How Much Can a Nutrigenomics Testing Owner Make by Year 5?

Key Takeaways

Volume helps only if lab and support stay controlled

Higher-touch mixes raise revenue but also labor and fulfillment

CAC must fall as marketing scales from $450k to $25m

Cash reserves matter before owner draws at month twelve

Owner income$15.4kNet margin-24% to 79%Revenue for target pay$1.48MBusiness difficultyHard

Want to test your owner income case?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the full forecast?

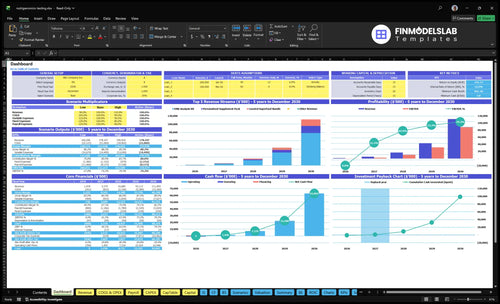

The Nutrigenomics Testing Service Financial Model Template shows dashboard outputs for revenue assumptions, sales mix, repeat customers, lab and kit costs, payroll, overhead, capex, cash, EBITDA, and owner income. Revenue runs from $1.476M to $111.459M; EBITDA moves from -$360K to $88.312M; CAC drops from $85 to $55; marketing rises from $450K to $25M; breakeven lands in Month 13, payback in Month 21, and minimum cash is $4K in Month 12.

Owner-income model highlights

Owner income output included

Revenue and EBITDA ramp

Scenarios stay editable

How many nutrigenomics tests must you sell for owner income?

You can’t use one universal test target for Nutrigenomics Testing Service; owner income depends on AOV, CAC, lab cost, payroll, and reserves. In Year 1, weighted product revenue is about $187 per order, based on 120 units and mix pricing of $199, $75, and $120. With $450,000 in marketing and $85 CAC, that’s about 5,294 new customers before repeat orders.

Year 1 order math

$187 weighted revenue per order

120 units drive the mix

Prices: $199, $75, $120

5,294 new customers at $85 CAC

Owner income drivers

CAC falls to $55 by Year 5

Variable costs drop from 200% to 156%

Repeat orders improve contribution

Solve owner pay after overhead and reserves

How does a nutrigenomics testing business scale owner income?

The Nutrigenomics Testing Service scales owner income when it grows order density, cuts customer acquisition cost (CAC), and drives repeat purchases, not just one-off test sales. Here’s the quick math: the provided model shows revenue rising from $1,476 million to $111,459 million as repeat customers move from 150% to 400%, repeat lifetime stretches from 12 to 36 months, and average repeat orders rise from 050 to 100 monthly. Owner-led delivery still caps capacity, so scale needs dietitian staffing, software, compliance controls, customer support, and quality review.

Income drivers

Higher order density lifts revenue fast.

Lower CAC protects margin.

Repeat purchases extend lifetime value.

More tests alone do not scale.

Scale limits

Owner-led delivery caps throughput.

Dietitian staffing supports managed delivery.

Compliance and privacy must stay tight.

Marketing economics decide owner income.

Can a nutrigenomics testing business pay the owner in the first year?

Yes, Nutrigenomics Testing Service can model owner pay in Year 1, but only as payroll: profit distributions aren’t supported because EBITDA is -$360,000. Start with the KPI math here, What Are The 5 Core KPIs For Nutrigenomics Testing Service Business?, then treat the $185,000 CEO salary as an operating cost, not an owner draw.

Owner Pay

Model CEO payroll: $185,000 annually

Skip profit distributions in Year 1

EBITDA runs negative: -$360,000

Breakeven lands around Month 13

Cash Risks

Revenue plan: $1.476 million

Marketing spend: $450,000

CAC target: $85

Fixed overhead: $19,200 monthly

Nutrigenomics Testing Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main income drivers?

