How Much A Mobile Hot Dog Stand Owner Can Make: $72K Model Pay

Mobile Hot Dog Stand Bundle

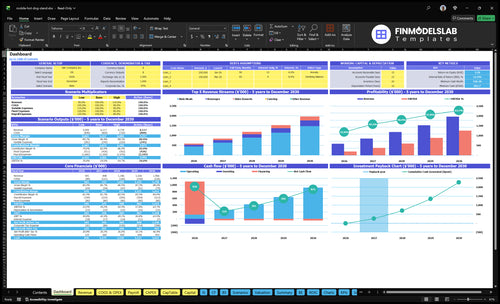

A mobile hot dog stand owner can plan around a modeled $72,000 annual owner role, plus possible distributions if cash is left after reserves and reinvestment In the researched Year 1 case, revenue is about $638,000, based on 80 to 150 daily transactions and $15 to $18 average tickets EBITDA is about $195,000 in Year 1 and grows to about $1253 million by Year 5 in the model These are planning estimates, not guaranteed owner pay

Owner income$72kNet margin37%Revenue for target pay$196kBusiness difficultyHard

Want to test your own hot dog cart income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will change with demand, margin, payroll, financing, and reserve policy.

How do you check owner income in the Mobile Hot Dog Stand model?

Can a mobile hot dog stand owner make more with events or multiple carts?

Yes—events and multiple carts can lift revenue for Mobile Hot Dog Stand, but they also add labor, prep, permits, and more management load. The model already shows weekend strength: Year 1 Saturday is 150 transactions and Sunday is 140, versus 80 on Monday, so the first win is denser weekend and event sales, not just more units.

Events add volume

0% catering in Year 1

1% in Year 2

3% in Year 3

5% in Year 4

More carts add overhead

Payroll rises from $172k to $241k

That happens by Year 3

Fees and cancellations cut profit

Weather and access can block sales

What is the profit margin on a mobile hot dog stand?

Can you make a living with a mobile hot dog stand?

Yes, a Mobile Hot Dog Stand can support a living in this model: owner labor is set at $72,000/year, while Year 1 revenue is about $638,000 with $195,000 EBITDA after modeled payroll; see What Is The Biggest Challenge Facing Your Mobile Hot Dog Stand's Growth?. EBITDA means profit before interest, taxes, depreciation, and amortization, so it’s not the same as cash you can spend.

Income Model

$72,000/year owner labor pay

$638,000 Year 1 revenue

$195,000 modeled EBITDA

760 weekly transactions assumed

Cash Reality

7 selling days drive the model

Part-time vending likely earns less

Events can lift weekend volume

Weather, debt, reserves delay cash

Mobile Hot Dog Stand Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six hot dog stand income drivers?

1

Foot Traffic

80-400/day

More people near the stand means more transactions, and that lifts take-home before costs.

2

Sell Time

7 days

More open days and better weather coverage raise weekly covers, but missed hours cut cash fast.

3

Ticket Mix

$15-$22

A higher ticket from weekend sales and add-ons grows revenue without matching labor.

4

Food Cost

12%-15%

Each point out of COGS (cost of goods sold) drops straight to gross profit.

5

Overhead

$21K/mo

Recurring rent, utilities, and payroll set the break-even floor, so fixed cost control matters.

6

Catering Mix

0%-5%

Catering adds bigger orders and helps smooth slower days when street sales dip.

Mobile Hot Dog Stand Core Six Income Drivers

Location Quality And Foot Traffic

Foot Traffic and Legal Access

Transactions are the biggest income lever here because the whole model runs on walk-up sales. In Year 1, volume ranges from 80 Monday transactions to 150 Saturday transactions; by Year 5, it rises to 200 Monday and 400 Saturday. That gap changes revenue, labor spread, and owner pay fast. One strong corner can beat a better menu on a weak one.

Legality matters as much as demand. Strong sites include permitted office lunch spots, parks, campuses, construction zones, nightlife areas, and event zones. Restricted vending spots can erase the volume gain, so the right location must be both busy and allowed. Here’s the quick math: Saturday is about 88% above Monday in Year 1 (150 vs. 80), so site quality directly shapes cash flow.

Track Orders per Hour

Measure orders per hour, not just foot traffic, because throughput drives labor use and waste. Track sales by site, daypart, and weather so you know which stops pay for staff and which ones only look busy. If a location can’t keep the line moving and stay legal, the revenue math breaks fast.

Orders per hour by location

Permitted vs. restricted sites

Waste per sale after each shift

Labor hours per transaction

The best sites lift volume and keep spoilage low, so more of each sale can flow to gross profit and owner draw. What this estimate hides is simple: a busy but blocked site is still a bad site.

