How Much Can a Mediterranean Restaurant Owner Make? $60k Salary Plus Profit

Key Takeaways

More covers drive the biggest revenue lift.

Menu price gains help if guests still see value.

Cost control protects margin faster than top-line growth.

Fixed labor and rent can wipe out owner cash.

Owner income$60kNet margin3.4%Revenue for target pay$1.8MBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not a guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Mediterranean Restaurant model?

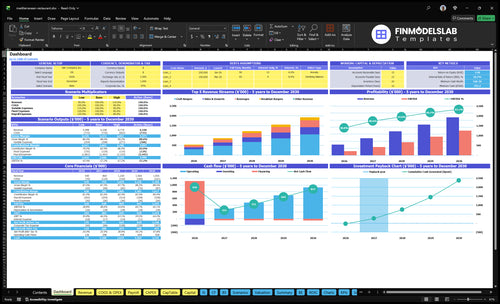

This dashboard in the Mediterranean Restaurant Financial Model Template shows revenue, margin, costs, reserves, and owner take-home, plus $519k sales, $210k EBITDA, $793k cash need, Month 3 breakeven, and 15-month payback—open the model.

Owner-income model highlights

Owner salary and take-home

EBITDA, breakeven, payback

Scenario comparison on inputs

How much revenue does a Mediterranean restaurant need to pay the owner?

A Mediterranean Restaurant owner pay check starts with the monthly payroll line, not the top line. In the Year 1 case, a $60k salary is $5k a month before payroll taxes and benefits, and with $519k average monthly sales that is only about 1% of revenue; the model still has to cover 130% listed COGS, 60% variable costs, and $2,150 in fixed monthly costs. The model shows total payroll at $175k and breakeven in Month 3, but owner distributions should wait until debt, taxes, reserves, and working cash are funded.

Owner pay math

$60k equals $5k monthly

$519k average monthly sales

Pay is about 1% of sales

Total payroll reaches $175k

Cash flow gate

130% listed COGS still gets funded

60% variable costs still apply

Breakeven is modeled in Month 3

Wait on payouts until cash is ready

How much does a Mediterranean restaurant owner make?

A Mediterranean Restaurant owner makes a modeled $60,000 Owner/Manager salary, plus possible distributions if sales, margin, debt, reserves, and reinvestment allow it; track What Is The Overall Customer Satisfaction Level For Your Mediterranean Restaurant? because repeat guests protect that profit pool. Year 1 shows about $6.227M revenue and $210k EBITDA, but EBITDA is not automatic take-home cash.

Owner Pay

$60,000 base Owner/Manager salary

Distributions depend on cash left

Debt payments reduce take-home

Reserves protect slow months

Profit Pool

Year 1 revenue: $6.227M

Year 1 EBITDA: $210k

Year 5 revenue: $2.046M

Year 5 EBITDA: $1.253M, validate locally

Does a Mediterranean restaurant owner make more as an owner-operator?

A Mediterranean Restaurant can look more profitable with an owner-operator because the model includes a $60k Owner/Manager role if the owner works that job, but that is real labor pay, not free profit. If a hired manager replaces the owner at similar pay and sales do not rise, distributable profit falls by about $60k before tax. So the real test is whether the owner’s work creates value above that salary, and a second site needs tight downside protection because the model also shows a $793k minimum cash need, Month 3 breakeven, and 15-month payback.

Owner pay is real

$60k owner salary is labor pay

Unpaid work can overstate profit

Hired manager cuts profit by $60k

Sales must rise to offset it

Second site risk

Minimum cash need is $793k

Breakeven hits in Month 3

Payback runs 15 months

Protect downside before expanding

Mediterranean Restaurant Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Table Turns

700/wk

Seven hundred weekly covers in Year 1 is the biggest income lever, because more seats filled and faster turns feed sales without adding fixed cost.

2

Menu Price

$12.50/$20

Midweek and weekend checks set revenue per guest, so even small price gains lift owner income across every cover.

3

Labor Model

$175K/yr

Year 1 payroll of $175K is a heavy fixed drag, and tight staffing plus the owner's role decide how much gross profit survives.

4

Cost Control

19%

Food, packaging, fuel, and event fees take about 19% of sales, so waste or spoilage drops cash fast.

5

Rent Load

$2.15K

Monthly fixed costs run about $2.15K, and lease terms plus site choice matter because soft traffic still has to cover them.

6

Channel Mix

4 ch.

The split between dine-in, takeout, delivery, and catering changes fees and ticket size, so the mix can raise take-home even at the same cover count.

Mediterranean Restaurant Core Six Income Drivers

Sales Volume And Table Turns

Sales Volume And Table Turns

700 weekly covers in Year 1 growing to 2,010 by Year 5 makes this the strongest top-line driver. More covers raise revenue and owner pay only if service quality holds; if the room slows down, the gain leaks into labor, waste, refunds, and churn.