1

Test Volume

75x

Revenue scales from $1.476M in Year 1 to $111.459M in Year 5, so test volume is the biggest swing in owner take-home.

2

Basket Size

1.2→2.1

More items per order lift revenue per client as the mix shifts toward supplements and bundles, even as the DNA kit price steps down from $199 to $169.

3

Unit Cost

20.0%→15.6%

Lab processing, logistics, payment fees, and affiliate commissions fall from about 20.0% of revenue in Year 1 to 15.6% in Year 5, so each point saved drops straight to EBITDA.

4

Dietitian Capacity

1.0→6.0 FTE

Registered dietitian staffing rises from 1.0 FTE to 6.0 FTE, so workflow speed decides whether growth stays efficient or turns into a labor bottleneck.

5

CAC

$85→$55

CAC falls from $85 to $55 while the annual marketing budget climbs from $450K to $2.5M, so paid growth only helps if conversion and repeat buys keep up.

6

Fixed Overhead

$19.2K/mo

Fixed overhead is $19,200 a month across cloud, HIPAA monitoring, office, insurance, software, and support, and that base helps explain the Month 13 breakeven.

Nutrigenomics Testing Service Core Six Income Drivers

Monthly nutrigenomics tests sold

Monthly Test Volume

More monthly tests spread fixed overhead and payroll across more customers, so owner income rises faster than revenue only when each added order stays profitable. In Year 1, revenue is $1.476 million, or about $123,000 monthly. With $450,000 of marketing at $85 CAC, the plan needs about 5,294 new customers before repeats.

That volume only helps if lab turnaround, dietitian review, and support stay tight. More tests can add cash, but delays, sample failures, or high service load can eat the margin and slow owner pay. One clean rule: grow orders only if the team can keep the same service standard at higher volume.

Track Volume by Channel

Measure tests sold, CAC by channel, turnaround time, and support tickets per 100 tests each month. Paid ads, search, practitioner referrals, gyms, wellness clinics, and affiliates can all fill the funnel, but each channel has to beat the $85 CAC target and stay within service capacity.

Forecast repeats separately from new sales. If one extra test creates more review time or more rework, owner income falls even when topline rises. The best test volume is the kind that pays for acquisition, covers service labor, and still leaves room for profit draw.

1

Average revenue per DNA nutrition client

Average revenue per DNA nutrition client

This driver is the dollars you collect from one client across kits, supplement packs, and bundles. In Year 1, the plan shows weighted order revenue of about $187, with 120 units per order. By Year 5, the mix shifts toward more supplement packs and bundles, and units per order rise to 210, so revenue per client can improve if the mix change holds.

Higher-touch packages can lift revenue, but they also add fulfillment, support, and practitioner labor. If extra order value brings more than extra service cost, owner pay gets squeezed even while sales grow. The clean test is simple: revenue per client has to rise faster than the cost to serve that client.

Track mix, not just orders

Measure average revenue per client by product type, not just in total. The key inputs are kit share, supplement share, bundle share, unit price, units per order, refund rate, and the labor minutes tied to each package. Here’s the quick math: average revenue = product mix × price, then subtract fulfillment and support cost to see what reaches profit.

Track revenue by product mix

Track labor minutes per order

Track refund and rework rates

Test whether bundle-heavy orders actually raise take-home income. If a higher-touch package lifts revenue but adds practitioner time or shipping cost, the margin can shrink. Watch gross margin per client, support tickets per order, and minutes of practitioner time before you change pricing or push more upgrades.

2

Lab and fulfillment cost per test

Lab and fulfillment cost per test

This cost line includes lab partner fees, kit materials, inventory sourcing, logistics, shipping, retesting, sample failures, and report generation. With no owned lab, lab partner pricing drives gross margin. In Year 1, lab processing and kit materials are 120% of revenue, and sourcing/logistics are 50%; that means the first orders can be cash-negative before overhead and owner pay.