1

Selling Schedule And Utilization

Selling Schedule And Utilization

Income here depends on how many open days actually turn into sales. The Year 1 model assumes 7 selling days and 760 weekly transactions, or about 109 transactions per day. Friday through Sunday carry 410 transactions, which is about 54% of weekly volume, so weekends do most of the work.

Here’s the quick math: with $71k monthly fixed overhead, fewer selling days only work if event traffic or ticket size is high enough to replace the lost weekday volume. Lunch rushes, late-night shifts, weather, and event calendars change daily results, so treating every day as equally profitable can overstate cash flow and owner pay.

Track Open Days, Not Just Hours

Measure sales by day, daypart, and location. Log transactions, weather, and event dates, then compare each open day against labor and prep cost. If a day misses its target, cut it, move it, or book it around a stronger crowd instead of assuming the cart should run every day.

Shorter schedules can work only when event volume or average ticket replaces the lost weekday sales. The goal is not more open time; it’s more profitable open time that helps cover fixed overhead and leaves room for the owner’s draw.

2

Average Ticket And Menu Mix

Average Ticket And Menu Mix

Average ticket, or average order value (AOV), is the average cash collected per sale. Here, Year 1 assumes $15 midweek and $18 weekend tickets, with sales mix at 75% main meals, 15% beverages, 10% sides and desserts, and 0% catering. That mix matters because drinks and add-ons usually lift revenue faster than adding another cart.

Higher tickets can raise owner take-home income without more foot traffic, but only if the upsell does not slow service. The Year 5 target of $18 midweek and $22 weekend means more revenue per customer, which helps cover fixed costs and leaves more profit after labor and food. If menu complexity hurts line speed, the extra dollars can disappear fast.

Raise Ticket Without Slowing The Line

Track attach rate on drinks, chips, premium toppings, sausages, and add-ons. Test combos first, since one bundled choice is faster than many small decisions. Keep the menu mix tight so the team can sell more without slowing the handoff. One clean rule: if the line gets longer, the upsell is too complex.

Measure AOV by daypart.

Track add-on sales per order.

Time orders from order to handoff.

Compare ticket lift to service speed.

Use the Year 1 split as your base: 75% meals, 15% beverages, 10% sides and desserts. If a new combo raises ticket but adds seconds to each sale, it can cut throughput and owner cash. Midweek pricing at $15 and weekend pricing at $18 gives you a simple forecast starting point.

3

Food Cost, Waste, And Gross Margin

Food Cost And Waste

This driver is the gap between menu price and the real cost of each sale. With 15% Year 1 COGS, made up of 10% specialized ingredients and 5% fresh produce/proteins, plus 4% payment and promotion variable costs, only 81% of sales is left before rent, permits, staff, and owner pay.

Waste cuts cash fast in a mobile hot dog stand because unsold buns, proteins, drinks, and toppings do not turn into later sales. If COGS improves to 12% by Year 5 and other variable costs stay flat, contribution rises to 84% of sales, so the same traffic can throw off more take-home profit.

Tighten Portions And Shrink

Track vendor price, portion size, spoilage, and sell-through by daypart. Gross profit starts with buying well and portioning tightly, so prep should follow actual lunch, weekend, and event volume instead of hope.

Weigh portions every shift.

Count unsold buns daily.

Log spoiled proteins separately.

Review payment and promo fees.

Match prep to traffic by hour.

Set a weekly food-cost target at 15% in Year 1 and test waste by item, not just by total. If drinks or toppings keep getting tossed, cut batch size or shorten prep windows before those losses hit owner draw.

4

Permits, Commissary, Insurance, Fuel, And Overhead

Fixed Overhead And Compliance

This driver includes stall rent, utilities, insurance, POS, cleaning, maintenance, pest control, permits, commissary access, fuel, storage, and repairs. The model’s recurring fixed expenses total $71k per month, so the business must clear that floor before owner pay starts. Even with strong gross margin, these costs can wipe out take-home if sales dip or the schedule shrinks.

Local permit and commissary rules vary by city and county, so the same cart can have very different cash needs in each market. Here’s the quick math: $5k stall rent, $1k utilities, $250 insurance, $150 POS, $400 cleaning, $200 maintenance, and $100 pest control already lock in monthly burn before fuel or repairs show up.

Track The Floor, Not Just Sales

Build the forecast from recurring cash needs first, then test whether daily sales cover them. Track permit fees, commissary charges, fuel, storage, and repair spend as separate lines, not one “other” bucket. If you miss any of these, owner pay will look better on paper than it is in cash.

