How do you check owner income in the financial model?

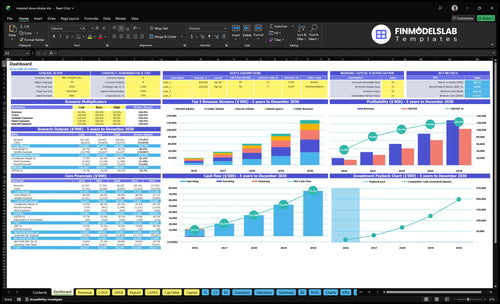

This dashboard shows five-year revenue, gross profit, contribution, owner pay capacity, and cash pressure; Year 1 revenue is $203M and contribution about $161M, while Year 5 revenue reaches $1.277B and contribution about $1.049B before fixed overhead and owner-specific items. Open the Metered Dose Inhaler Supplies Financial Model Template.

Owner-income model highlights

Five-year owner pay view

Revenue, margin, cost stack

Scenario testing for pricing

How much revenue does an inhaler supply business need to pay the owner?

For Metered Dose Inhaler Supplies, owner pay is driven by contribution margin after product costs, variable expenses, fixed overhead, and cash reserves. Using the model margin alone, $100,000 of pre-tax owner-pay capacity needs about $126,000 of Year 1 revenue at a 79.4% contribution margin; with Year 5 margin near 82.1%, it’s about $122,000. Real required revenue will be higher once payroll, rent, licensing, debt, and retained cash are added.

Core math

Revenue needed = pay + fixed costs + reserves

Divide by contribution margin

Year 1 margin is about 79.4%

Year 5 margin is about 82.1%

What changes the number

Payroll raises the revenue target

Owner-operated can cut paid labor

Staffed models can support more unit volume

Keep reserve cash in the plan

Is a metered dose inhaler supplies business profitable?

Yes—Metered Dose Inhaler Supplies can be profitable on paper if volume, margin, compliance, inventory, and receivables stay tight. One model shows $203M in Year 1 revenue and about $161M in contribution after direct costs and variable expenses, before fixed overhead and owner draws. The catch is simple: cash can still get trapped in inventory, expired stock, or slow-paying accounts; this is business planning, not medical advice.

Profit drivers

High volume supports margin.

Compliance keeps sales usable.

Reliable suppliers protect fill rates.

Fast collections protect cash.

Big risks

Inventory expiration can erase margin.

Receivables delays can squeeze cash.

Channel concentration can cut pricing power.

Owner overhead can break profit.

How much profit can a metered dose inhaler supplies business make?

Metered Dose Inhaler Supplies can produce about $161M in Year 1 contribution on $203M revenue from 300,000 units, before fixed overhead, taxes, debt service, and reinvestment; see How To Launch Metered Dose Inhaler Supplies Business? for the launch path. By Year 5, the planning case reaches $1.277B revenue from 1,675,000 units and about $1.049B contribution. Actual owner profit depends on sales volume, blended gross margin, compliance cost, insurance, storage, sales labor, reserves, and the owner’s role.

Profit Math

Year 1 revenue: $203M

Year 1 units: 300,000

Year 1 contribution: $161M

Contribution margin: about 79.3%

Profit Drivers

Year 5 revenue: $1.277B

Year 5 units: 1,675,000

Year 5 contribution: $1.049B

Main caveat: planning assumptions, not guaranteed income

Metered Dose Inhaler Supplies Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers that matter most?

1

Price Mix

86%-87%

Higher prices and a cleaner channel mix keep more of each sale after direct cost and rebates, so take-home rises fastest here.

2

Unit Volume

300K-1.675M

Volume climbs from 300K units in Year 1 to 1.675M in Year 5, which spreads fixed overhead and lifts EBITDA.

3

Product Mix

$180-$200

The combo inhaler sells at $180 to $200, so a richer mix raises revenue per unit without adding the same fixed cost.

4

Supplier Cost

$3.2-$8.4

Unit COGS runs about $3.20 to $8.40, so better sourcing and terms protect margin on every device.

5

Compliance Load

7.0%-5.0%

Revenue-based costs step down from 7.0% to 5.0%, so lower commissions, shipping, and rebate drag leave more EBITDA.

6

Cash Turns

$1.235M

The plan needs about $1.235M at the low point in Month 1, and slow turns can trap cash even when sales grow.

Metered Dose Inhaler Supplies Core Six Income Drivers

Channel Mix And Pricing Power

Channel mix

Clinic contracts can bring repeat volume, but they often trade price for predictability. Smaller direct accounts may pay more, yet orders can be uneven. That mix drives gross margin and cash flow, not just top-line revenue. If sales commissions start at 40% in Year 1 and fall to 25% by Year 5, early channel choices matter a lot.

Price points

Year 1 researched prices are $45 for a rescue inhaler, $120 for a steroid inhaler, $35 for a valved spacer, $40 for a pediatric spacer, and $180 for a combo. That spread matters because product mix can lift average selling price without adding much extra overhead. Higher-price items help margin only if discounts stay controlled.