By Year 5, those costs fall to 80% and 30%, so more of each sale stays in the business. The owner’s take-home income rises only if turnaround stays tight and quality stays high; cheap volume that triggers more retests or failed samples can wipe out the margin gain.

Control landed cost, not just sticker price

Track landed cost per completed report: lab fee, kit, freight, replacements, and report labor. Also track the share of orders that need retesting or fail on sample quality. One bad batch can make a volume tier look cheaper on paper but more expensive in cash.

Negotiate price breaks only when quality, turnaround, and data handling stay reliable. The key inputs are tests sold, average revenue per client, and cost per test; if cost stays above revenue in early years, the owner needs faster pricing improvement or lower failure rates before taking distributions.

3

Practitioner delivery efficiency

Practitioner delivery efficiency

Practitioner time is the choke point here. It includes dietitian review, geneticist oversight, and client support. If each client needs long one-on-one interpretation, revenue can rise while owner pay stalls, because labor grows with volume. The plan already shows registered dietitian staffing rising from 10 FTE at $85,000 to 60 FTE by Year 5, and lead geneticists from 10 FTE at $160,000 to 20 FTE.

Software-driven report delivery scales better than manual consults, so the key test is whether labor stays faster than revenue. Here’s the quick math: consult minutes per client, report revision rate, and support tickets tell you if each new sale adds margin or just adds payroll. If consults stay heavy, gross margin tightens and the owner’s income lags sales growth.

Cut manual review time

Track the unit economics per client, not just headcount. Measure consult minutes per client, report revision rate, and support tickets each month, then compare them with revenue per order and staff cost. If those three metrics rise, the service is getting harder to scale and the owner’s draw gets squeezed.

Push simple cases to software and reserve experts for exceptions. That keeps the 10 to 60 FTE labor ramp from swallowing cash flow. A good target is fewer revisions, shorter calls, and faster first-pass report delivery, so added clients lift profit instead of just filling calendars.

Track minutes per client.

Flag high-revision reports.

Route repeats to self-serve.

4

Customer acquisition cost and conversion

CAC and conversion

Your profit here depends on how much it costs to win a buyer and how many leads actually convert. In the plan, CAC falls from $85 in Year 1 to $55 in Year 5, while annual marketing rises from $450,000 to $25 million. At Year 1 spend, that’s about 5,294 new customers before repeats. If conversion slips, owner income falls even when revenue spend rises.

Paid ads can scale fast, but they can squeeze margin if they bring low-intent traffic. Search, practitioner referrals, gyms, wellness clinics, and affiliate partners can lower blended CAC, which is the average cost to acquire one paying customer across channels. Not every lead is profitable, so CAC payback, conversion rate, repeat customer rate, and refund rate matter as much as top-line growth.

Track channel payback first

Measure CAC by channel, not just in total. If paid ads cost more than search or referral traffic, the blended number can hide weak spend. Use simple math: CAC = marketing spend / new customers. Then compare that to gross profit per order and time to pay back the spend. If payback stretches, cash flow tightens and owner draws get harder to support.

Watch the four controls that change take-home income: conversion rate from lead to buyer, repeat purchase rate, refund rate, and the share of customers from low-CAC partners. If conversion is soft, spend less and fix the funnel before scaling. If repeat orders rise, you can support higher CAC because each customer earns more over time.

Split CAC by channel.

Track lead-to-buyer conversion.

Check CAC payback monthly.

Monitor repeat and refund rates.

5

Fixed overhead, compliance, and reserves

Fixed Overhead and Reserve Cash

This driver is the monthly fixed load before owner pay: $19,200 for cloud hosting, HIPAA monitoring, office lease, insurance, software, and customer support. That is $230,400 a year before payroll. Add $745,000 of Year 1 payroll and $390,000 of capital spending (capex), and the business has a heavy cash burden before any owner draw.

The reserve rule is the key limiter. With minimum cash at $4,000 in Month 12, distributions come last, not first. If overhead or compliance costs rise without a matching lift in revenue, take-home pay gets delayed because cash has to stay inside the business to keep operations and reporting on track.

