larger inventory, and fleet replacement, the margin gets tighter fast.

What owner labor hides

Sales cost is the owner’s time

Delivery work is not priced separately

Repairs stay off the labor line

Billing and management are absorbed

What scaling adds

Utilization risk can stay low

Collections can come in late

Damaged equipment can hit cash flow

Inventory and fleet replacement tie up cash

Key Takeaways

Sales mix drives cash timing and margin quality.

Utilization only helps when downtime stays low.

Fixed overhead sets a $96k monthly break-even floor.

Delivery and service costs already take about 5%.

Compare lean, base, and high-performance owner-income scenarios

Owner income scenarios

Owner income moves with conversion, repeat rentals, route density, and repair costs. This table shows lean, base, and upside planning cases for the same medical equipment model.

Lean, base, and upside owner income cases for planning and cash control.

Scenario

Low CaseOwner-operated

Base CaseStaffed

High CaseFleet-heavy

Launch model

A slower launch with weaker conversion and thin repeat orders keeps owner income tight.

A staffed core model with steady conversion and repeat business supports the modeled income level.

A fleet-heavy model with better conversion, stronger retention, and denser routes lifts owner income.

Typical setup

Traffic is lighter, repeat orders are weaker, utilization stays low, delivery and repair costs run higher, and reserves need to stay larger.

First-year revenue is about $855k, gross margin is about 90%, contribution margin is about 81%, fixed costs are about $1.152m, and pre-tax owner-income capacity is about $577k before taxes, debt, payroll, and reserves.

More visitors convert, repeat customers stay longer, routes run denser, and better buying terms support a higher pre-tax owner-income level.

Cost drivers

Lower conversion

weaker repeat orders

lower utilization

higher delivery costs

higher repair costs

Modeled conversion

steady repeat demand

normal route density

fixed overhead

standard reserves

Higher conversion

stronger retention

denser routes

better buying terms

lower unit costs

Owner income rangeBefore owner reserves

$250k - $400kLean case

$550k - $600kCore case

$700k - $900kUpside case

Best fit

Use this to stress-test an owner-operated opening plan with slower referrals and tighter cash.

Use this as the main staffed operating plan for budgeting, hiring, and cash timing.

Use this to test upside from stronger sales, more fleet use, and better supplier terms.

!

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Medical Equipment Core Six Income Drivers

Sales And Rental Mix

Sales and Rental Mix

Mix drives cash timing and margin quality. In year one, the modeled mix is 30% hospital beds, 25% wheelchairs, 20% oxygen concentrators, 15% diagnostic monitors, and 10% crutches, with a weighted average unit price of $1,22750. That mix matters because sales bring cash in once, while rentals spread cash in over time.

Here’s the quick math: more one-time sales can raise gross profit if acquisition cost stays near the modeled 8%. Rentals can smooth income, but only if utilization stays high and costs for delivery, maintenance, refurbishment, and replacement do not eat the spread. If rental days slip, owner pay drops even when the catalog looks busy.

Track Mix by Margin, Not Just Volume

Measure each product line by sale price, rental days, utilization, and cost to serve. The owner should know which items create the best cash per unit after delivery, setup, cleaning, and replacement. A higher mix of sales can help cash now; a higher mix of rentals can help if units stay on hire and turn fast.

Track revenue by product category

Track rental days per unit

Track repair and replacement cost

Track gross profit after logistics

If one category needs heavy refurbishment or slow delivery, it can cut take-home income fast. So price that work into the mix, and shift more volume toward the lines with the strongest cash yield after the full service cost.

Cash Flow, Reserves, And Debt

Cash Flow, Reserves, And Debt

Operating profit is not cash you can safely take home. In a medical equipment rental and sales business, cash gets tied up in inventory purchases, rental fleet expansion, damaged equipment, replacement units, and slow collections. Even with the modeled 90% gross margin after 8% direct acquisition and 2% refurbishment, owner pay can be much lower if cash is still sitting in stock or receivables.

Loan payments tighten the squeeze. The model should treat debt service and a separate reserve rate or reserve dollar amount as cash needs before any draw. If collections lag or equipment loss rises, the business can look strong on paper but still need cash from the owner to stay liquid.

Protect Cash Before Owner Pay

Build the forecast with these inputs: operating profit, debt payment, reserve amount, inventory buys, fleet additions, and delayed collections. That makes cash available to distribute clearer than the income statement alone.

Use a simple order: profit first, then debt, then reserves, then owner draw. If cash drops below the reserve target, cut distributions before cutting maintenance or replacement spend. That keeps working capital in place and protects the next month’s orders and rentals.

Track cash after debt.