Table turns means how often a table sells in one service window. Here’s the quick math: more lunch traffic, dinner demand, and weekend volume push covers up, but capacity, hours, and kitchen speed set the ceiling. The source model ties that growth to annual revenue moving from $6,227k to $2,046M under the stated cover and check assumptions.

Protect Covers Without Breaking Service

Track covers by daypart, then watch turn time, wait time, and no-shows. If one dinner shift fills up but lunch stays weak, the fix is staffing and seating flow, not blanket discounting. Keep owner income tied to revenue per seat hour, not just foot traffic.

Measure covers by lunch, dinner, weekend.

Test table turns weekly.

Staff to peak demand.

Cap bookings when kitchen slips.

If volume rises faster than line speed, service drops and repeat visits fade. So forecast covers against labor and prep capacity first, then open more seats or longer hours only when the team can keep checks moving and the guest experience stays tight.

1

Average Check And Menu Pricing

Average Check And Menu Pricing

Average check is the revenue from one guest ticket: entrées, shared starters, beverages, desserts, and catering bundles. In Year 1, the model uses $1,250 midweek and $2,000 on weekends, rising to $1,500 and $2,300 by Year 5. Higher check lifts owner income only when food cost and labor stay flatter than sales.

Here’s the quick math: if a guest adds a drink or dessert, revenue rises without adding a full extra table turn. The model’s Year 1 mix shows beverages at 180% and sides/desserts at 190%, so add-ons matter. What this estimate hides: local competition and guest value perception can cap pricing power, even when demand is healthy.

Track Check By Daypart And Mix

Track check by weekday, weekend, server, and menu item. The inputs that move income are guest count, mix of entrées versus add-ons, drink attach rate, dessert attach rate, and catering bundle price. If weekend check climbs faster than weekday check, owner pay usually improves because fixed costs do not rise one-for-one with each guest.

Test starter, drink, dessert bundles.

Watch check by weekday and weekend.

Price to local value, not guesswork.

Track margin after labor and food.

Raise prices in small steps and compare reorder rates, comp requests, and guest comments. If guests push back, use portion design, bundle pricing, or premium beverages instead of broad menu hikes. The goal is a higher revenue per guest with the same kitchen hours, so the owner keeps more cash after payroll and fixed rent.

2

Food And Beverage Cost Control

Food and Packaging Cost Control

Every point of food or packaging cost cuts straight into owner cash before tax. In this model, food ingredients are 100% of sales in Year 1 and 90% in Year 5, while packaging moves from 30% to 25%. The source lists gross margin after those costs as 870%, so the model should be checked before use. One point of miss is about $62k in Year 1 and $205k in Year 5.

This driver includes recipe costing, portion control, supplier pricing, spoilage tracking, and beverage mix. Estimate it from covers, average check, recipe yield, and packaging per order. If proteins, produce, imported items, or oil rise, margin gets squeezed fast, and the owner’s draw falls even if sales hold. One simple rule: higher sales do not fix bad food cost.

Track plate cost weekly

Measure cost per dish, portion yield, and waste by item each week. Tie every menu item to a recipe card, then compare actual food and packaging spend against sales mix. If a dish misses target, cut the portion, change the spec, renegotiate the supplier, or reprice it.

Audit recipes monthly

Weigh portions at service

Watch beverage mix shift

Log spoilage and comps daily

Use the forecast before month-end. A small cost change across a high-volume item can move owner cash more than a few extra covers, so fix the biggest leak first.

3

Labor Model And Owner Role

Labor Mix Sets Owner Pay

Staffing decides what is left after service is covered. Payroll is $175k in Year 1, $2175k in Year 2, $256k in Year 3, and $260k in Years 4 and 5, plus a $60k owner salary each year. The model uses a lead chef, cook/prep staff, service staff, and part-time event support from Month 13.

Here’s the quick math: if labor rises faster than sales, owner distributions fall. A hired manager only makes sense if added sales or better execution pay for the extra fixed cost. Unpaid owner labor is not true profit, so the real test is cash left after payroll, not just kitchen output.

Track Labor Per Cover

Measure payroll against covers, sales, and service hours. Split labor by role so you can see the cost of the lead chef, prep staff, floor staff, and event support. One clear rule: if hours go up and covers do not, margin gets thinner fast.

Before adding a manager, test whether the role lifts sales, table turns, or guest flow enough to cover the extra wage. Keep owner time tied to the highest-value tasks, and forecast pay after labor, not before it. That protects the $60k draw and keeps distributions from getting squeezed.

4

Rent, Location, And Occupancy Cost

Rent and Occupancy Cost

Fixed location cost is the rent and site bill the restaurant pays before any owner draw. In the source model, that’s $750 monthly commissary rent plus other fixed costs of $2,150 per month, and breakeven is modeled in Month 3. That means location cost is manageable here, but it still has to be covered by covers and average check before the owner gets paid.

High rent only works when the site earns it back. A better spot needs enough foot traffic, parking, seating, patio use, and neighborhood demand to lift covers and check size. If the lease shifts from a light commissary setup to a full-service space, owner income can change fast because every extra dollar of rent comes out before profit and pay.