Guard the Cash Floor First

Build the forecast from these inputs: fixed overhead lines, payroll, capex timing, and the $4,000 cash floor. Here’s the quick rule: if the 12-month model can’t stay above that floor, owner draws are too early. One clean line: reserve cash before reward cash.

Track monthly burn against plan.

Review compliance spend every month.

Pause draws before cash gets thin.

6

Nutrigenomics Testing Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high owner income scenarios

Owner income scenarios

Owner pay is thin at launch because Year 1 revenue is $1.476 million with -$360,000 EBITDA, then improves as CAC falls and repeat orders build. The spread between cases comes from marketing efficiency, repeat customers, and mix shift.

Low, base, and high owner-income cases tied to launch, breakeven, and scale.

Scenario

Low CaseLaunch risk

Base CaseBreakeven near

High CaseScale upside

Launch model

Owner pay stays tight and mostly salary-only while the business absorbs launch losses.

Owner pay starts to open up once the model clears breakeven and cash reserves are in place.

Owner pay can become meaningfully larger if repeat revenue and order frequency keep scaling.

Typical setup

Year 1 looks like $1.476 million revenue, -$360,000 EBITDA, $85 CAC, and $450,000 marketing with heavy lab, logistics, and payroll pressure.

Year 2 reaches $5.375 million revenue and $2.213 million EBITDA with $75 CAC, lower variable costs, and room for distributions after reserves.

Year 5 reaches $111.459 million revenue and $88.312 million EBITDA with $55 CAC, 40% repeat customers, and a stronger mix of recurring supplement and superfood sales.

Cost drivers

High CAC

$450k marketing

lab processing costs

fixed payroll

Lower CAC

more repeat orders

lower variable costs

reserve build

Low CAC

40% repeat customers

higher order frequency

richer product mix

Owner income rangeBefore owner reserves

Salary onlyLaunch draw only

Salary plus distributionsReserve-backed

Salary plus strong distributionsScale upside

Best fit

Use this to stress-test the first 12 months and the cash gap before breakeven around Month 13.

Use this as the most likely operating case for a funded launch that reaches payback around Month 21.

Use this to test upside when the customer base is mature and repeat demand carries most of the growth.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

The planning case shows a modeled CEO salary of $185,000 in Year 1, but EBITDA is -$360,000, so profit distributions are not supported at launch By Year 2, EBITDA reaches $2213 million on $5375 million revenue Any owner draw should come after taxes, reserves, debt service, and reinvestment

The model reaches breakeven around Month 13 and payback around Month 21 That timing assumes Year 1 revenue of $1476 million, $450,000 in marketing, $85 CAC, and $745,000 of payroll If CAC rises or lab fulfillment slows repeat buying, breakeven can move later

Not in this model The cost structure assumes lab processing and kit materials as a percentage of revenue, starting at 120% in Year 1 and falling to 80% by Year 5 The owner still needs vendor controls, data privacy processes, quality review, customer support, and clear compliance oversight

CAC, repeat orders, lab costs, and practitioner labor move profit fastest CAC improves from $85 to $55 across the model, while repeat customers rise from 150% to 400% Registered dietitian staffing grows from 10 to 60 FTE, so consult workflow matters as much as pricing

Build repeat revenue before adding heavy payroll The model improves as repeat lifetime rises from 12 to 36 months and repeat orders grow from 050 to 100 per month Keep CAC below contribution margin, monitor $19,200 monthly fixed overhead, and set reserves before taking distributions

About the author

Nicholas Webb

Founder-Focused Content Writer

Nicholas Webb is a founder-focused content writer for Financial Models Lab who helps online business beginners make sense of business expense analysis and what it really costs to operate. He writes practical founder checklists and planning guides that support decisions before money is invested. With a calm, structured approach, he explains business costs clearly and without unnecessary jargon.

Choosing a selection results in a full page refresh.