Rescue: $45

Steroid: $120

Valved spacer: $35

Pediatric spacer: $40

Combo: $180

Discount pressure

A 10% price concession on $203M Year 1 revenue cuts revenue by $20.3M before overhead. Add a 10% group purchasing organization rebate, slow receivables, and contract-heavy sales, and cash gets tight fast. The real question is not just “what did we sell,” but “how much cash did we keep and when did it arrive?”

Price cuts hit cash, not just revenue.

Rebates reduce net sales.

Slow collections trap working capital.

Margin to owner pay

Stronger pricing power raises gross margin and owner pay capacity because less revenue leaks to discounts, rebates, and commissions. Here’s the quick math: if pricing holds and cash collection stays clean, more of each sale can fund inventory, overhead, and distributions. If onboarding drags, receivables and reserves will eat that gain.

Unit Volume And Repeat Orders

Volume math

Here’s the quick math: total units rise from 300,000 in Year 1 to 1,675,000 in Year 5, and revenue rises from $203M to $1,277M. That only helps owner pay if margin stays intact, fulfillment holds, and receivables stay current. More units can also mean more cash tied up.

Product mix

Volume is spread across rescue inhalers (100,000 to 550,000), steroid inhalers (50,000 to 275,000), valved spacers (80,000 to 450,000), pediatric spacers (40,000 to 220,000), and combo inhalers (30,000 to 180,000). That mix matters because each unit family changes storage, picking accuracy, and quality checks.

Repeat orders

Repeat orders help forecast buys, lower stockouts, and improve inventory turns, which protects distributable cash. One clean rule: if orders repeat, buying becomes planned instead of reactive. Still, higher volume without collection discipline can create cash strain even when sales look strong.

Cash control

The real ceiling is working capital, not demand. More units require more purchasing, storage, fulfillment labor, and tighter controls on expiries and receivables. If collections slip, the business can grow revenue and still trap cash in inventory. That is where owner pay gets squeezed.

Inhaler And Spacer Product Mix

Revenue mix

Year 1 revenue is $203M: $45M rescue inhalers, $60M steroid inhalers, $28M valved spacers, $16M pediatric spacers, and $54M combo inhalers. That’s about 78% inhalers and 22% spacers. One clean line: the mix sets gross profit, not just sales.

COGS load

Direct unit COGS run from $320 to $840: rescue inhalers $380, steroid inhalers $620, valved spacers $320, pediatric spacers $340, and combo inhalers $840. Higher-COGS items need tighter pricing and less waste. One bad discount can wipe out the margin gain.

Margin lift

Spacer add-ons can raise order value without changing the clinical decision. If an account already buys inhalers, adding spacer devices can lift blended revenue and spread fulfillment cost over more dollars sold. The upside shows up only if inventory turns stay healthy and contract discounts don’t outrun margin. One more unit should add profit, not just volume.

Stock risk

The main risk is stocking low-turn SKUs too early. Pediatric spacers and other slow movers tie up cash, can expire or go stale, and force bigger inventory reserves. Track units on hand, months of cover, and discount depth before you buy more. Owner take-home improves when cash is not sitting on the shelf.

Supplier Cost And Purchasing Terms

Supplier Floor

Supplier pricing sets the floor for gross profit and cash pressure. In this model, direct product costs run about $13M in Year 1 and $75M in Year 5 before the 70% revenue-based COGS layer. Unit buys of $380 rescue, $620 steroid, $320 valved spacer, $340 pediatric spacer, and $840 combo items drive owner take-home.

Cost Build

Estimate spend as units × unit price × months covered, then add freight and safety stock. Use supplier quotes for each item, plus minimum order quantities and payment timing. What this hides: if allocation is unreliable, you may need more cash than the purchase price suggests.

Terms Control

Better payment terms shrink the gap between inventory purchase and customer collection, so cash lasts longer. Avoid unauthorized sourcing and excessive minimum buys. A supplier price increase hits every unit sold, and it can cancel out the benefit of higher volume if pricing does not move with it.

Cash Discipline

Payment timing, allocation reliability, and minimum order quantities affect how much cash stays available for owner take-home. Strong procurement terms protect margin and reduce working capital strain, while weak terms lock cash into stock before customers pay. That cash gap is the real pressure point, not just unit cost.

Compliance And Fulfillment Cost Discipline

Margin Can Still Hide Weak Pay

Gross margin can look fine, but owner income gets squeezed by compliance and fulfillment. Here, the revenue-based burden before unit COGS is 140% in Year 1 and 120% in Year 5, so planning has to include testing, sterilization, rebates, freight, and reserves. If those costs drift, cash for owner pay drops fast.

Compliance Cost Stack

Budget compliance as a percentage of revenue, not a vague overhead bucket. Use 15% for quality control testing, 20% for sterilization services, 10% for regulatory fees, 5% for inventory insurance, and 20% for waste and scrap. Estimate each line with revenue × rate, vendor quotes, and months of coverage.