Use a monthly control sheet with fixed costs, cash paid, and contribution left. The key question is simple: after the $71k floor, is there enough left to pay the owner? If repairs or fuel run hot for two straight months, cut routes, raise prices, or trim low-yield service days fast.

5

Events, Catering, And Private Bookings

Events, Catering, And Private Bookings

Events can lift both volume and ticket size, but they are not free money. For this cart, catering starts at 0% of Year 1 sales, then rises to 5% by Year 4 before easing to 4% in Year 5. The real win is a higher revenue per service window, if the booking minimum covers labor, travel, and setup time.

Watch the trade-off. Private parties, festivals, fairs, and corporate lunches can fill slow weekdays, but event fees, extra staffing, prep time, rain, cancellations, and permit limits can cut into margin fast. If minimum spend does not cover direct costs, the owner may see more sales but less cash to pay themselves.

Track booking profit, not just booking count

Measure each event by booking fee, minimum spend, labor hours, travel cost, and net cash after prep. A simple check: if the booking cannot cover the extra staff time and miles, it is a weak deal even if the top line looks good. That matters more in a mobile model with narrow service windows.

Test event pricing by day and format. Keep a record of weekday lunch jobs, private parties, festivals, and cancellations, then compare them to normal street sales. The goal is higher income per shift, not just more work. If rainy weekends or permit limits raise no-show risk, require deposits and clear minimums before the team rolls out.

6

Mobile Hot Dog Stand Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high mobile hot dog stand income scenarios

Owner income scenarios

Owner income shifts with traffic, weekend mix, AOV, and staffing. The model moves from a lean Year 1 case to a heavier Year 3 and Year 5 path, so cash need and pay change fast.

Compare low, base, and high owner income cases for planning.

Scenario

Low CaseTraffic risk

Base CasePayroll load

High CaseUpside case

Launch model

Owner income is modeled on the lean Year 1 setup.

Owner income follows the modeled Year 3 operating case.

Owner income stretches in the Year 5 upside case.

Typical setup

Traffic starts at 80 weekday transactions and 150 on weekends, with $15 midweek AOV and $18 weekend AOV, about $638k revenue, 85% gross margin before variable fees, and $195k EBITDA.

Traffic rises to 130 weekday transactions and 270 weekend transactions, AOV moves to $16 to $20, revenue is about $1.175m, EBITDA is $598k, and payroll reaches $241k.

Traffic reaches 200 weekday transactions and 400 weekend transactions, AOV is $18 to $22, revenue is about $1.961m, EBITDA is $1.253m, and the owner role stays at $72k before distributions.

Cost drivers

weekday traffic

weekend traffic

AOV

food cost

fixed payroll

higher traffic

higher AOV

catering mix

$241k payroll

fixed overhead

peak traffic

premium AOV

catering mix

heavier staffing

cash need

Owner income rangeBefore owner reserves

$72k modeled payLow case

$72k plus profit shareBase case

$72k plus distributionsHigh case

Best fit

Best if you want to test thin traffic and tight staffing.

Best for planning the model's middle path and staffing ramp.

Best for operators with strong sites and enough cash to staff for peak demand.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

In this model, the owner role is $72,000 per year before taxes The business also shows about $195,000 in Year 1 EBITDA on roughly $638,000 of revenue Extra owner distributions depend on reserves, debt, reinvestment, and cash timing, so do not treat EBITDA as automatic take-home pay

The model reaches breakeven in Month 3 and payback in 14 months That assumes the stand hits the planned sales ramp, including 80 to 150 daily transactions in Year 1 and $15 to $18 average tickets Slower permitting, weak locations, weather, or higher labor needs can push breakeven later

Yes, a mobile hot dog stand usually needs local approvals, but exact rules and fees vary by city and county This model includes recurring overhead such as $250 monthly insurance and $5,000 monthly stall rent, but it does not give local permit advice Confirm health, vending, commissary, and location rules before spending startup cash

Foot traffic, selling days, average ticket, and labor drive profit the most In Year 1, weekly transactions total 760, with weekend days carrying much of the volume Food-level COGS is 15%, while fixed costs run $7,100 per month Small changes in daily sales can move owner cash fast

The best schedule is the one with high demand and enough repeat selling days In the model, Friday through Sunday produce about 410 of 760 weekly Year 1 transactions Weekday lunch routes help consistency, while events can add spikes The owner should compare revenue per hour, staff cost, prep time, and weather risk

About the author

Kevin West

Startup Cost Researcher

Kevin West is a startup cost researcher at Financial Models Lab who writes practical guides for people planning their first business. He focuses on break-even planning and on comparing business ideas by cost and effort, with an emphasis on realistic small business planning for founders with limited capital. His work connects business ideas to realistic startup budgets.

Choosing a selection results in a full page refresh.