Set a reserve target.

Pay owner last.

Gross Margin And Acquisition Cost

Gross Margin and Acquisition Cost

Gross margin here starts with buying discipline, not just a higher selling price. On the first-year model, 8% direct equipment acquisition plus 2% rental refurbishment leaves a 90% gross margin; by the fifth model year, those costs drop to 6% and 1.5%, lifting gross margin to 92.5%. That extra 2.5 points flows straight into owner income.

Here’s the quick math: every $100 of revenue with $10 of direct cost leaves $90 gross profit. But that margin is fragile if vendor terms, refurbished sourcing, category mix, warranty claims, returns, or compliance exposure push landed cost up. Weak purchasing doesn’t just reduce profit; it can trap cash in inventory that earns nothing.

Track True Landed Cost

Track landed cost per unit, not just purchase price. Include vendor terms, refurbishment spend, warranty obligations, returns, and any compliance-related write-offs. Then compare each category against the model mix so you can see where margin is leaking before it hits owner pay.

Measure cost by equipment type

Separate new vs. refurbished units

Watch warranty and return rates

Test supplier terms each quarter

If a unit costs more to acquire or restore than planned, the business needs more revenue just to stay even. Better buying improves cash flow because less money sits in inventory, and more of each dollar sold can support overhead, debt, and the owner draw.

Overhead And Staffing Efficiency

Overhead And Staffing Efficiency

Fixed overhead sets the break-even floor before owner pay. In this model, fixed costs are $96k per month: $4k warehouse rent, $25k platform hosting and maintenance, $800 insurance, $600 utilities and internet, $1k professional services, $400 supplies and software, and $300 security.

Payroll data is not provided, so owner labor must stay separate from hired labor. That matters because staffing too early can turn strong gross margin into thin cash flow. At a 90% gross margin, the business needs about $106.7k in monthly revenue just to cover this overhead before owner pay.

Track Fixed Burn Before Hiring

Measure monthly fixed burn, then map it to revenue needed at your actual gross margin. Here’s the quick math: $96k ÷ 90% = $106.7k break-even revenue before owner pay. If margin slips or headcount grows, that floor moves up fast.

Keep one clean line for owner pay and one for staff payroll. Track overhead as a share of revenue, hiring plan by role, and payback from each hire. If a new person does not cut delivery time, raise utilization, or reduce errors, delay the hire.

Watch fixed costs monthly.

Separate owner and employee labor.

Hire only after workload proof.

Rental Utilization

Rental Utilization

Rental utilization is the share of rentable equipment that is actively billing. Idle units pay nothing, but storage, insurance, cleaning, maintenance, and replacement still hit cash flow. The key check is revenue per unit-month against downtime and repair days; utilization helps owner take-home only if 2% refurbishment and 5% logistics stay inside plan.

Rentable units available

Billing days per month

Downtime and repair days

Revenue per unit-month

Reserve units needed for swaps

Track Revenue Per Unit

Measure utilization by category and by unit, not just fleet-wide. Use rentable days ÷ available days, then compare each unit’s monthly revenue to its service cost and reserve need. If a bed, wheelchair, or monitor cycles through repairs, the headline rate can look strong while owner cash falls. Better use is only better income when costs stay controlled.

Watch units with repeat damage, long cleanup time, or slow turnaround. If a unit earns less than its monthly carrying cost, move it to sale, retire it, or keep a spare so the fleet can keep billing while one unit is out.

Delivery, Maintenance, And Service Costs

Delivery, Maintenance, And Service Costs

Every delivery, pickup, setup, cleaning, part, and repair takes cash before the owner gets paid. At the model’s 5% logistics and fulfillment rate, that’s $42,750 on $855,000 of revenue. Here’s the quick math: each extra $100,000 of revenue adds about $5,000 of service cost, so growth only helps if route density and repair control stay tight.

The main inputs are order count, delivery distance, technician time, downtime, damaged equipment, and repair turnaround. Good service can drive repeat rentals and sales, but it also raises labor and parts costs. If cleaning or repairs run above plan, distributable owner income falls first, not last.

Price Service Into Every Order

Track service cost per order and by job type: delivery, pickup, setup, cleaning, and repair. If a route or technician team is losing money, fix the schedule, tighten the service radius, or raise the rental and sale price. The goal is to keep total logistics near 5% of revenue, not let it drift with volume.

Use clear damaged equipment rules, set repair turnaround targets, and forecast spare parts needs before they hit cash. Measure downtime days, repeat demand, and labor hours per job. If service quality brings more repeat orders, that helps revenue, but only if the extra work is priced in and still leaves room for owner pay.