Match Rent to Demand

Track rent as a fixed monthly claim on cash, then test it against sales by daypart and by location. The key inputs are covers, average check, foot traffic, parking, seating, patio use, and neighborhood demand. If the site does not raise traffic or check size, keep the space small and the lease light.

Rent must fit monthly sales.

Covers must cover fixed cost.

Check size must support the lease.

Site demand must justify expansion.

Use the lease to protect cash flow, not just to look upscale. The operator’s job is simple: only take on more space when that space brings enough guests to pay for itself and still leave owner income after all fixed costs.

5

Channel Mix And Off-Premise Revenue

Off-Premise Revenue Mix

Off-premise sales can lift revenue, but owner pay only improves if each order leaves enough contribution margin after packaging, labor, and fees. In Year 1, the model assumes 30% of sales for packaging and 60% variable costs overall, including fuel, operating costs, and event or location fees. A busy week can still miss cash goals if commissions or fees are too high.

Track pickup, delivery, catering, and dine-in separately. The inputs are order count, average check, packaging per order, labor minutes, and fee rate. Month 13 adds part-time event support, so private events only help income if the extra labor is covered by margin. High-volume orders with low fees are best; high-fee orders can wipe out profit fast.

Measure Channel Contribution

Use a simple channel P&L for each order type. Here’s the quick math: contribution = revenue - food cost - packaging - delivery or event fees - extra labor. If a channel does not beat dine-in margin, raise the minimum, charge for delivery, or push pickup. What this estimate hides: refunds, remakes, and wasted prep time.

Track fee by channel.

Measure labor minutes per order.

Set minimums for delivery.

Price events to cover support.

Watch mix, not just sales. If delivery commissions are too high, steer guests to pickup. If catering or private events start in Month 13, price them to cover setup time and support hours, or they add work without adding take-home income.

6

Mediterranean Restaurant Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: Compare low, base, and high owner-income planning cases

Owner income scenarios

Owner income changes with weekly covers, ticket size, and how fast payroll scales. The same model can stay salary-led in Year 1, then add distributions as volume grows.

Salary and distribution paths by operating scale.

Scenario

Low CaseConservative ramp

Base CaseOperating scale

High CaseMature volume

Launch model

This is a conservative ramp built around Year 1 traffic.

This is the modeled core case at Year 3 scale.

This is the stronger case at Year 5 volume.

Typical setup

About 700 weekly covers, $12.50 midweek and $20.00 weekend tickets, $175k payroll, and $210k EBITDA before any owner distribution.

About 1,350 weekly covers, $13.75 midweek and $21.50 weekend tickets, $256k payroll, and $665k EBITDA before owner distributions.

About 2,010 weekly covers, $15.00 midweek and $23.00 weekend tickets, $260k payroll, and $1.253M EBITDA before owner distributions.

Cost drivers

weekly covers

ticket size

food ingredients

payroll

commissary rent

weekly covers

ticket size

payroll growth

food and packaging

event fees

weekly covers

higher ticket size

payroll control

food costs

vehicle overhead

Owner income rangeBefore owner reserves

$60k salarySalary-led

Salary plus distributionsDistribution upside

Salary plus larger distributionsMature upside

Best fit

Use this to stress-test the first operating year and thin-margin weeks.

Use this as the core planning case for staffing and cash flow.

Use this to test what a mature, high-volume route can support.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The researched case includes a $60,000 annual Owner/Manager salary plus possible distributions Year 1 sales are about $622,700, and EBITDA is modeled at $210,000 That profit pool is not automatic take-home because debt service, taxes, cash reserves, and reinvestment come first

The model shows breakeven in Month 3 and a 15-month payback period That assumes the stated cover counts, average checks, staffing, and costs hold If traffic ramps slower, food costs rise, or payroll runs ahead of sales, breakeven and payback can move later

Yes, reserves should come before owner distributions The model shows a minimum cash need of $793,000 in Month 2, which is separate from the $60,000 owner salary EBITDA may look healthy, but restaurants still need working cash for payroll, suppliers, repairs, taxes, and slow weeks

Covers, average check, food cost, labor, fixed costs, and channel mix drive take-home In Year 1, the model uses 700 weekly covers, a $1250 midweek check, a $2000 weekend check, 130% listed COGS, and $175,000 of payroll Small cost misses hit owner cash fast

The best format is the one with the strongest contribution margin after labor, packaging, fees, and fixed costs Catering and takeout can add volume, but packaging is modeled at 30% of sales in Year 1 and event-related variable costs matter Compare profit per order, not just sales

About the author

Oliver Pierce

Startup Cost Researcher

Oliver Pierce is a startup cost researcher at Financial Models Lab, where he writes practical guides for people planning their first business. He focuses on break-even planning and on comparing business ideas by cost and effort, with a clear, realistic approach to small business planning. His work is aimed at non-finance readers and is written to make business planning easier to understand and use.

Choosing a selection results in a full page refresh.