Test cost per lot

Sterilization quote per run

Insurance months covered

Fulfillment Cost Stack

Sales commissions start at 40% of revenue, shipping and logistics at 20%, and GPO rebates stay at 10%. Here’s the quick math: every order needs commission rate, freight per shipment, and rebate terms tied to units sold. Underpriced shipping and weak pick accuracy usually hit owner pay before anyone notices.

Order count times freight

Commission rate on booked sales

Rebate timing by contract

Keep Overhead Tight

Storage, software, sales labor, payroll, documentation, and fulfillment checks are required costs, not fluff. Fixed overhead should stay in line with gross profit, or the business ends up overhiring and spending into margin. The cleanest savings come from tighter pick accuracy, better shipping quotes, and strong compliance controls, which leave more cash for owner pay.

Inventory Turns And Working Capital Reserves

Cash Comes First

In inhaler supply, accounting profit can overstate take-home because inventory is bought weeks before payment arrives. With slow turns, delayed receivables, and upfront purchasing, a big contract can still drain cash. Faster turns and tighter reserves make more of revenue distributable.

Reserve Math

Reserve math covers slow-moving stock, expiring units, and inventory insurance. The model uses a 20% waste and scrap allowance and a 0.5% insurance effect. On $203M Year 1 revenue, waste and scrap is about $406,000; on $1,277M in Year 5, it rises to about $26M.

Cash Traps

The cash traps are slow-moving stock, late customer payments, and product mix mistakes. A contract can look profitable and still need cash to buy inhalers weeks before payment arrives. If receivables slip, owner take-home drops even when revenue is up.

Set reorder points from demand.

Track days sales outstanding.

Trim safety stock monthly.

Turns Pay Owners

Faster inventory turns free cash for distributions. Keep safety stock tied to real demand, and model reserves as cash locked away, not optional overhead. That way accounting profit and owner take-home stay closer together.

Metered Dose Inhaler Supplies Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income swings with product mix, pricing, and how much cash stays in reserve. Early ramp is cash-sensitive; Year 5 scale improves draw capacity but raises receivables pressure.

A quick view of lean, base, and high owner draw capacity.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is a lean owner-income path built on early ramp, lower pricing power, and tight cash use.

This is the modeled owner-income path using Year 1 volume and pricing from the plan.

This is the stronger owner-income path near Year 5 scale and pricing.

Typical setup

Volume runs below Year 1, commissions and shipping stay high, reserves stay heavy, and the owner stays hands-on to keep production moving.

It assumes 300,000 units, $20.3M revenue, direct unit COGS, and enough EBITDA to cover fixed overhead and a modest owner draw.

It assumes 1,675,000 units, $127.7M revenue, stronger mix, and better scale, but more cash tied up in inventory and receivables.

Cost drivers

Lower volume

weaker pricing

higher commissions

higher shipping

heavier reserves

Year 1 volume mix

modeled pricing

direct unit COGS

commissions and shipping

fixed overhead

Year 5 volume mix

stronger pricing

lower commissions

lower shipping

receivables and inventory

Owner income rangeBefore owner reserves

Limited owner drawLow Case

Modeled owner drawBase Case

Strong owner drawHigh Case

Best fit

Use this to stress-test an owner-operated launch with slow collections and little cash cushion.

Use this as the main planning case for pricing, staffing, and cash management.

Use this to test what happens when procurement, fill rates, and collections all scale cleanly.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The researched model shows about $161M of Year 1 contribution before fixed overhead, taxes, debt service, and retained cash That comes from $203M revenue, 300,000 units, and about 794% contribution margin after listed unit COGS, revenue-based COGS, commissions, logistics, and rebates Actual owner take-home depends on payroll, rent, reserves, and cash collection

Owner pay becomes realistic when gross profit covers fixed overhead and inventory funding In the Year 1 model, monthly revenue averages about $169M, but that does not mean the owner can distribute cash right away If receivables are slow or inventory buys run ahead of sales, cash may stay in the business despite strong modeled margins

Yes, this business likely needs meaningful working capital because inventory is bought before customer cash is collected The model includes waste and scrap at 20% of revenue and inventory insurance at 05% On Year 1 revenue of $203M, those two items equal about $507,500 before any extra reserve for receivables delays or safety stock

Pricing, supplier cost, contract discounts, product mix, freight, and expired inventory affect margin most The model uses Year 1 prices from $35 for a valved spacer to $180 for a combo inhaler, with direct unit COGS from $320 to $840 A 10% pricing change on Year 1 revenue equals about $203,000

Start with unit economics, then subtract fixed overhead, reserves, debt service, and taxes before setting owner distributions Use the researched Year 1 contribution of about $161M and Year 5 contribution of about $1049M as capacity markers, not salaries The best forecast tests lower pricing, higher shipping, slower collections, and extra inventory waste

About the author

Robert Spencer

Startup Planning Writer

Robert Spencer is a startup planning writer at Financial Models Lab who focuses on simple financial projections that make business ideas easier to evaluate. He helps readers compare opportunities by breaking down the cost and income assumptions behind everyday business ideas. With a clear, grounded style, he explains how small businesses operate day to day and gives beginners a practical way to understand the numbers before they commit.

Choosing a selection results in a full page refresh.